Bata Pakistan Limited (PSX: BATA) was incorporated in Pakistan in 1951 and became public in 1979.

The company is engaged in the manufacturing and sale of all kinds of footwear along with sale of accessories and hosiery items. Bafin B.V. (Nederland) is the parent company of BATA whereas the ultimate parent company is Compass Limited, Bermuda.

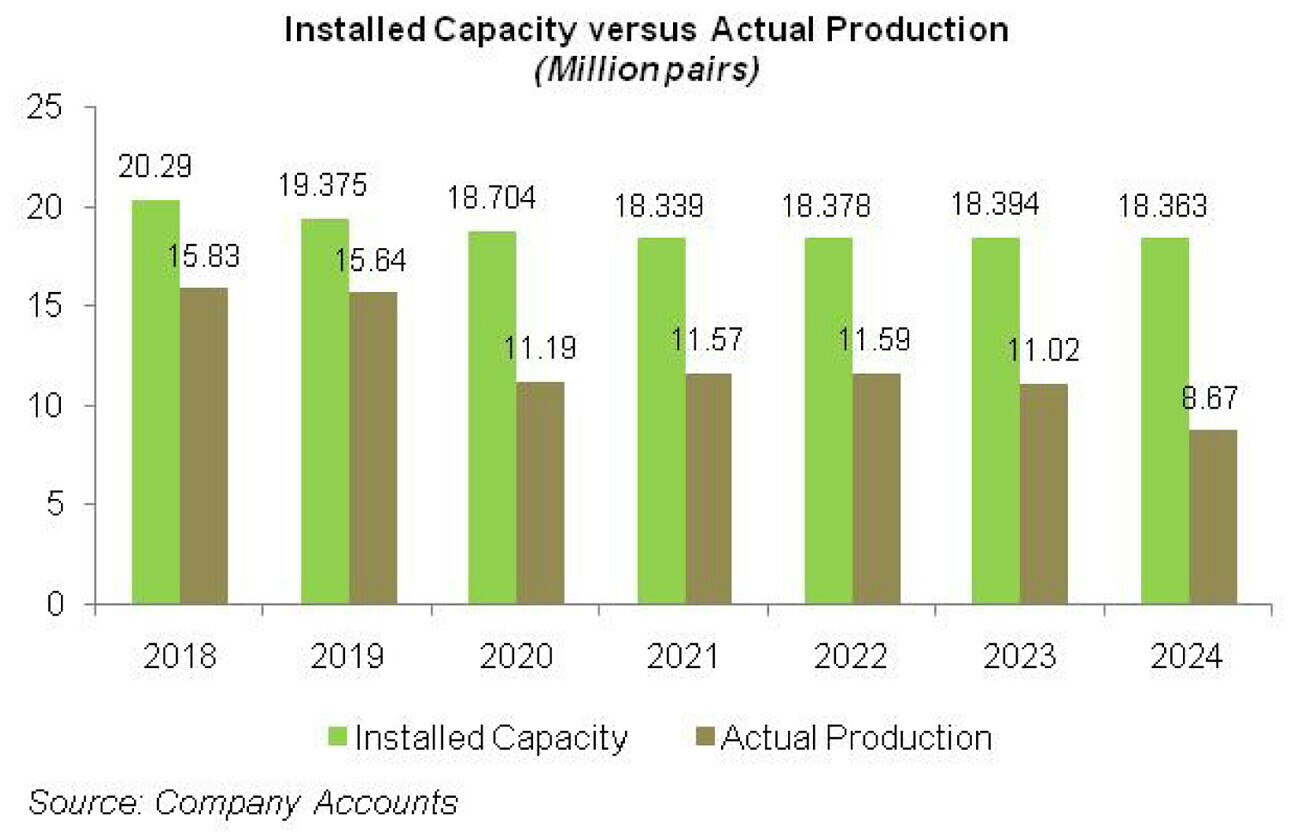

As of December 31, 2023, BATA has 444 retail outlets across Pakistan. The company has an annual production capacity of 18.394 million pairs.

