Mughal Iron & Steel Industries Limited (PSX: MUGHAL) was incorporated in Pakistan as a public limited company in 2010. The company is engaged in the manufacturing and sale of mild steel products related to ferrous segments. MUGHAL also deals in non-ferrous segments.

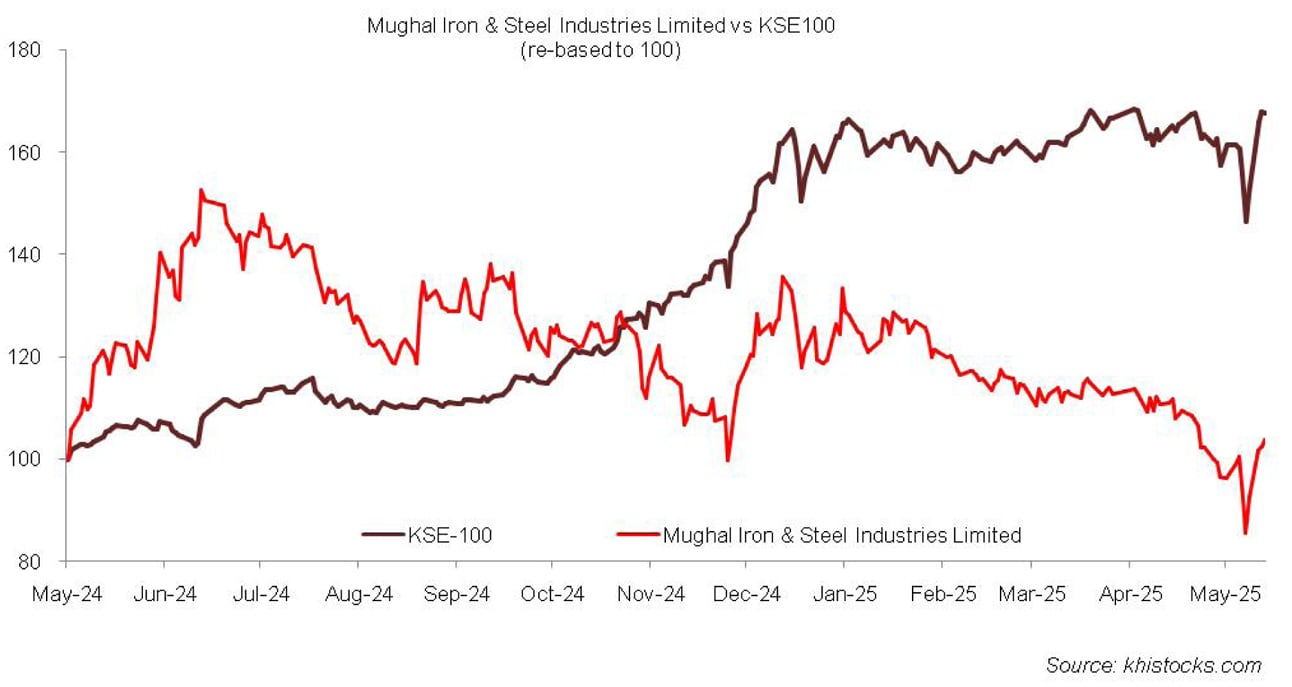

Pattern of Shareholding

As of June 30, 2024, MUGHAL has a total of 335.634 million shares outstanding which are held by 6014 shareholders. Directors, CEO, their spouse and minor children have the majority stake of 43.20 percent in the company followed by associated companies, undertakings and related companies holding 32.16 percent shares.

Local general public accounts for 7.06 percent of MUGHAL’s shares while Modarabas & Mutual Funds hold 5.83 percent shares. Around 5.16 percent of MUGHAL’s shares are held by Banks, DFIs and NBFIs and 1.911 percent by the insurance companies. The remaining shares are held by other categories of shareholders.

