Security Papers Limited (PSX: SEPL) was established as a joint venture company of Pakistan, Iran and Turkey in 1967. The company is engaged in manufacturing banknote and other security papers e.g. prize bonds, non-judicial stamp paper, passport paper, educational certificates, share certificates etc. SEPL turned into a public limited company and listed itself on Pakistan stock exchange in 1967. It started its commercial operations in 1969.

Pattern of Shareholding

As of June 2024, the company has an outstanding share volume of 59.256 million shares which are held by 1931 shareholders. Associated companies, undertakings and related parties have the majority stake of 60.03 percent in the company. Within this category, Pakistan Security Printing Corporation (Pvt) Limited holds the highest proportion of shares i.e. 40.03 percent. Local general public has the stake of 13.17 percent in the company followed by insurance companies owning 11.31 percent shares. Banks, DFIs and NBFIs stood next with 7.24 percent of company’s shares.

Modarabas and Mutual funds account for 4.44 percent of SEPL’s outstanding shares. The remaining shares are held by other categories of shareholders.

Historical Performance (2019-2024)

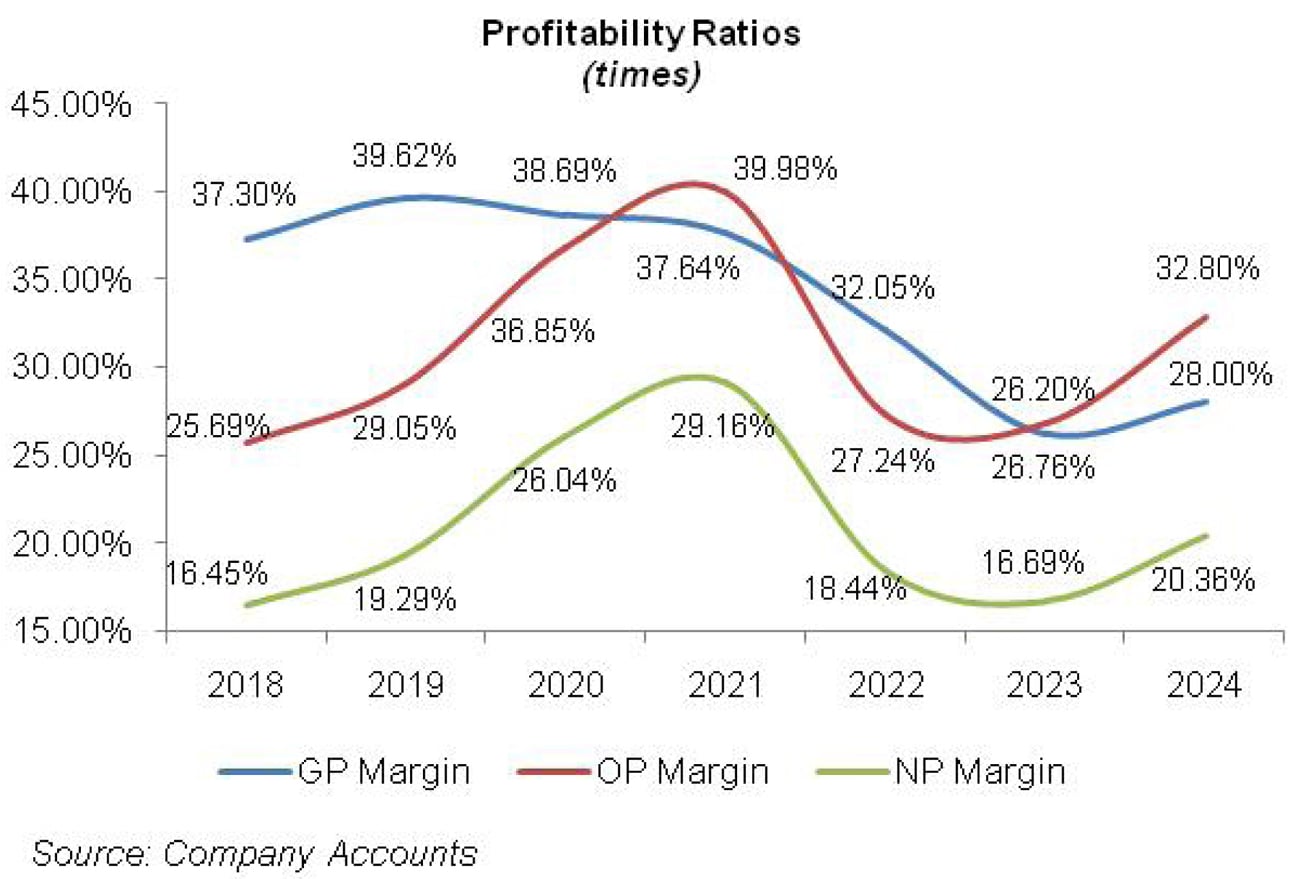

SEPL’s topline rode an upward journey over the period under consideration. In contrast to its unabated topline growth, SEPL’s bottomline slid in 2022. The company’s margins have been oscillating over the period under consideration. Gross margin which maxed out in 2019 started dipping thereafter to reach its lowest level in 2023. This was followed by an uptick in 2024.

Operating and net margins rode an uphill journey to attain their optimum level in 2021 only to slide back and touch their lowest levels in 2023. In 2024, operating and net margins also considerably recovered. The detailed performance review of the period under consideration is given below.

