Agritech Limited (PSX: AGL) was incorporated in Pakistan in 1959 as Pak-American Fertilizers Limited. The company is engaged in the production and sale of urea and granulated single super phosphate fertilizer. The company’s products are sold under the brand name “Tara” in the fertilizer market.

Pattern of Shareholding

As of December 31, 2024, the company has a total of 424.645 million shares outstanding which are held by 1761 shareholders. Associated companies, undertakings and related parties have the majority stake of 53.14 percent in AGL followed by Banks, DFIs and NBFIs holding 21.70 percent shares. Joint stock companies account for 17.69 percent shares of the company while local general public holds 2.13 percent shares.

Around 1.50 percent of the company’s shares are held by public sector companies & corporations, 1.47 percent by foreign companies and 1.12 percent by Modarabas & Mutual Funds. The remaining shares are held by other categories of shareholders.

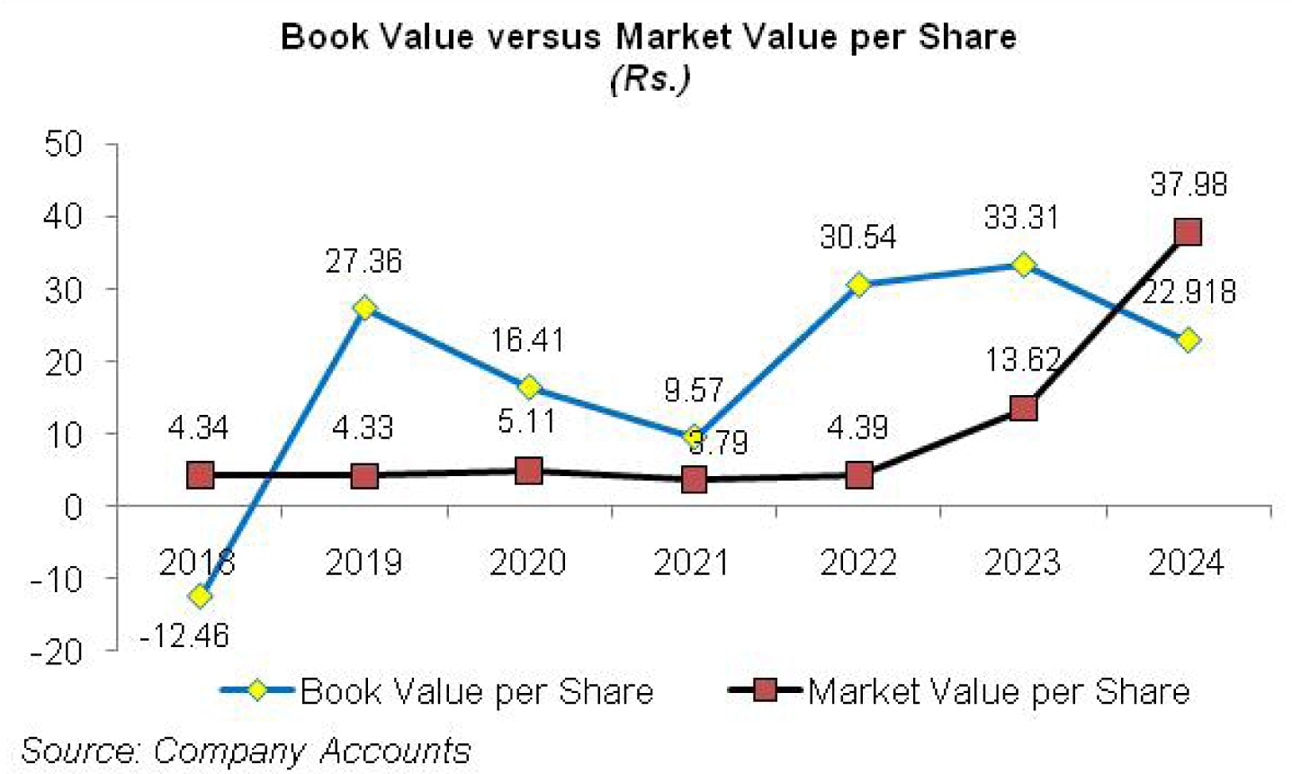

Historical Performance (2019-24)

