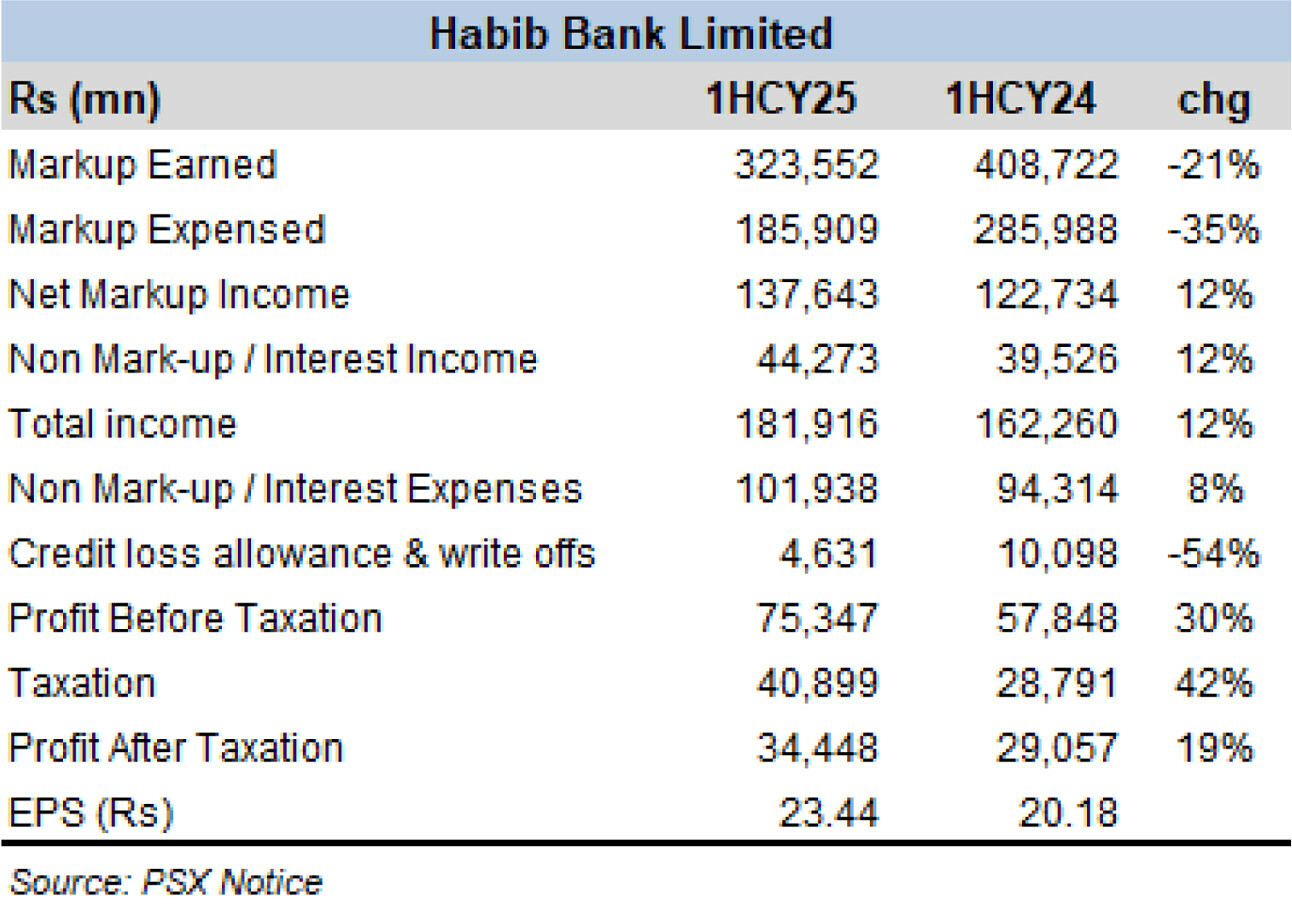

HBL in 1HCY25 did what it has been accustomed to for some time: deliver solid profits and dividends. The economic realities keep changing, and the largest commercial bank tunes itself to keep raking in profits. Interest rates high or low, advances up or down – HBL finds a way, and that is all it did during the half year ending June 2025.

