Nishat Mills Limited (PSX: NML), the flagship company of Nishat Group was established in 1951. Being one of the largest vertically integrated companies in Pakistan, the company is engaged in spinning, weaving, printing, dyeing, bleaching, and stitching and apparel business. NML deals in yarn, linen and other products made from raw cotton and synthetic fiber. The company is also in to the business of generating and supplying electricity.

Pattern of Shareholding

As of June 30, 2024, Nishat Mills Limited has a total of 351.600 million shares outstanding which are held by 13,209 shareholders. Local general public has the majority stake of 35.09 percent in the company followed by directors, CEO, their spouse and minor children holding 25.22 percent of the company’s shares. Associated companies, undertakings and related parties grab the next spot with a stake of 8.93 percent in NML.

Around 6.93 percent of the company’s shares are held by Banks, DFIs and NBFIs and 6.89 percent by joint stock companies. Modarabas & Mutual funds account for 4.78 percent shares of NML while provident/pension funds hold 4.17 percent shares.

Foreign companies and foreign general public have 2.84 percent and 1.88 percent of NML’s shares respectively. The remaining ownership is held by other categories of shareholders.

Historical Performance (2019-24)

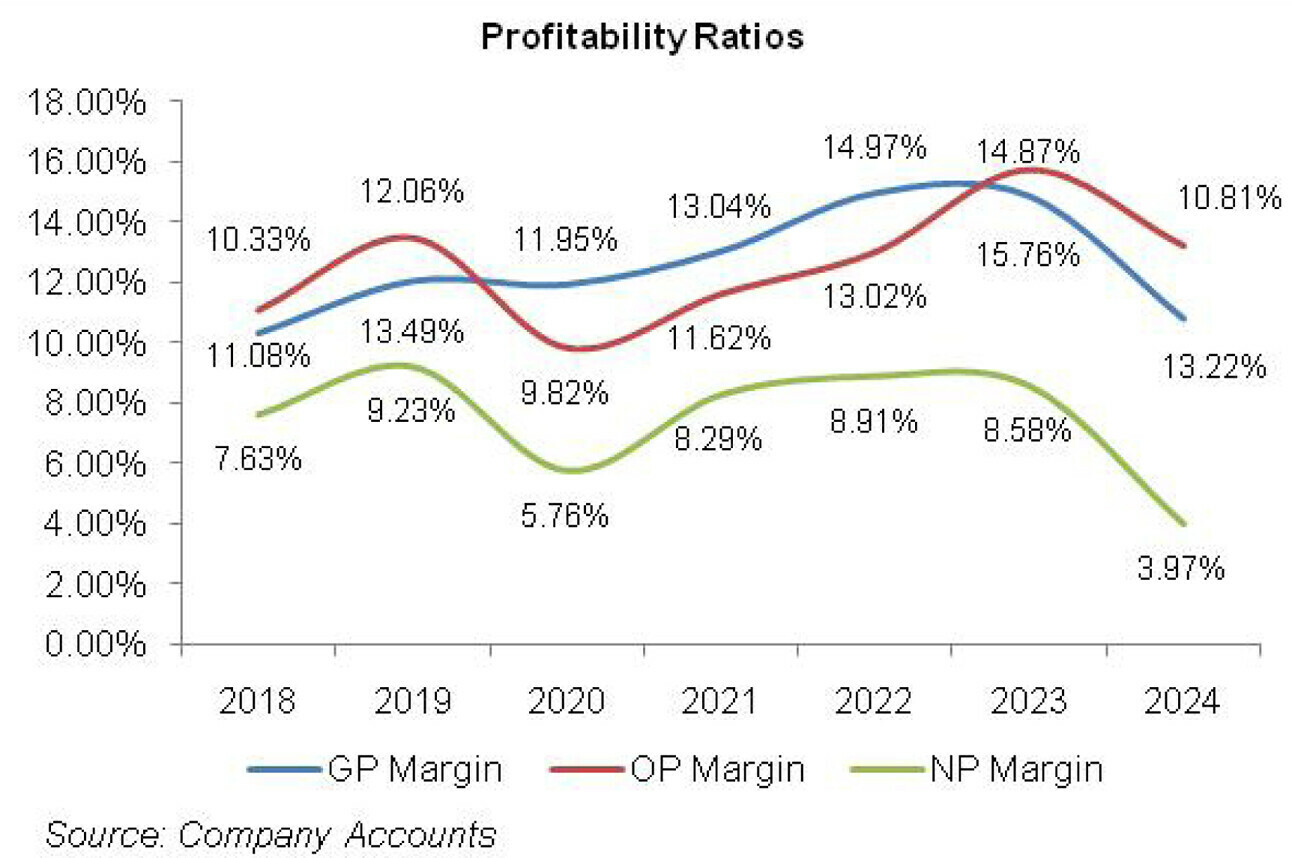

Except for a dip in 2020, NML’s topline and bottomline rode an upward trajectory in all the years under consideration. Conversely, its bottomline declined in 2020 and 2024. NML’s margins which grew reasonably in 2019 bounced back in 2020.

