Hi-Tech Lubricants Limited (PSX: HTL) is incorporated in Pakistan as a public limited company.

The company is engaged in the procurement and distribution of lubricants and petroleum products.

In 2017, the company was granted a license by OGRA to establish an OMC and in 2019, the company received permission to operate new storage facility at Sahiwal and to distribute petroleum products in the province of Punjab under the brand name of HTL fuel stations.

HTL products are largely sold under the brand name “ZIC” which are available at over 20,000 retail outlets and wash stations across the country. In 2017, the company stepped into retail industry and established HTL Express Centers which provide one-stop vehicle maintenance solution. Later, HTL adopted franchise model for its Express Centers.

Pattern of Shareholding

As of June 30, 2024, HTL has a total of 139.205 million shares outstanding which are held by 5,403 shareholders. Directors, their spouse and minor children have the majority stake of 69.10 percent in the company followed by local general public holding 18.10 percent shares of HTL.

Associated companies, undertakings and related parties account for 7.37 percent of the outstanding shares of HTL. The remaining shares are held by other categories of shareholders.

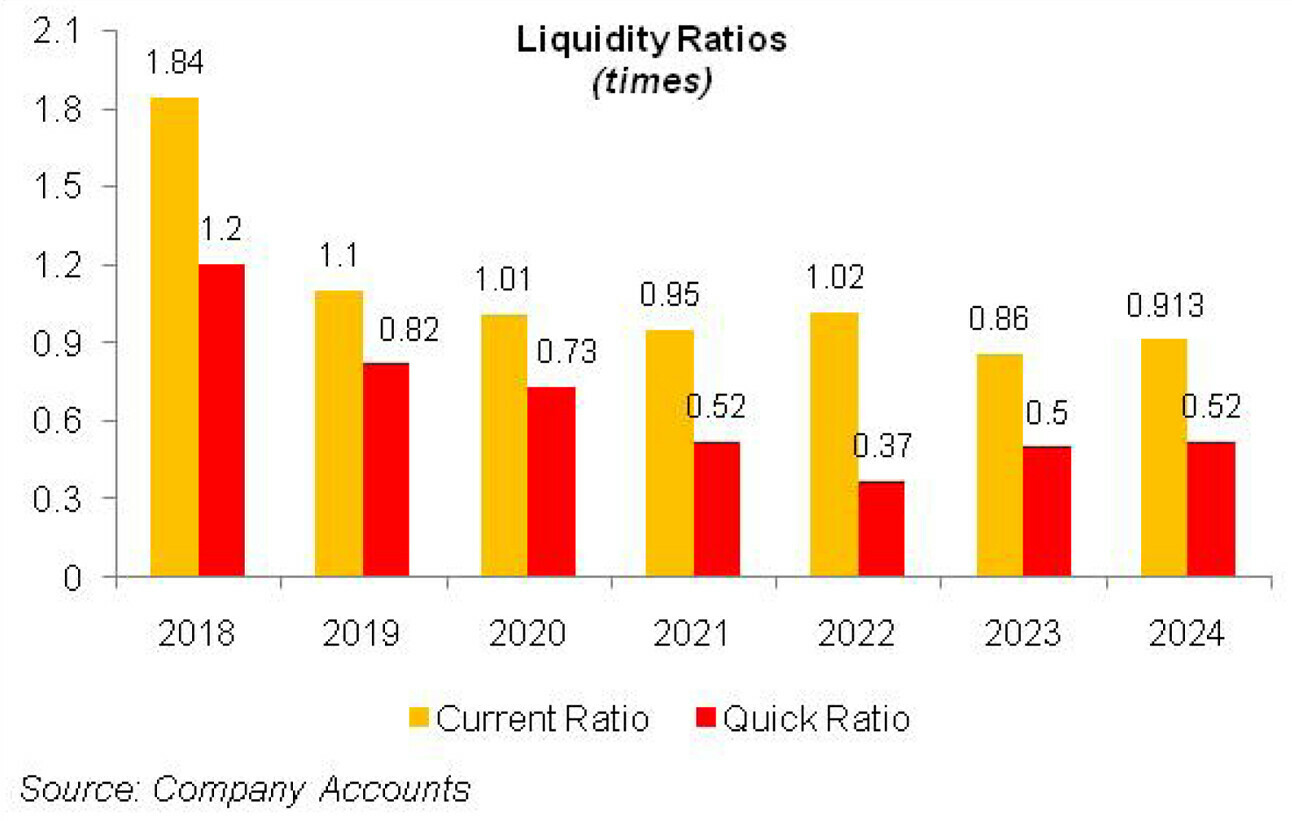

Historical Performance (2019-24)

