Fauji Fertilizer Company Limited (PSX: FFC) is incorporated in Pakistan as a public limited company. The company is engaged in the manufacturing, purchasing and marketing of fertilizers and chemicals. The company also undertakes investment in other fertilizer, chemicals, cement, food processing, energy generation and banking operations.

Pattern of Shareholding

As of December 31, 2024, FFC has a total of 1,423.109 million shares outstanding which are held by 29,400 shareholders. Associated companies, undertakings and related parties (Committee of Admin Fauji Foundation) have the majority stake of 43.51 percent in FFC followed by local general public holding 25.06 percent shares.

Public sector companies and corporation account for 9.62 percent shares of FFC while Banks, DFIs, NBFIs, Insurance, Pension Funds, Takaful and Modarabas collectively hold 9.02 percent shares. Around 2.39 percent of FFC’s shares are held by foreign companies. The remaining shares are held by other categories of shareholders.

Financial Performance (2019-24)

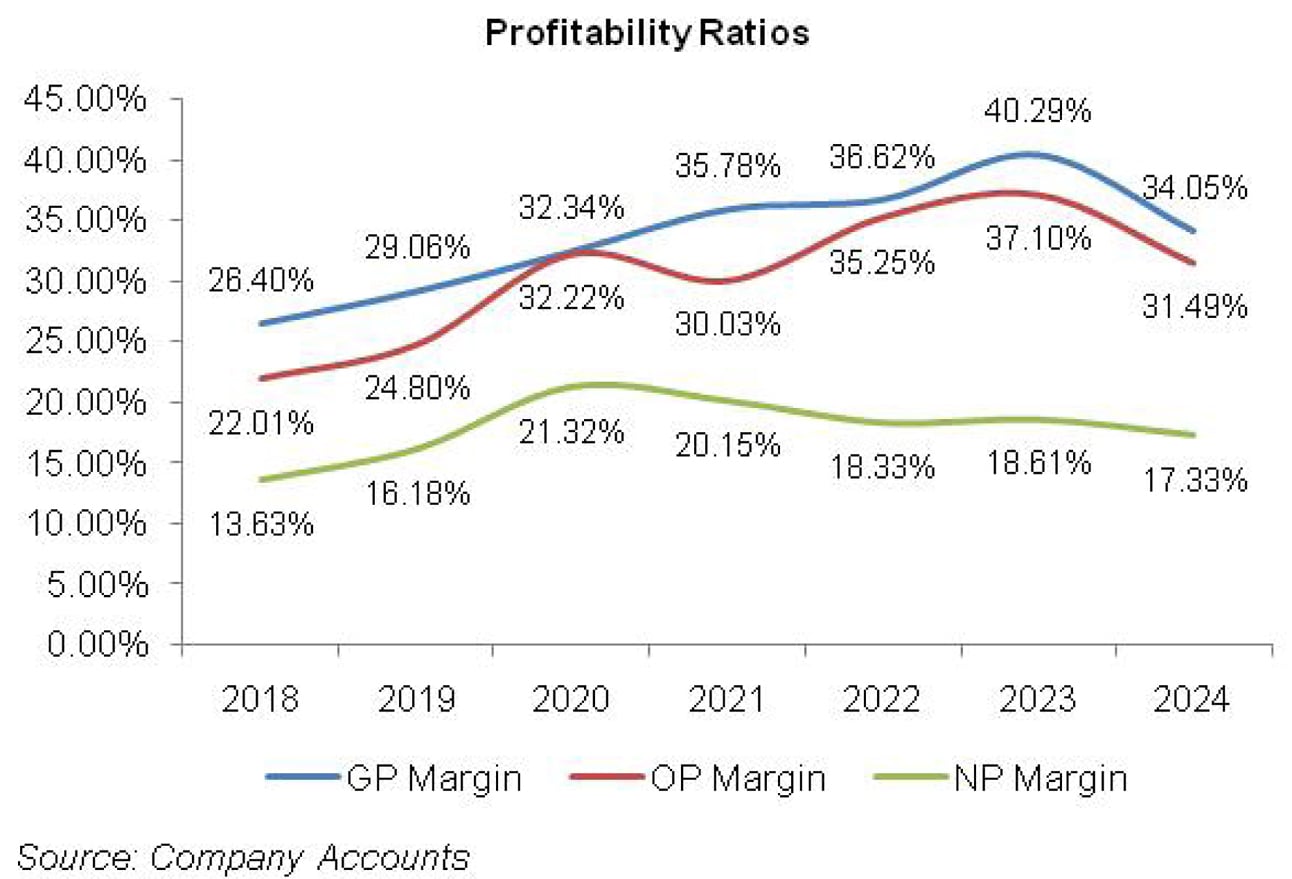

Over the period under consideration, FFC’s topline declined in 2019 and 2020 . Conversely, its bottomline slid only once in 2022. The company’s margins registered an unabated growth until 2020. In the subsequent year, gross margin continued its growth trajectory, however, operating and net margins eroded.

