Dynea Pakistan Limited (PSX: DYNO) was incorporated in Pakistan as a public limited company in 1982. The principal activity of the company is the manufacturing and sale of formaldehyde, urea/melamine formaldehyde and molding compound.

Pattern of Shareholding

As of June 30, 2024, DYNO had a total of 18.872 million shares outstanding which are held by 1523 shareholders. Foreign investors have the majority stake of 26.08 percent in the company followed by AICA Asia Pacific holding Pte Limited, a related party of DYNO, holding 24.99 percent of its shares.

Local individuals account for 22.66 percent of the outstanding shares of DYNO followed by Mutual funds with 12.35percent shares. Joint stock companies hold 9.46percent shares of DYNO while Banks, DFIs and NBFIs hold 3.31 percent shares. The remaining shares are held by other categories of shareholders.

Historical Performance (2019-24)

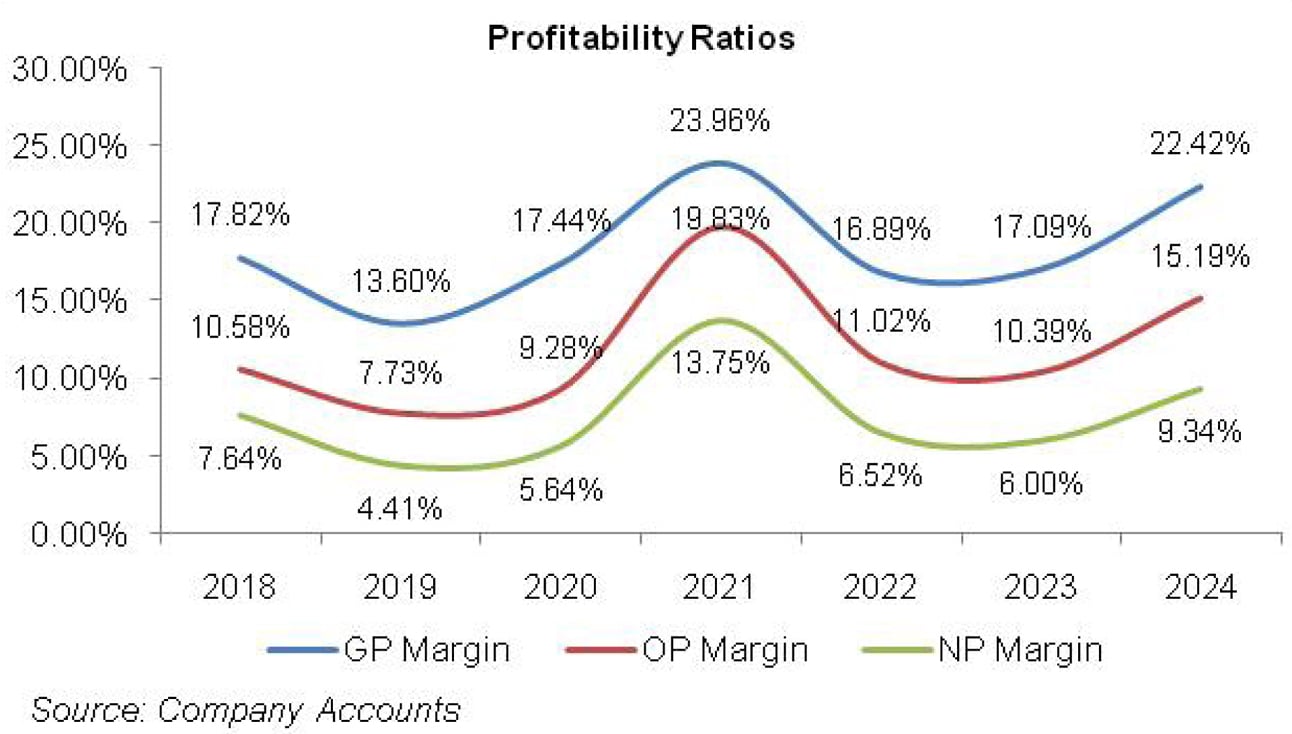

During the period under consideration, DYNO’s topline dipped only in 2020, however, its bottomline plunged twice i.e. in 2019 and 2022. DYNO’s margins nosedived in 2019 followed by a recovery witnessed for the two successive years before slipping again in 2022. In 2023, gross margin slightly ticked up while operating and net margins continued to fall. All the margins posted a staggering rebound in 2024. The detailed performance review of the period under consideration is given below.

