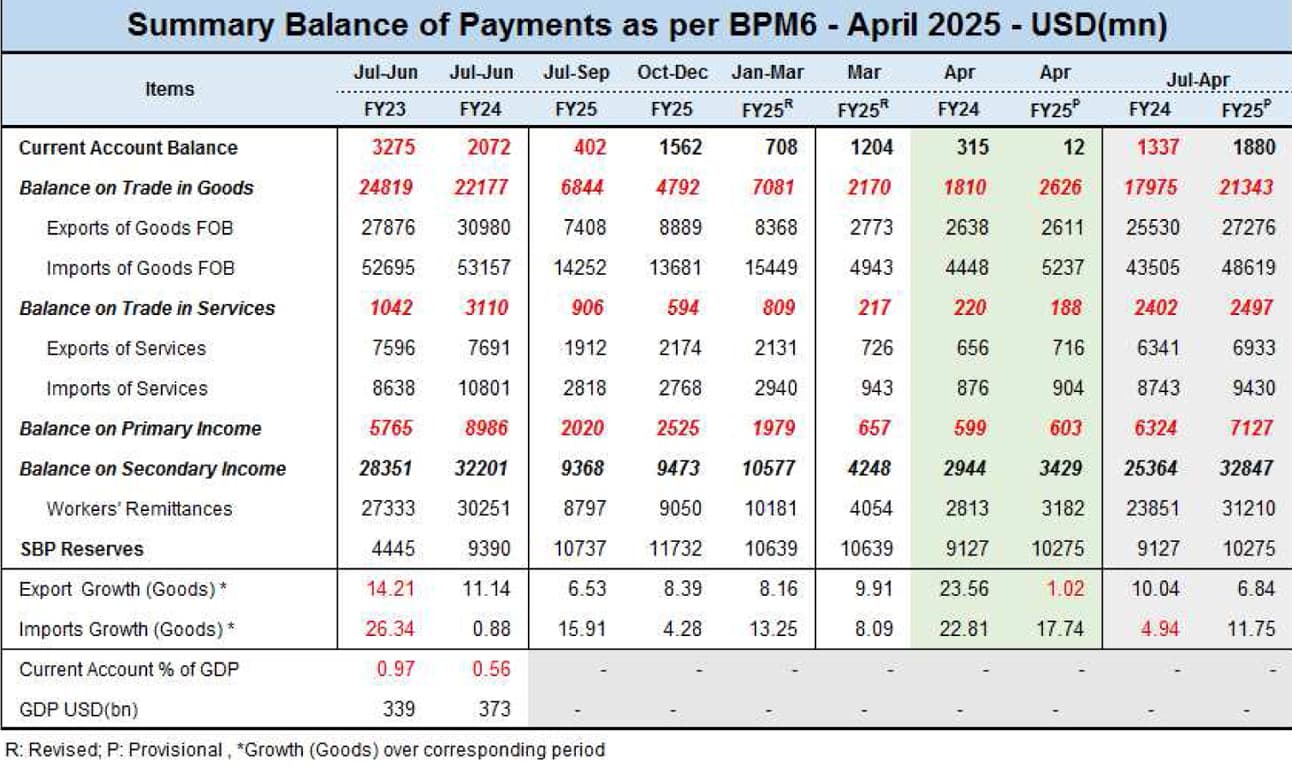

The comfort of the current account surplus continues, as despite growing imports and a monthly drop in remittances, the current account remained marginally in surplus at $12 million in April 2025. In 10MFY25, the current account surplus stood at $1.9 billion, compared to a deficit of $1.3 billion in the same period last year.

This is even though imports are picking up. Based on PBS data (shipment basis), imports in April 2025 stood at $5.6 billion — the highest figure since August 2022. There are signs of import demand picking up, as global commodity prices remain low and import volumes are rising.

