Javedan Corporation Limited (PSX: JVDC) was incorporated in Pakistan as a public limited company in 1961. The company discontinued its cement business in 2010 and the company utilized its land for developing a housing scheme called “Naya Nazimabad” which includes commercial and residential sites, open plots, flat sites etc.

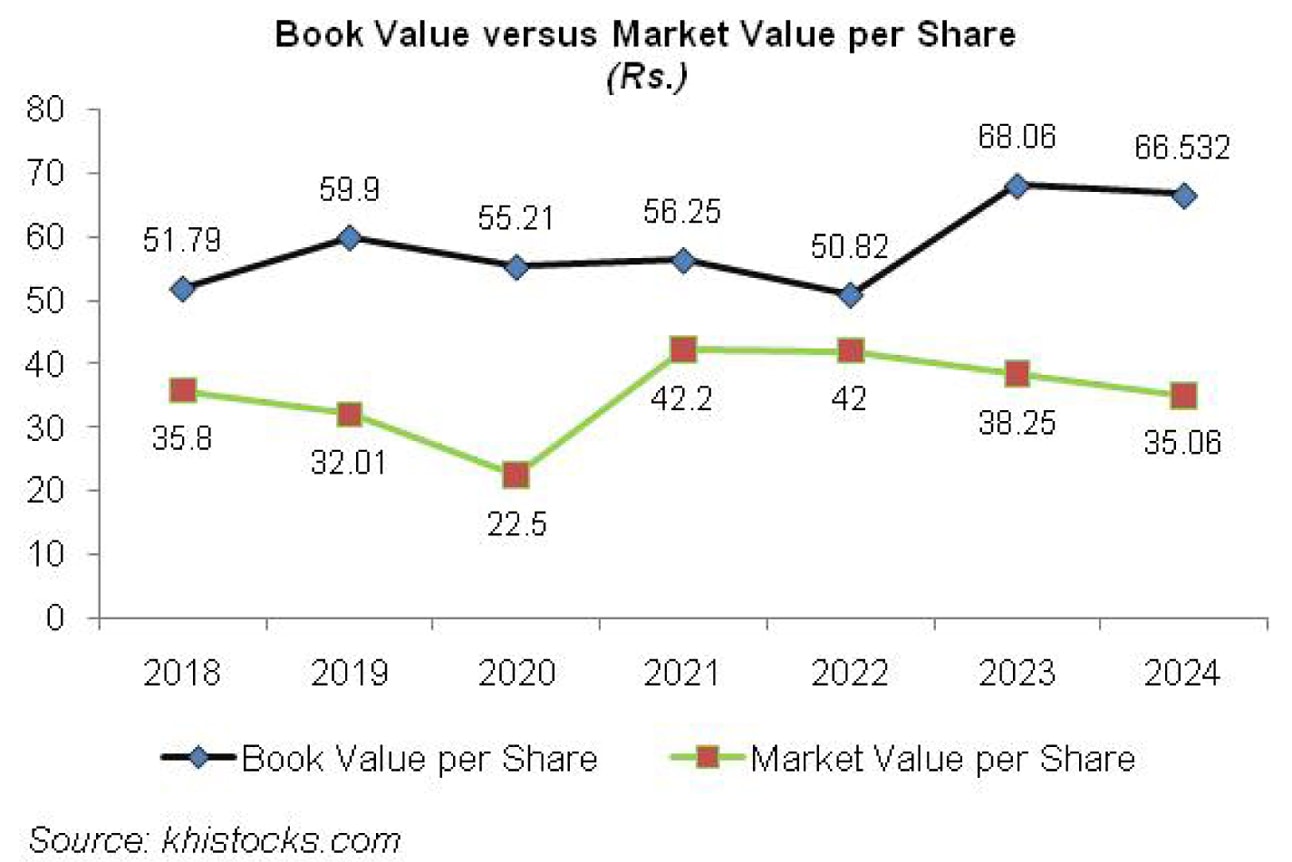

Pattern of Shareholding

As of June 30, 2024, JVDC has a total of 380.86 million shares outstanding which are held by 3015 shareholders. Associated companies, undertakings and related parties have the majority stake of 63.44 percent in the company followed by local general public holding 19.07 percent shares of JVDC.

Directors, their spouse and minor children account for 2.36 percent shares of the company. The remaining shares are held by other categories of shareholders.