In 2019, DYNO’s net revenue posted 33.22 percent year-on-year rise to clock in at Rs.5140.03 million. This was on account of 15.21 percent growth in the turnover of resin division and 56.05 percent growth in the turnover of molding compound division. The resin division of the company operated at 59 percent capacity in 2019 versus 60 percent capacity utilization recorded in 2018.

Conversely, the actual production of molding compound division stood at 110 percent of the rated capacity in 2019 versus 87 percent capacity utilization recorded in 2018.Steep depreciation of Pak Rupee and rise in raw material and energy prices pushed the cost of sales up by 40 percent during the year.

While DYNO’s gross profit in 2019 was 1.63 percent higher than that in 2018; GP margin tumbled from 17.82 percent in 2018 to 13.60 percent in 2019. Distribution expense dropped by 7.75 percent year-on-year in 2019 on account of lower freight charges as well as curtailed sales promotion expense. Conversely, administrative expense grew by 19.30 percent year-on-year in 2019 which was the result of higher payroll expense caused by high inflation.

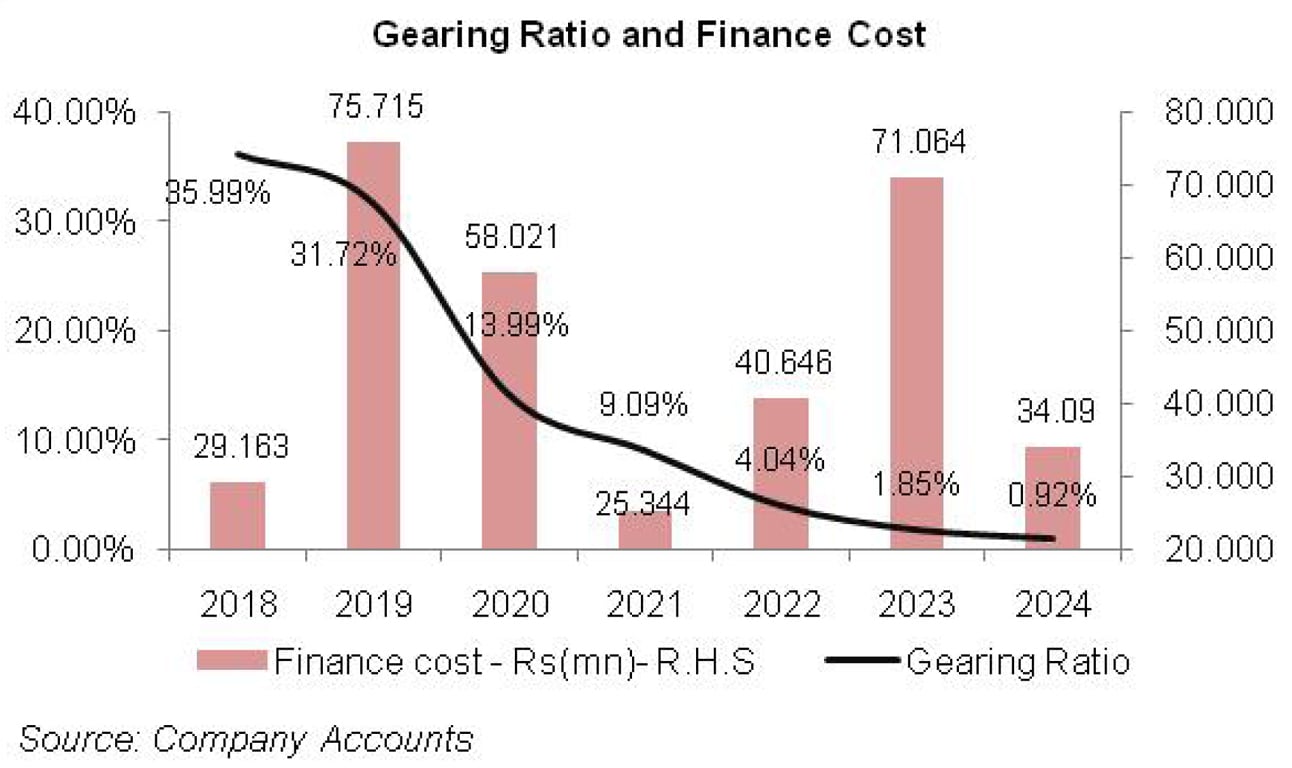

Operating profit posted 2.71 percent decline in 2019 translating into OP margin of 7.73 percent versus OP margin of 10.58 percent recorded in 2018. Finance cost posted 159.63 percent growth in 2019 due to higher discount rate. All these factors resulted in 23 percent year-on-year shrinkage in DYNO’s net profit in 2019. Net profit clockedin at Rs.226.90 million in 2019.

DYNO recordedNP margin of 4.41 percent in 2019 versus NP margin of 7.64 percent recorded in 2018. EPS also slid from Rs.15.63 in 2018 to Rs.12.02 in 2019.

In 2020, DYNO’s topline registered 12.60 percent year-on-year decline to clock in at Rs.4492.45 million. Owing todeceleration of economic activity due to COVID-19, construction and allied industries also came to a standstill. Consequently, the turnover of both resin and molding compound division nosedived by 22.7 percent and 3.14 percent respectively in 2020.