Pattern of Shareholding

As of December 31, 2024, BATA has a total of 7.56 million shares outstanding which are held by 1316 shareholders. Bafin B.V. (Nederland), the parent company of BATA, has a major shareholding of 75.21 percent followed by NIT & ICP holding 15.22 percent shares of BATA. Local general public has 4.25 percent stake in the company while insurance companies account for 3.49 percent shares.

Around 1.56 percent of BATA’s shares are held by pension funds. The remaining shares are held by other categories of shareholders.

Financial Performance (2019-24)

Except for a decline in 2020 and 2024, BATA’s topline has posted reasonable growth in all the years under consideration. Its bottomline declined in 2019, 2020 and 2024.

The company registered net loss in 2020.

The company’s gross margin slightly inched up in 2019, while its operating and net margins plunged. This was followed by a drastic drop inall margins in 2020.

BATA’s margin recovered for the next two years only to slide back in 2023.

In 2024, gross and operating margins picked up while net margin descended.The detailed performance review of the period under consideration is given below.

In 2019, BATA’s topline grew by 3.75 percent year-on-year to clock in at Rs.17,424.89 million. During the year, the company reduced its production capacity from 20.29 million pairs to 19.375 million pairs and operated at 80.73 percent capacity versus 78 percent capacity utilization attained in 2018.

The change in production and sales enabled the company to record 4.57 percent higher gross profit in 2019 with GP margin climbing up from 44.81 percent in 2018 to 45.16 percent in 2019.

Distribution expense increased by 8.94 percent in 2019 mainly on account of higher depreciation on right-of-use assets, higher trademark license fee, elevated advertising expense as well as increased payroll expense. This was despite the fact that during the year, the company streamlined its number of outlets from 476 to 462 which meant lesser sales force.

Administrative expense grew by a mere 2.04 percent in 2019 due to higher payroll expense as well as management service fee payable to Global Footwear Services Pte Limited and Bata Brands S.A.R.L., Switzerland for management and information technology services, respectively. Other expense plummeted by 15.68 percent in 2019 due to lower profit related provisioning booked during the year.

Other income also shrank by 32.59 percent in 2019 due to less income from financial assets. Operating profit slid by 0.58 percent in 2019 with OP margin clocking in at 13.17 percent versus OP margin of 13.74 percent attained in 2018.

Finance cost escalated by 1779.73 percent in 2019 on account of elevated level of discount rate as well as lease liability recorded during the year as the company obtained retail outlets and wholesale depots on lease from different parties. This translated into 27.48 percent lower net profit to the tune of Rs.1088.862 million recorded in 2019.

EPS slipped from Rs.198.6 in 2018 to Rs.144.03 in 2019. NP margin clocked in at 6.25 percent in 2019 versus NP margin of 8.94 percent posted in 2018.

BATA’s net sales drastically tumbled by 32.79 percent to clock in at Rs.11,710.77 million in 2020. This was on account of sluggish performance of both retail and non-retail outlets due to COVID-19. The company reduced its retail outlets from 462 in 2019 to 444 in 2020 due to weak demand.

Production capacity was also reduced to 18.704 million pairs with capacity utilization of 59.81 percent achieved in 2020. Cost of sales tapered off by 23.18 percent in 2020 which was much lower than the decline recorded in net sales. This was due to lower absorption of fixed overheads. This resulted in 44.46 percent lower gross profit recorded by BATA in 2020 with GP margin of 37.32 percent.

Distribution expense leveled off by 12.90 percent in 2020. Higher depreciation charge was diluted by lower payroll expense due to lesser number of operational outlets, lesser rent, and lower utility expense as well as curtailed trademark license fee incurred during the year.

Administrative expense inched down by 1 percent in 2020 due to lower payroll expense as number of employees was reduced from 2683 in 2019 to 2287 in 2020. 50 percent lower other expense incurred during the year was the result of no profit-related provisioning done during the year. Rent concessions received during the year resulted in 1429.48 percent higher other income recorded by BATA in 2020. The company recorded operating loss of Rs.106.93 million in 2020.

Finance cost grew by 1.38 percent in 2020 due to higher interest on lease liability. BATA recorded net loss of Rs.627.345 million in 2020 with loss per share of Rs.82.98.

