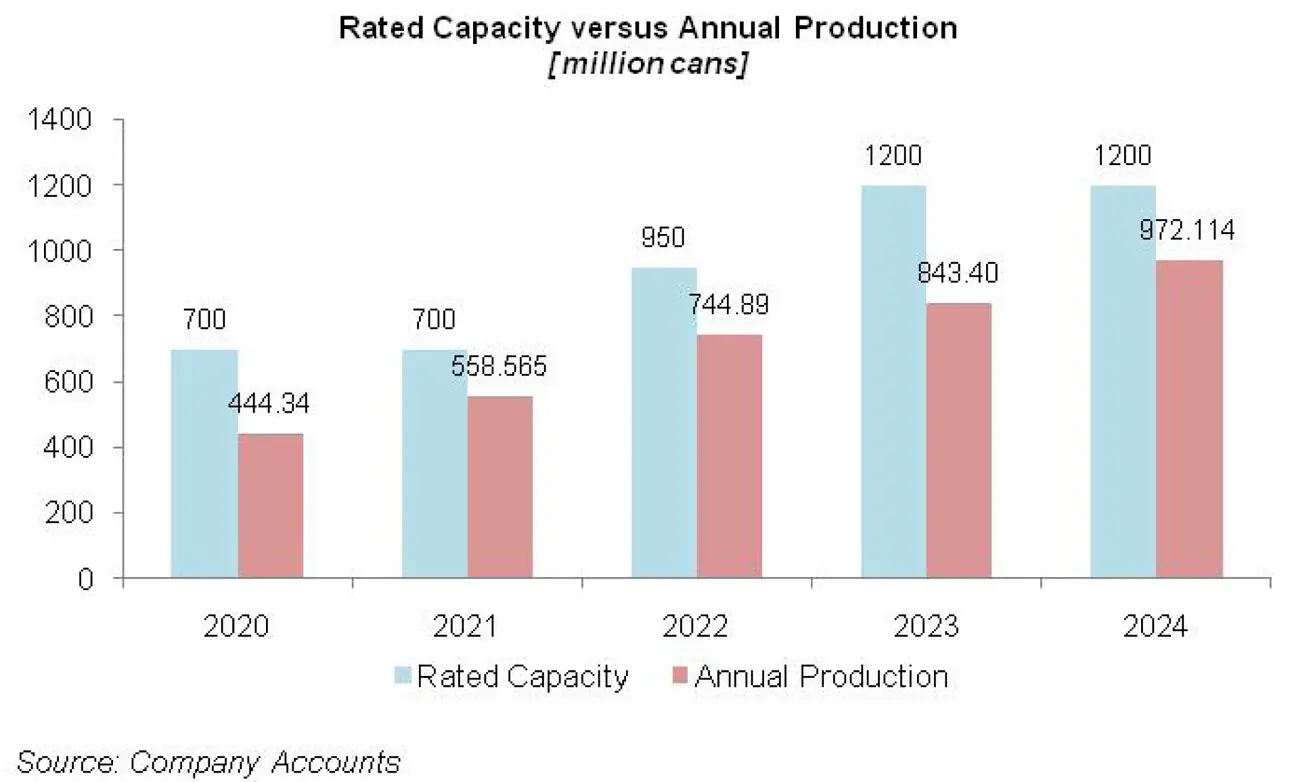

Pakistan Aluminum Beverage Cans Limited (PSX: PABC) was incorporated in Pakistan as a public unlisted company in 2014. It was listed on the stock exchange in 2021. The company is engaged in the manufacturing and sale of aluminum cans. The company began its commercial production in 2017 and by 2022; it had achieved yearly output of 950 million cans.

Pattern of Shareholding

As of December 31, 2024, PABC has a total of 361.108 million shares outstanding which are held by 2742 shareholders.

Sponsors, Directors, CEO, their spouse and minor children have the majority stake of 55.62 percent in the company followed by Soorty Enterprises (Private) Limited, an associated company of PABC holding 20 percent of shares.

Local general public accounts for 14.96 percent of the outstanding shares of PABC while Banks, DFIs and NBFIs hold 3.2 percent shares. The remaining ownership is distributed among other categories of shareholders.