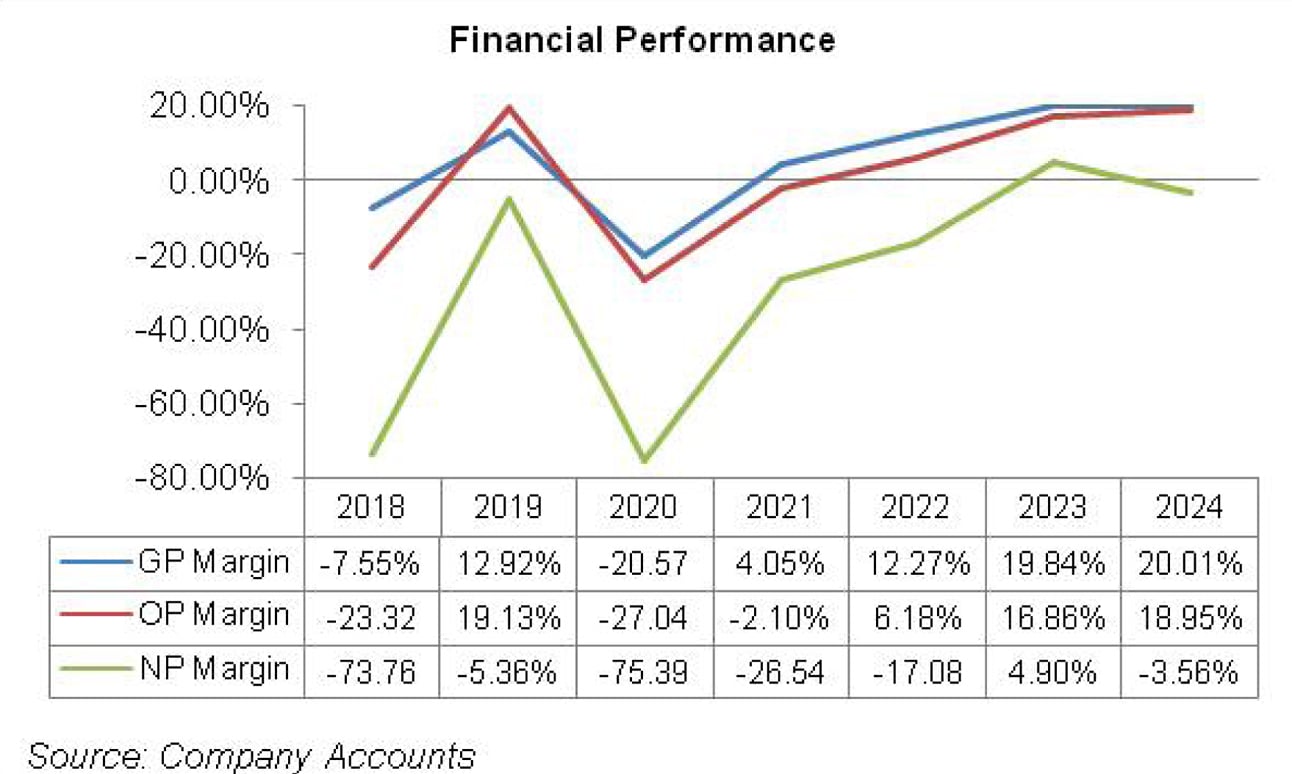

Except for a year-on-year drop in 2020, AGL’s topline has posted staggering growth over the period under consideration. Despite that, the company is unable to post net profit in any of the years except 2023. In fact, in 2020, the company was not even able to post gross profit.

AGL’s gross and operating margins which came out of the negative zone in 2019 fell back to the same ditch in 2020. Gross and operating margins took an upward flight thereafter. Conversely, net margin stayed in the negative zone in all the years except 2023. The detailed performance review of the period under consideration is given below.

In 2019, AGL’s topline boasted a tremendous 168.55 percent year-on-year growth to clock in at Rs.12,174,42 million. The growth was an industry-wide phenomenon due to robust return on major crops which increased the purchasing power of farmers.

The fertilizer production across the industry also grew by 10 percent during the year due to better gas supply. During 2019, AGL produced 338 KT of Urea which is 2.5 times of the production volume achieved by the company in 2018. The sales volume also grew from 101KT in 2018 to 320KT in 2019, registering a 216.83 percent growth. The cost of sales also grew by 117.43 percent in 2019 due to steep rise in the prices of raw and packing material as well as fuel and power.