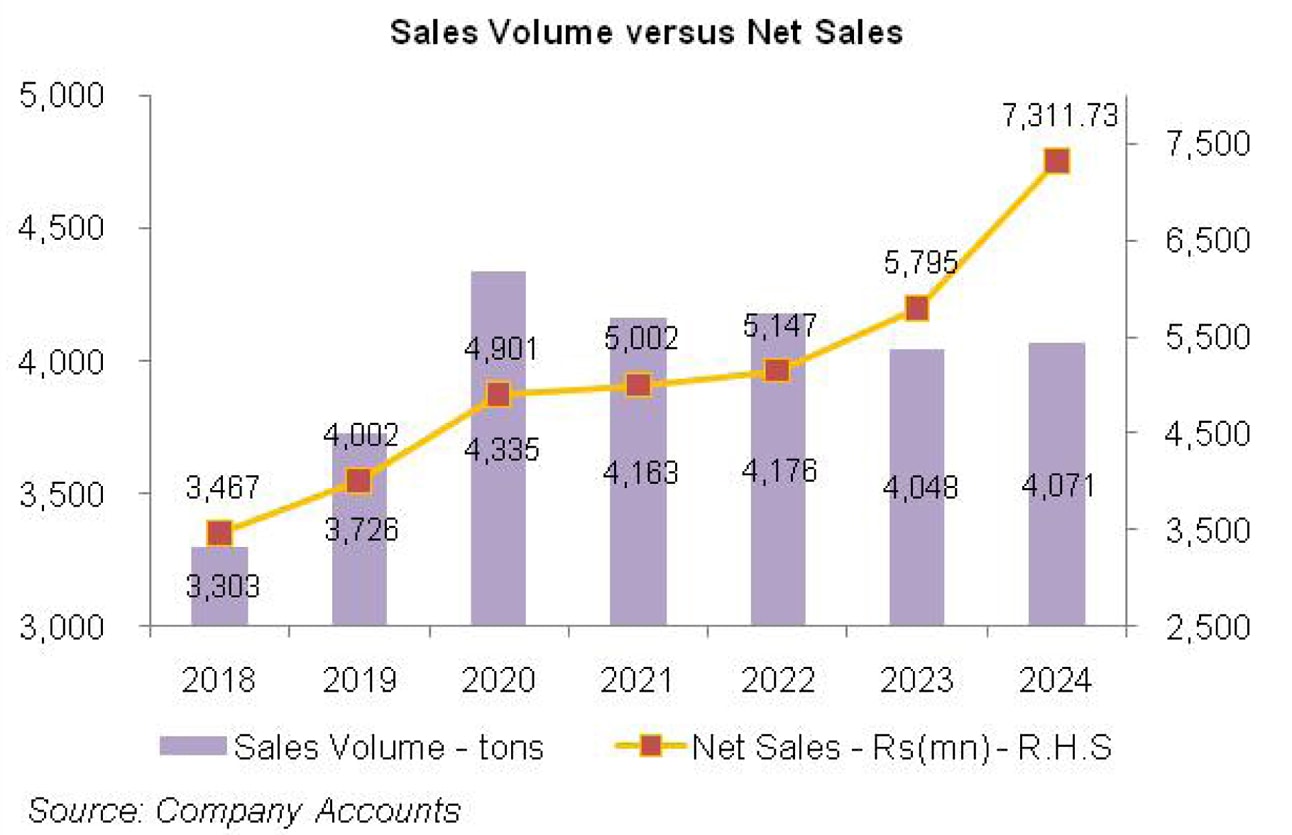

In 2019, SEPL’s net sales grew by 15.42 percent year-on-year to clock in at Rs.4001.59 million. This was on the back of 12.8 percent growth in sales volume due to increased demand from the major customer of SEPL i.e. Pakistan Security Printing Corporation (Private) Limited (see the graph of sales volume versus net sales).

Improved sales volume, cost efficiency achieved due to economies of scale and increased product value resulted in 22.58 percent year-on-year rise in gross profit in 2019 with GP margin climbing up from 37.30 percent in 2018 to 39.62 percent in 2019.

Administrative expense declined by 1.77 percent year-on-year in 2019 on the back of reduced payroll expense as the company streamlined its workforce from 387 employees in 2018 to 372 employees in 2019. Increased discount rate resulted in better profit rates on fixed income securities and bank placements which drove up other income by 31.93 percent in 2019.

However, 23.04 percent year-on-year rise in other expense due to unrealized loss on the re-measurement of mutual funds as the value of KSE-100 index fell, conveniently offset other income recognized by SEPL in 2019. Nevertheless, operating profit rebounded by 30.49 percent in 2019 with OP margin rising up from 25.69 percent in 2018 to 29.05 percent in 2019.

Finance cost slumped by 28.32 percent year-on-year in 2019 despite high discount. This was due to reduced bank charges and no mark-up charged on WPPF in 2019. Net profit spiraled by 35.36 percent year-on-year in 2019 to clock in at Rs.772.03 million with EPS of Rs.13.03 versus EPS of Rs.9.63 posted in 2018. NP margin also mounted from 16.45 percent in 2018 to 19.29 percent in 2019.

During 2020, SEPL sold 4,335 tons of bank notes and security paper products which was 16.3 percent higher than the sales volume of 2019.