Financial Performance (2020-24)

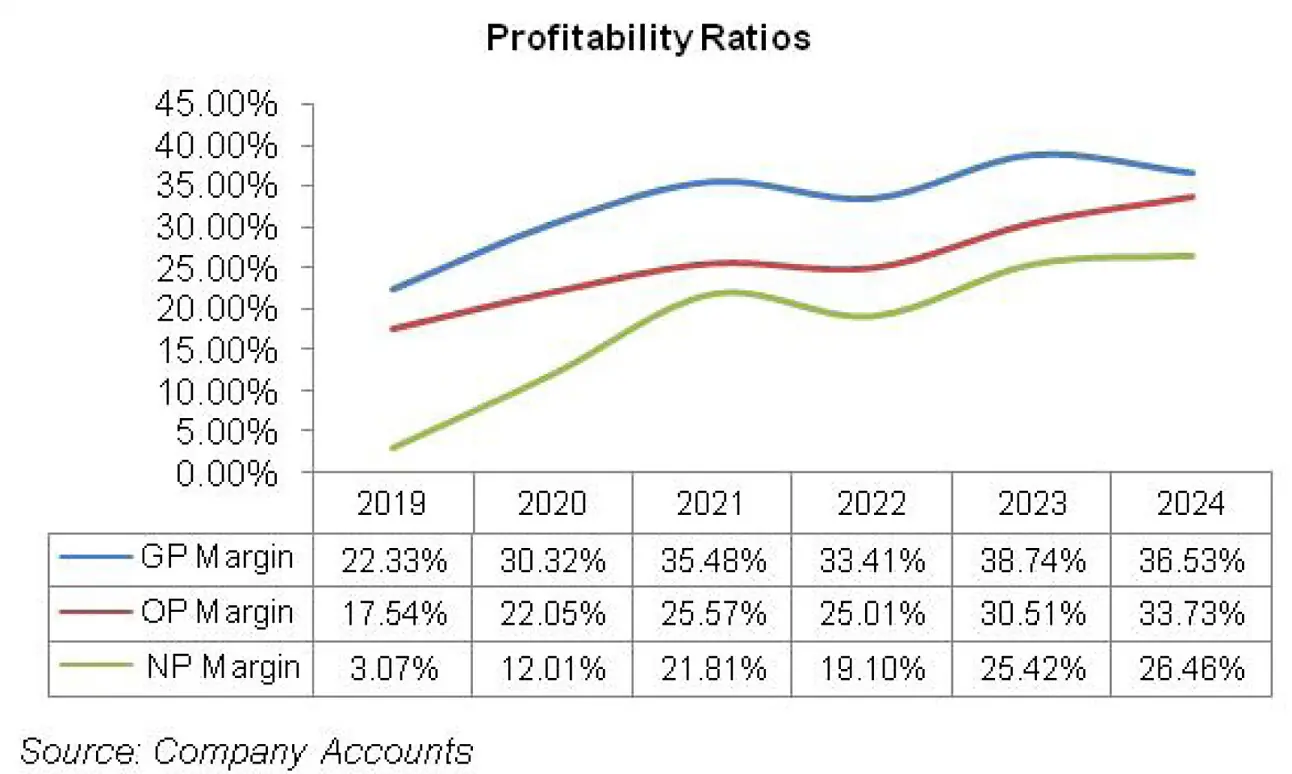

PABC’s topline and bottomline have made robust strides over the period under consideration. Its margins also rode a steep upward trajectory in 2020 and 2021 followed by a decline in the subsequent year.

In 2023, PABC margins posted a phenomenal growth. In 2024, gross margin plunged while operating and net margins continued to pick up. The detailed performance review of the period under consideration is given below.

In 2020, PABC’s topline grew by 5.72 percent year-on-year to clock in at Rs.5083.81 million. This was on account of improved sales volume as well as revised pricing strategy. PABC produced 444.34 million cans in 2020, up 6 percent year-on-year. This translated into capacity utilization of 63.5 percent in 2020 versus capacity utilization of 59.81 percent recorded in the previous year.

Cost of sales diminished by 5.16 percent in 2020 which was primarily the consequence of lower rent, rates and taxes as well as reduced travelling, conveyance & lodging charges on account of COVID-19.

This translated into 43.59 percent bigger gross profit in 2020 with GP margin rising up from 22.33 percent in 2019 to 30.32 percent in 2020. Administrative expense slid by 7.08 percent in 2020 on account of lower legal & professional charges, travelling charges as well as vehicle rentals. Lower freight charges incurred during the year resulted in 12.09 percent lower distribution expense in 2020.

Higher profit related provisioning, exchange loss and impairment loss inflated other expense by 739.57 percent in 2020. Conversely, other income slid by 71.54 percent in 2020 as exchange gain recorded in 2019 turned into exchange loss in 2020.

Operating profit mounted by 32.94 percent in 2020 with OP margin rising up to 22.05 percent from 17.54 percent in 2019. Finance cost slumped by 26.74 percent in 2020 due to monetary easing as well as significantly lower outstanding short-term borrowings at the end of the year.