The subsequent two years marked the period of recovery for NML’s margins. However, in 2023, gross and net margins slightly faded while operating margin continued to heighten. The detailed performance review of the period under consideration is given below.

In 2019, NML’s net sales flourished by 18.18 percent year-on-year to clock in at Rs.63,499.029 million. Export sales, which constituted over 83 percent of the company’s total sales mix, rebounded by 23 percent year-on-year in line with the company’s marketing strategy of expanding its footprint in diverse geographies.

Gross profit rose by 37.95 percent in 2019 with GP margin climbing up from 10.33 percent in 2018 to 12.06 percent in 2019.

This was on account of Pak Rupee depreciation which considerably drove up the margins of export sales. Moreover, cost rationalization, scalability of production and availability of gas and electricity at subsidized rates of USD 6.5 per MMBTU 7.5 cents per KWH during the year also greatly contributed in achieving robust GP margin.

Distribution expense multiplied by 13.60 percent in 2019 mainly on account of outward freight & handling and commission to selling agents on account of increased export sales.

Administrative expense spiraled by 4.15 percent in 2019 due to higher payroll expense incurred during the year. Elevated profit related provisioning resulted in 90.34 percent spike in other expense during the year.

However, it was washed away by superior other income on account of net exchange gain and dividend income earned by NML in 2019. Operating profit mounted by 43.93 percent in 2019 with OP margin clocking in at 13.49 percent up from OP margin of 11.08 percent posted in 2018. 67.85 percent hike in finance cost in 2019 was the consequence of higher discount rate and increased borrowings due to greater working capital requirements.