In 2022, both gross and operating margin ticked up while net margin shrank owing to high finance cost. In 2023, FFC registered significant growth in all its margins followed by a downtick registered in 2024 (see the graph of profitability ratios). The detailed performance review of the period under consideration is given below.

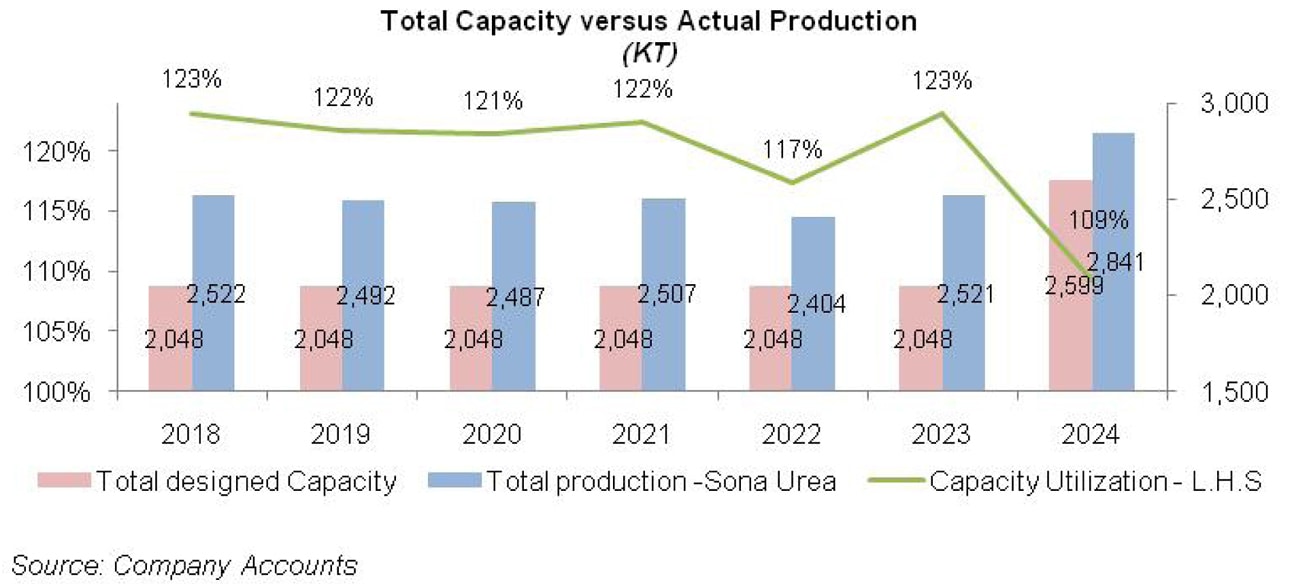

In 2019, FFC’s topline slid by 0.17 percent to clock in at Rs.105,783.41 million. Off-take of Sona urea and imported fertilizer dropped by 2 percent and 50 percent respectively in 2019 (see the graph of sales volume). This was on account of lower cultivable acreage, poor farm economics and scarcity of water which resulted in 4 percent decline in the output of major crops.

The government also imported 100,000 tons of urea during the year despite sufficient local production. This created surplus in the market and resulted in price wars.

The company was able to cut down its cost by 3.77 percent in 2019. This resulted in 9.86 percent rise in FFC’s gross profit in 2019 with GP margin climbing up from 26.40 percent in 2018 to 29.06 percent in 2019.

Distribution expense slid by 6.17 percent in 2019 due to lower DAP imports by FFC on account of Pak Rupee depreciation, high fuel prices and axle load restriction which had magnified the overall transportation cost.

Other income improved by 14.45 percent in 2019 due to substantial rise in dividend income, income from associated companies as well as interest income on bank deposits. Higher profit related provisioning and impairment loss arising from Fauji Fresh & Freeze resulted in 9.52 percent higher other expense incurred by FFC in 2019.

The company was able to boost its operating profit by 12.48 percent in 2019 with OP margin recorded at 24.8 percent up from OP margin of 22.01 percent posted in 2018. Finance cost mounted by 51.32 percent in 2019 on account of higher discount rate as well as higher borrowing requirements.

