Ferozsons Laboratories Limited was incorporated in Pakistan as a public limited company in 1954. It was converted into a public limited company in 1960. The principal activity of the company is the manufacturing, importing and sale of pharmaceutical products and medical devices.

Pattern of Shareholding

As of June 30, 2024, FEROZ has a total of 43.469 million shares outstanding which are held by 4196 shareholders. Associated companies, undertakings and related parties have the majority stake of 37.36 percent in FEROZ followed by local general public holding 24.37 percent shares.

Around 10.41 percent of the company’s shares are held by its Directors, CEO, their spouse and minor childrenand 10.39 percent by insurance companies. Modarabas & Mutual Funds account for 7.89 percent shares of FEROZ while NIT & ICP hold 4.31 percent shares. Other local companies hold 3.49 percent shares while foreign general public hold 1.24 percent shares of FEROZ. The remaining shares are held by other categories of shareholders.

Historical Performance (2019-24)

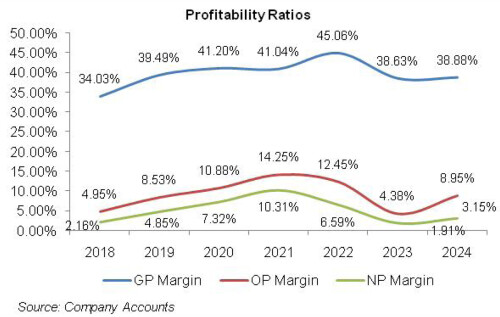

FEROZ’s topline rode an upward trajectory over the period under consideration. Its bottomline also strengthened until 2021 followed by a dip in 2022 and 2023. In 2024, FEROZ’s net profit registered staggering growth. The company’s margins registered sound growth until 2020. In 2021, gross margin slightly fell, however, operating and net margins continued to enlarge. This was followed by gross margin attaining its optimum level in 2022 while operating and net margins slid. All the margins posted drastic decline in 2023 followed by an uptick in 2024. The detailed performance review of the period under consideration is given below.

In 2019, FEROZ’s net sales grew by 17.5 percent year-on-year to clock in at Rs.5180.804 million. The company’s imported line of products as well as branded generic product portfolio did exceptionally well during the year while institutional sales dwindled due to lower public sector health procurement. In 2018, institutional sales pertaining to Hepatitis C boosted institutional sales.

Lesser contribution of institutional sales in the overall sales mix in 2019 coupled with lesser diminution in net realizable value of stock of Sovaldi resulted in an improved GP margin of 39.49 percent in 2019 versus GP margin of 34 percent recorded in the previous year. In absolute terms, gross profit strengthened by 36.37 percent in 2019. Distribution expense multiplied by 23.91 percent in 2019 on account of field force and branding expense incurred during the year to expand the company’s market base.

Administrative expense also surged by 16.52 percent in 2019 particularly on the back of higher payroll expense as workforce was enlarged from 945 employees in 2018 to 1056 employees in 2019. 141.76 percent higher other expense incurred during the year was the consequence of hefty exchange loss, higher profit related provisioning and unrealized loss incurred on the re-measurement of short-term investments in 2019.

Other expense was conveniently offset by 41.29 percent higher other income recorded in 2019. Stronger other income was the result of commission income, dividend income as well as gain on sale of operating fixed assets during the year. Operating profit grew by 102.53 percent in 2019 with OP margin clocking in at 8.53 percent versus OP margin of 4.95 percent recorded in 2018.

Finance cost surged by 112 percent in 2019 due to higher discount rate. Net profit enhanced by 163.13 percent in 2019 to clock in at Rs.251.046 million with EPS of Rs.8.32 versus EPS of Rs.3.16 recorded in 2018. NP margin also ticked up from 2.16 percent in 2018 to 4.85 percent in 2019.

In 2020, FEROZ recorded 4.26 percent year-on-year uptick in its net sales which clocked in at Rs.5401.732 million. While the company’s generic sales grew by 11 percent during the year, institutional sales recorded 40 percent decline as the provincial governments used their healthcare budgets in COVID-19 relief packages. Lesser institutional sales further improved FEROZ’s GP margin to 41.20 percent in 2020 with gross profitability improving by 8.79 percent year-on-year.

Distribution expense tapered off by 1.5 percent in 2020 as the company had to either cancel or postpone its advertising and promotion activities during the year due to COVID-19. Administrative expense inched down by 0.5 percent in 2020 due to slight drop in payroll expense.

While the company booked greater provisioning for WWF and WPPF and also booked provisioning for loss allowance during the year, considerably lower exchange loss resulted in 27.20 percent lesser other expense in 2020. Other income also slumped by 48.94 percent in 2020 mainly because FEROZ didn’t record any commission income. Operating profit picked up by 32.91 percent in 2020 with OP margin climbing up to 10.88 percent.