Historical Performance (2019-24)

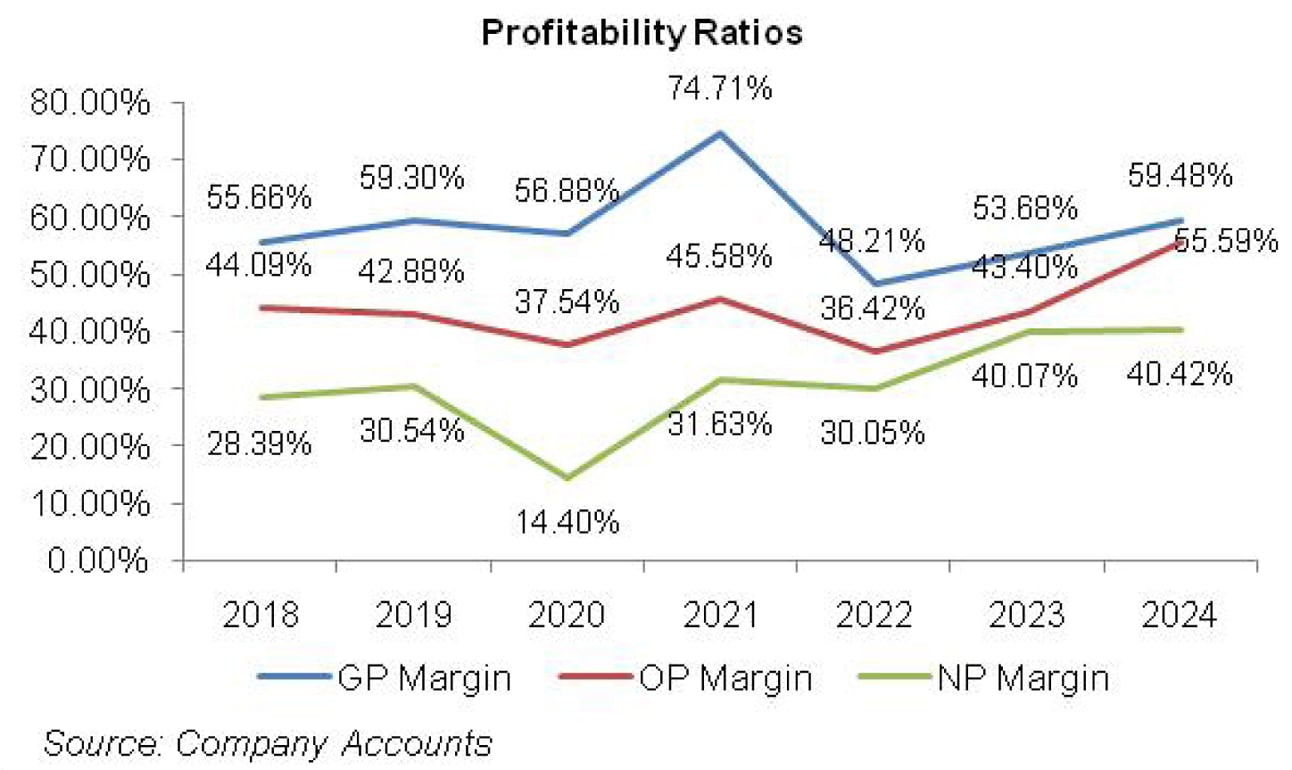

JVDC’s topline which contracted until 2021 rebounded for the subsequent two years. In 2024, the topline fell again. Its bottomline followed an ascending path since 2020 except for year-on-year decline registered in 2024. The company’s margins oscillated over the period under consideration. In 2019, gross and net margins grew while operating margin fell. This was followed by a significant fall in all the margins in 2020. In 2021, the margins regained their momentum.

However, in 2022, all the margins slid back. JVDC’s margins posted a rise in 2023 and 2024 (see the graph of profitability ratios). The detailed performance review of the period under consideration is given below.

In 2019, JVDC’s topline plunged by 23.40 percent year-on-year to clock in at Rs.1899.01 million. This was due to lower sales as the company had limited inventory available from blocks launched during yesteryears. Cost of sales dipped by 29.69 percent in 2019 due to lesser number of properties sold during the year. This resulted in 18.69 percent year-on-year decline in gross profit in 2019. GP margin improved from 55.66 percent in 2018 to 59.30 percent in 2019. Distribution expense slumped by 18 percent in 2019 mainly on account of lesser events and exhibitions conducted during the year.