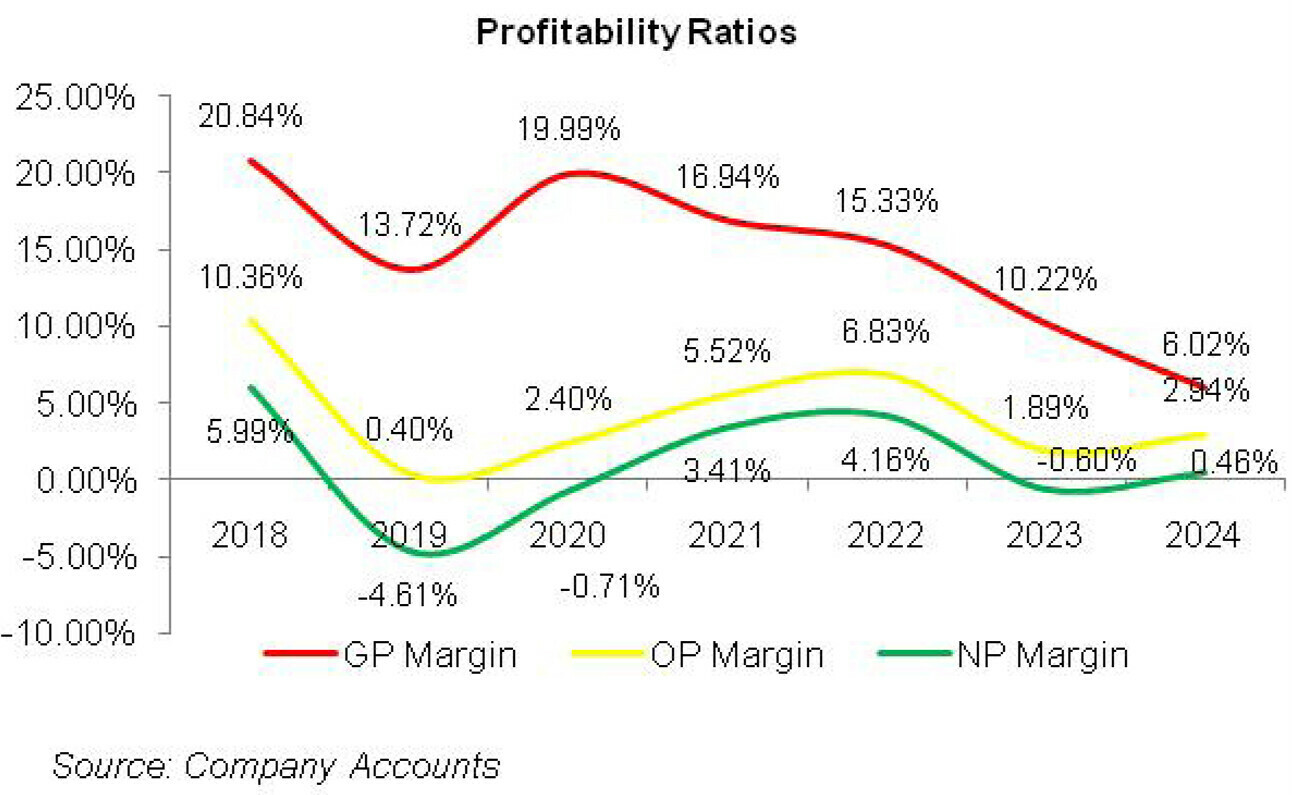

Except for a drop in 2020 and 2023, the sales of HTL posted growth over the period under consideration. Conversely, the company posted net losses in 2019, 2020 and 2023. The gross margin of the company after experiencing a dip in 2019, recovered in 2020 however started tapering off in the subsequent years to clock in at its lowest level in 2024.

Conversely, operating margin and net profit margin of HTL posted a plunge in 2019 then took a flight until 2022 followed by a drastic fall in 2023. In 2024, operating and net margins ticked up. The detailed performance review of each of the period consideration is given below.