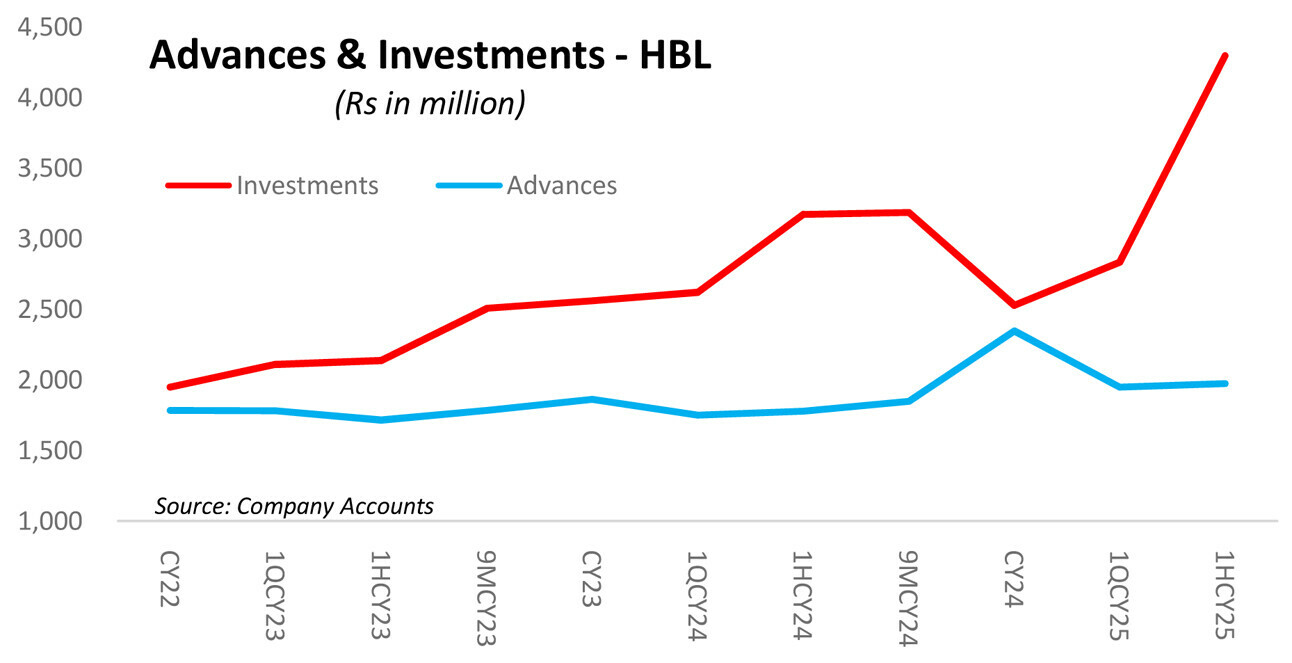

The balance sheet growth remained phenomenal – up a massive 26 percent over December 2024. On the asset front, re-composition continued, as investments continue to be the favored parking spot. HBL’s investment portfolio shot up to a colossal Rs4.3 trillion – adding a whopping Rs1.8 trillion since December 2024.

