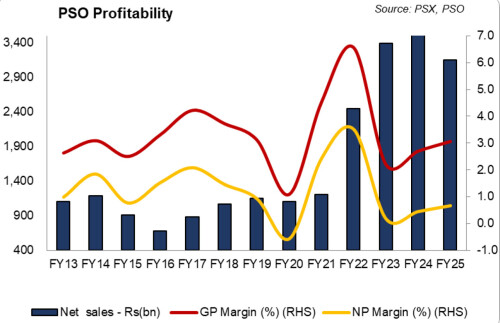

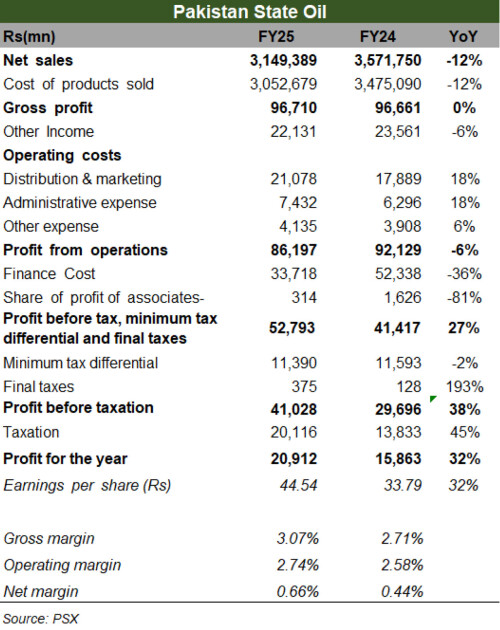

Pakistan State Oil (PSX: PSO) closed FY25 with earnings up 32 percent to Rs21 billion in FY25. This improvement in the bottom line came despite a decline in revenues, as net sales contracted 12 percent to Rs3.15 trillion against Rs3.57 trillion in the previous year. The contraction was largely attributed to a fall in petroleum product prices coupled with lower sales volumes, with motor spirit and high-speed diesel volumes slipping 4 percent and 5 percent year on year, respectively, while furnace oil volumes dropped sharply by 47 percent. On the other hand, the RLNG business provided some stability as PSO handled over 110 cargoes during the year.

Despite topline pressures, PSO managed to improve gross margins to 3.1 percent in FY25 from 2.7 percent a year earlier, primarily due to reduced inventory losses. In the fourth quarter, however, margins eased to 2.9 percent compared to 3.2 percent in the prior quarter as inventory losses resurfaced. Finance costs were a major source of relief, falling 36 percent year on year, as the company benefitted from lower interest rates and reduced borrowings.

The tax burden, however, remained heavy, with an effective tax rate of about 60 percent in FY25 compared to 62 percent in FY24. In the last quarter alone, the effective tax rate reached 61 percent, continuing to weigh down the net margin, which stood at 0.7 percent for the year versus 0.4 percent previously. PSO maintained a dividend payout of Rs 10 per share, in line with FY24, implying a payout ratio of 22 percent. On the balance sheet side, trade debts improved to Rs 437 billion at the end of June 2025 reflecting stronger collections.

Overall, PSO’s FY25 performance underscored a recovery in earnings despite subdued operational momentum. The company delivered higher profits lower borrowing costs, and reduced inventory losses, even as revenues fell due to weaker product prices and volumes. With structural decline in furnace oil consumption and continued taxation pressures, PSO still faces headwinds.

Yet, improved liquidity, better collections, and tighter debt management have placed the company on firmer ground, with future performance hinging on sustaining these financial efficiencies, managing inventory risks in volatile oil markets, and addressing the long-standing challenges of receivables and circular debt.

Comments

Comments are closed for this article.