Administrative expense mounted by 39.44 percent in 2019 due to higher payroll expense on account of inflation and increase in number of employees from 487 in 2018 to 498 in 2019. Other income strengthened by 153.55 percent in 2019 primarily due to higher transfer fees from plots and bungalows.

Furthermore, JVDC rental income and re-measurement gain on investments properties also improved during the year. Operating profit shrank by 25.50 percent in 2019 with OP margin sliding down to 42.88 percent from OP margin of 44 percent recorded in 2018. The company incurred finance cost of Rs.117.82 million in 2019 versus finance income of Rs.7.56 million recorded in the previous year. This was due to considerably lower dividend received on preference shares coupled with increased borrowings and higher discount rate.

Net profit slumped by 17.60 percent year-on-year in 2019 to clock in at Rs.579.88 million with EPS of Rs.1.83 versus EPS of Rs.2.84 recorded in 2018. NP margin grew from 28.39 percent in 2018 to 30.54 percent in 2019.

In 2020, JVDC’s topline plummeted by 13.47 percent to clock in at Rs.1643.27 million. This was on account of global pandemic which resulted in sluggish sale of inventory from the already launched blocks and the deferral of the apartment project.

Cost of sales contracted by 8.32 percent in 2020, resulting in 17 percent thinner gross profit and GP margin of 56.88 percent. Distribution expense dropped by 5.76 percent in 2020 due to lesser exhibition and events expense as well as lesser sales commission incurred during the year.

Administrative expense inched up by 5.98 percent in 2020 due to higher legal, professional & consultancy charges incurred during the year. Payroll expense declined in 2020 as the company trimmed down its workforce to 171 employees. Other income grew by 11.60 percent in 2020 mainly due to higher re-measurement gain on investment properties. Operating profit contracted by 24.24 percent in 2020 with OP margin falling down to 37.54 percent.

Finance cost surged by 76.17 percent in 2020 due to higher discount rate for most part of the year. Net profit posted 59.18 percent year-on-year decline to clock in at Rs.236.700 million in 2020 with EPS of Rs.0.75 and NP margin of 14.4 percent – the lowest during the period under consideration.

JVDC’s topline posted year-on-year decline of 36.27 percent to clock in at Rs. 1047.29 million in 2021. This was on account of no new projects launched during the year. Cost of sales dwindled by 62.62 percent in 2021 as lesser number of plots and bungalows were sold during the year.

Gross profit dipped by 16.29 percent in 2021, however, GP margin reached its highest level of 74.71 percent. 33.19 percent lower distribution expense incurred during the year was the result of a check on sales promotion drives, events and exhibitions in 2021.

Administrative expense escalated by 9 percent in 2021 due to elevated payroll expense as number of employees grew to 207. Furthermore, higher utility charges, fee & subscription charges, repair & maintenance and caretaking charges also drove up administrative expense in 2021. Other income posted 24.78 percent year-on-year rise in 2021 on the back of higher transfer fee from plots and bungalows, rental income and mark-up on saving accounts.

Operating profit slipped by 22.61 percent in 2021 with OP margin clocking in at 45.58 percent. Finance cost slid by 48.34 percent in 2021 due to monetary easing. While profit before tax was down by 9.57 percent in 2021, the effect of prior and deferred taxation resulted in 77.45 percent lower tax expense in 2021.

Consequently, net profit picked up by 39.94 percent to clock in at Rs.331.24 million in 2021 with EPS of Rs.0.87 and NP margin of 31.63 percent.

Unlike past year, where JVDC posted continuous decline in its net revenue, in 2022, JVDC’s topline built up tremendously to the tune of 378.34 percent. JVDC’s topline was recorded at Rs.5009.54 million in 2022. During the year, the company launched a project of 1300 apartments over 9 towers. This was developed under corporate structure of developmental REIT named as GLOBE Residency REIT. Cost of sales mounted by 879.30 percent in 2022. Gross profit grew by 208.71 percent in 2022, however, GP margin dropped to 48.21 percent.

Distribution expense continued to slide in 2022. While exhibitions and events were done during the year, lesser sales promotion and commission pushed the distribution expense down in 2022.

Administrative expense grew by 8.84 percent in 2022 due to higher payroll expense and utility charges incurred during the year. Number of employees grew to 229 in 2022. During the year, the company took permission from Sindh Government to construct a flyover connecting Manghopir Road with North Nazimabad. This resulted in flyover cost of Rs.404.312 million in 2022.