Finance cost magnified by 15.81 percent in 2020 as the company acquired long-term loan under SBP Refinance Scheme for the payment of salaries & wages. The company also obtained short-term borrowings to meet working capital requirements during the year. Net profit recorded 57.60 percent rise year-on-year in 2020 to clock in at Rs.395.655 million with EPS of Rs.10.92 and NP margin of 7.32 percent.

FEROZ’s topline mounted by 30.21 percent in 2021 to clock in at Rs.7033.622 million. In-market generic sales and institutional sales improved by 18 percent and 49 percent respectively in 2021. Export sales also rose by 49 percent during the year. Higher raw material and conversion charges coupled with the variation in the sales mix resulted in slight downtick in GP margin which was recorded at 41 percent in 2021.

In absolute terms, gross profit increased by 29.71 percent in 2021. As travelling restrictions were eased during the year, the company could plan its field promotional activities. This resulted in 18.21 percent higher distribution expense in 2021. FEROZ also expanded its workforce from 1059 employees in 2020 to 1127 employees in 2021 which resulted in higher payroll expense. Consequently, administrative expense surged by 16 percent in 2021.

Net effect of no exchange loss and higher provisioning for WWF, WPPF and CRF resulted in 0.93 percent downtick in other expense in 2021. 47.48 percent higher other income was the result of exchange gain, commission income as well as higher gain recorded on sale of property, plant & equipment in 2021. Operating profit multiplied by 70.61 percent in 2021 with OP margin picking up to 14.25 percent – the highest during the period under consideration.

Finance cost tumbled by 19.88 percent in 2021 due to the onset of monetary easing cycle since 4QFY20. Net profit progressed by 83.30 percent to clock in at Rs.725.235 million in 2021 with EPS of Rs.20.02 and NP margin attaining its highest level of 10.31 percent.

In 2022, FEROZ’s net sales improved by 11 percent to clock in at Rs.7806.414 million. Unlike last year, institutional sales registered a decline of 1 percent in 2022, while in-market generic sales continued to pick up, posting 20 percent year-on-year rise. The company’s stock was valued at historical average exchange rate with no integration of Pak Rupee depreciation during the year.

This coupled with change in sales mix resulted in 21.85 percent improved gross profit in 2022 with GP margin attaining its highest level of 45 percent. 29.26 percent higher distribution expense incurred in 2022 came on the back of increased promotion and advertising activities to increase market penetration.

Workforce expansion undertaken during the year took the headcount to 1366 employees in 2022. This resulted in higher salaries expense which together with elevated travelling & conveyance charges drove administrative expense up by 20.65 percent in 2022. Other expense registered a whopping 199.32 percent year-on-year hike in 2022 due to hefty exchange loss incurred during the year.

Unlike previous years, other income couldn’t offset other expense in 2022 despite posting 33.71 percent year-on-year rise. Higher other income was the result of robust dividend income, reversal of loss allowance and higher share in profit of Farmacia – 98 percent owned partnership firm of FEROZ. Operating profit thinned down by 3 percent in 2022 with OP margin falling down to 12.45 percent.

Finance cost escalated by 72 percent in 2022 due to higher discount rate and increased short-term borrowings to meet working capital requirements. FEROZ’s net profit descended by 29.11 percent in 2022 to clock in at Rs.514.149 million with EPS of Rs.11.83 and NP margin of 6.59 percent.

In 2023, FEROZ recorded 26.73 percent enhancement in its net sales which stood at Rs. 9893.39 million. This was backed by 14 percent growth in in-market generic sales, 43 percent growth in institutional sales as well as 98 percent growth in export sales over the previous year. Change in sales mix in favor of institutional sales coupled with increase in raw material cost,

Pak Rupee depreciation and unprecedented level of inflation translation into a thinner GP margin of 38.63 percent in 2023. Gross profit inched up by 8.66 percent in absolute terms in 2023. Inflationary impact, higher fuel prices and increased travelling and salaries expense resulted in 24.12 percent spike in distribution expense in 2023.

Administrative expense also mounted by 24.36 percent in 2023 due to heightened payroll expense, travelling expense, fuel & power and canteen expenses incurred during the year. Number of employees increased to 1388 in 2023 from 1366 in 2022. Other expense magnified by 100.14 percent in 2023 due to sharp increase in exchange loss on account of Pak Rupee depreciation as well as hefty loss allowance against trade debt and earnest money booked during the year.

Other income inched up by 10.26 percent in 2023 due to higher dividend income, commission income and share in profit of Farmacia recorded during the year. FEROZ’s operating profit dwindled by 55.38 percent in 2023 with OP margin falling to its lowest level of 4.38 percent. Finance cost surged by 323.36 percent in 2023 due to elevated discount rate and increased short-term and long-term borrowings obtained during the year. Net profit declined by 63.23 percent to clock in at Rs.189.043 million in 2023 with EPS of Rs.4.35 and the lowest NP margin of 1.91 percent.