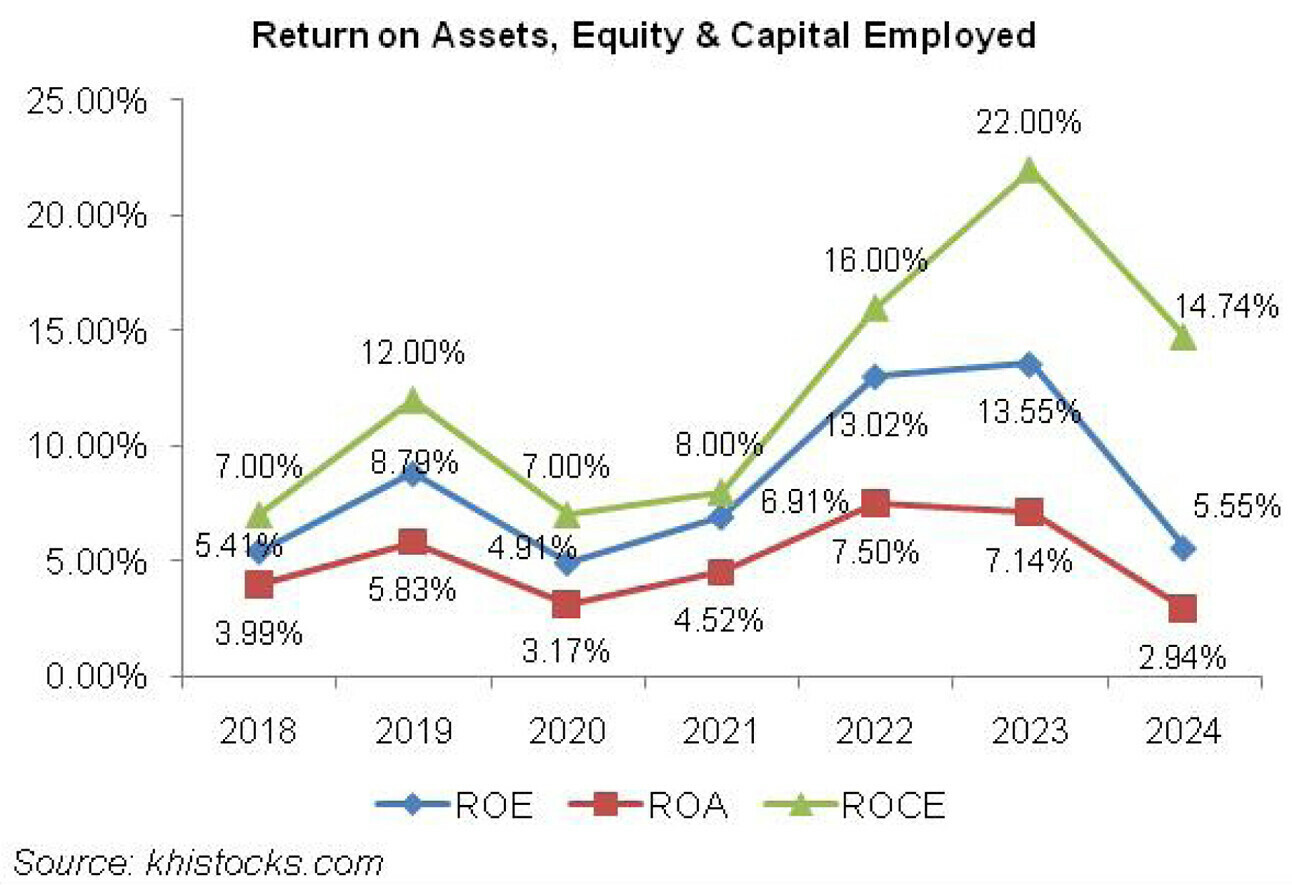

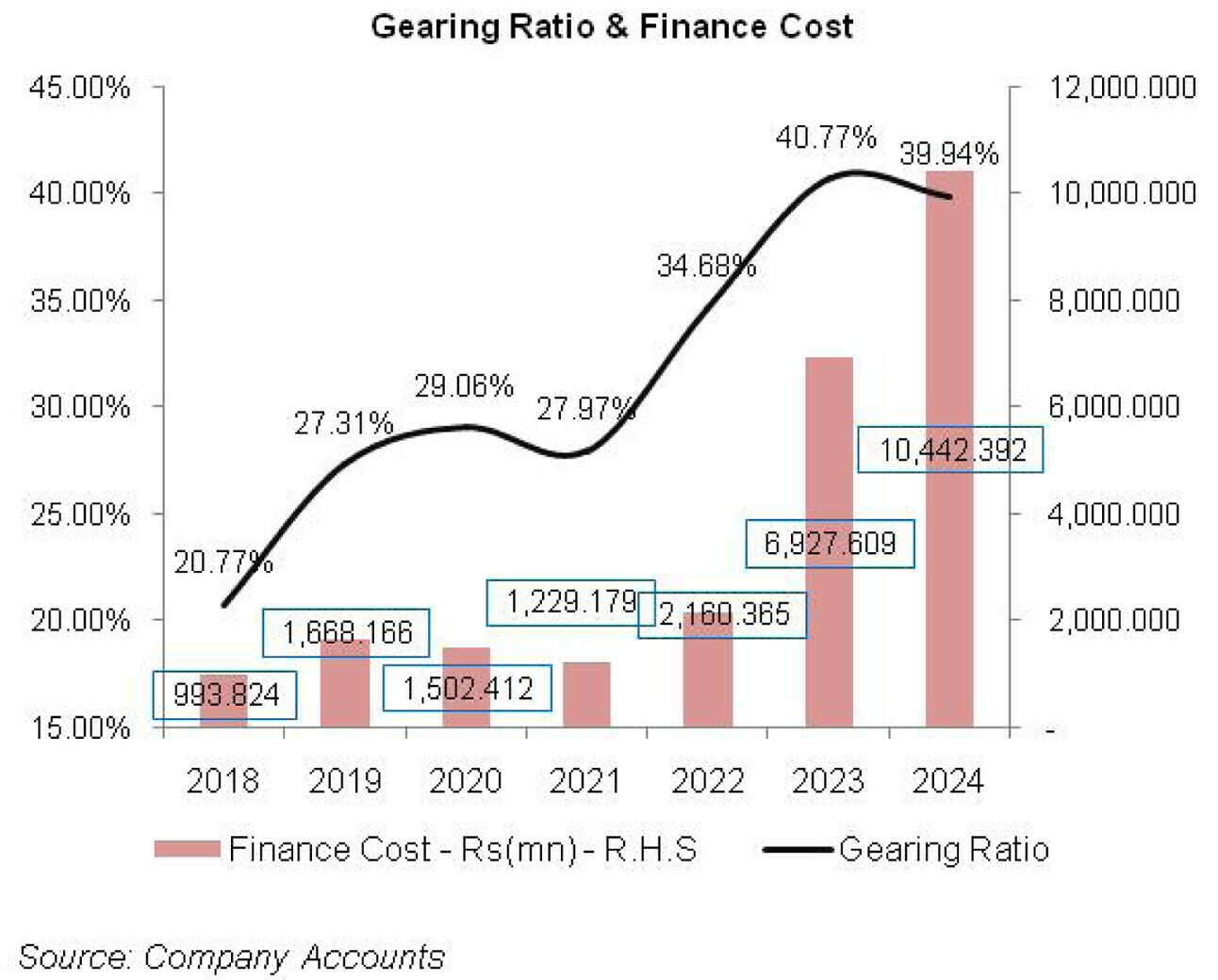

NML’s gearing ratio picked up from 20.77 percent in 2018 to 27.31 percent in 2020. Nevertheless, NML was able to register 43 percent year-on-year growth in its net profit which clocked in at Rs.5859.048 million in 2019 with EPS of Rs.16.66 versus EPS of Rs.11.65 in 2018. NP margin also enlarged from 7.63 percent in 2018 to 9.23 percent in 2019.

After a year full of achievements and recovery in term of margins and profitability, came 2020, where NML’s topline posted a year-on-year downtick of 4.09 percent to clock in at Rs.60,904.096 million. These were the times when the local as well as global economies were crippled due to the global pandemic.

NML’s topline took a hit as export sales to its main markets – China, US and Europe – dropped considerably during the year owing to lockdowns imposed in the last quarter.

Gross profit plummeted by 4.97 percent in 2020, however, GP margin marginally ticked down to clock in at 11.95 percent. Distribution expense posted a marginal growth of 3.81 percent in 2020 due to higher outward freight & handling charges due to restrictions imposed on the movement of people and goods during the year.

Administrative expense hiked by 10.67 percent in 2020 on account of higher payroll expense as the company added 567 new employees to its workforce to take it up to 18,278 employees in 2020.

This was because the company expanded its yarn production facility besides establishing a new towel manufacturing unit and installing a 3.075 MW solar power plant during 2020.

All these expansions required additional employees. Other expense slid by 40.97 percent in 2020 on account of lesser provisioning for WPPF.

Other income also eroded by 41.21 percent in 2020 due to thinner dividend income and lesser net foreign exchange gain recorded by NML in 2020. As a consequence, operating profit declined by 30.16 percent in 2020 with OP margin slipping to 9.82 percent.

Finance cost also shrank by 9.94 percent during the year due to monetary easing towards the end of the year. Net profit slumped by 40.16 percent in 2020 to clock in at Rs.3506.284 million with EPS of Rs.9.97 and NP margin of 5.76 percent.

In 2021, NML’s topline registered 17.28 percent year-on-year rise to clock in at Rs. 71,431.01 million. This was the result of a remarkable 84 percent rise in local sales. Export sales also inched up by 2.2 percent as COVID related restrictions began to ease off. Duty drawback incentive on export sales also positively contributed in topline growth in 2021.

