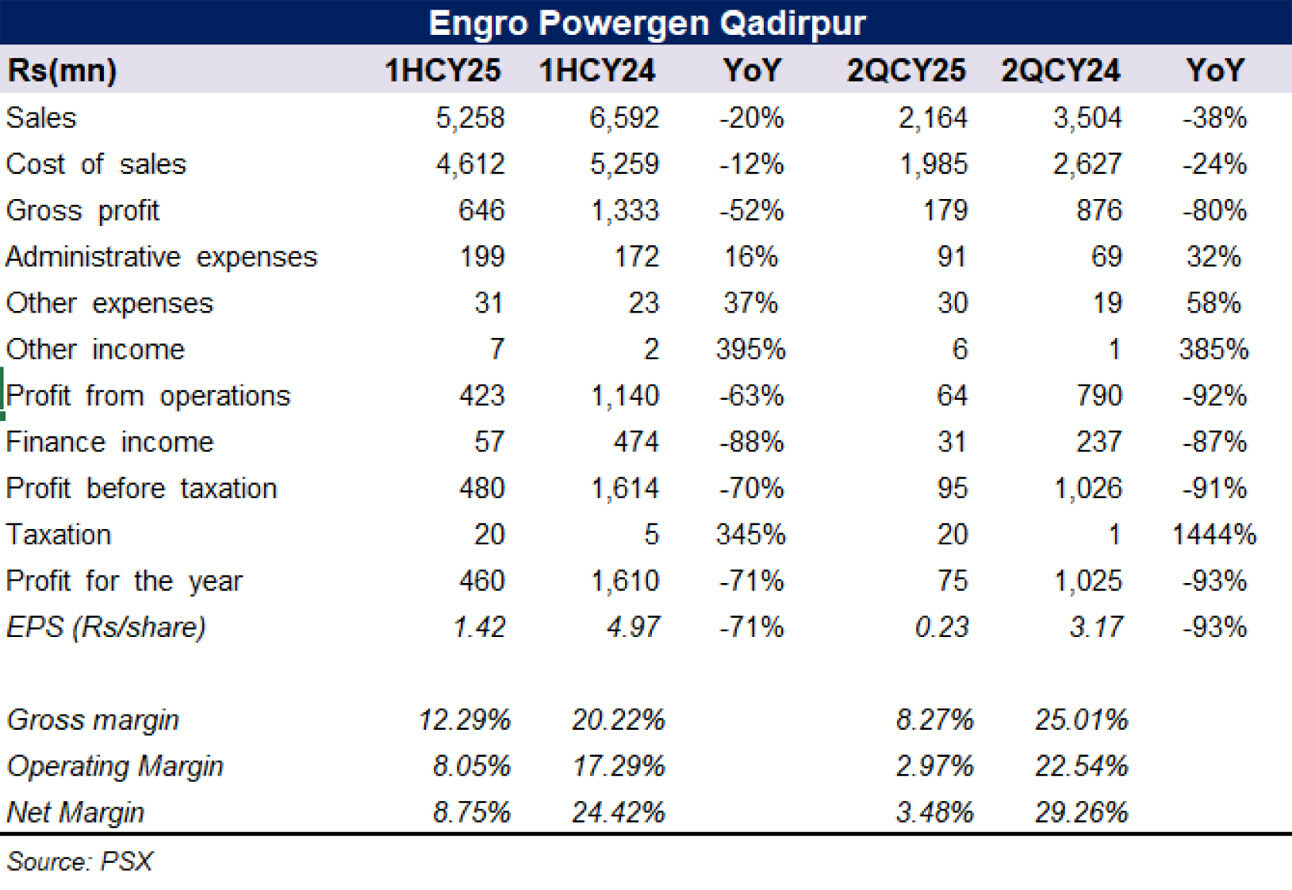

Engro Powergen Qadirpur’s (PSX EPQL) financial performance in the first half of CY25 reflects the structural impact of the shift to the Hybrid Take and Pay model and lower plant utilization levels.