FEROZ’s net sales grew by 28.49 percent to clock in at Rs.12,711.714 million in 2024. This was due to 31 percent increase in in-market generic sales and 27 percent increase in institutional sales during the year. During the year, the topline growth was solely supported by an increase in sales volume while prices stayed intact at lastyear’s level. Cost of sales surged by 28 percent due to inflationary pressure as well as Pak Rupee depreciation. Gross profit improved by 29.30 percent in 2024 with GP margin slightly ticking up to 38.88 percent.

Distribution expense surged by 24.58 percent in 2024 due to higher sales volume coupled with inflationary effect which pushed up the salaries of sales force, travelling & conveyance expense as well as sales promotion expense. Administrative expense also escalated by 27.41 percent in 2024 due to higher payroll expense. Number of employees grew to 1485 in 2024. Other expense fell by 65.82 percent in 2024 due to no exchange loss incurred on account of relatively stable value of local currency since 2QFY24.

Other income grew by 1.32 percent in 2024. This was because the impact of hefty exchange gain, gain on sale of fixed assets as well as unrealized gain onre-measurement of short-term investment to fair value was offset by thinner dividend income and share in profit of Farmacia. Operating profit strengthened by 162.30 percent in 2024 with OP margin climbing up to 8.95 percent.

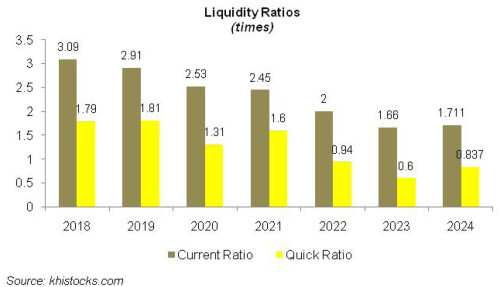

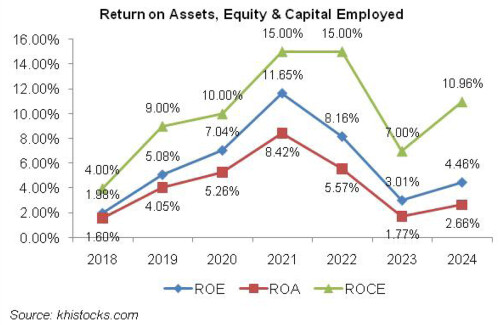

Finance cost multiplied by 233 percent in 2024 due to high discount rate coupled with higher long-term loan and increased utilization of working capital lines. FEROZ’s gearing ratio surged from 12.72 percent in 2023 to 23.52 percent in 2024. Net profit improved by 111.62 percent to clock in at Rs.400.054 million in 2024. This culminated in EPS of Rs.9.20 and NP margin of 3.15 percent in 2024.

Recent Performance (9MFY25)

During 9MFY25, FEROZ’s net sales ticked up by 13.10 percent to clock in at Rs.10,811.374 million. While in-market generic sales posted 26 percent rise during the period, the supply of medical devices during 9MFY24 resulted in 8 percent decline in institutional sales in 9MFY25. The change in sales mix coupled with the increase in prices resulted in 18 percent stronger gross profit in 9MFY25 with GP margin clocking in at 39.68 percent versus GP margin of 38.014 percent recorded in 9MFY24. Distribution expense and administrative expense escalated by 16 percent and 8.74 percent respectively during the period under review on account of inflationary pressure. Lower exchange loss appears to be the driver of 30.87 percent thinner other expense in 9MFY25. Other income also dwindled by 17.86 percent during the period, seemingly due to lower profit from bank deposits on account of monetary easing. FEROZ recorded 32.93 percent higher operating profit in 9MFY25 with OP margin clocking in at 9.20 percent versus OP margin of 7.83 percent recorded in 9MFY24. Finance cost ticked up by 3.46 percent in 9MFY25 due to monetary easing and a plunge in short-term borrowings. The change in tax regime for export sales by the federal government resulted in effective tax rate of 39 percent in 9MFY25 versus effective tax rate of 33 percent in 9MFY24. Net profit improved by 44.41 percent to clock in at Rs.390.442 million in 9MFY25. This translated into EPS of Rs.8.98 in 9MFY25 versus EPS of Rs.6.22 in 9MFY24. NP margin also picked up from 2.83 percent in 9MFY24 to 3.61 percent in 9MFY25.

Future Outlook

Increase in institutional sales may increase the sales volume and add to the topline of FEROZ, however, it is drastically squeezing its margins amid high raw material and conversion cost. Moreover, institutional sales are also driving up the outstanding receivables of the company, resulting in increased booking of loss allowance. This also creates liquidity constraints for the company resulting in the utilization of external financing lines. To offset the negative impact of institutional sales on its financial performance, FEROOZ is venturing into new geographical markets and introducing market relevant products that can add diversity to its revenue lines and shield its margins from contraction.

Comments

Comments are closed for this article.