In 2019, HTL’s topline posted a marginal year-on-year growth of 1.92 percent to clock in at Rs.9431.16 million. This was on the back of price increase while sales volume was down by 4 percent year-on-year.

Low demand in 2019 was on account of high inflation and discount rate which not only pushed up the cost of doing business for the companies but also restricted the consumers from spending on vehicle related products and services. This halted the sales of lubricants as well as HTL Express Centers in 2019.

Cost of sales grew by 11 percent year-on-year in 2019 on account of Pak Rupee depreciation as well as import overhead cost. This translated into 32.88 percent year-on-year decline in gross profit with GP margin radically plunging to 13.72 percent in 2019 from GP margin of 20.84 percent recorded in 2018.

Distribution expense grew by 31.21 percent year-on-year in 2019 mainly on account of increase in advertisement and sales promotion in 2019 coupled with higher salaries of sales force. Administrative expense also inched up by 14.22 percent year-on-year in 2019, reflecting high inflation.

Higher exchange loss on account of Pak Rupee depreciation, massive jump in allowance booked for expected credit losses, slow moving and damaged inventory items as well as doubtful advances to suppliers translated into 64.21 percent year-on-year spike in other expense in 2019.

Other income posted a meager 5 percent year-on-year growth primarily on the back of higher profit on bank deposits, credit balances written back as well as scraps sales. Operating profit shrank by 96 percent year-on-year in 2019 with OP margin sliding down to 0.4 percent in 2019 from OP margin of 10.36 percent recorded in 2018.