While prices of raw material significantly hiked during the year, strategic pricing and cost control strategies adopted by the company enabled it to attain 28.06 percent year-on-year growth in gross profit with GP margin rising up to 13.04 percent in 2021.

Distribution expense escalated by 7.69 percent in 2021 on account of higher outward freight and handling charges.

Administrative expense surged by 8.22 percent in 2021 as NML’s workforce expanded to incorporate 20,599 employees which drove up the payroll expense. 55.64 percent hike in other expense was the consequence of increased profit related provisioning done in 2021.

However, it was wiped off was by 23.67 percent bigger other income recognized during the year on the back of superior dividend income particularly from MCB Bank Limited, an associated company of NML.

Scrap sales and rental income also strengthened other income in 2021. This translated into 38.75 percent rise in operating profit in 2021 with OP margin picking up to 11.62 percent.

Finance cost declined for the second consecutive year due to monetary easing and better cash flow to meet working capital requirement for the year. Net profit posted a staggering 68.91 percent year-on-year growth in 2021 to clock in at Rs.5922.470 million with EPS of Rs.16.84 and NP margin of 8.29 percent.

Among all the years under consideration, 2022 stands out when it comes to topline and bottomline growth. NML’s topline magnified by 62.07 percent to clock in at Rs.115,768.065 million in 2022. The growth was the result of favorable pricing and bigger volumes sold during the year. Local and export sales mounted by 84 percent and 62 percent respectively during the year.

Pak Rupee depreciation, supply chain disruptions, huge increase in raw cotton prices due to damage of cotton crop on account of catastrophic floods, energy crisis as well as upward revisions in energy prices increased the cost of sales by 58.47 percent 2022, however, with better volume and prices, the company was able to attain 86.05 percent rise in its gross profit with GP margin reaching its optimum level of 14.97 percent in 2022.

Massive 82.98 percent year-on-year hike in distribution expense during the year was the effect of higher outward freight and handling charges as well as commission to selling agents. Expansion of workforce to 24,086 employees resulted in 24.72 percent spike in administrative expense in 2022. Improved profitability allowed the company to book higher provision for WPPF.

This resulted in 51.30 percent bigger other expense incurred in 2022. Superior dividend income, net exchange gain, rental income and scrap sales drove other income up by 48.56 percent in 2022. All these factors led to 81.54 percent stronger operating profit recorded by NML in 2022 with OP margin of 13.02 percent. Finance cost soared by 75.76 percent in 2022 on account of higher discount rate and increased working capital related borrowings.

NML’s gearing ratio reached 34.68 percent in 2022 from 27.97 percent in 2021. The imposition of super tax also diluted the bottomline growth which nevertheless registered year-on-year rise of 74.11 percent in 2022 to clock in at Rs.10,311.674 million with EPS of Rs.29.33 and NP margin of 8.91 percent.

In 2023, NML’s topline mustered 22.45 percent year-on-year growth to clock in at Rs.141,756.469 million. This was on the back of better local and export sales made during the year. Despite elevated raw material cost, energy price hikes, Pak Rupee depreciation and high indigenous inflation, NML was able to keep a check on its cost of sales by implementing rigorous cost control measures.

This coupled with upward revision in prices and Pak Rupee depreciation allowed NML to record 21.60 percent year-on-year rise in gross profit with GP margin slightly ticking down to 14.87 percent. Distribution expense hiked by 10.10 percent due to higher payroll expense, commission to selling agents, fuel and travelling cost incurred during the year.

During the year, NML streamlined its workforce from 24,086 employees to 21,975 employees; however, adjustment in minimum wage rate resulted in higher payroll expense and drove up administrative expense by 28.67 percent. Higher provisioning for WPPF resulted in 11.12 percent higher other expense incurred by NML in 2023.

Superior dividend income from its associated companies particularly MCB, higher net exchange gain and interest income earned on loan granted to Nishat Linen (Private) Limited, a wholly owned subsidiary of NML, resulted in record high other income of Rs.10,201.578 million in 2023, up 83.11 percent year-on-year.

