Din Textile Mills Limited (PSX: DINT) was incorporated in Pakistan in 1988. The company is engaged in the manufacturing and sale of yarn and fabric.

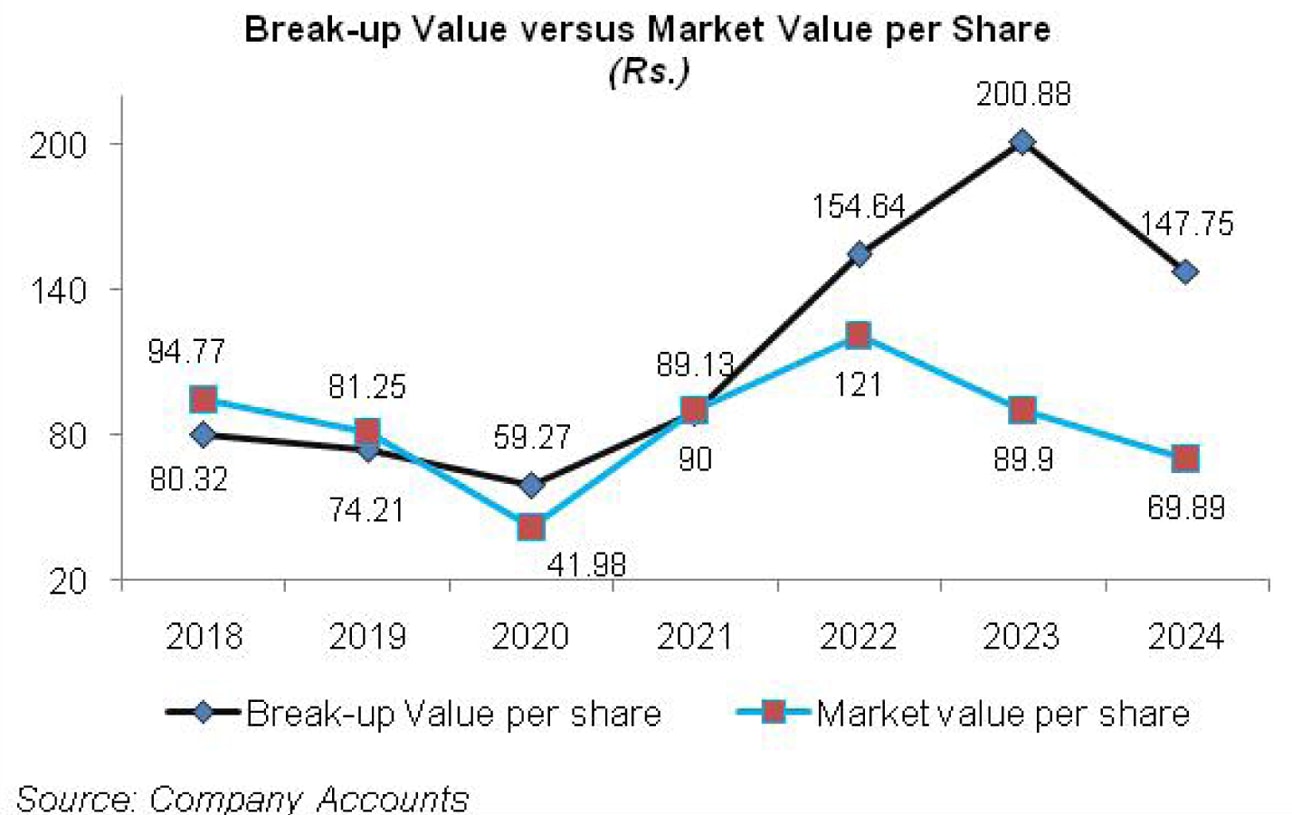

Pattern of Shareholding

As of June 30, 2024, DINT has a total of 52.467 million shares outstanding which are held by 854 shareholders. Directors, CEO, their spouse and minor children have the majority stake of 46.64 percent in DINT followed by local general public holding 27.78 percent shares of the company.

Associated companies, undertaking and related parties account for 12.33 percent shares of the company. Around 1.53 percent of DINT’s shares are held by NIT & ICP. The remaining shares are held by other categories of shareholders.

Financial Performance (2019-24)

DINT’s topline rode an upward trajectory over the period under consideration while its bottomline declined thrice during the period i.e. in 2020, 2023 and 2024. In 2023 and 2024, the company registered net loss. Its margins which considerably improved in 2019 fell in 2020. This was followed by two successive years of resurgence of margins. In 2023 and 2024, DINT’s margins collapsed. The detailed performance review of the period under consideration is given below.