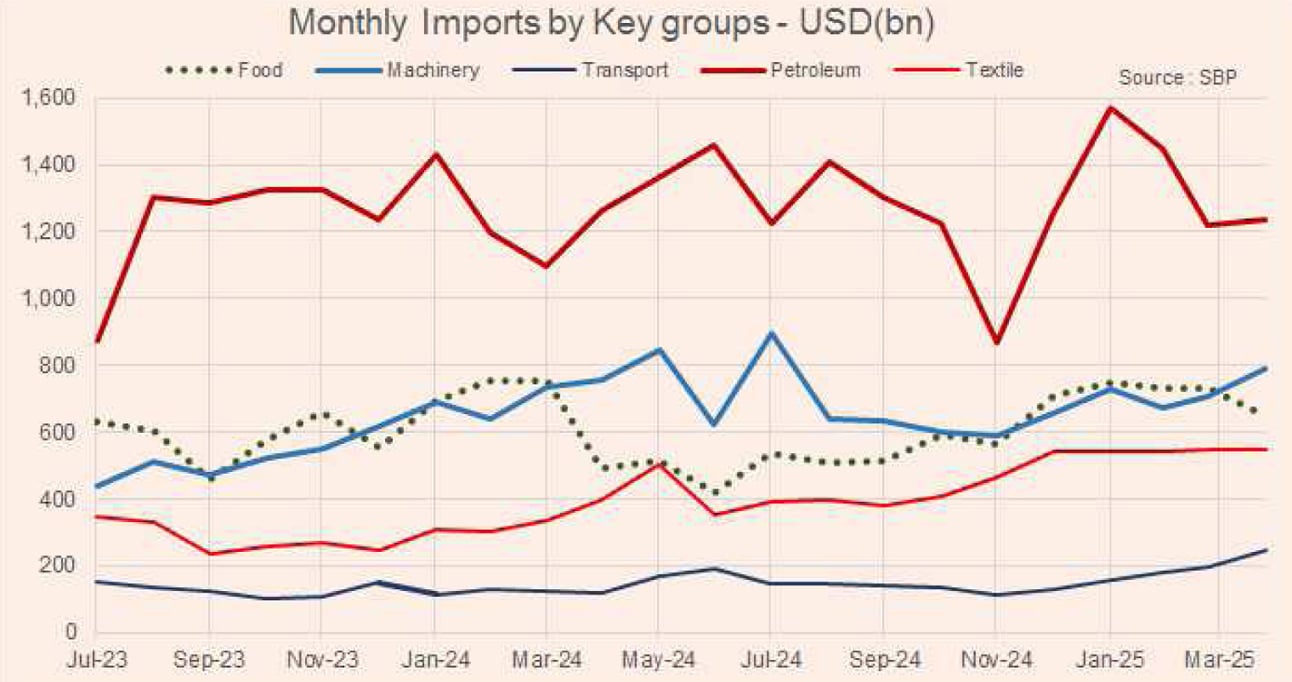

In 10MFY25, the biggest increase was in the textile group, where Chinese dumping and an adverse taxation policy for the local supply chain are resulting in higher raw material imports. Transport is also picking up, as auto demand rises and consumers are offered plenty of choices.

The import toll stood at $5.24 billion (based on SBP payment basis data) up by 18 percent YoY and 6 percent MoM. The impact of slashing interest rates is expected to slowly bring back demand and confidence. Businesses may expand where required, and consumers may begin discretionary spending.

There are early signs of this trend building up. A measured increase can be afforded given low commodity prices and robust remittance growth. The SBP has an implicit check on import demand beyond uncomfortable levels. There is a new norm for managing inflows and outflows by bank treasuries within the interbank system. The silent, implied SBP policy is being implemented to the letter, with banks only catering to import demand they can match export and remittance proceeds.

That is why some banks are offering (out of pocket) discounts in addition to the government’s announced subsidy to attract remittances — the higher the inflows, the more import (L/C-based) business banks can manage. They are not only competing for business but also eroding the already shrinking share of the informal hundi and hawala system.

The upbeat performance in remittances adds credence to the story. The toll was at an all-time high of $4.1 billion in March but dropped to $3.2 billion in April due to seasonal factors. May and June are expected to bring higher inflows as well, owing to seasonal Bakra Eid-related transfers. Overall, in 10MFY25, remittance inflows are up a whopping 31 percent to $31.2 billion.

This year, these inflows are equivalent to 91 percent of the combined exports of goods and services. There is no doubt that remittances are the star performer, and their increase is helping fuel consumer demand, as the bulk is sent back home for families to spend.