Operating profit multiplied by 48.23 percent in 2023 with OP margin reaching its highest level of 15.76 percent. 220.67 percent surge in finance cost in 2023 was the consequence of unprecedented level of discount rate and additional short-term loans obtained during the year due to working capital requirements.

NML registered the highest gearing ratio of 40.77 percent in 2023 versus 34.68 percent in 2022. Net profit grew by 17.98 percent in 2023 to clock in at Rs.12,166.022 million with EPS of Rs.34.60 and NP margin of 8.58 percent.

In 2024, NML registered year-on-year growth in its topline which clocked in at Rs.160,256.56 million. Export sales remained stable during the year, however, local sales posted a tremendous year-on-year growth of 44.68 percent to clock in at Rs.58,985.799 million.

Cost of sales surged by 18.44 percent on account of elevated gas and electricity prices. This coupled with reduced export sales and the forced price reductions due to increased competition resulted in 17.82 percent decline in gross profit in 2024 with GP margin drastically falling down to 10.81 percent.

Distribution expense inched up by 4.47 percent in 2024. While outward freight and handling charges shrank due to lower export sales, salaries of sales force and commission to selling agents were the growth drivers of distribution expense in 2024.

Administrative expense mounted by 20.38 percent in 2024 due to higher payroll expense due to workforce expansion to 23,170 employees. Other expense contracted by 51.39 percent in 2024 due to lesser profit related provisioning done during the year.

Other income posted a staggering year-onyear growth of 29.79 percent in 2024 due to superior dividend income from associated companies such as MCB Bank Limited, Pakgen Power Limited, Lalpir Power Limited and Nishat Power Limited.

The company recorded 5.14 percent decline in its operating profit with OP margin falling down to 13.22 percent. Finance cost escalated by 50.74 percent in 2024 due to higher discount rate and increased borrowings to finance new projects and working capital requirements.

In 2024, NML invested Rs.18.74 billion in new facilities related to denim and workwear units, alternate energy and efficient energy projects. NML’s gearing ratio clocked in at 39.94 percent in 2024. Net profit eroded by 47.65 percent to clock in at Rs.6368.85 million in 2024. This translated into EPS of Rs.18.11 and NP margin of 3.97 percent. This was the lowest NP margin recorded by the company.

Recent Performance (9MFY25)

During 9MFY25, NML’s topline posted year-on-year growth of 11.98 percent to clock in at Rs.134,676.29 million. The growth was primarily driven by local sales – both in terms of value and volume. While export sales to Europe remained steady during the period, export sales to Asia, America, Africa and Australia posted a plunge.

Cost of sales surged by 11.49 percent during the period owing to high energy cost and inflationary pressure. However, with price optimization, NML was able to record 15.97 percent higher gross profit with GP margin clocking in at 11.32 percent in 9MFY25 versus GP margin of 10.93 percent recorded in 9MFY24.

Selling & distribution expense mounted by 20.79 percent in 9MFY25 due to higher freight charges, salaries of sales force and commission to selling agents recorded during the year. Administrative expense also posted an increase of 15.94 percent in 9MFY25 due to higher payroll expense as the company is continuously expanding its workforce as it is spreading out its various facilities such as denim, workwear etc.

Other income plummeted by 24.79 percent during 9MFY25 due to lesser dividend income and interest income on loan to subsidiary companies. NML’s operating profit dwindled by 11.30 percent in 9MFY25 with OP margin recorded at 11.1 percent versus OP margin of 13.97 percent posted in 9MFY24.

Finance cost fell by 19.64 percent in 9MFY25 due to lower discount rate. Net profit ticked down by 9.51 percent to clock in at Rs.4839.22 million in 9MFY25. This translated into EPS of Rs.13.76 in 9MFY25 versus EPS of Rs.15.21 recorded in 9MFY24. NP margin also eroded from 4.45 percent in 9MFY24 to 3.59 percent in 9MFY25.

Future Outlook

Local economic conditions have posted sound recovery over the past few months. This coupled with a reduction in energy cost have created positive waves in the Pakistan Textile sector. However, increase in the US trade tariff will create barriers in achieving optimum export sales.

Comments

Comments are closed for this article.