Despite shortage of cotton comber (the main raw material for the company) due to lower cotton production and supply chain bottlenecks owing to COVID-19, the company was able to perform remarkably well across all the bank denominations and security paper products. SEPL recorded 22.48 percent year-on-year growth in its topline which clocked in at Rs.4901.28 million in 2020. Besides increased volumes, topline growth in 2020 is also attributable to increase in selling prices and better product mix.

The cost of imported raw material (security thread and chemicals) increased sharply owing to Pak Rupee depreciation during the period, however, the company’s ability to reduce production losses kept the cost of sales in check. As a result, gross profit grew by 19.62 percent year-on-year with a marginal downtick in the GP margin to clock in at 38.69 percent in 2020.

Other income performed quite well during the year, posting a year-on-year growth of 105 percent mainly due to markup received on investment in government securities. Then there was a sharp drop in other expense as there was no unrealized loss on the re-measurement of mutual funds as against the loss of over Rs.245 million in 2019. Consequently, operating profit multiplied by 55.37 percent in 2020.

OP margin also took a sharp flight from 29.05 percent in 2019 to 36.85 percent in 2020. The company maintained a minimum leverage position and its capital structure mainly comprised of share capital and reserves. Consequently, the company flaunted a healthy interest coverage ratio of 595:1 as of 2020. Although finance cost increased during the year owing to markup on finance lease, however, it still stood at less than 0.09 percent of sales. Net profit registered staggering growth of 65.31 percent in 2020 to clock in at Rs.1276.25 million with NP margin of 26 percent and EPS of Rs.21.54

In 2021, SEPL topline grew by a paltry 2.05 percent year-on-year to clock in at Rs.5001.69 million. While sale of bank notes and security paper products remained steady during the year, the sale of passport paper drastically dropped owing to travel restrictions imposed by various countries amidst COVID-19.