Other income registered a staggering 101.41 percent rise in 2022 on the back of transfer fee from bungalows and plots, re-measurement gain on investment properties, mark-up on saving deposits as well as rental income. Operating profit enhanced by 282.12 percent in 2022 with OP margin clocking in at 36.42 percent. Despite monetary tightening, JVDC was able to squeeze its finance cost by 36.82 percent.

While borrowings also grew during the year, higher borrowing cost capitalized in the cost of qualifying asset, resulted in curtailed finance cost. Net profit grew by 354.40 percent to clock in at Rs.1505.145 million with EPS of Rs.3.95 and NP margin of 30 percent.

In 2023, JVDC posted another staggering topline growth of 235.90 percent. Topline clocked in at Rs.16,827.21 million in 2023. This year marked successful completion of GLOBE Residency REIT transactions. During the year, the company also launched Signature Tower project which was transferred into “Signature Residency REIT”. Moreover, some land parcels were also successfully sold to REITs.

The REIT projects not only allowed JVDC to realize gain on land but also earn dividends. Cost of sales grew by 200.42 percent in 2023, resulting in 274 percent higher gross profit and GP margin of 53.68 percent. Distribution expense surged by 181.84 percent in 2023 due to greater sales promotion drives, events and exhibitions undertaken during the year.

Flyover cost amplified by 160.15 percent in 2023. Administrative expense inched up by 5.2 percent in 2023 due to higher payroll expense, utility expense and depreciation expense incurred during the year. JVDC chopped down its workforce to 580 in 2023.

Other income grew by 24.85 percent in 2023 due to higher re-measurement gain on investment properties and higher rental income. Operating profit built up by 310.40 percent in 2023 with OP margin climbing up to 44.45 percent. Finance cost surged by 667.61 percent in 2023 due to unprecedented level of discount rate and higher borrowings. Net profit rose by 347.93 percent to clock in at Rs.6741.951 million in 2023 with EPS of Rs.17.7 and NP margin of 40 percent.

In 2024, JVDC’s topline tumbled by 74.95 percent to clock in at Rs.4214.92 million. This was due to massive decline in sale of plots and bungalows in 2024.During the year, “Peace Apartments” were launched under Naya Nazimabad Apartment REIT which was well received by the market.

During the year, UBL Bank purchased a commercial plot of 14,092 square yards for its regional office. Bank Alfalah was also in the process of acquisition of 9,465 square feet for its digital lifestyle experience branch. The completion of Naya Nazimabad Flyover, Naya Nazimabad Gymkhana and Jama Masjid also entered their final stages in 2024. Cost of sales dipped by 78 percent, resulting in 72.25 percent thinner gross profit recorded by JVDC in 2024.

However, GP margin inched up to 59.48 percent in 2024. Distribution expense shrank by 58.41 percent in 2024 due to lesser events and exhibitions organized during the year.

JVDC also cut down its sales promotion activities in 2024. Flyover cost also nosedived by 30.67 percent in 2024. Administrative expense posted an uptick of 14.30 percent in 2024 due to higher payroll expense and utility charges incurred during the year.

Other income multiplied by 209.46 percent in 2024 as the company recorded a massive re-measurement gain on investment designated at FVTPL.

Operating profit slid by 68.70 percent in 2024 with OP margin picking up to 55.59 percent. Finance cost dwindled by 68 percent in 2024 due to lesser borrowings and improved liquidity position. Net profit slid by 74.73 percent to clock in at Rs.1703.627 million in 2024 with EPS of Rs.4.47 and NP margin of 40.42 percent.