Weak demand was also evident in the curtailed capacity utilization of both the plants of DYNO during the year. In 2020, resin segment operated at 47.5 percent capacity versus 59 percent capacity utilization recorded in 2019.Molding compound division operated at 99 percent capacity versus capacity utilization of 110 percent posted in 2019.

Cost of sales dropped by 16.48 percent year-on-year which drove gross profit up by 12 percent year-on-year in 2020. GP margin also grew to 17.4 percent during the year. Lower cartage and freight charges on account of drop in sales volume translated into 8.93 percent year-on-year dip in distribution expense. Conversely, administrative expense remained constant during the year.

During the year, DYNO also booked provision of Rs.95.59 million against expected credit losses (ECL). This was due to depressed economic activity which increased the probability of non-payments on trade debts. The provision against ECL booked in 2020 was 696.20 percent higher than the provision booked in 2019.

Cost optimization and operational efficiency enabled DYNO to attain 4.91 percent higher operating profit and OP margin of 9.28 percent despite depressed sales in 2020.

Finance cost also buttressed the bottomline as it dwindled by 23.37 percent year-on-year in 2020 which was the consequence of a significant reduction in borrowings. Net profit rose by 11.66 percent year-on-year in 2020 to clock in at Rs.253.35 million with NP margin of 5.64 percent and EPS of Rs.13.42.

2021 appears to be a rejuvenating year for DYNO where it recovered from the scars of the previous year and posted a robust 51.97 percent year-on-year growth in its topline which jumped up to Rs.6827.20 million. Both resin and molding compound division posted a rebound in their net revenue to the tune of 39.03 percent and 61.63 percent respectively in 2021.