Overall, sales volume of SEPL tumbled by 4 percent year-on-year to clock in at 4163 tons in 2021. High cost of production owing to increase in the prices of imported raw materials coupled with high freight cost and Pak Rupee depreciation seized the gross profit growth. GP margin inched down to 37.64 percent in 2021. Other income came to the rescue as it grew by 63.87 percent year-on-year in 2021 owing to gain on re-measurement of mutual funds on account of monetary easing.

Operating profit heightened by 10.73 percent in 2021. Unprecedented OP margin of 39.98 percent achieved during the year speaks volumes of SEPL’s superior operational performance. Finance cost also took 17 percent plunge on account of low discount rate during 2021. The bottomline grew by 14.28 percent year-on-year in 2021 to clock in at Rs. 1458.45 million with NP margin clocking in at 29.16 percent – a level never seen after 2017. EPS was recorded at Rs.24.61 in 2021.

2022 was a rather difficult year for the company. During the year, SEPL’s topline registered a marginal 2.91 percent growth to clock in at Rs.5147.26 million, while its bottomline contracted by 34.93 percent year-on-year with a considerable erosion of margins. The company achieved an offtake of 4176 tons which is merely 13 tons (or 0.3 percent) up than what it sold in 2021.

Cost of sales hiked by 12.14 percent in 2022 due to elevated prices of cotton comber, security thread and chemicals which coupled with Pak Rupee depreciation and escalation in freight cost suppressed SEPL’s gross profit by 12.38 percent in 2022. GP margin slipped to 32.05 percent in 2022. 10.34 percent increase in administrative expense in 2022 was the consequence of higher payroll expense despite contraction of workforce from 317 employees in 2021 to 301 employees in 2022.

Other income didn’t impress either and dropped by 36.62 percent year-on-year while other expense multiplied by 73.97 percent in 2022 owing to loss on the measurement of mutual funds on account of subdued capital market. All these factors translated into 29.88 percent thinner operating profit recorded by SEPL in 2022 with OP margin sinking to 27.24 percent.

Finance cost expanded due to high discount rate, bank charges and workers’ profit participation fund, however, proportionately, it still stood at 0.9 percent of sales due to equity backed capital structure. Net profit crashed by 34.93 percent year-on-year in 2022 to clock in at Rs. 949 million with EPS of Rs. 16.02 and NP margin of 18.44 percent.

In 2023, SEPL’s topline registered 12.58 percent year-on-year rise to clock in at Rs.5794.59 million. This was despite 3.1 percent year-on-year drop in sales volume which clocked in at 4048 tons. This clearly reflects that the topline appreciation was the result of upward revision in prices.

However, stronger topline couldn’t trick down to trigger any growth in gross profit which plummeted by 7.97 percent in 2023 on the back of rising international commodity prices owing to Russia-Ukraine war, unprecedented level of inflation and Pak Rupee depreciation. GP margin stooped to its lowest level of 26.20 percent in 2023. Administrative expense hiked by 12.68 percent in 2023 owing to adjustment of minimum wage rate. Number of employees fell from 301 in 2022 to 294 in 2023.

Other expense nosedived by 7.27 percent in 2023 as no loss was incurred on the re-measurement of investment in mutual funds. This offset hefty exchange loss and higher provisioning done for WWF and WPPF in 2023. Other income grew by a stupendous 81.39 percent in 2023 on account of improved profit rates on bank placements and fixed income securities.

Operating profit progressed by 10.58 percent year-on-year in 2023; however, OP margin inched down to 26.76 percent. Finance cost grew by 54.69 percent in 2023 due to increased discount rate. Imposition of super tax further diluted bottomline growth which was recorded at 1.94 percent year-on-year in 2023. Net profit stood at Rs.967.38 million in 2023 with EPS of Rs.16.33 and NP margin of 16.69 percent.