Financial Performance (2019-24)

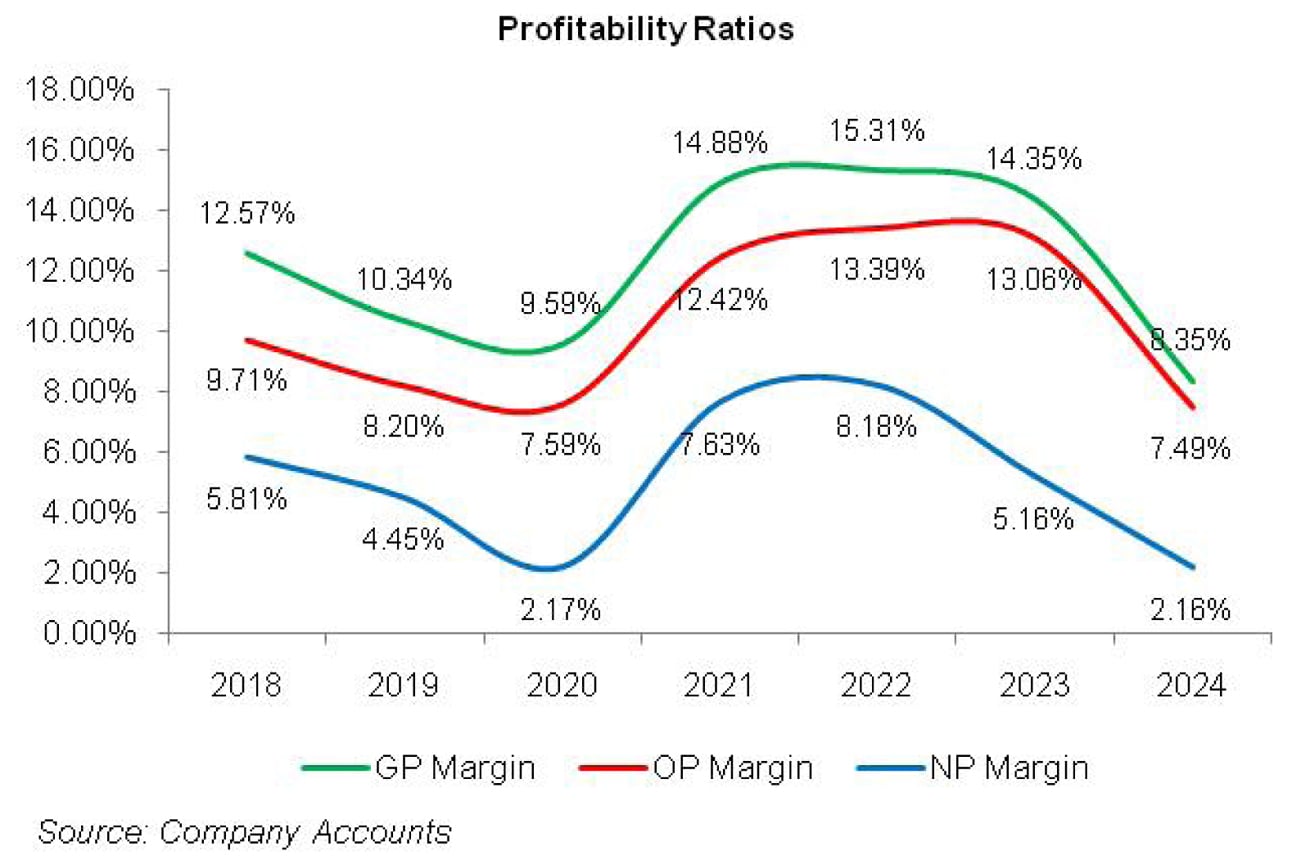

Except for a year-on-year dip in 2020, MUGHAL’s topline rode an upward trajectory over the period under consideration. However, its bottomline dipped in 2019, 2023 and 2024. The company’s margins which declined until 2020 registered a significant turnaround in 2021 and 2022 only to level down in the subsequent years. The detailed performance review of the period under consideration is given below.