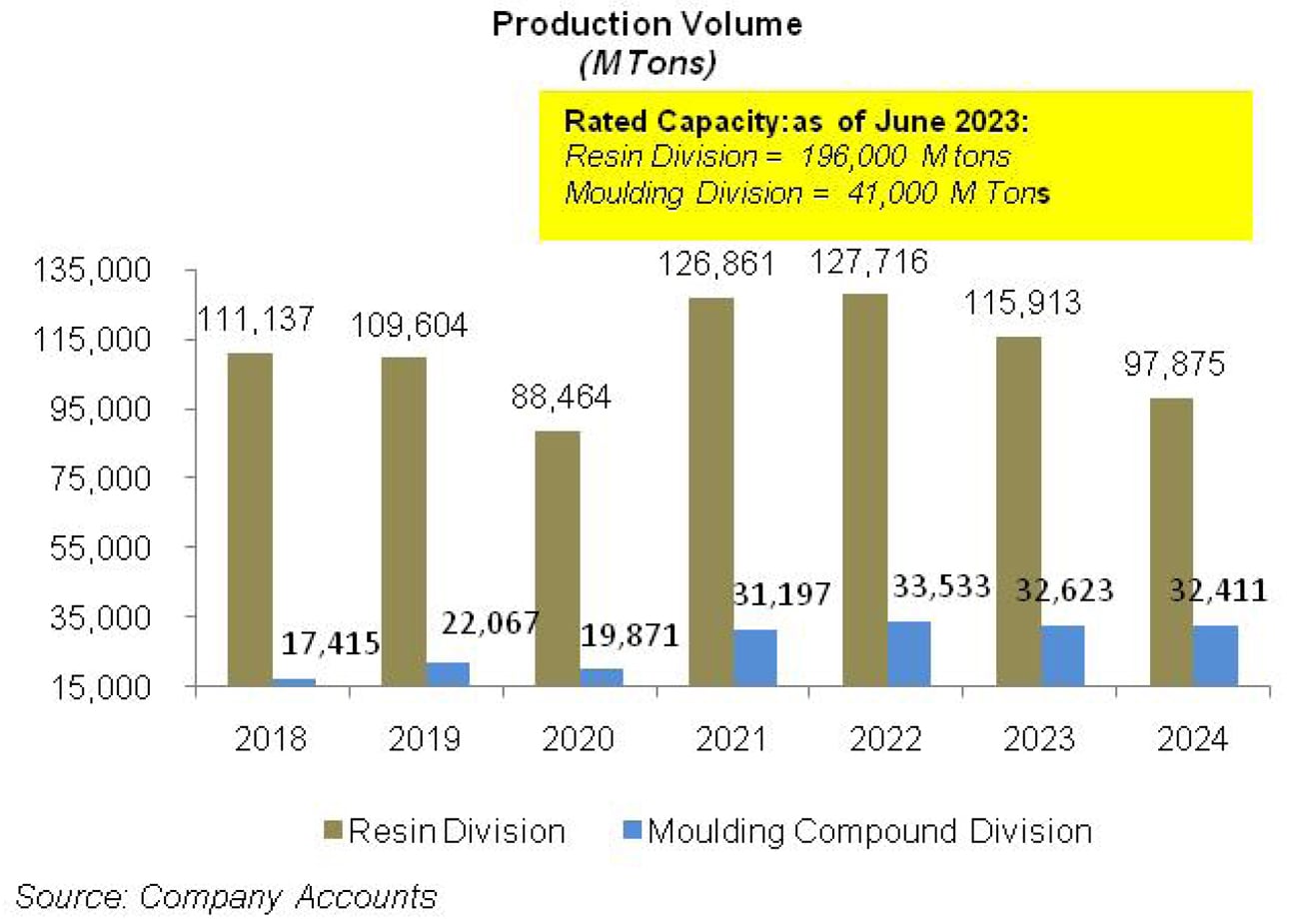

The company also increased its molding compound capacity from 20,000 MT in 2020 to 35,000 MT in 2021 and operated at 89 percent capacity. Resin plant also operated at an enhanced capacity of 68 percent in 2021 to meet the rising demand which was the result of recovery in the construction and allied industries.

Cost of sales grew by 39.96 percent year-on-year, resulting in 108.83 percent growth in gross profit in 2021. GP margin posted its optimum value of 23.96 percent in 2021.

Higher payroll expense was incurred in 2021 due to an increase in the size of workforce in line withmolding compound segment’s expansion. This resulted in 32.48 percent year-on-year hike in administrative expense in 2021.

Distribution expense also posted 39.35 percent year-on-year spike in 2021 on account of higher cartage and freight charges. As against previous years, in 2021, the company booked reversals of Rs.111.31 million against ECL. Some noticeable movement was also observed in the other expense and other income account in 2021.