In 2019, DINT’s net sales posted a healthy year-on-year growth of 21.96 percent to clock in at Rs. 11,560.48 million. This was due to considerable improvement in both local and export sales proceeds. Local sales volume considerably improved in 2019.

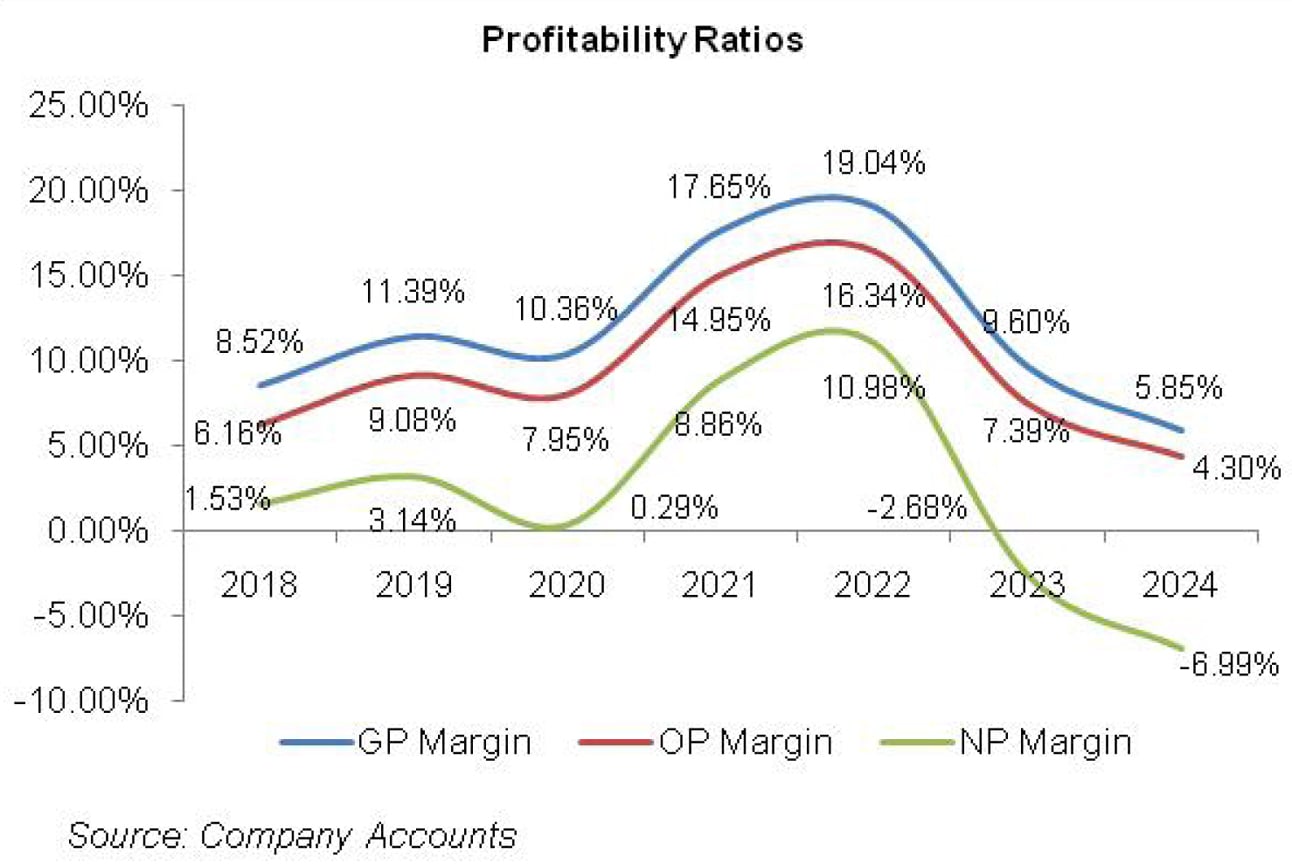

Pak Rupee depreciation made export sales highly lucrative by increasing its margin in 2019. This drove DINT’s gross profit up by 63.17 percent in 2019 with GP margin climbing up to 11.39 percent versus GP margin of 8.52 percent recorded in 2018.