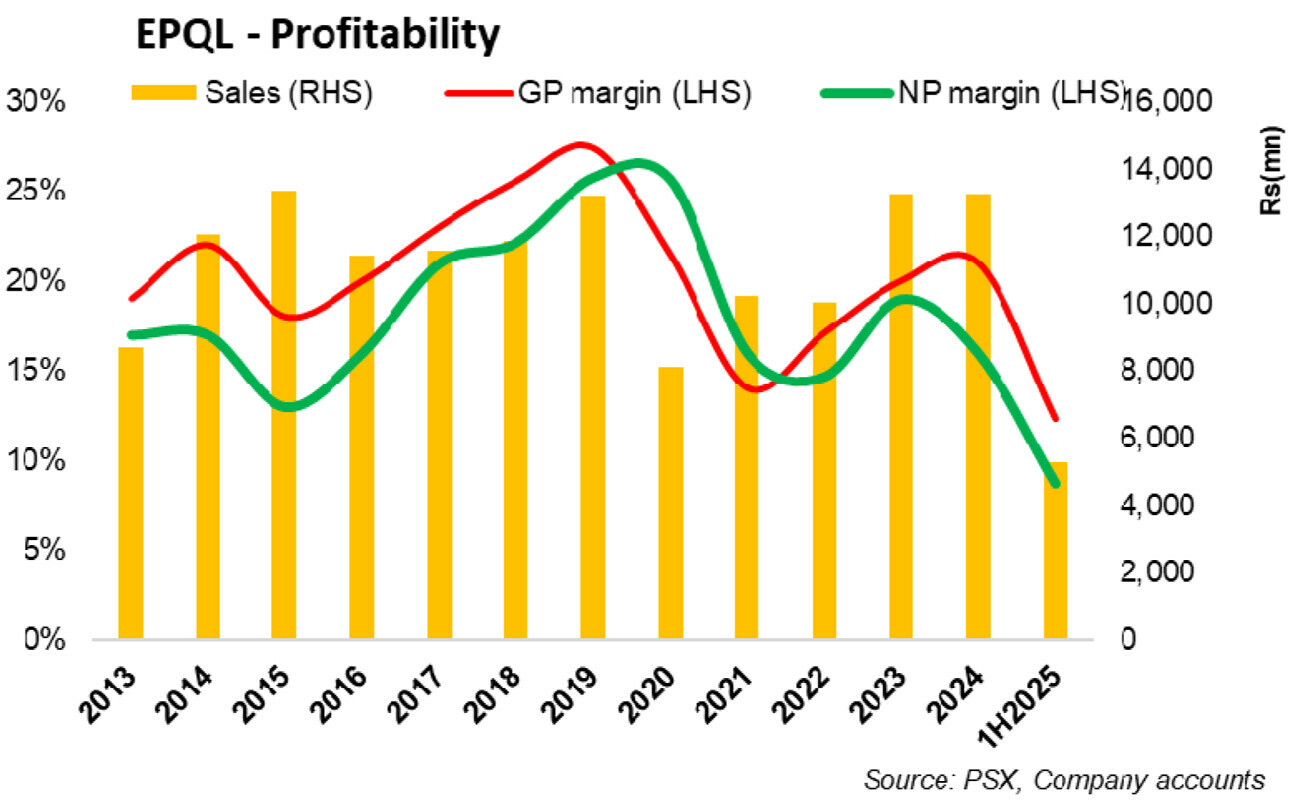

Net sales fell 20 percent year-on-year to Rs5.26 billion, primarily due to a reduced period weighting factor and subdued dispatch levels. Gross profit halved during 1HCY25, with the gross margin contracting to 12.3 percent from 20.2 percent a year earlier, underscoring the squeeze on operational profitability.

Operating profit declined 63 percent year-on-year, while administrative expenses increased 16 percent year-on-year, further eroding operating leverage.

Finance income also fell sharply (88% YoY)) because of the settlement of overdue receivables and the waiver of late payment surcharges agreed under the amended power purchase arrangement.

Consequently, net profit dropped 71 percent year-on-year. The second quarter was particularly weakas plant utilization fell to 31.8 percent from 46.7 percent in 2QCY24 and gross profit slid 80 percent year-on-year.

Despite weaker earnings, EPQL announced cash dividends of Rs 7.5/share in Q1 and Rs 2.5/share in Q2, which was likely due to the one-off settlement of outstanding receivables. This payout, alongside a reduction in short-term debt from Rs5.9 billion in 1QCY25 to Rs 1.8 billion in 2QCY25 reflects a stronger liquidity position despite operational headwinds.

Strategically, EPQL is focusing on fuel security. The company has reportedly highlighted that a 10-month delay in regulatory approval for gas supply from a field resulted in additional costs and forex outflows. As a result, the company has sought urgent government support to enable the use of indigenous low-BTU gas from the field to mitigate the risk of declining Qadirpur gas supplies and reduce dependence on costly alternatives.

EPQL’s near-term outlook hinges on two key variables: fuel security and the operational impact of the Hybrid Take and Pay model. The transition away from the legacy take-or-pay tariff framework has structurally reduced guaranteed earnings, making plant utilization and fuel efficiency critical to profitability.

With Qadirpur gas supplies on a declining trajectory, the company’s ability to secure indigenous low-BTU gas and obtain timely regulatory approvals will be central to stabilizing operations and avoiding costly reliance on imported alternatives.

While receivable clearance has strengthened liquidity and allowed exceptional dividends, sustained earnings growth will depend on dispatch volumes and tariff recoveries.

Successful execution of its gas strategy could partially offset the margin squeeze and improve earnings visibility in the medium term, though volatility remains elevated until fuel arrangements and regulatory matters are fully resolved.

Comments

Comments are closed for this article.