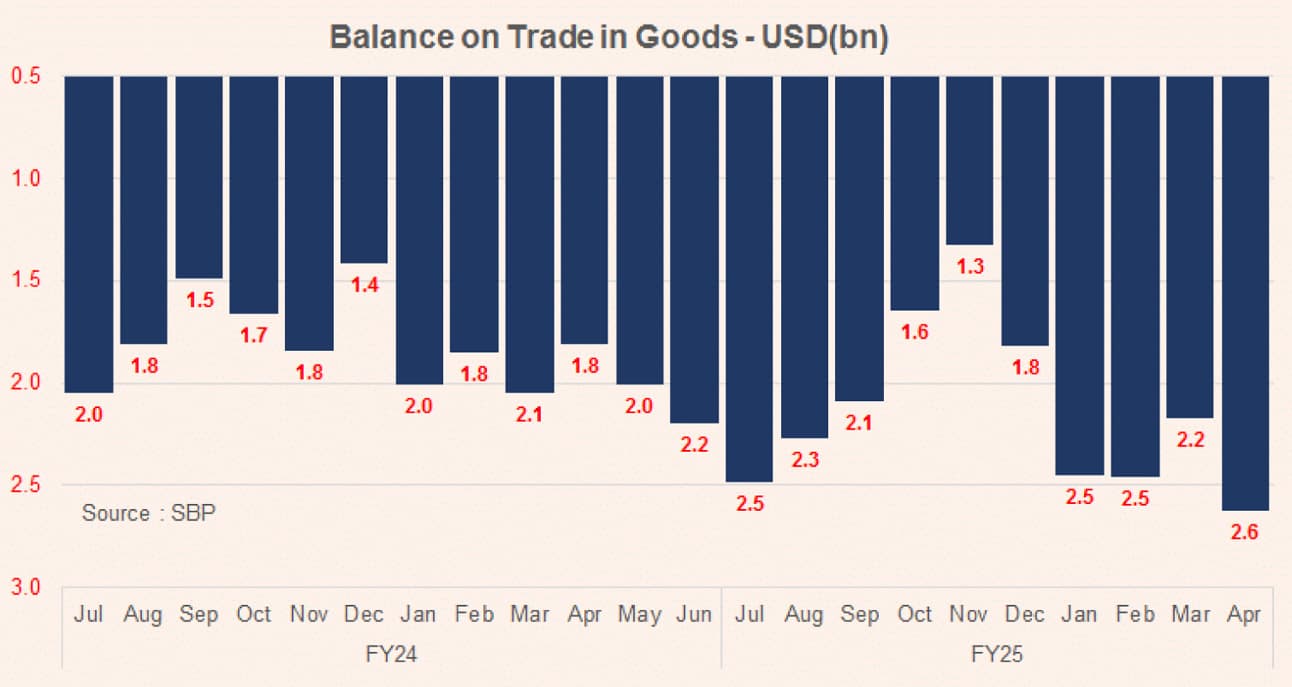

Goods export growth remains limited — unable to catch up with imports and overshadowed by booming remittances. The tally stood at $2.6 billion in April 2025 — down 1 percent year-on-year and 6 percent month-on-month. In 10MFY25, goods exports rose by 7 percent to $27.3 billion.

The growth pattern has been consistent so far this year. However, the earlier rice export boom is tapering off, with rice exports down 17 percent to $2.6 billion. Within textiles, there has been strong double-digit growth in knitwear, bedwear, towels, and readymade garments, while cotton yarn and cotton cloth exports have continued to decline.

The yarn and cloth industries are on the verge of crisis due to an influx of low-cost raw material imports from China, coupled with the dumping of textiles and other products into the Pakistani market. Exporters also enjoy a cash flow advantage under the Export Facilitation Scheme (EFS) for imports — keeping net textile export growth limited.

Nonetheless, the current account is likely to remain comfortable in FY26, as global commodity prices are expected to stay low and the remittance bonanza continues.

The thorny issue is the financial account, which remains in the red and is eating up all the gains from the current account surplus. In 10MFY25, the financial account recorded a deficit of $1.6 billion, compared to a surplus of $4.2 billion during the same period last year. Stronger inflows last year were driven by higher net external assistance received by the government, which stood at $2.0 billion in 10MFY24 but has now turned negative at $100 million. Consequently, the overall balance of payments surplus declined to $423 million in 10MFY25, down from $2.4 billion in the same period last year.

Reserves came down to $10.5 billion. However, they are building up again with the IMF tranche being received. The State Bank of Pakistan (SBP) expects foreign exchange reserves to reach $14 billion by the end of June. This implies reduced pressure on the PKR and an increased likelihood of further monetary easing within the calendar year.

Copyright Business Recorder, 2025

Comments

Comments are closed for this article.