Discontinuation of super tax during the year resulted in 8.3 percent lower tax expense incurred during the year. Consequently, net profit enlarged by 18.51 percent in 2019 to clock in at Rs.17,110.49 million with EPS of Rs.13.45 versus EPS of Rs.11.35 posted in 2018. NP margin greatly rebounded from 13.63 percent in 2018 to 16.18 percent in 2019.

FFC’s net sales further shrank by 7.68 percent to clock in at Rs. 97,654.75 million in 2020. Sales of Sona urea grew by 2 percent in 2020 while imported fertilizer sales remained intact at 253 KT. As the government suspended GIDC on gas during the year, FFC also reduced the selling prices of urea which resulted in a lower topline.

The company was able to cut down its cost by 11.96 percent due to saving in fixed cost as well as reduction in GIDC. This enabled FFC to drive up its gross profit by 2.75 percent in 2020 with GP margin climbing up to 32.34 percent. Distribution expense plunged by 5.31 percent in 2020 due to lesser fuel prices and partial implementation of axle load regulations by the GoP. Other income slid by 10.59 percent in 2020 due to lower interest income from bank deposits due to lower discount rate.

Lower scrap sales and no dividend from FCCL and FBBL also contributed in driving down other income in 2020. Other expense escalated by 14.28 percent in 2020 on account of increased provisioning for WWF and WPPF as well as higher R&D cost incurred during the year. All these factors culminated into 19.96 percent higher operating profit recorded by FFC in 2020 with OP margin mounting to 32.22 percent.

Finance cost contracted by 24.37 percent in 2020 due to monetary easing. Net profit rebounded by 21.68 percent to clock in at Rs.20,819.46 million in 2020 with EPS of Rs.16.36 and NP margin of 21.32 percent – the highest among all the years under consideration.

In 2021, FFC topline multiplied by 11.26 percent to clock in at Rs.108,650.89 million. This appears to be the result of revised selling prices as sales volumes of Sona Urea and imported fertilizers declined by 1 percent and 11 percent respectively in 2021. Prices of fertilizers in the international market recorded a massive rise due to production cuts, export restrictions imposed in several countries, high energy and fuel prices which drove up the freight expense.

Gross profit gained 23 percent strength in 2021 with GP margin rising up to 35.78 percent. One of the reasons for better GP margin was the abolishment of GIDC. Higher freight expense due to hiking fuel prices resulted in 7.15 percent higher distribution expense incurred by FFC in 2021.

The company also booked unwinding on re-measurement of GIDC along with ECL on subsidy receivable from the government which diluted its operating performance during the year. Elevated dividend income particularly from AKBL and interest income from its investment in mutual funds culminated into 23.17 percent taller other income recorded by FFC in 2021. Other expense also magnified by 11.64 percent in 2021 as a result of R&D expense and profit related provisioning booked during the year.

Due to elevated expenses and other losses, FFC’s operating profit posted a marginal 3.71 percent growth in 2021 with OP margin sliding down to 30.03 percent. Finance cost enhanced by 22.34 percent in 2021 due to hike of discount rate and increased borrowings As a consequence, FFC’s net profit could post a paltry 5.17 percent rise in 2021 to clock in at Rs.21,896.14 million with EPS of Rs.17.21 and NP margin of 20.15 percent.

2022 brought about a paltry 0.66 percent growth in the topline of FFC which clocked in at Rs.109,363.82 million. During the year, the company sold 2 percent less Sona Urea than it did last year while imported fertilizer sales fell by a drastic 68 percent in 2022. Exorbitant prices of imported fertilizer due to supply chain disruptions, escalated global prices as well as Pak Rupee depreciation drove the demand down in 2022 and the company had to carry 78 KT of imported fertilizer to next year.

The agriculture sector recorded a robust growth of 4.4 percent in 2022 versus last year growth of 3.5 percent. This was the result of higher yield, supportive government policies and agricultural credit. However, in the latter half of the year, devastating flood in the southern region of the country turned down the agriculture sector forecasts for 2023.

Due to plant turnaround during the year as well as lower production, the company’s cost of sales also slipped by 0.65 percent in 2022, resulting in 3 percent rise in gross profit with GP margin touching new high of 36.62 percent. Distribution expense multiplied by 20.20 percent in 2022 which was the effect of higher inflation and soaring fuel prices.