Selling & distribution expense tumbled by 10.37 percent in 2019 due to lower ocean freight and air freight charges incurred during the year while local freight charges continued to built up signifying higher sales volume in the home market. Administrative expense also picked up by 9.50 percent in 2019 on account of higher payroll expense as additional human resources were hired during the year to cater to high demand.

In 2019, DINT’s workforce comprised of 2632 employees versus 2586 employees in 2018. 159.45 percent escalation in other expense in 2019 was the consequence of higher profit related provisioning as well as loss on sale of fixed assets. Operating profit mounted by 79.66 percent in 2019 with OP margin rising up to 9.1 percent versus OP margin of 6.16 percent posted in the previous year.

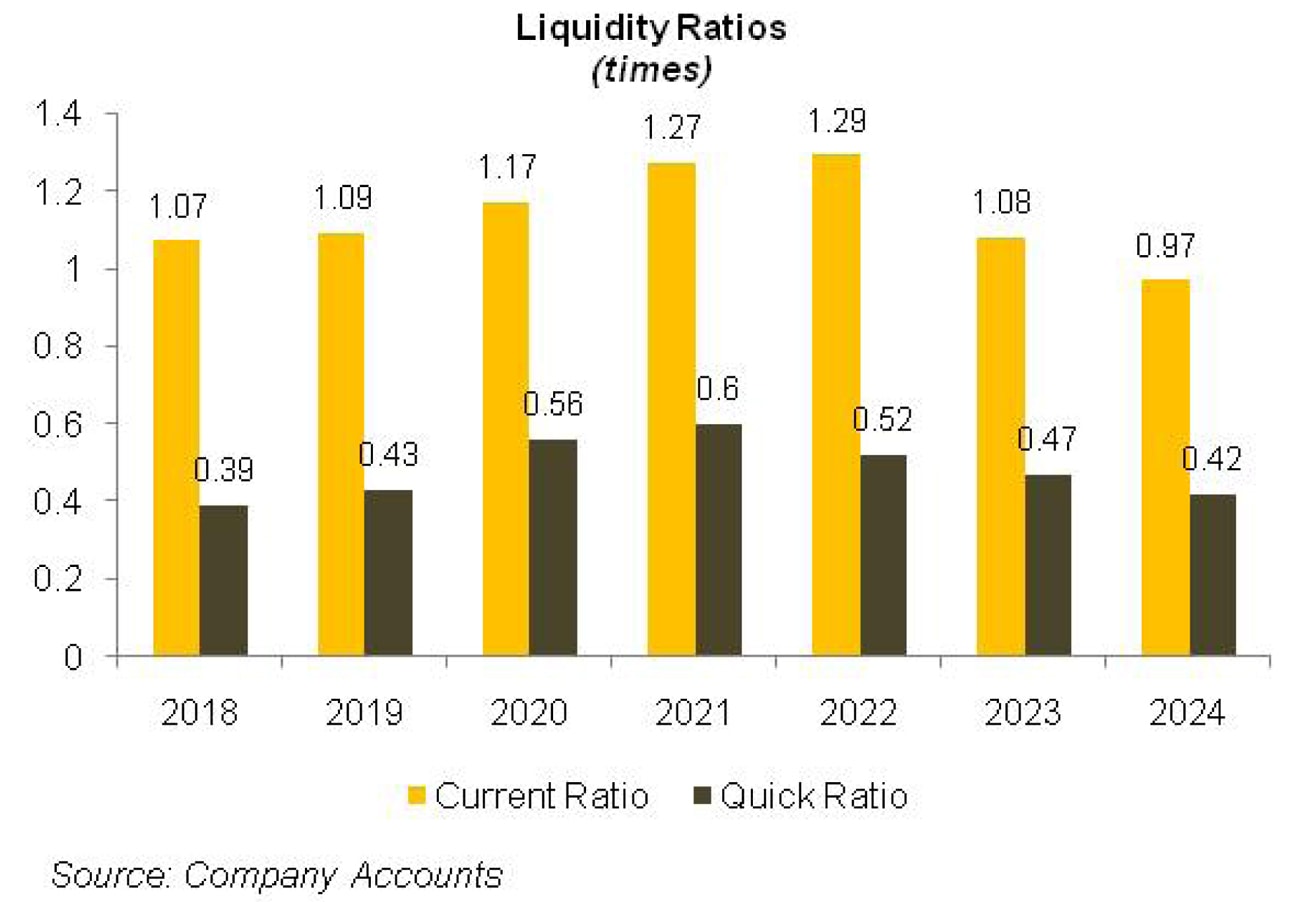

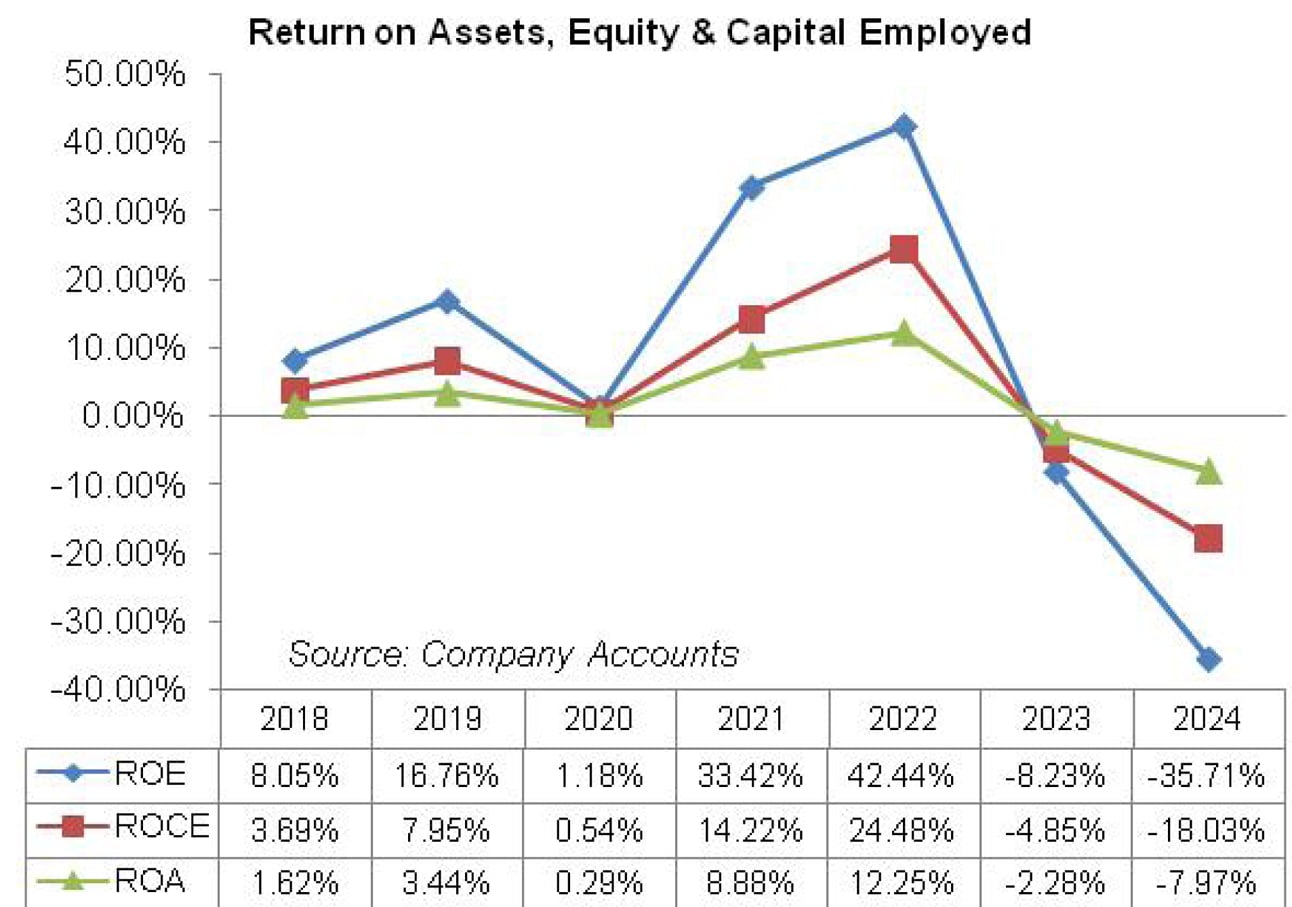

DINT’s financial charges surged by 78.83 percent in 2019 on account of higher discount rate as well as increased external borrowings. As a consequence, the company’s gearing ratio built up from 65.12 percent in 2018 to 69.59 percent in 2019. Net profit rebounded by 150.16 percent in 2019 to clock in at Rs.362.45 million with EPS of Rs.10.46 versus EPS of Rs.4.97 in 2018. NP margin also spiraled from 1.53 percent in 2018 to 3.14 percent in 2019.