In 2019, MUGHAL’s topline grew by 38.70 percent year-on-year to clock in at Rs. 30,828.09 million. This was the result of combination of higher sales volume as well as improved prices. The economic parameters of the country had been deteriorating in 2019 which was evident from rising interest rates, elevated inflation level as well as Pak Rupee depreciation.

The government had considerably curtailed the PSDP budget which could dent MUGHAL’s off-take, however, 34 percent low PSDP spending was decently counterbalanced by booming demand in the housing sector. This was on account of increasing population and the emergence of nuclear families.

Escalating input prices resulted in a plunge in GP margin from 12.57 percent in 2018 to 10.34 percent in 2019, despite 14.12 percent bigger gross profit recorded by the company in 2019. Selling & distribution expense slid by 18.16 percent in 2019 on account of lower advertising and sales promotion expense as well as freight charges incurred during the year.

Conversely, administrative expense enlarged by 17.24 percent year-on-year in 2019 which was the consequence of an increase in the number of employees from 772 in 2018 to 1127 in 2019. Higher profit related provisioning resulted in 8.62 percent hike in other expense in 2019 while other income shrank by 17.50 percent on account of lower interest income.

MUGHAL recorded 17.11 percent higher operating profit in 2019, however, its OP margin diminished from 9.71 percent in 2018 to 8.20 percent in 2019.

Finance cost magnified by 42.33 percent in 2019 on account of hiking discount rates as well as increased long-term financing for various BMR projects and short-term financing to meet working capital requirements. MUGHAL’s gearing ratio spiraled from 54 percent in 2018 to 64 percent in 2019.

The company recorded 6.41 percent rise in its net profit which clocked in at Rs.1372.93 million in 2019 with EPS of Rs.5.46 versus EPS of Rs.5.13 posted in 2018. However, NP margin plummeted from 5.81 percent in 2018 to 4.45 percent in 2019.

MUGHAL’s topline nosedived by 11.4 percent year-on-year in 2020 to clock in at Rs. 27,304.99 million. This was the consequence of lower sales volume due to disruption of operational activities during the lockdown period. At the onset of 2020, the economy had started moving towards stability with a rebound in business confidence; however, the outbreak of COVID-19 came as a shock and changed the entire paradigm of the local and global economies.

During the year, the company’s gross profit diminished by 17.92 percent year-on-year with GP margin moving down to 9.59 percent as the company couldn’t pass on the effect of cost hike to its consumers. Selling & distribution expense eroded by 28.63 percent in 2020 due to lower advertising budget and freight outward incurred during the year.

During 2020, MUGHAL expanded its workforce to 1661 employees resulting in higher payroll expense which drove up the administrative expense by 10.95 percent in 2020. 56.72 percent decline in other expense was due to lower profit related provisioning. Other income mounted by 95.97 percent in 2020 due to higher interest income. Despite keeping a check on its operating expense, operating profit contracted by 18 percent in 2020 with OP margin slipping to 7.59 percent.

Finance cost enlarged by 92.64 percent in 2020 on account of higher discount rate for most part of the year, increase in average outstanding borrowings as well as exchange loss on foreign currency borrowings due to Pak Rupee depreciation. MUGHAL’s net profit marched down by 56.82 percent year-on-year in 2020 to settle at Rs.592.87 million with EPS of Rs.2.25 and NP margin of 2.17 percent.

With 64.70 percent year-on-year boost in its topline, 2021 marked a significant year of revival for MUGHAL. Net sales clocked in at Rs. 44,971.84 million. The staggering growth was the consequence of increase in both prices and sales volumes in ferrous and non-ferrous segments. The government provided incentives to the construction industry during the year.

Moreover, monetary easing also provided impetus for a noticeable rise in housing finance. This greatly fueled the demand in the allied industries such as steel and cement. During 2021, MUGHAL’s gross profit improved by 155.64 percent as the company acquired cheap inventory when the prices were low. This resulted in significant inventory gain. GP margin reached up to 14.88 percent in 2021.