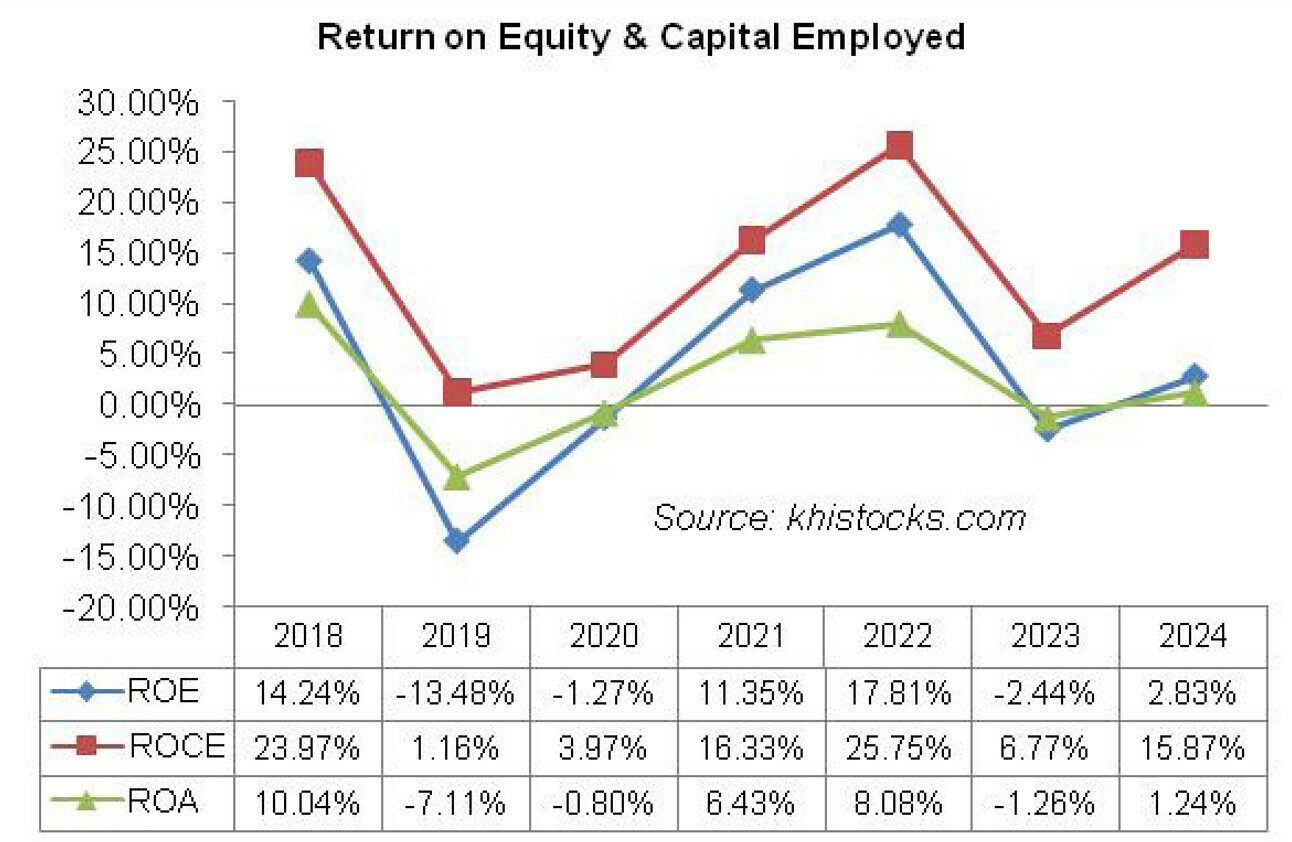

Finance cost magnified by 184.79 percent year-on-year in 2019 due to high discount rate and also because of a substantial rise in borrowings in 2019. HTL’s debt-to-equity ratio rose from 18.14 percent in 2018 to 39.13 percent in 2019.