In 2020, DINT’s net sales multiplied by 7.89 percent to clock in at Rs.12,482.83 million. Sales volume plunged during the year owing to COVID-19. Low capacity utilization resulted in lower absorption of fixed cost during the year. This culminated into 1.82 percent year-on-year decline in gross profit.

GP margin also shrank to 10.36 percent in 2020. Distribution expense mounted by 15.56 percent in 2020 on the back of higher local freight charges as well as increased clearing & forwarding charges. Administrative expense also mounted by 25.53 percent in 2020 due to higher payroll expense as number of employees increased to 2656 in 2020.

DINT curtailed its profit related provisioning during the year. This coupled with no loss incurred on the sale of fixed assets unlike last year drove other expense down by 15.91 percent in 2020. Other income magnified by 1301 percent in 2020 to clock in at Rs.6.95 million due to gain on sale of fixed assets as well as government grant received during the year.

Operating profit contracted by 5.42 percent in 2020 with OP margin dropping down to 7.95 percent. Finance cost grew by 29.17 percent in 2020 due to increased long-term borrowings as well as higher discount rate for the initial three quarters of 2020. Net profit descended by 89.89 percent in 2020 to clock in at Rs.36.63 million with EPS of Rs.0.86. NP margin slipped to 0.29 percent in 2020.

In 2021, DINT’s net sales posted robust recovery of 41.33 percent to clock in at Rs.17,641.44 million. This was on the back of sound growth in both local and export sales. During the year, the company also setup a weaving unit with the capacity of 144 looms.

Higher sales volume coupled with better yarn prices in local and international market as well as cost control measures implemented by the management resulted in 140.71 percent higher gross profit recorded by the company in 2021 with GP margin ascending to 17.65 percent. Distribution expense posted a steep hike of 96.48 percent in 2021 due to higher ocean freight and local freight charges as well as elevated clearing and forwarding charges.

Increased capacity utilization and commissioning of weaving unit required additional resources which took the total human resources count to 3405 in 2021. This resulted in 44.81 percent higher administrative charges in 2021. DINT also made greater provisioning for WWF and WPPF during 2021 which combined with loss incurred on the sale of fixed assets pushed other expense up by 202.59 percent. This was partially offset by 1011.43 percent higher other income recorded by the company in 2021.

Superior other income was the result of government grant of Rs.76.97 million received during the year. Operating profit posted staggering growth of 165.77 percent in 2021 with OP margin picking up to 14.95 percent. Monetary easing resulted in 14 percent drop in finance cost in 2021 despite hefty long-term loans obtained during the year. Net profit progressed by 4166.31 percent in 2021 to clock in at Rs.1562.92 million with EPS of Rs.29.79. NP margin mounted to 8.86 percent in 2021.

During the period under consideration, 2022 stands out on account of highest year-on-year topline growth of 77.72 percent. DINT’s net sales was recorded at Rs.31,352.71 million. This was the result of better local and export sales made during the year coupled with higher yarn prices.

Increased volume and prices as well as higher margin on export sales due to Pak Rupee depreciation drove gross profit up by 91.79 percent in 2022 with GP margin rising up to 19 percent – the highest during the period under consideration. Distribution expense soared by 186.66 percent in 2022 particularly due to significantly higher ocean freight charges and local freight charges on the back of improved volume as well increase in petroleum prices.

Administrative expense escalated by 23.79 percent in 2022 due to significantly higher payroll expense due to inflation as well induction of additional resources which took the workforce to 3488 employees. Increased profit related provisioning and provisioning for doubtful debt pushed other expense up by 101 percent in 2022. Other income also grew by 63.76 percent in 2022 due to government grant of Rs.116.846 million received during the year.

Operating profit multiplied by 94.19 percent in 2022 with OP margin boasting its highest value of 16.34 percent. Monetary tightening coupled with elevated short-term borrowings pushed finance cost up by 98.21 percent in 2022. Net profit spiraled by 120.31 percent year-on-year in 2022 to clock in at Rs.3443.297 million with EPS of Rs.65.63 and NP margin of 11 percent.

DINT’s net sales growth couldn’t impress in 2023 as it stood at a meager 3.07 percent. DINT’s net sales clocked in at Rs.32,313.74 million. This was due to decline in sales volume both locally and globally owing to world-wide recession, elevated prices of gas & electricity, removal of subsidies, import restrictions, Pak Rupee depreciation, unprecedented level of discount rate, political headwinds and scarcity of locally produced cotton due to floods at the onset of FY23.