The company also booked other losses as the re-measurement of GIDC liability recorded in 2020 had to be reversed for the next four years. This coupled with ECL on subsidy receivable from the government translated into other losses of 2788.51 million in 2022. Other expense also ticked up by 3.08 percent in 2022 on account of increased provisioning for WPPF. However, 82.37 percent higher other income made by FFC during the year compensated it reasonably. This growth was the consequence of gain on investment in mutual funds as well as dividend income from associated companies particularly FWEL-I, FWEL-II and PMP.

Operating profit mounted by 18.15 percent in 2022 with OP margin clocking in at 35.25 percent.112 percent year-on-year growth in finance cost of FFC in 2022 came on the back of exorbitantly high discount rate as well as superior working capital requirements. This pushed the bottomline down by 8.43 percent to clock in at Rs.20,049.51 million with EPS of Rs.15.76 and NP margin of 18.33 percent.

In 2023, FFC’s topline registered handsome growth of 45.82 percent to clock in at Rs.159,471.95 million. During the year, Sona urea sales grew by 2 percent while sale of imported fertilizers mounted by 72 percent. 60.44 percent expansion in gross profit with GP margin reaching its optimum high value of 40.29 percent speaks volume of the company’s ability to pass on the impact of 75 percent hike in gas prices to its consumers.

Distribution expense mounted by 25.49 percent in 2023 due to higher fuel prices, increased sales volume as well as axle load requirements as the company’s primary transportation is done by road. During the year, the company recorded the loss allowance of 2900 million on subsidy receivable from the government which along with unwinding of GIDC payable resulted in other losses magnifying by 45.61 percent.

Other expense surged by 78.92 percent in 2023 owing to elevated R&D expense and profit related provisioning. Other income spiraled by 18.38 percent in 2022 on account of higher interest income and dividend income.

All these factors translated into 53.47 percent year-on-year rise in FFC’s operating profit in 2023 with its OP margin climbing up to 37.10 percent. Finance cost picked up by 15.52 percent in 2023 due to higher discount rate and increased working capital requirements. Higher effective tax rate of 45 percent due to retrospective increase in super tax levy drove up tax expense by 75.07 percent in 2023. Net profit picked up by 48 percent year-on-year in 2023 to clock in at Rs.29,673.35 million with EPS of Rs.22.32 and NP margin of 18.61 percent.

In 2024, FFC’s net sales grew by a staggering 134.23 percent to clock in at Rs.373,536.92 million. This came on the back of 17 percent rise in the dispatches of Sona urea and 19 percent rise in the dispatches of imported fertilizer. During the year, a scheme of arrangement was signed for the amalgamation of of FFBL into FFC.

The effective date of merger was July 01, 2024. Hence, the financial figures presented in the annual report include full year results of FFC and second half result of FFBL. Cost of sales mounted by 158.73 percent in 2024 due to spike in the price of gas and imported raw materials and also because of inflationary pressure.

Gross profit enhanced by 97.93 percent in 2024, however, GP margin drastically dropped to 34 percent. Distribution expense escalated by 131.50 percent in 2024. This included the distribution expense of not only Sona urea and imported fertilizer but also granular urea.

Other losses mounted by 33.37 percent in 2024 due to loss allowance on subsidy receivable from the GoP, unwinding charge on GIDC liability (which completed during the year) and also because of impairment booked on the FFC’s investment in Fauji Fresh & Freeze (FFF). Other income strengthened by 106 percent in 2024 due to higher dividend income and elevated interest income due to better cash availability and increased discount rate.

Other expense magnified by 83.82 percent in 2024 as the company booked higher provisioning for WWF and WPPF on account of increased profitability due to merged entity. FFC’s operating profit built up by 98.81 percent in 2024, however, OP margin slid to 31.49 percent. Finance cost grew by 16 percent in 2024. While FFBL had paid its entire long-term borrowings before merger, the transfer of its short-term borrowings to FFC’s books resulted in the combined short-term borrowings of Rs.38 billion as of December 31, 2024 versus Rs.24 billion at the close of last year. FFC recorded 118.15 percent growth in its net profit which clocked in at Rs.64,731.44 million in 2024. This translated into EPS of Rs.45.49 and NP margin of 17.33 percent.

