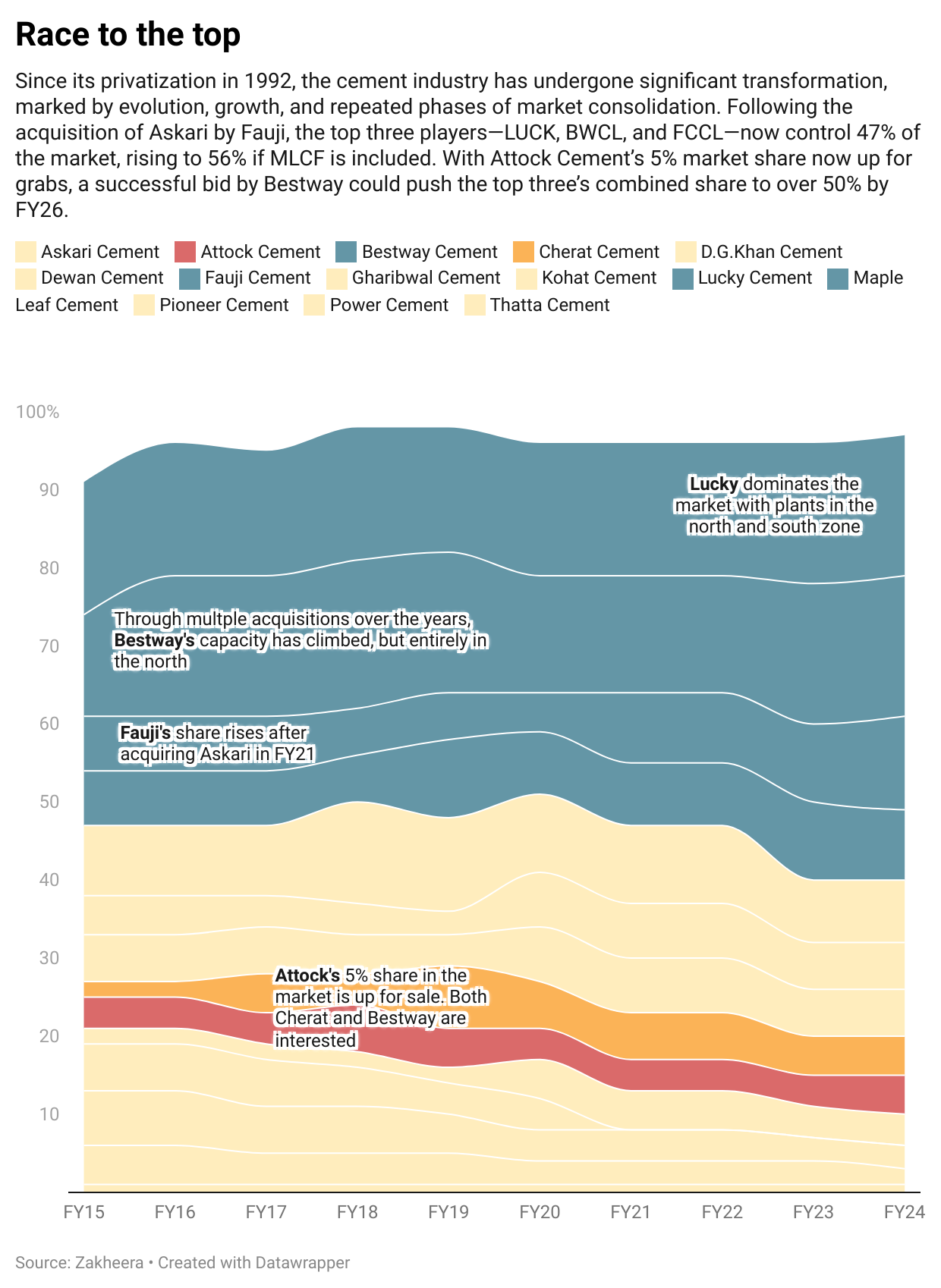

Attock Cement’s Lebanese owners want out, and the market is buzzing with interest. As a mid-sized cement plant, Attock’s financial and operational performance has also remained fairly mid-level, never performing strikingly better than peers, remaining on an average or below average position on the chart.

Recently, the company has made strategic investments to expand its capacity, and reduce its power costs which has brought down the costs of production compared to previous periods and expanded market share by capacity. In FY24, the company improved its capacity utilization to 68 percent (FY24: 65%) at a time when the industry capacity utilization had dropped to 53 percent.

This was made possible by selling much more clinker to markets overseas. Maybe the company did not fetch the most competitive rates on these exports, but it was able to improve its profitability; net margins up from just 5 percent (FY23) to 12.5 percent in FY24. This was higher than Mapleleaf, Fauji and DGKC in that year.

Having said that, Attock has had financial hiccups, maintaining a weak financial performance over the years. But one could argue that with better management, the plant's inherent advantages could be better leveraged, and operational efficiencies improved to unlock its unrealized potential.

Attock has solidified its presence in the domestic markets. Its Falcon brand is known locally by name, and it has created channels in the global network which could be attractive to a potential investor.

Attock’s exports share has grown from 10 percent in FY15 to 21 percent and 22 percent during FY19 and FY20 and back down to 15 percent in FY24. When the global market is more receptive, and pricing is competitive, Attock has gained favourablemarket access abroad. In FY20, when profitability of the entire industry declined, Attock was one of the few companies whose after-tax profits remained intact.

Given the location advantage, Attock could be a strategic investment for a company like Bestway that has extensive experience in acquisitions and has been expanding its market share by owning several plants in various locations, this investment would perhaps be the most strategic.

While Bestway near dominates the market by capacity, locking the position with Lucky, its profits are nowhere near the latter. Perhaps what Bestway needs is a presence in the south and access to clinker exports markets whilst retaining its position in the north zone of the country.

But Bestway would have to outbid Cherat, a mid-sized player with solid financials or another contenderaltogether in the form of Kot Addu Power Company, a large Independent Power Producer that is considering a consortium bid with Fauji Cement that recently acquired Askari.

For either of these cement players: Cherat, Bestway or Fauji, this could turn into a rewarding investment as all three of these players are seasoned and know how to run a cement plant, profitably.Investors and markets however, will be keener on seeing how a new management could squeeze a better financial performance out of Attock given all its latent potential.

Comments

Comments are closed for this article.