All these factors inflated cost of sales by 15 percent in 2023 resulting in 48 percent year-on-year plunge in gross profit with GP margin falling down to 9.60 percent. Distribution expense surged by 53.53 percent in 2023 due to exceptionally high freight charges on account of spike in petroleum prices.

Administrative expense picked up by 6.76 percent in 2023 on the back of high vehicle running & maintenance charges, utility expense, repair & maintenance and miscellaneous expenses incurred during the year. While number of employees grew from 3488 in 2022 to 3507 in 2023, DINT was able to trim down its payroll expense.

Other expense plummeted by 86.62 percent in 2023 due to no profit related provisioning done during the year. Other income performed well as it enlarged by 48 percent in 2023 due to gain on translation of foreign currency account and government grant received during the year.

Operating profit dwindled by 53.36 percent in 2023 with OP margin sliding down to 7.40 percent. 116.96 percent bigger finance cost incurred during the year was the effect of higher discount rate as well as increased short-term and long-term borrowings obtained during the year. DINT incurred net loss of Rs.867.523 million in 2023 with loss per share of Rs.16.53.

In 2024, DINT recorded year-on-year growth of 22.57 percent in its topline which clocked in at Rs.39,608.14 million. This came on the back of 49.16 percent growth in revenue proceeds from local sales which clocked in at Rs.29,685.869 million in 2024.

Conversely, export sales ticked down by 19.34 percent to clock in at Rs.10,290.933 million in 2024. High cost of production in the local market particularly on the back of elevated energy cost has made Pakistan’s textile exports uncompetitive in the international market particularly in the midst of towering recession and depressed demand.

Gross profit tapered off by 25.32 percent in 2024 with GP margin falling down to its lowest level of 5.85 percent. Distribution expense slumped by 18.40 percent in 2024 due to lower ocean freight charges on account of thinner export sales. Administrative expense ticked up by 2.18 percent in 2024 due to higher payroll expense as the company expanded its workforce from 3507 employees in 2023 to 3522 employees in 2024.

Considerably lesser donations, drop in provisioning for ECL and no loss recorded on the sale of property, plant and equipment resulted in 55.23 percent plunge recorded in other expense in 2024. Other income also dipped by around 1 percent due to no translation gain recorded on foreign currency account and lesser government grant recognized during the year.

DINT recorded 28.74 percent thinner operating profit in 2024 with OP margin falling down to 4.30 percent. Finance cost surged by 32.23 percent in 2024 due to higher discount rate. The company recorded net loss of Rs.2768.500 million in 2024, up 219.13 percent year-on-year. This culminated into loss per share of Rs.52.77 in 2024.

Recent Performance (9MFY25)

During the nine months of the ongoing fiscal year, DINT recorded 8.42 percent uptick in its net sales which clocked in at Rs.32.17 million. This was due to higher local sales coupled with upward revision in prices. Gross profit enhanced by 118.87 percent in 9MFY25 with GP margin staggeringly growing to 8.33 percent from GP margin of 4.13 percent recorded in 9MFY24.

Lower export sales translated into 27.68 percent decline in distribution expense in 9MFY25. Conversely, administrative expense inched up by 8.85 percent due to higher payroll expense on account of inflationary pressure. Operating profit picked up by 204.29 percent in 9MFY25 with OP margin recorded at 7 percent versus OP margin of 2.49 percent recorded in 9MFY24.

Finance cost ticked down by 19.51 percent in 9MFY25 due to lower discount rate and better working capital management. DINT was able to cut down its net loss by 75.57 percent which clocked in at Rs.0.562 million in 9MFY25. This translated into loss per share of Rs.10.72 in 9MFY25 versus loss per share of Rs.43.88 recorded during the same period last year.

Future Outlook

The imposition of 10 percent universal tariff on imported goods and additional reciprocal tariffs on the countries with high trade barriers resulted in a total of 29 percent tariff imposed on Pakistan’s exports to the US market. This coupled with higher local energy tariff will result in further decline in the country’s textile exports which is already grappling against regional counterparts such as India, Bangladesh and Vietnam.

The company is actively seeking for ways to reduce its energy cost by installing a solar unit and also enhancing its capacity. Lower discount rate will also significantly reduce the company’s finance cost. The company has also recently inaugurated its stitching unit to make its ways into value-added sector. This will add diversity to the company’s sales mix and will also enhance its margins.

Comments

Comments are closed for this article.