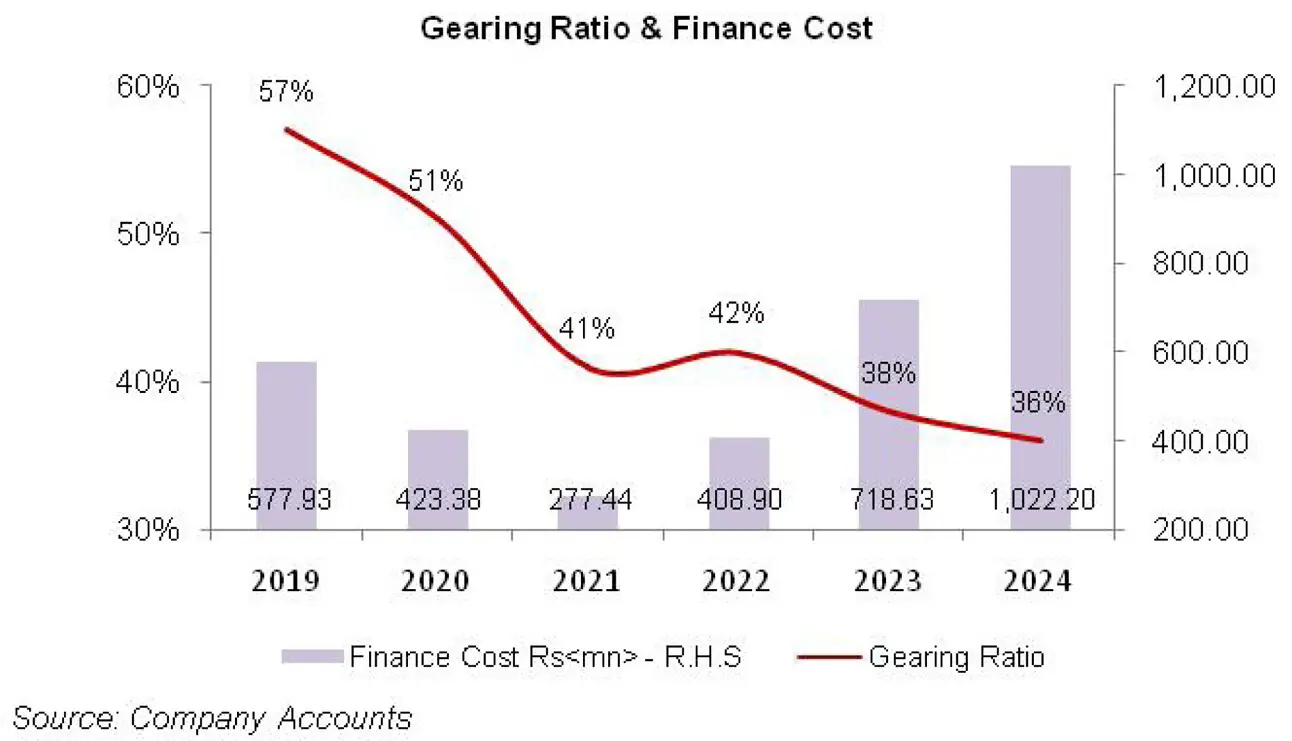

PABC’s gearing ratio declined from 57 percent in 2019 to 51 percent in 2020. Net profit enlarged by 314.09 percent in 2020 to clock in at Rs.610.655 million with EPS of Rs.1.69 versus EPS of Rs.0.45 reported in the previous year. NP margin also rose from 3.07 percent in 2019 to a whopping 12.01 percent in 2020.

In 2021, PABC’s topline climbed up by 42.21 percent to clock in at Rs.7229.92 million. This was on account of resumption of HORECA industry, educational institutions and offices resulting in improved demand of canned beverages during the year.

In accordance with the demand revival, the company produced 558.57 million cans in 2021, resulting in 79.8 percent capacity utilization. Improved sales volume - both in domestic and export markets - as well as upward revision in pricing resulted in 66.40 percent appreciation in PABC’s gross profit with GP margin jumping up to 35.48 percent in 2021.

Higher GP margin was also the result of the company’s efforts to reduce its cost of sales. One such effort was the installation of solar panels to curb the rising energy cost.

Administrative expense surged by 36.50 percent in 2021 which was the consequence of higher payroll expense as the number of employees increased from 123 in 2020 to 132 in 2021. Furthermore, higher utility expense as well as legal & professional charges also inflated the administrative expense during the year.