In 2021, BATA recorded 19.41 percent higher net sales to the tune of Rs.13,983.50 million. This was due to change in sales mix, increased volume as well as upward revision of prices. In pursuance of better production and sales mix, the company reduced its production capacity to 18.339 million pairs per annum and operated at 63.1 percent capacity.

Cost of sales ticked up by just 2.29 percent in 2021, resulting in 48.15 percent improved gross profit recorded in 2021 with GP margin of 46.31 percent. Distribution expense grew by 6.80 percent in 2021 due to higher payroll expense, elevated freight charges as well as increased trademark license fee incurred during the year.

Administrative expense grew by 1.58 percent in 2021 mainly because of higher management service fee and increased payroll expense incurred during the year, although, BATA right sized its workforce to 2274 employees in 2021 from 2287 employees in 2020.

Other expense grew by 46.60 percent in 2021 due to higher profit related provisioning and exchange loss incurred during the year. Other income contracted by 33.28 percent in 2021 due to greater rent concessions received in 2020.

The company was able to record operating profit of Rs.1525.93 million in 2021 with OP margin of 10.91 percent. Finance cost slid by 10.29 percent in 2021 due to monetary easing and less lease liabilities outstanding. Net profit clocked in at Rs.546.089 million in 2021 with EPS of Rs.72.23 and NP margin of 3.91 percent.

BATA registered net sales of Rs. 17,733.99 million, up 26.82 percent year-on-year in 2022. During the year, BATA slightly increased its annual production capacity to 18.378 million pairs and operated at 63.05 percent capacity. Improved volume, right sales mix, upward price revision and cost cutting measures resulted in 32.64 percent higher gross profit in 2022 with GP margin of 48.43 percent – the highest level achieved to-date.

Distribution expense mounted by 29 percent in 2022 due to considerable hike in payroll expense, trademark license fee, rent as well as advertising and promotion budget incurred during the year. 24.17 percent higher administrative expense incurred during 2022 was the result of higher payroll expense, management service fee as well as travelling charges.

BATA made increased profit related provisioning during the year and also incurred higher exchange loss which translated into 28.29 percent higher other expense in 2022. Other income dropped by 17.73 percent in 2022 due to significantly less rent concessions received during the year as well as lower profit earned on bank deposits and investments.

BATA’s operating profit registered 41.6 percent year-on-year rise in 2022 with OP margin mounting to 12.18 percent, Finance cost grew by 4.32 percent in 2022 due to higher discount rate and higher mark-up incurred on WPPF and employees/agents’ securities and personal accounts.

Higher effective tax rate due to imposition of super tax slightly diluted the bottomline which posted 60.10 percent rise to clock in at Rs.874.288 million in 2022 with EPS of Rs.115.65 and NP margin of 4.93 percent.

BATA’s sales improved by 8.62 percent to clock in at Rs.19,262.62 million in 2023. The company’s production capacity slightly increased to clock in at 18.394 million pairs per annum, however, the company operated at 59.93 percent capacity. The capacity enhancement was particularly done in cemented footwear.

High inflation, Pak Rupee depreciation, hike in commodity prices as well as high energy cost resulted in 10.62 percent higher cost of sales in 2023. Gross profit grew by 6.49 percent in 2023, however, GP margin dwindled to clock in at 47.48 percent. Distribution expense grew by 7.58 percent in 2023 particularly on account of higher payroll expense and elevated level of depreciation charge recorded during the year.

While the company reduced its workforce from 2142 employees in 2022 to 1983 employees in 2023, its payroll expense multiplied due to inflationary pressure. This resulted in 28.80 percent higher administrative expense in 2023. Other expense grew by 14.60 percent in 2023 due to higher exchange loss and greater provisioning for WWF.

Other expense was conveniently offset by 103.20 percent higher than other income which was the result of gain on lease modification as well as higher income on investments and bank deposits. Operating profit thinned down by 2.99 percent in 2023 with OP margin ticking down to 10.88 percent.

Despite high discount rate, BATA was able to keep a check on its finance cost which grew by a mere 0.46 percent in 2023. This was due to lesser outstanding lease liabilities in 2023. Net profit grew by 4.80 percent to clock in at Rs.916.288 million in 2023 with EPS of Rs.121.2 and NP margin of 4.76 percent.

