In an unexpected twist, Pakistan is witnessing a sharp acceleration in money supply growth at precisely the time it should have been slowing.

Despite the public sector’s long-awaited retreat from wheat procurement—and with it, the traditional seasonal build-up in commodity operations debt—money supply indicators are rising across the board. Currency in Circulation (CiC), Reserve money (M0), and Broad money (M2) are all clocking over 14 percent year-on-year growth since March 2025. The timing is not coincidental.

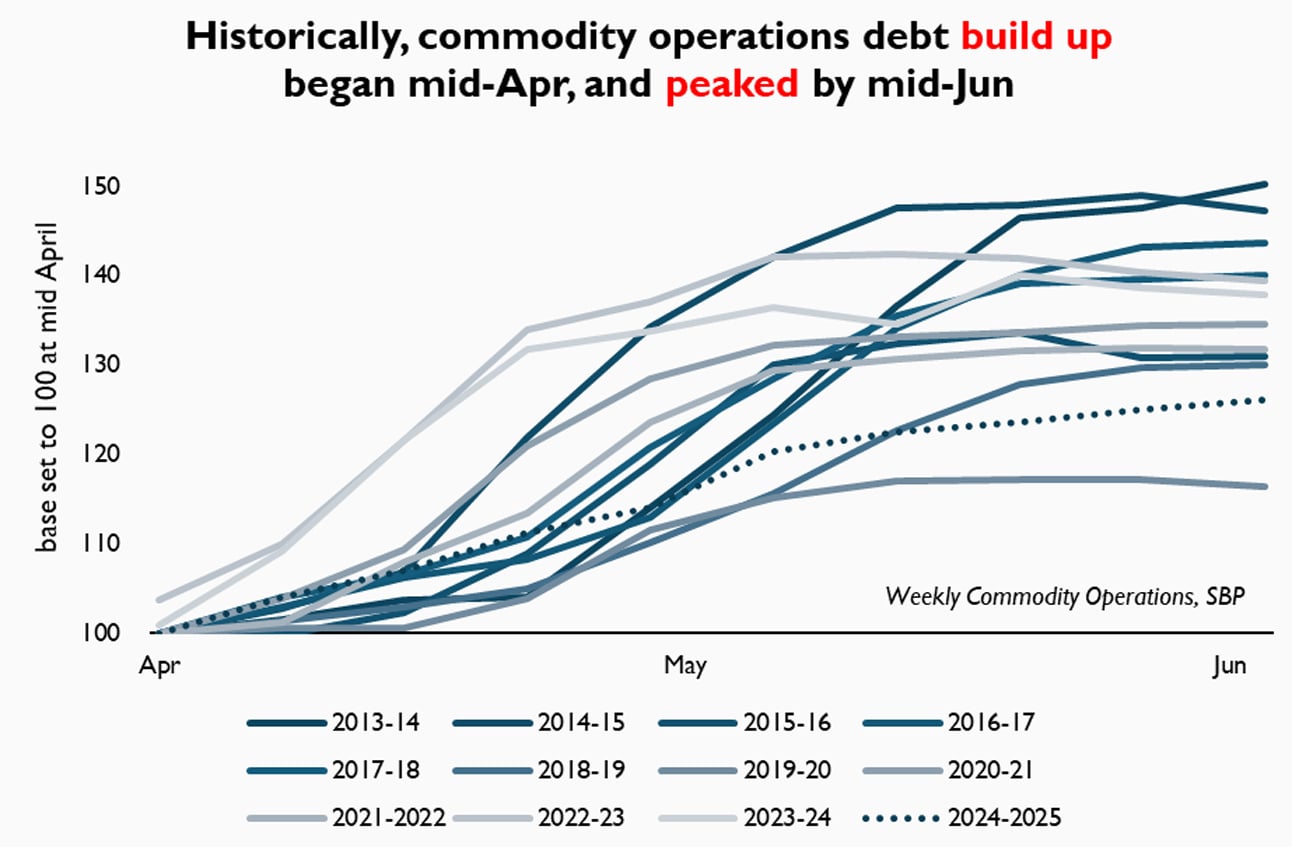

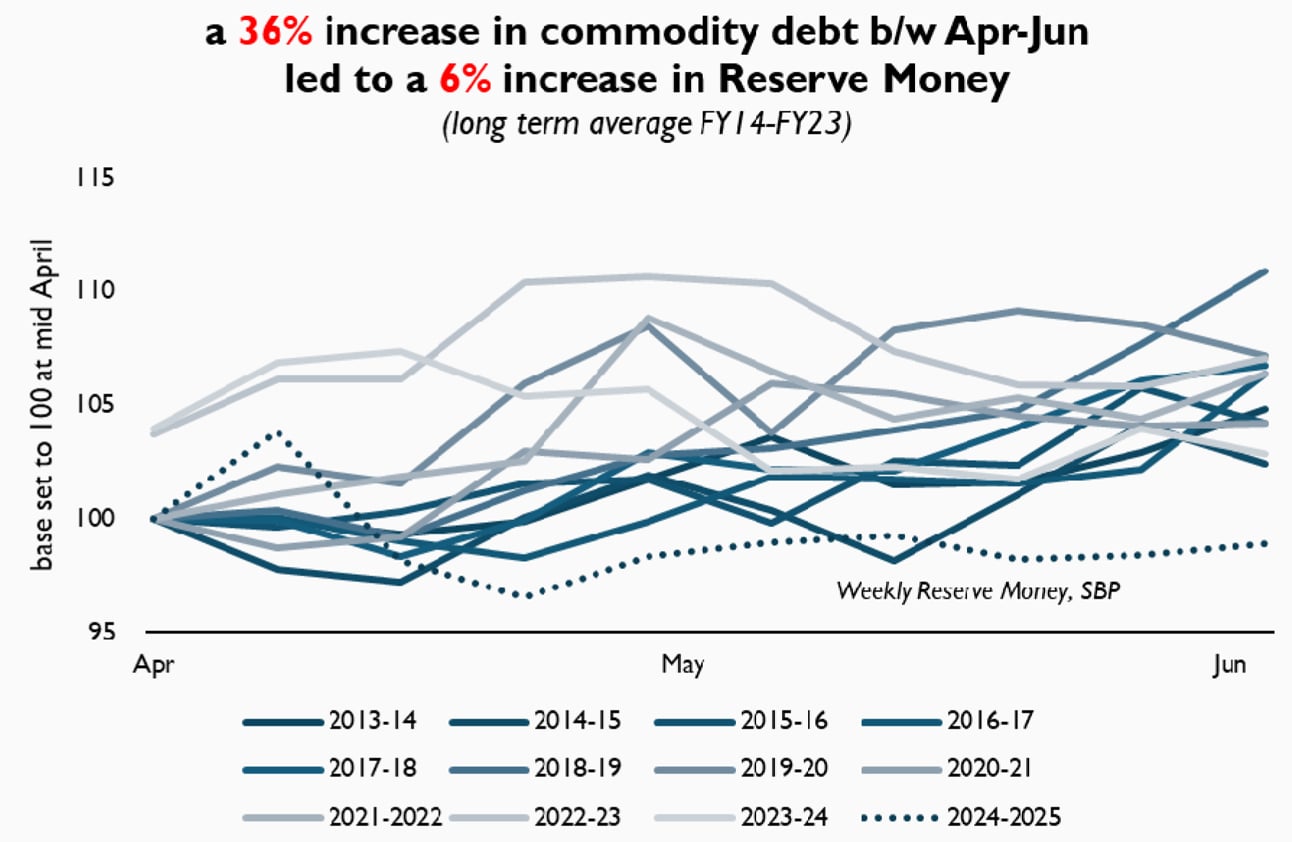

Historically, the fiscal machinery—via commodity operations—was the primary culprit behind post-harvest liquidity spikes. Between 2013 and 2023, commodity operations debt rose by an average 36 percent between April and June each year. While this debt was formally captured under M2, it consistently leaked into M0, causing Reserve money (M0) to grow by 6 percent during the same seasonal window.

Why? Because the government’s borrowing from banks to purchase wheat injected cash directly into rural markets, feeding cash demand and drawing on liquidity in the interbank to support vault cash and reserve requirements.

But not this year. Government borrowing for commodity operations is in net settlement mode. There is no surge in seasonal debt. There is no fresh fiscal injection into rural mandis. And yet—Reserve money is booming. The big question is: why?

The answer likely lies offshore. March 2025, coinciding with Ramzan and Eid-ul-Fitr, saw record growth in monthly inward remittances—up over 35 percent year-on-year. But here is the critical dynamic: SBP insists that it is not injecting dollars to defend the exchange rate.