Distribution expense also multiplied by 23.11 percent in 2021 as a result of higher freight charges. Higher profit related provisioning, loss incurred on derivative instruments and expense on IPO drove up other expense by 161.66 percent in 2021.

Other income also amplified by 173.30 percent in 2021 on account of higher profit on TDRs and saving deposits as well as exchange gain recognized on the back of robust export sales. Operating profit rebounded by 64.89 percent in 2021 with OP margin clocking in at 25.57 percent. Finance cost shrank by 34.47 percent in 2021 due to lower discount rate. This was despite increased short-term borrowings particularly in the category of export refinance facility.

However, increase in the company’s equity resulted in lower gearing ratio of 41 percent in 2021. Net profit climbed up by 158.18 percent in 2021 to clock in at Rs.1576.587 million with EPS of Rs.4.37. NP margin also progressed to 21.81 percent in 2021.

In 2022, PABC’s topline boasted a staggering 95.76 percent growth to clock in at Rs.14,152.97 million. This was the result of improved sales volume as the company expanded in both domestic and international markets.

During the year, the company’s production capacity was enhanced to 950 million cans. Production volume stood at 744.89 million cans in 2022, up 33 percent year-on-year. This culminated into capacity utilization of 78.41 percent in 2022.

Cost of sales surged by 102.04 percent in 2022 due to rising commodity prices in the consequence of Russia-Ukraine crisis as well as Pak Rupee depreciation.

Higher cost couldn’t be fully reflected in PABC’s product pricing, resulting in GP margin inching down to 33.41 percent in 2022. In absolute terms, gross profit enhanced by 84.33 percent in 2022. Administrative expense registered 66.52 percent spike in 2022 on account of higher payroll expense as workforce was expanded by 30 employees during the year which took the tally to 162.

Higher utility expense also contributed in driving up administrative expense in 2022. Distribution expense hiked by a whopping 377.81 percent in 2022 which was primarily the consequence of amplified freight & other logistics charges. Higher profit related provisioning, exchange loss and provision for slow moving stores & spares drove up other expense by 22.37 percent in 2022.

Conversely, other income strengthened by 380.15 percent in 2022 on the back of higher interest income as well as insurance claim received during the year. Operating profit picked up by 91.49 percent in 2022, however, OP margin slightly eroded to clock in at 25.01 percent.

Higher discount rate inflated finance cost by 47.38 percent in 2022. PABC operated in Faisalabad special economic zone and hence was exempted from taxation on the basis of minimum tax liability for ten years from the start of its commercial operations.

However, during the year, the exemption was withdrawn through Finance Act, 2022. This resulted in a steep 7922.48 percent spike in PABC’s tax expense during the year. This diluted the bottomline growth recorded by the company in 2022. PABC net profit grew by 71.42 percent in 2022 to clock in at Rs.2702.612 million with EPS of Rs.7.48 and NP margin of 19.10 percent.

PABC ended 2023 on a vigorous note with 39.45 percent year-on-year growth in its topline which clocked in at Rs.19,735.90 million. This came on the back of tremendously higher export sales as well as Pak Rupee depreciation.

Conversely, local sales struggled during the year as inflationary pressure resulted in reduced consumption of canned beverages. Export sales constituted 59.55 percent of PABC’s overall net sales mix in 2023 versus its share of 42.32 percent in the net sales in the previous year.

In line with robust demand from export market, PABC not only enhanced its rated capacity to 1200 million cans in 2023 but also increased its annual production by 13.23 percent to clock in at 843.40 million cans. This resulted in capacity utilization of 70.28 percent in 2023. The change in sales mix resulted in PABC’s GP margin reaching its highest level of 38.74 percent in 2023.

In absolute terms, gross profit strengthened by 61.70 percent in 2023. Unprecedented level of inflation as well as workforce expansion to 204 employees resulted in elevated payroll expense which drove up administrative expense by 61.1 percent in 2023. Distribution expense registered 55.1 percent spike in 2023 due to improved export volumes which culminated into higher freight charges, export surcharges & commission and other logistics charges.

Other expense mounted by 31.54 percent year-on-year in 2023 on account of higher profit related provisioning, exchange loss and generous donations. Other income improved by 106.34 percent in 2023 due to higher interest income.

All these factors translated into 70.11 percent bigger operating profit in 2023 with OP margin of 30.51 percent. Finance cost spiraled by 75.75 percent in 2023 on account of higher discount rate and increased short-term borrowings.