In 2024, SEPL recorded 26.18 percent year-on-year improvement in its topline which reached Rs.7311.73 million. Sales volume ticked up by a paltry 0.6 percent to clock in at 4071 tons in 2024. The growth was mainly supported by the sale of banknotes and ballot paper. Cost of sales surged by 23.11 percent in 2024 due to inflationary pressure, soaring prices of key raw materials and elevated gas and electricity prices recorded during the year.

However, the company received price adjustment on the sale of banknote paper from its key customer, Pakistan Security Printing Corporation (Pvt) Limited. This resulted in 34.84 percent stronger gross profit recorded in 2024 with GP margin defying its downward journey and ticking up to 28 percent.

Administrative expense surged by 19.86 percent in 2024 mainly on account of higher payroll expense on account of inflation. This was despite the fact that SEPL streamlined its workforce from 294 employees in 2023 to 280 employees in 2024. Other income improved by 49.31 percent in 2024 mainly on account of gain from reverse repo transactions, amortization of discount on Pakistan Investment Bond as well as mark-up recognized on Pakistan Investment Bonds and Treasury Bills. Other expense plunged by 24.74 percent in 2024 as unlike last year, the company didn’t record any exchange loss and loss on redemption of investment in mutual funds in 2024.

SEPL’s operating profit multiplied by 54.66 percent in 2024 with OP margin climbing up to 32.80 percent. Finance cost tapered off by 12.19 percent in 2024 as the company paid off its entire outstanding lease liabilities during the year. SEPL recorded 53.89 percent growth in its net profit in 2024 which clocked in at Rs.1488.68 million. This translated into EPS of Rs.25.12 and NP margin of 20.36 percent.

Recent Performance (9MFY25)

During the nine month period of the ongoing fiscal year, SEPL recorded topline growth of 9.97 percent which took its net sales to Rs.5825.20 million. Revenue from banknote paper increased during the period, however, revenue from non-commercial paper drastically declined.

Overall sales volume of the company was recorded at 2839 tons in 9MFY25 versus sales volume of 3070 recorded in 9MFY24. Cost of sales mounted by 10.81 percent during 9MFY25 due to higher utility charges as well as charges pertaining to annual plant turnaround carried out during the period.

SEPL recorded 7.79 percent uptick in its gross profit with GP margin clocking in at 27.45 percent in 9MFY25 versus GP margin of 28 percent recorded in 9MFY24. Administrative expense ticked up by 5.84 percent in 9MFY25 due to higher payroll expense. Other income dipped by 7.52 percent during 9MFY25 owing to lower discount rate.

Other expense surged by 4.92 percent probably due to higher profit related provisioning booked during the period. Operating profit ticked up by 1.73 percent in 9MFY25 with OP margin recorded at 30.75 percent versus OP margin of 33.24 percent recorded in 9MFY24. Finance cost tumbled by 62.95 percent in 9MFY25 due to monetary easing.

Net profit picked up by 1.64 percent to clock in at Rs.1100.79 million in 9MFY25. This translated into EPS of Rs.18.58 in 9MFY25 versus EPS of Rs.18.28 recorded during the same period last year. NP margin eroded from 20.45 percent in 9MFY24 to 18.90 percent in 9MFY25.

Future Outlook

With diversification and better product mix, improved prices and transfer to local raw materials, SEPL’s margins are expected to grow stronger. The company has entered into a technical consultancy agreement with a leading European Security paper company and aims to benchmark it operational efficiencies. Moreover, with SBP’s decision to introduce new currency notes to counter the issue of counterfeit notes, SEPL’s business is likely to grow further.

Recently, the company has also undertaken various projects such as renewal of its paper inspection system, development of two underground bores for the supply of sub-soil water, development of R.O plant, comber storage building project, capacity enhancement of effluent water treatment plant, installation of solar power plant etc. These projects will add to the company’s operational efficiency and reduce its cost.

Copyright Business Recorder, 2025

Comments

Comments are closed for this article.