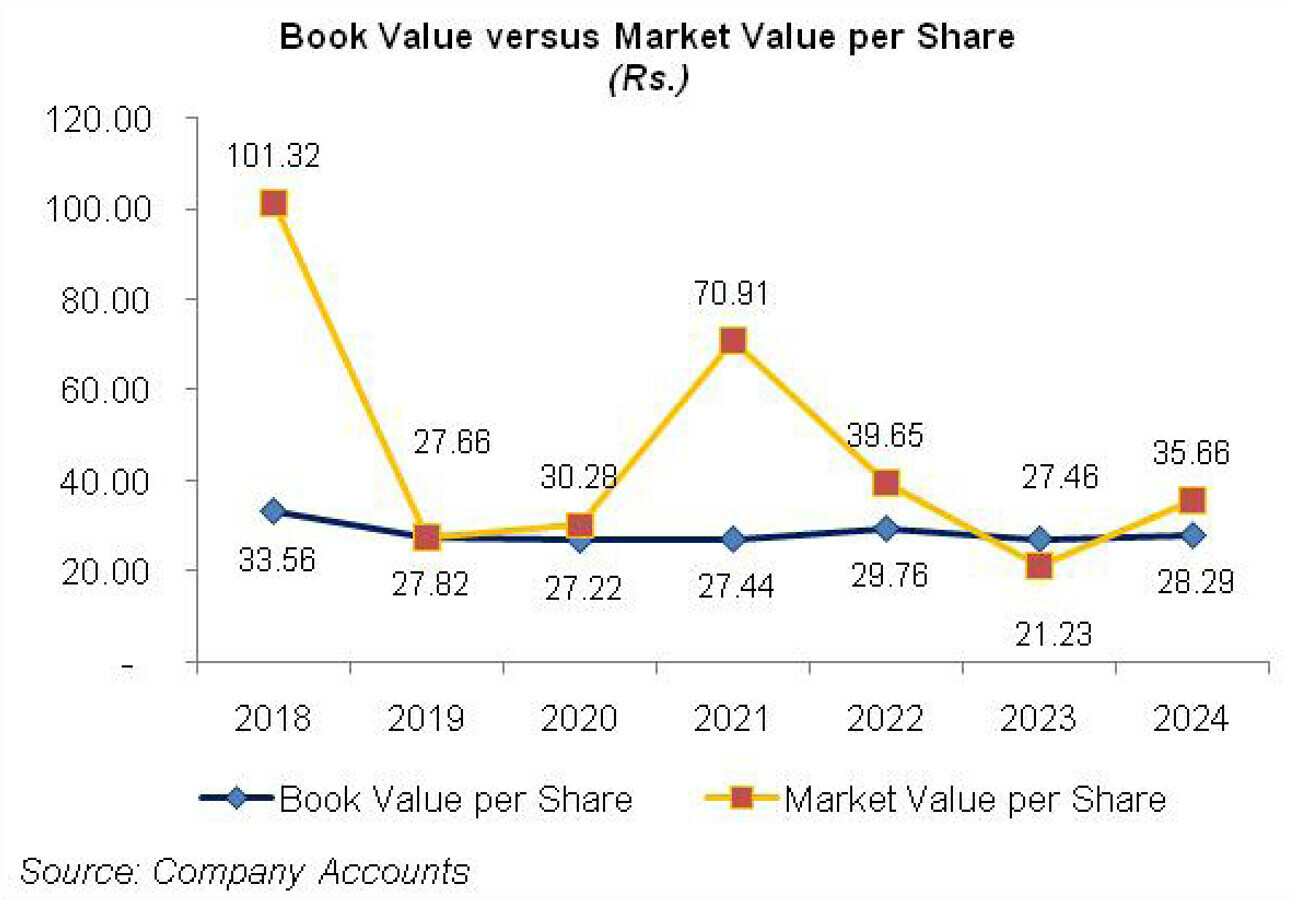

High finance cost resulted in a negative bottomline of Rs.434.81 million in 2019 with loss per share of Rs.3.75 as against net profit of Rs.554.43 million and EPS of Rs.4.78 posted in 2018.

In 2020, HTL’s topline slumped by 40.32 percent year-on-year to clock in at Rs.5628.66 million. The year began with low GDP growth and ended with COVID-19 pandemic bringing the economic activities at a standstill. While sales revenue from lubricants dropped in 2020, sales revenue from spare parts sales, services at HTL Express Centers, dispensing pumps and petroleum products performed well in 2020.

Lower sales volume pushed cost of sales down by 44.65 percent year-on-year in 2020. GP margin improved to 20 percent due to better prices and sales mix.

Lower freight charges as well as curtailment in advertising and promotion expense trimmed the distribution cost down by 14.47 percent year-on-year in 2020.

Administrative expense also inched down by 11.88 percent year-on-year mainly on account of low payroll expense as the company reduced its permanent employees from 366 in 2019 to 335 in 2020.

Other expense posted a nosedive of 76.36 percent year-on-year in 2020 particularly as the company didn’t book any allowance for expected credit losses in 2020 and also because the company didn’t incur any exchange loss unlike the previous year.

Other income grew by 13.85 percent year-on-year in 2020 due to reversals booked against expected credit losses, higher dividend income and profit on bank deposits as well as exchange gain earned in 2020.

All these factors resulted in 258.31 percent year-on-year rise in operating profit while OP margin jumped up to 2.40 percent in 2020. Although finance cost dwindled by 20.74 percent year-on-year in 2020 due to significant reduction in HTL’s short-term loans, yet finance cost of Rs.186.33 million was huge enough to produce net loss of Rs. 40.12 million and loss per share of Rs.0.35 in 2020. HTL’s net loss shrank by 90.77 percent year-on-year in 2020.

After two successive years of lackluster sales and net losses, HTL’s topline grew by a massive 88.29 percent year-on-year in 2021to clock in at Rs.10,598.21 million. This came on account of resurfacing of the demand that was restricted during the COVID period. The sale revenue from petroleum products posted an impressive growth of 6.5 times in 2021.

The revenue from lubricants almost doubled during 2021. Conversely, services at HTL Express Centers and sale of dispensing pumps weren’t encouraging in 2021. Cost of sales grew by 95.45 percent year-on-year.

While gross profit surged by 59.63 percent in 2021, GP margin climbed down to 16.94 percent. Distribution and administrative cost grew by 13.86 percent and 23.15 percent year-on-year respectively in 2021 mainly on account of rise in revenue lines and higher payroll expense as number of employees grew to 383 in 2021 from 335 in 2020.

Other expense grew by 68.56 percent year-on-year in 2021 on account of higher charities and donations, receivables written off during the year as well as allowance booked for expected credit losses. Other income slid by 13.21 percent year-on-year as lower discount rate trimmed down HTL’s profit on bank deposits.

Operating profit grew by 332.60 percent in 2021 with OP margin climbing up to 5.52 percent. Significantly lower short-term borrowings during the year coupled with monetary easing resulted in 56.45 percent year-on-year drop in finance cost in 2021.

HTL was able to post net profit of Rs.361.32 million in 2021 with NP margin of 3.41 percent. EPS clocked in at Rs.2.60 in 2021.

In 2022, HTL mustered 67.38 percent year-on-year growth in its net sales which clocked in at Rs. 17,739.04 million. This was because the company expanded its distribution channels and invested in its brands. Sales revenue from lubricants, petroleum products, dispensing pumps as well as franchise and joining fee increased during the year.