Instead, it is mopping up the excess FX from the interbank market to prevent the rupee from appreciating too quickly—and using those purchases to meet country’s external debt obligations. In doing so, it is injecting rupee liquidity into the system. If those rupee injections are not being sterilized—if the counterpart Pak Rupee is left floating in the banking system—then we have a new, powerful monetary injection mechanism: remittance-driven reserve money expansion.

And this time, it is likely showing up not just in banks’ deposits with SBP, but also in currency in circulation (CiC), which had previously plateaued. Between Mar-Nov 2024, year-on-year increase in CiC had averaged below 5 percent. Over the past 12 weeks, it has averagedat nearly 15 percent. Reserve money (M0), appears to be following similar trends, averaging 13 percent, against 7 percent between Mar-Nov 2024.

If Reserve money is rising despite the absence of fiscal monetization—and due instead to remittance driven Pak Rupee injections—then SBP must come clean about its intervention and sterilization strategy. The question no longer is whether the exchange rate is being defended, but whether remittance absorption is being silently monetized.

If unsterilized remittance inflows are driving liquidity expansion, SBP risks fuelling demand-side inflation just as the economy begins to stabilize. In a low-velocity, high-liquidity environment, the lag may be deceptive—but the inflation impulse, when it comes, will be real.

The central bank must urgently clarify its sterilization strategy. If it chooses to absorb remittances without mopping up the resulting liquidity, it must do so with eyes wide open—and a credible inflation management plan in place. Failing that, it may find itself once again chasing inflationary shadows with a blunt rate hike months too late.

Comments

Comments are closed for this article.