Selling & distribution expense spiked by 76.74 percent in 2021 due to higher freight and advertising expense incurred. The company expanded its workforce to 1971 employees as it commenced it bar re-rolling plant during the year which required additional employees. This resulted in 32.15 percent higher administrative expense incurred during the year.

Other expense made a massive jump of 609.55 percent in 2021 on account of profit-related provisioning as well as provision booked for doubtful debts. Operating profit magnified by 169.65 percent in 2021 with OP margin clocking in at 12.42 percent. Finance cost ticked down by 9.54 percent in 2021 due to reduction in foreign exchange loss during the year.

MUGHAL’s net profit spiraled by 478.40 percent in 2021 to clock in at Rs.3429.15 million with EPS of Rs.11.16 and NP margin of 7.63 percent.

MUGHAL’s growth trajectory continued in 2022 with 47.10 percent year-on-year rise in its topline which clocked in at Rs.66,152.81 million. The increase in topline was primarily the result of price revision.

The sales volume of ferrous segment inched down in 2022 due to a standstill in the construction activity in the country owing to political turmoil, unprecedented level of discount rate, high inflation, Pak Rupee depreciation and soaring commodity prices on account of Russia-Ukraine war.

Non- ferrous segment registered an increase in sales volume which majorly included exports to PRC. Effective inventory management enabled MUGHAL to overshadow the adverse impact of the aforementioned economic conditions.

This resulted in 51.36 percent bigger gross profit recorded by the company in 2022 with GP margin reaching its optimum level of 15.31 percent. Selling and distribution expense was streamlined by 3.42 percent in 2022 which was in line with inflation and increase in logistics cost due to hike in petroleum prices.

Administrative expense increased by 31.1 percent in 2022 mainly on account of rise in salaries due to increase in the number of employees to 2197 coupled with the adjustment of minimum wages. 40.47 percent higher other expense incurred in 2022 was the result of higher profit-related provisioning as well as exchange loss.

Other expense was partially offset by 219.31 percent rise in other income which was the result of commission against corporate guarantees, sales tax adjustment as well as claims against materials supplied to the company. Operating profit got 58.55 percent bigger in 2022 with OP margin touching an incomparable level of 13.39 percent. 91.36 percent bigger finance cost incurred in 2022 was the consequence of higher discount rate as well as increased overall borrowings.

MUGHAL’s net profit stood at Rs.5410.96 million in 2022, up 57.79 percent year-on-year with EPS of Rs.16.12 and NP margin of 8.18 percent.

In 2023, MUGHAL’s topline posted a paltry 1.9 percent year-on-year growth to clock in at Rs.67,390.17 million. The topline growth was merely price led while overall volumes declined. Political turmoil in the country, devastating floods, import restrictions, global commodity super cycle and drastically declining value of Pak Rupee, high inflation and discount rates etc took a heavy toll on industrial and construction activity in the country.

Gross profit dropped by 4.51 percent year-on-year with GP margin sliding down to 14.35 percent in 2023 on the back of high cost of sales. Selling & distribution and administrative expense took a slide of 36.84 percent and 3.24 percent respectively in 2023.

This was on account of lower advertisement budget and curtailed payroll expense respectively. Other expense plummeted by 33.63 percent in 2023 as a result of lower profit related provisioning in line with reduced profitability. Other income grew by 51.87 percent in 2023 on account of higher interest income, gain on disposal of tangible fixed assets as well as higher net foreign exchange gain.

Operating profit slipped by 0.6 percent in 2023 with OP margin clocking in at 13.06 percent. Finance cost mounted by 68.69 percent in 2023 on account of higher discount rate. MUGHAL’s net profit eroded by 35.68 percent in 2023 to clock in at Rs.3480.49 million with EPS of Rs.10.37 and NP margin of 5.16 percent.