Other expense grew by 159.73 percent year-on-year to stand at 1.4 percent of the net revenue in 2021 as against its standing of 0.8 percent in the previous year. This was due to massive provisioning for WWF and WPPF booked during the year.

Other income also grew by 285.36 percent year-on-year to stand at 0.5 percent of DYNO’s net sales in 2021 as against 0.2 percent in 2020. This was primarily on account of profit on saving accounts as well as exchange gain.

Operating profit grew by 224.97 percent year-on-year in 2021 with OP margin touching a new height of 19.83 percent. Finance cost slid by 56.32 percent year-on-year in 2021 due to lower discount rate and lower external financing obtained during the year.

Net profit multiplied by 270.47 percent year-on-year in 2021 to clock in at Rs.938.61 million with NP margin of 13.75 percent and EPS of Rs.49.73.

The growth trajectory continued in 2022 with 39.68 percent year-on-year growth recorded in topline. DYNO’s topline clocked in at Rs.9,536.32 million in 2022. This was backed by 58 percent year-on-year growth in the turnover of resin division and 28 percent year-on-year growth in the turnover of molding compound division. To meet the growing demand, the company increased the capacity of resin division from 186,000 MT to 196,000 and operated at 65 percent capacity.

Molding compound division also witnessed capacity enhancement from 35,000 MT to 41,000 MT with capacity utilization of 81.78 percent recorded during the year. 2022 came with its own baggage of challenges whereby not only did the prices of raw materials hiked in the international market, Pak Rupee depreciation made the matters even worse. To top it off import restrictions were imposed due to dwindling foreign exchange reserves of the country.

High local inflation, energy price hikes as well as high discount rate and taxation greatly suppressed the business sentiments. Cost of sales grew by 52.66 percent year-on-year, pushing the gross profit down by 1.51 percent in 2022. GP margin also slipped to 16.89 percent in 2022 from 23.96 percent in the previous year.

Distribution and administrative expense grew by 30.22 percent and 19.81 percent respectively in 2022 not only because of expansion in the size of business and increased yearly off-take but also on account of unprecedented level of inflation.

Operating profit shrank by 22.40 percent year-on-year in 2022 with OP margin ticking down to 11 percent. Despite lesser borrowings, high discount rate resulted in 60.38 percent hike in finance cost. This pushed net profit down by 33.78 percent year-on-year to clock in at Rs.621.50 million in 2022 with NP margin of 6.52 percent and EPS of Rs.32.93.

In 2023, DYNO’s net sales grew by 16.19 percent year-on-year to clock in at Rs.11,080.44 million. Thiswas on the back of 6.3 percent rise in the turnover of resin division and 24.06 percent growth in the turnover of molding compound division in 2023.

During the year, the company also commenced its export business and recorded export sales of Rs.45.276 million. Cost of sales escalated by 15.92 percent in 2023 due to surge in the prices of raw materials, high conversion cost due to soaring inflation as well as Pak Rupee depreciation.

However, with better prices, the company was able to register 17.54 percent rise in its gross profit in 2023 with GP margin slightly inching up to clock in at 17.1 percent. Distribution expense escalated by 28.1 percent in 2023 due to higher cartage & freight charges.

Administrative expense also spiked by 28 percent in 2023 on the back of higher payroll expense and amortization expense. Workforce was squeezed to 227 employees in 2023 versus 231 employees in 2022.

Higher profit related provisioning and exchange loss resulted in 97.19 percent spike in other expense in 2023. Other income grew by 187.97 percent in 2023 due to hefty profit earned on deposit and saving accounts.

Operating profit improved by 9.54 percent in 2023 with OP margin sliding down to 10.39 percent. Finance cost multiplied by 74.83 percent in 2023 due to higher discount rate while outstanding borrowings significantly reduced during the year. DYNO’s gearing ratio inched down from 4.04 percent in 2022 to 1.85 percent in 2023. Net profit strengthened by 7 percent to clock in at Rs.665.16 million in 2023 with EPS of Rs.35.25 and NP margin of 6 percent.