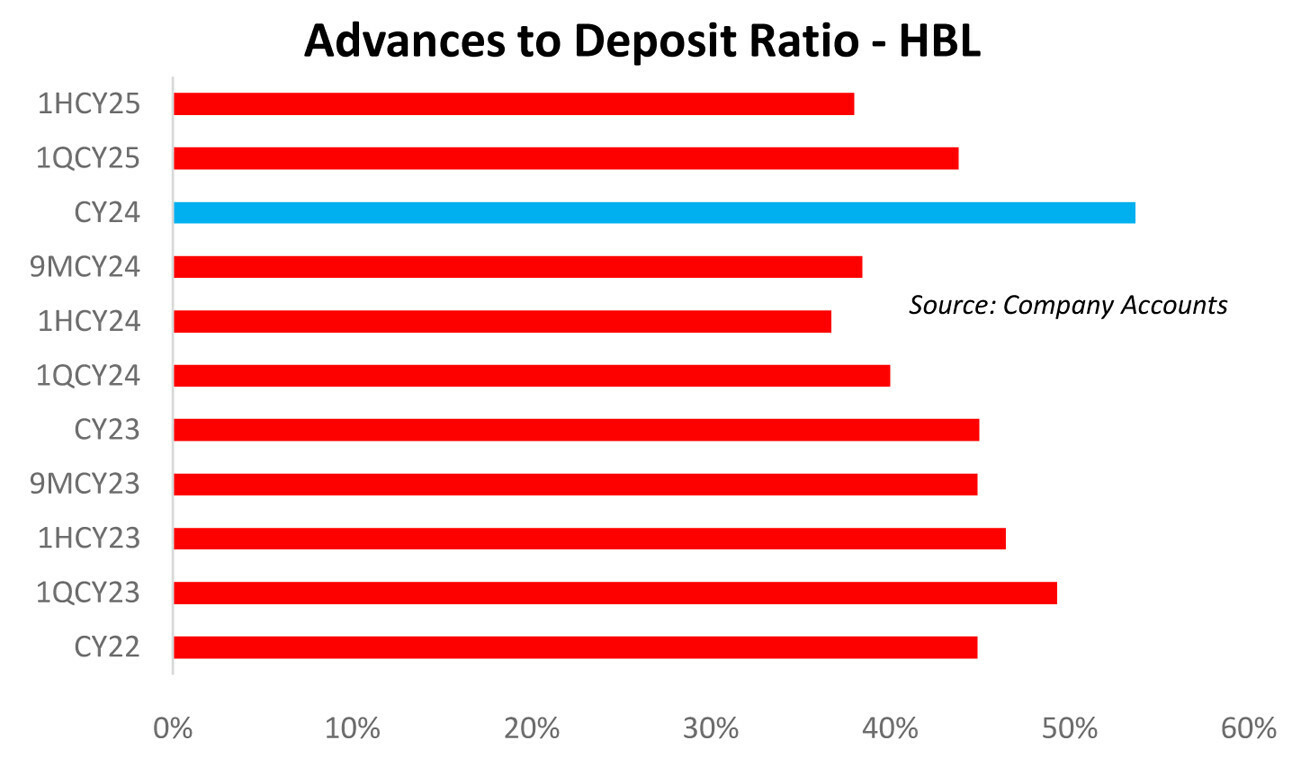

The investments-to-deposit ratio stood at a jaw-dropping 83 percent. It is a massive 70 percent — yes, seventy — increase over December-end 2024, growing at a never-before-seen rate, as against industry growth of 21 percent (ex-HBL). HBL’s investment portfolio growth accounted for nearly a quarter of the sectoral growth of Rs7.4 trillion over December 2024.

There has not been much going on the advances front in CY25 thus far. The industry advances stock is down 15 percent over December 2024 and almost unchanged from the end of 1QCY25.

HBL’s advances portfolio followed the sectoral trend, shedding nearly 16 percent over December 2024. Macroeconomic indicators may well have visibly improved and interest rates substantially down from a year ago – nothing seems to have reignited the credit appetite as such.

Whether banks shy away from lending or there is a genuine lack of credit demand is never fully known – but the pace of turnaround of the economic engine suggests nobody is in a rush for more bank loans. The SME and agriculture sectors keep getting highlighted, but the growth remains negligible.

Meanwhile, money supply is growing like there is no tomorrow. Banking sector total deposits soared 17 percent over December 2024. This is the sharpest increase in banking system deposits for any December-to-June period since at least 2002.

The 20-year average deposit growth for the period is 9 percent. June is typically the month that sees the highest month-on-month increase in deposits – and 2025 saw deposits grow 9 percent month-on-month – only behind June 2021 – in the last 23 years.

What HBL could not finance from deposits, it did from borrowings that nearly doubled over December 2024. Repurchase borrowings went up 2.5x to Rs1.2 trillion.

HBL’s own deposit book growth was largely in line with industry trends – growing 19 percent over December 2024. Current deposits constituted over 50 percent of total growth and now constitute over 40 percent of total deposits. Better deposit mix and reduced markup rates led to a substantial 578 basis points dip in cost of deposits.

Non-markup income stayed strong thanks to timely realization of capital gains. Costs were kept in check, leading to an improved cost-to-deposit ratio of 55 percent – down from 57 percent in the same period last year. Infection ratio and coverage ratio read healthy readings at 5 and 90 percent, respectively.

The push for advances may only happen in the final quarter, as has been the case since the introduction of penal tax on ADR thresholds. Nobody is complaining. The profits keep on coming.

Comments

Comments are closed for this article.