However, gearing ratio slid to 38 percent on account of higher un-appropriated profits which drove up the equity. Net profit rose by 85.67 percent year-on-year to clock in at Rs.5017.836 million in 2023 with EPS of Rs.13.9 and NP margin of 25.42 percent.

In 2024, PABC’s topline picked up by 16.88 percent to clock in at Rs.23,067.77 million. This was on account of improved sales volume of cans coupled with upward revision in prices. During the year, the company produced 972.11 million cans, up 15.26 percent year-on-year. This translated into capacity utilization of 81.01 percent in 2024.

Cost of sales surged by 21 percent in 2024 on the back of supply chain disruptions, border closures, heightened energy tariff and elevated commodity prices.

Gross profit ticked up by 10.24 percent in 2024, however, GP margin inched down to 36.53 percent. Administrative expense posted a marginal growth of 7.75 percent in 2024 on the back of higher payroll expense as the company expanded its workforce from 204 employees in 2023 to 240 employees in 2024.

Distribution expense surged by 101.44 percent in 2024 particularly on account of higher export commission, marketing expenses as well as freight & other logistics charges incurred during the year.

Export sales constituted 62.66 percent of the total sales of PABC in 2024 versus its contribution of 59.55 percent in the sales mix in the previous year. No exchange loss, donations and ECL on trade debts in 2024 resulted in 13.50 percent downtick in other expense. Conversely, other income strengthened by 376.79 percent in 2024 and unlike previous years, it outweighed other expense.

Superior other income was the result of dividend income from mutual funds, unrealized gain recorded on the re-measurement of investments in mutual funds and capital gain on mutual funds. Besides, improved profitability on bank deposits due to higher discount rate also pushed up other income in 2024.

PABC recorded 29.21 percent higher operating profit in 2024 with OP margin attaining its optimum level of 33.73 percent. Finance cost escalated by 42.24 percent in 2024 due to higher discount rate and increased short-term borrowings. However, increased un-appropriated profit resulted in higher equity which pushed down gearing ratio to 36 percent in 2024.

Tax expense surged by 129.30 percent in 2024 as the company’s export income is now being treated under normal tax regime instead of presumptive tax regime. Net profit improved by 21.65 percent to clock in at Rs.6104.198 million in 2024. This translated into EPS of Rs.16.9 and NP margin of 26.46 percent in 2024.

Recent Performance (1HCY25)

During the first half of CY25, PABC recorded year-on-year growth of 15.42 percent in its net sales which clocked in at Rs.13,544.29 million. This mainly came on the back of 22.25 percent growth recorded in local sales during the period. Despite border closures, export sales also ticked up by 11 percent in 1HCY25.

Export sales constituted 58.44 percent of the company’s total sales in 1HCY25 versus its share of 60.76 percent in 1HCY24. Cost of sales surged by 19.55 percent in 1HCY25 due to the withdrawal of aluminum coil rebate by the Chinese government.

The effect of this cost hike could not be passed on to the customers, resulting in GP margin dipping from 37.15 percent in 1HCY24 to 34.90 percent in 1HCY25. In absolute terms, gross profit ticked up by 8.42 percent in 1HCY25. Improved sales volume resulted in 97.21 percent higher distribution expense in 1HCY25.

Administrative expense also surged by 19.94 percent during the period as the company enhanced its production capacity to 1300 million cans which required additional human resources. Higher profit related provisioning appears to be the cause of 21.65 percent higher other expense recorded in 1HCY25.

However, it was conveniently offset by 42.26 percent stronger other income recognized during the period which was the result of the company’s prudent investment decisions. Operating profit inched up by 5.1 percent in 1HCY25 with OP margin clocking in at 32 percent versus OP margin of 35.14 percent recorded in 1HCY24.

Finance cost plunged by 21.72 percent in 1HCY25 due to monetary easing. PABC recorded 40.75 percent higher net profit to the tune of Rs.3891.205 million in 1HCY25. This translated into EPS of Rs.10.78 in 1HCY25 versus EPS of Rs.7.66 recorded in 1HCY24. NP margin improved from 23.56 percent in 1HCY24 to 28.73 percent in 1HCY25.

Future Outlook

Currently, Afghanistan is the largest export market of PABC; however, recurring tensions at Afghan border and growing production capacity in the Central Asia can take its toll on the company’s export sales. With new targeted geographical markets, the company can diversify its export sales.

The company can also target new players in the local market to boost its local sales. Lately, the local market is showing stability which also serves as a positive omen to enhance local sales.

The company is also focusing on improving its operational efficiency and strengthening partnership with suppliers to mitigate cost pressure and ensure superior financial performance.

Comments

Comments are closed for this article.