In 2024, MUGHAL posted year-on-year growth of 37 percent in its topline which clocked in at Rs.92,382.60 million. During the year, both ferrous and non-ferrous sales increased by 47.01 percent and 14.30 percent respectively. This was the result of increase in both prices and volumes during the year. Cost of sales mounted by 46.68 percent in 2024 due to high energy cost and raw material prices. This squeezed gross profit by 20.20 percent in 2024 with GP margin hitting its lowest level of 8.35 percent.

Selling expense mounted by 33.62 percent in 2024 due to higher advertisement budget as well as export related expenses incurred during the year. Administrative expense surged by 25.80 percent in 2024 due to higher payroll expense as well as fee & subscription charges related to the issuance of various Sukuk transactions.

The company streamlined its workforce from 2250 employees in 2023 to 2216 employees in 2024. Other expense plunged by 75.95 percent in 2024 due to considerably lower provisioning done for WWF and WPPF. Other income ticked up by 9.64 percent in 2024 due to higher profit on saving accounts, gain on sale of store items, balances written back and finance income recognized on loan granted to a subsidiary company, Mughal Energy Limited.

MUGHAL recorded 21.37 percent thinner operating profit in 2024 with OP margin falling down to 7.49 percent. Finance cost mounted by 43.88 percent in 2024 due to higher discount rate and increased short-term borrowings. This resulted in gearing ratio of 56.96 percent in 2024 versus gearing ratio of 50.61 percent recorded in 2023. During the year, MUGHAL also booked reversal of allowance booked for ECL to the tune of Rs.60.45 million. This was against the allowance for ECL booked in the rest of the year. MUGHAL’s net profit descended by 42.54 percent to clock in at Rs.1999.89 million in 2024. This translated into EPS of Rs.5.96 and NP margin of 2.16 percent in 2024.

Recent Performance (9MFY25)

During the nine months of the ongoing fiscal year, MUGHAL’s net sales tumbled by 1.44 percent to clock in at Rs.66,168.14 million. This was on account of 23 percent year-on-year drop recorded in the sales of non-ferrous segment due to lower sales volume recorded in both local and export markets during 9MFY25. The decline in the sales of non-ferrous segment was in line with the company’s strategic shift towards the ferrous segment.

The company also curtailed the business of its non-ferrous segment due to operational and regulatory hurdles. Sales of ferrous segment posted an increase of 7 percent in 9MFY25 which was the result of higher dispatches. The change in sales mix resulted in 8.79 percent drop in gross profit in 9MFY25 with GP margin clocking in at 8.87 percent versus GP margin of 9.58 percent recorded in 9MFY24.

Selling & distribution expense mounted by 42.42 percent in 9MFY25 due to higher sales volume of ferrous segment as well as increased advertising budget. Administrative expense ticked up by 5.56 percent in 9MFY25 due to inflationary pressure. Lower profit related provisioning resulted in 76.45 percent lesser other expense recorded in 9MFY25. Other income ticked up by 9.87 percent during the period under review probably due to gain recognized on the sale of store items.

MUGHAL’s operating profit dwindled by 8.8 percent in 9MFY25 with OP margin clocking in at 7.83 percent versus OP margin of 8.46 percent recorded in 9MFY24. Finance cost ticked down by only 0.51 percent during 9MFY25 as the effect of lower discount rate was greatly offset by increased borrowings.

MUGHAL recorded 67.44 percent lower net profit to the tune of Rs.453 million in 9MFY25. This translated into EPS of Rs.1.35 in 9MFY25 versus EPS of Rs.4.15 recorded in 9MFY24. NP margin fell from 2.1 percent in 9MFY24 to 0.68 percent in 9MFY25.

Future Outlook

Improvement in macroeconomic indicators such as lower discount rate, downward trending inflation and stability of Pak Rupee will greatly fuel the demand in the construction sector. Besides, cheaper energy purchased from Mughal Energy Limited will reduce the company’s cost of sales and buttress it margins and profitability.

Comments

Comments are closed for this article.