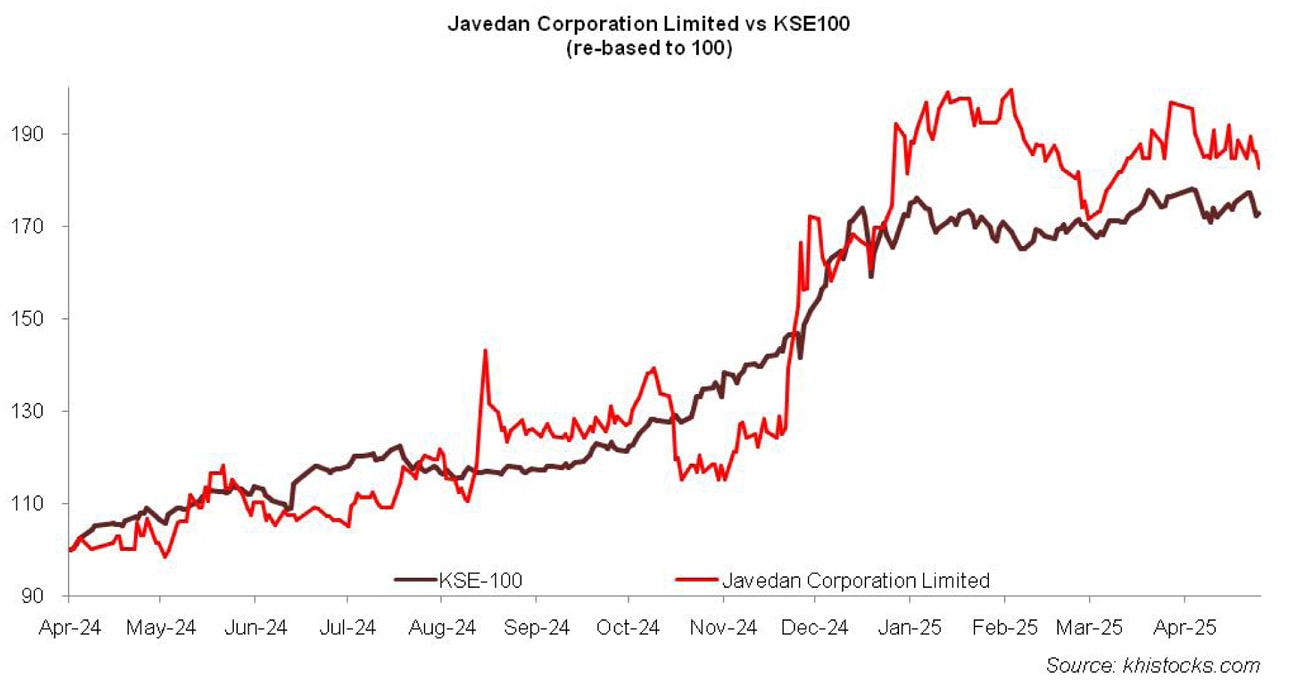

Recent Performance (9MFY25)

During 9MFY25, JVDC’s net sales strengthened by 62.61 percent to clock in at Rs.5063.16 million. Improvement in key economic indicators – declining inflation, discount rate, stability of Pak Rupee etc – provided impetus to real-estate demand. During the period under consideration, JVDC also launched low rise to mid-rise commercial plots “Naya Nazimabad Business Enclave” which received great traction.

A major boost to the company’s net sales came on the back of sale of commercial plots worth Rs.1700 million to Arif Habib Corporation Limited. Cost of sales surged by 48.26 percent in 9MFY25, resulting in 76.15 percent higher gross profit recorded during the period. GP margin also improved from 51.46 percent in 9MFY24 to 55.75 percent in 9MFY25. Distribution expense mounted by 15.89 percent in 9MFY25 due to higher sales promotion activities.

Administrative expense also surged by 36.40 percent in 9MFY25 due to elevated payroll expense. Other income dwindled by 57.29 percent in 9MFY25 due to lower re-measurement gain recognized on investments designated at FVTPL. Operating profit picked up by 59.66 percent in 9MFY25 with OP margin recorded at 52.58 percent versus OP margin of 53.55 percent recorded during the same period last year.

Finance cost escalated by 68.76 percent during 9MFY25 due to lesser borrowing cost capitalized in the cost of qualifying asset and thinner finance income recognized during the period due to lower discount rate. Net profit grew by 55.52 percent to clock in at Rs.1811.32 million in 9MFY25. This translated into EPS of Rs.4.76 in 9MFY25 versus EPS of Rs.3.06 recorded during the same period last year. NP margin weakened from 37.41 percent in 9MFY24 to 35.77 percent in 9MFY25.

Future Outlook

With over 2000 apartments and houses under construction, commencement of Naya Nazimabad Gymkhana and the launch of Business Enclave, JVDC’s topline is expected to jump up. Flyover project is nearing completion.

REIT structure is progressing as planned. Furthermore, strengthening macroeconomic indicators is driving recovery in construction activity and real-estate market which will further boost the performance of JVDC.

Comments

Comments are closed for this article.