In 2024, BATA’s net sales ticked down by 4.83 percent to clock in at Rs.18,332.46 million. During the year, the company not only reduced its annual capacity to 18.363 million pairs but also recorded the lowest ever capacity utilization of 47.21 percent. This resulted in the annual production of 8.67 million pairs of shoes.

BATA also significantly reduced its number of retail outlets from 444 in 2023 to 401 in 2024. The decline in production, retail presence and sales volume speak volumes of the tough economic conditions prevailing in the country. Prolonged period of high inflation significantly squeezed the purchasing power of consumers which kept them at bay from the purchase of non-essential products.

Cost of sales slid by 7.89 percent in 2024 resulting in 1.45 percent drop recorded in gross profit for the year. However, cost control measures and the ability to pass on the onus of cost hike to its consumers resulted in the highest GP margin of 49.17 percent in 2024. Distribution expense tumbled by 4.72 percent in 2024 due to lower salaries of sales force as the company reduced its retail presence during the year.

Moreover, lesser advertising & sales promotion, trademark license fee as well as repair & maintenance charges also contributed to pushing down the distribution expense in 2024. Administrative expense ticked up by 4.95 percent in 2024 due to higher payroll expense. This was despite the fact that the company drastically downsized from 1983 employees in 2023 to 1796 employees in 2024.

No exchange loss incurred during the year coupled with lesser provisioning done for WWF and WPPF resulted in 50.11 percent lower other expense recorded in 2024. Other income also dwindled by 31.19 percent in 2024 due to lesser income from bank deposits and short-term investments as well as thinner gain recorded on lease modification.

BATA recorded 2 percent weaker operating profit in 2024, however, OP margin slightly improved to clock in at 11.20 percent. Finance cost shrank by 11 percent in 2024 due to discount rate cut in the latter half of the year coupled with lesser outstanding liabilities at the end of the year.

BATA recorded net profit of Rs.850.73 million in 2024, down 7.15 percent year-on-year. This translated into EPS of Rs.112.53 and NP margin of 4.64 percent in 2024.

Recent Performance (1QCY25)

During the first quarter of the ongoing calendar year, BATA recorded net sales of Rs.5283.12 million, up 17.32 percent year-on-year. This was on account of Eid shopping spree as Eid fell in March this year versus April in the previous year. Barring the Eid factor, the company was still grappling against thinner demand which resulted in reduced capacity utilization at both of its plants.

Cost of sales surged by 12 percent in 1QCY25. Cost optimization and upward price revision enabled BATA to attain 22.67 percent higher gross profit in 1QCY25 with GP margin of 52 percent versus GP margin of 49.79 percent attained in 1QCY24.

Distribution expense escalated by 26.68 percent in 1QCY25 seemingly due to higher advertising & promotion expense and increased salaries of workforce. Conversely, administrative expense dropped by 5.14 percent during the period under review. This may be due to the fact that the company has been squeezing its workforce since 2021.

Higher profit related provisioning appears to be the cause of 133.82 percent growth in other expense in 1QCY25. Conversely, other income tumbled by 83.92 percent probably due to lower interest income on account of monetary easing. Operating profit multiplied by 12.48 percent in 1QCY25; however, OP margin deteriorated from 11.50 percent in 1QCY24 to 11 percent in 1QCY25.

Finance cost surged by 30 percent in 1QCY25 due to increased borrowings. Net profit strengthened by 15.63 percent to clock in at Rs.247.984 million in 1QCY25. This translated into EPS of Rs.32.80 in 1QCY25 versus EPS of Rs.28.37 recorded in 1QCY24. NP margin slightly dipped from 4.76 percent in 1QCY24 to 4.69 percent in 1QCY25.

Future Outlook

Effective sales mix and rising export sales have been the mantra of BATA’s improved net sales over the years. This coupled with lower discount rate and down-trending inflation will prove to be good omen for the company. The company should also focus on expanding its online presence and boosting its online sales through effective marketing and supply chain strategies to add diversity to its sales channels.

Comments

Comments are closed for this article.