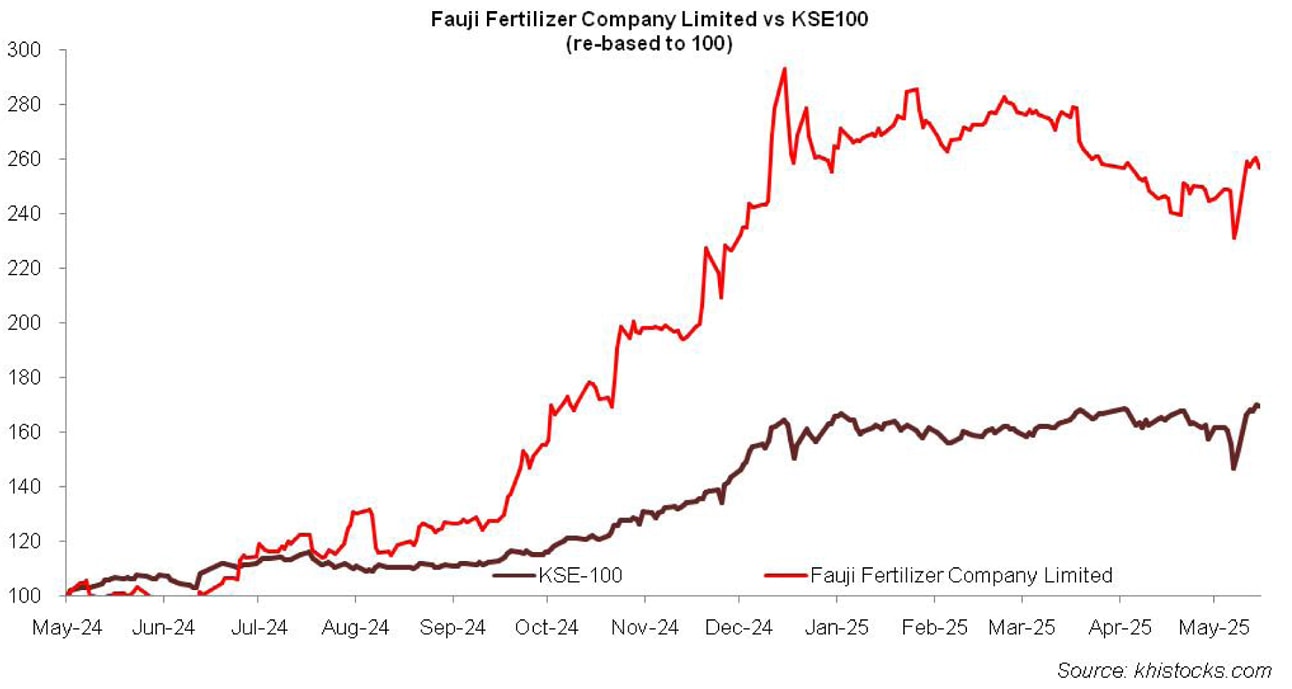

Recent Performance (1QCY25)

In the first quarter of the ongoing calendar year, FFC’s net sales improved by 8.95 percent to clock in at Rs.63,636.85 million. The industry remained oversupplied in 1QCY25 due to lower than expected rainfall and poor farm economics. During the period under review, FFC urea off-take tumbled by 26 percent year-on-year to clock in at 538,000 tons. This reflected market share of 49 percent in 1QCY25 versus market share of 45 percent recorded during the same period last year. FFC’s market share in the DAP market was recorded at 63 percent in 1QCY25.

Cost of sales slid by 0.32 percent in 1QCY25 due to stability in the value of local currency and downward trending inflation. Lower production during the quarter was also one of the reasons contributing to thinner cost of sales. Gross profit improved by 31 percent in 1QCY25 with GP margin clocking in at 35.60 percent versus GP margin of 29.60 percent recorded in 1QCY24.

No other losses was recorded in 1QCY25 versus other loss of Rs.1,162.12 million recorded in 1QCY24. Distribution expense escalated by 17.42 percent in 1QCY25 due to axle load requirement. Lesser discount rate resulted in 27.55 percent decline in other income in 1QCY25.

Higher profit related provisioning resulted in 12.95 percent uptick in other expense recorded in 1QCY25. FFC recorded 13.16 percent higher operating profit in 1QCY25 with OP margin of 34.73 percent versus OP margin of 33.44 percent recorded in 1QCY24.

Finance cost surged by 12.86 percent in 1QCY25. Net profit picked up by 26.19 percent to clock in at Rs.13,277.82 million. This translated into EPS of Rs.9.33 in 1QCY25 versus EPS of Rs.8.27 recorded in 1QCY24. NP margin increased from 18 percent in 1QCY24 to 20.86 percent in 1QCY25.

Future Outlook

Going forward, challenging farm economics due to significant reduction in wheat cultivation area and wheat prices and drought conditions in Sindh and lower Punjab will result in lower off-take of the fertilizer industry. However, with reduced discount rates and inflation, the company may be able to improve its profitability and margins.

Comments

Comments are closed for this article.