In 2024, DYNO’s topline ascended by 15.16 percent year-on-year to clock in at Rs.12,759.90 million. During the year, the turnover of resin division dwindled by 4.5 percent while the turnover of molding compound division registered 28.6 percent increase during the year.

Export sales tremendously grew during the year to the tune of 1379.58 percent to clock in at Rs. 669.908 million. Cost of sales grew by 7.75 percent in 2024. Improved prices, greater export salesand cost cutting measures employed during the year such as installation of solar plant resulted in 51 percent higher gross profit in 2024 with GP margin clocking in at 22.42 percent.

Distribution expense inched up by 7.81 percent in 2024 owing to higher salaries of sales force as well as elevated travelling & conveyance and repair & maintenance charges incurred during the year.

Administrative expense surged by a massive 69.47 percent in 2024 due to higher payroll expense on account of inflationary pressure as well as workforce enhancement from 227 employees in 2023 to 230 employees in 2024. The company also booked provision of Rs.192.29 million in 2024 versus reversal of Rs.10.92 million booked in 2023.

Other expense slid by 36.45 percent in 2024due to relatively stable value of Pak Rupee which resulted in lower exchange loss. Other income strengthened by 192.73 percent in 2024 due to higher profit on bank deposits as well as gain recognized on the disposal of operating fixed assets. Operating profit improved by 68.42 percent in 2024 with OP margin clocking in at 15.19 percent.

Finance cost tapered off by 52 percent in 2024 due to lower outstanding borrowings. Net profit multiplied by 79.13 percent to clock in at Rs.1191.51 million in 2024. This translated into EPS of Rs.63.13 and NP margin of 9.34 percent in 2024.

Recent Performance (9MFY25)

During 9MFY25, DYNO’s topline recorded year-on-year decline of 5.27 percent to clock in at Rs.9736.38 million. This was on account of a dip in local sales during the period. Export sales continued to pick up during 9MFY25, however, stood at only 6.63 percent of the DYNO’s net sales.

During the period under consideration, the company started exporting to Kenya. Net turnover of the Resin division fell by 21.29 percent during 9MFY25 while net sales of the molding compound division posted year-on-year rise of 3.44 percent. Despite lower net sales, cost of sales ticked up by 1.73 percent in 9MFY25 due to inflationary pressure and high energy tariff. This resulted in 27.84 percent drop in gross profit in 9MFY25 with GP margin clocking in at 18 percent versus GP margin of 23.70 percent recorded in 9MFY24.

Distribution expense mounted by 16.14 percent in 9MFY25 seemingly due to higher salaries of sales force and increased freight & cartage charges incurred during the period. Administrative expense ticked up by 7 percent during the period under consideration which predominantly represents higher payroll expense.

DYNO booked reversal worth Rs.21.51 million of provision booked against ECL in 9MFY25. This was against the provision of Rs.94.66 million booked during the same period last year. Lower profit related provisioning resulted in 25.47 percent plunge in other expense in 9MFY25.

Other income also ticked down by 2.22 percent during the period under consideration due to lower profit recognized on saving deposits on account of monetary easing.

DYNO recorded 33.83 percent erosion in its operating profit in 9MFY25 with OP margin recorded at 11.85 percent versus OP margin of 16.96 percent recorded in 9MFY24.

Despite lower discount rate, finance cost surged by 28 percent during 9MFY25. This was due to additional running finance obtained during the period. DYNO’s net profit dwindled by 35.69 percent to clock in at Rs.691.10 million in 9MFY25. This translated into EPS of Rs.36.62 in 9MFY25 versus EPS of Rs.56.94 recorded in 9MFY24. NP margin also fell from 10.46 percent in 9MFY24 to 7.10 percent in 9MFY25.

Future Outlook

DYNO’s expansion into export market will not only improve its turnover and margins but will help in minimizing exchange losses incurred on the purchase of raw materials from the international market.

Moreover, reduction in financial charges due to lower discount rate will also buttress its bottomline. Improvement in local economic dynamics will also fuel demand.

Comments

Comments are closed for this article.