Cost of sales grew by 70.62 percent year-on-year on the back of inflation and Pak Rupee depreciation. This drove GP margin down to 15.33 percent in 2022 despite 51.47 percent year-on-year growth in gross profit in 2022. Higher salaries, freight expense, advertising expense as well as utilities expense pushed up the distribution and administrative expense by 34.41 percent and 20 percent respectively in 2022.

Other expense grew by an exorbitant 471.92 percent in 2022 due to massive exchange loss borne by the company during the year coupled with higher provisioning done for WWF and WPPF.

However, other expense was offset by 240.15 percent year-on-year rise in other income due to handsome dividend income from the subsidiary company, Hi-Tech Blending (Private) Limited. This resulted in 106.96 percent year-on-year rise in operating profit with OP margin climbing up to 6.83 percent in 2022.

Finance cost mounted by 140.94 percent year-on-year in 2022 due to higher discount rate coupled with high short-term loans obtained during the year. This coupled with the imposition of super tax and recognition of deferred tax liabilities diluted the growth of bottomline.

Yet, net profit rose by 104.23 percent year-on-year in 2022 to clock in at Rs.737.92 million with NP margin of 4.16 percent. EPS grew to Rs. 5.3 in 2022.

During 2023, HTL’s topline went down by 12.44 percent to clock in at Rs.15,531.69 million. This was on account of decline in sales revenue from lubricants and petroleum products.

Lackluster sales performance of the key products of HTL counterbalanced higher sales revenue from dispensing pumps, high franchising and joining fee earned during the year and the sale of packing materials, spare parts and base oil to Hi-Tech Blending (Private) Limited, a subsidiary company of HTL.

Pak Rupee depreciation as well as rise in the commodity prices due to Russia-Ukraine crisis didn’t allow the cost to drop by the same proportion, resulting in 41.66 percent lower gross profit recorded in 2023. GP margin also fell down to 10.22 percent in 2023. Distribution expense inched down by 4.48 percent year-on-year in 2023 due to considerably lower freight, sales promotion and advertising expense incurred during the year.

Administrative expense expanded by 27.55 percent during 2023 due to higher payroll expense despite the fact that the company streamlined its workforce to 478 employees, down from 530 employees in 2022.

Other expense shrank by 84.69 percent in 2023 due to considerably lower exchange loss incurred during the year coupled with no provisioning made for WWF, WPPF and doubtful advances to suppliers. Other income strengthened by 31.95 percent in 2023 due to higher dividend income which primarily includes dividend received from Hi-Tech Blending (Private) Limited. Interest on short-term loans to subsidiary, credit balances written back and income from storage & handling services also buttressed other income in 2023.

Operating profit slid by 75.76 percent in 2023, translating into OP margin of 1.89 percent.

Finance cost mounted by 142.75 percent in 2023 due to high discount rate and increased borrowings which culminated into gearing ratio of 34.43 percent in 2023 versus gearing ratio of 28.71 percent posted in 2022. HTL ended up posting net loss of Rs.93.41 million in 2023 with loss per share of Rs.0.67.

HTL’s net sales grew by 54.63 percent in 2024 to clock in at Rs.24,016.48 million. The growth was backed by favorable sales mix as well as price management initiatives which buttressed the demand of company’s products.

However, high cost of sales due to Pak Rupee depreciation and fluctuations in the prices of international commodities pushed gross profit down by 8.95 percent in 2024 with GP margin falling down to 6 percent.

Distribution expense ticked down by 2.38 percent in 2024 due to lower salaries of sales force. Administrative expense largely remained intact at the last year’s level. Other expense mounted by 50.95 percent in 2024 due to fixed assets written off, advances to suppliers written off and higher allowance for ECL booked during the year.

Other income posted a tremendous 109.56 percent improvement in 2024 due to robust dividend income received from Hi-Tech Blending (Private) Limited and promotional incentive recognized from SK Enmove Co.

Limited, a principal supplier and long-term partner of HTL. The company recorded 140.75 percent year-on-year growth in its operating profit in 2024 with its OP margin ticking up to 2.94 percent. Finance cost surged by 14.63 percent in 2024 due to higher discount rate. HTL posted net profit of Rs.111.40 million in 2024 with EPS of Rs.0.8 and NP margin of 0.46 percent.

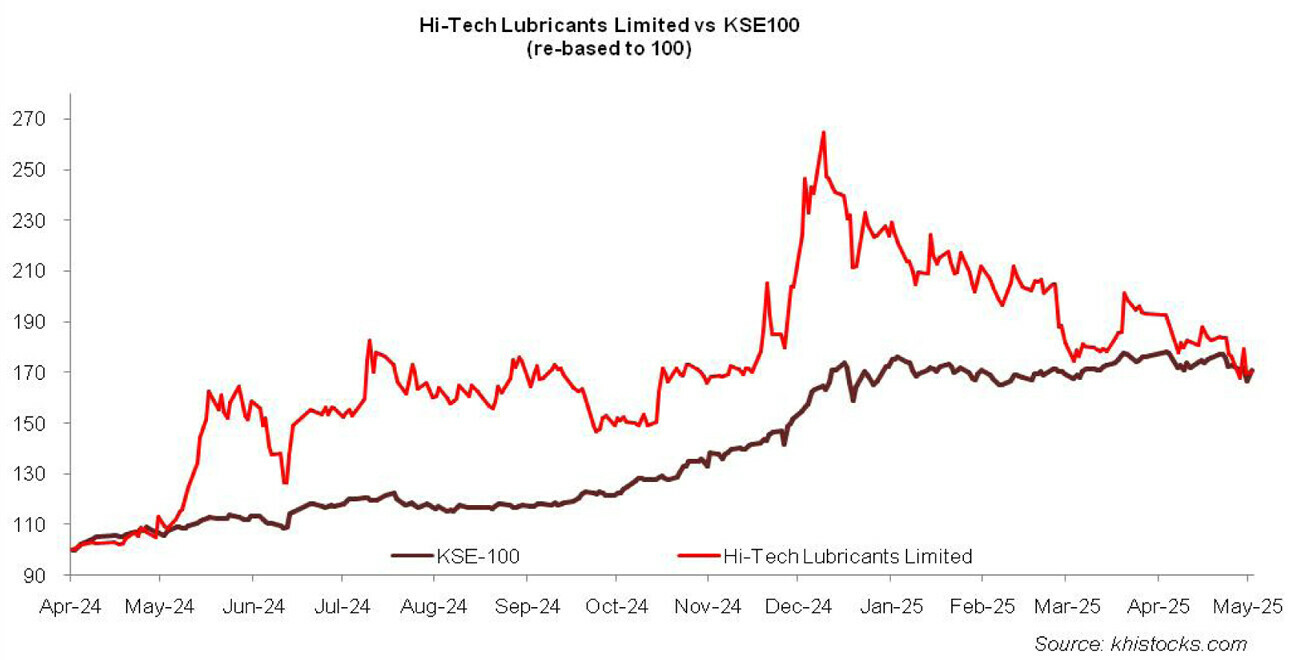

Recent Performance (9MFY25)

During 9MFY25, HTL registered year-on-year growth of 52.52 percent in its topline which clocked in at Rs.23,950.62 million. This was on account of growth in the company’s product portfolios which include lubricants and fuel. Not only did the company increased its range of locally blended products but also recorded profitability from both OMC and polymer segments. Increased localization resulted in gross profit picking up by 70 percent in 9MFY25 with GP margin clocking in at 6.24 percent versus GP margin of 5.60 percent recorded in 9MFY25.

Increased sales volume resulted in 38.43 percent spike in distribution expense in 9MFY25. Administrative expense ticked up by 8.30 percent in 9MFY25 due to inflationary pressure. Other expense surged by 54.84 percent in 9MFY25 probably due to higher allowance for ECL booked during the period. Other income fell by 72.61 percent seemingly due to lower dividend income.

HTL registered 70 percent thinner operating profit in 9MFY25 with OP margin falling down to 0.66 percent versus OP margin of 3.38 percent recorded in 9MFY24.

Finance cost dwindled by 18.29 percent in 9MFY25 due to lower discount rate and lesser borrowings. HTL posted net loss of Rs.286.59 million with loss per share of Rs.2.06 in 9MFY25. This was against net profit of Rs.58.927 million and EPS of Rs.0.42 recorded in 9MFY24.

Future Outlook

The gradual recovery of automobile sector particularly growth in the sale of hybrid cars and motor cycles, increase in HTL branded fuel stations and the government’s initiatives to control the smuggling of fuel warrant increase in the demand for HTL products. Besides, the company is also eyeing to expand its outreach in export market by leveraging its strategic partnership with SK Enmove.

Copyright Business Recorder, 2025

Comments

Comments are closed for this article.