Yet, AGL was able to post gross profit of Rs.1573.07 million in 2019 as against gross loss of Rs.342.34 million posted in 2018. GP ratio for 2019 stood at 12.92 percent. High freight charges pushed the distribution cost up by 208.45 percent in 2019. Administrative expense grew by 34 percent in 2019 which largely signifies market induced rise in salaries and wages, travelling and conveyance as well as utility charges.

Other expense nosedived by around 99.57 percent during 2019 due to lesser provisioning done against doubtful receivables. Conversely, other income multiplied by over 4300 percent in 2019 due to reversal of late payment surcharge (LPS) and present value adjustment of GIDC in 2019.

This greatly buttressed the operating results of AGL in 2019 and the company posted an operating profit of Rs.2,329.41 million in 2019 as against operating loss of Rs.1057.09 million in 2018. OP margin for 2019 hovered around 19.13 percent.

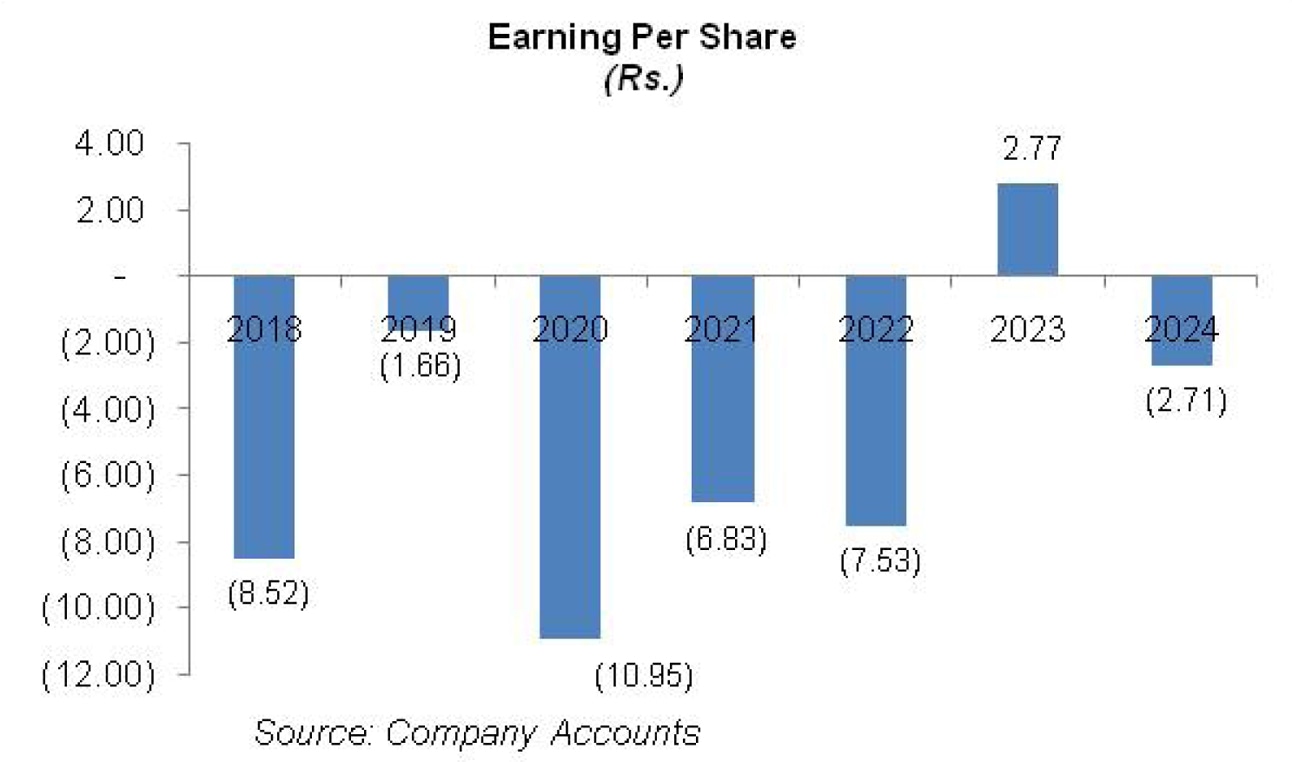

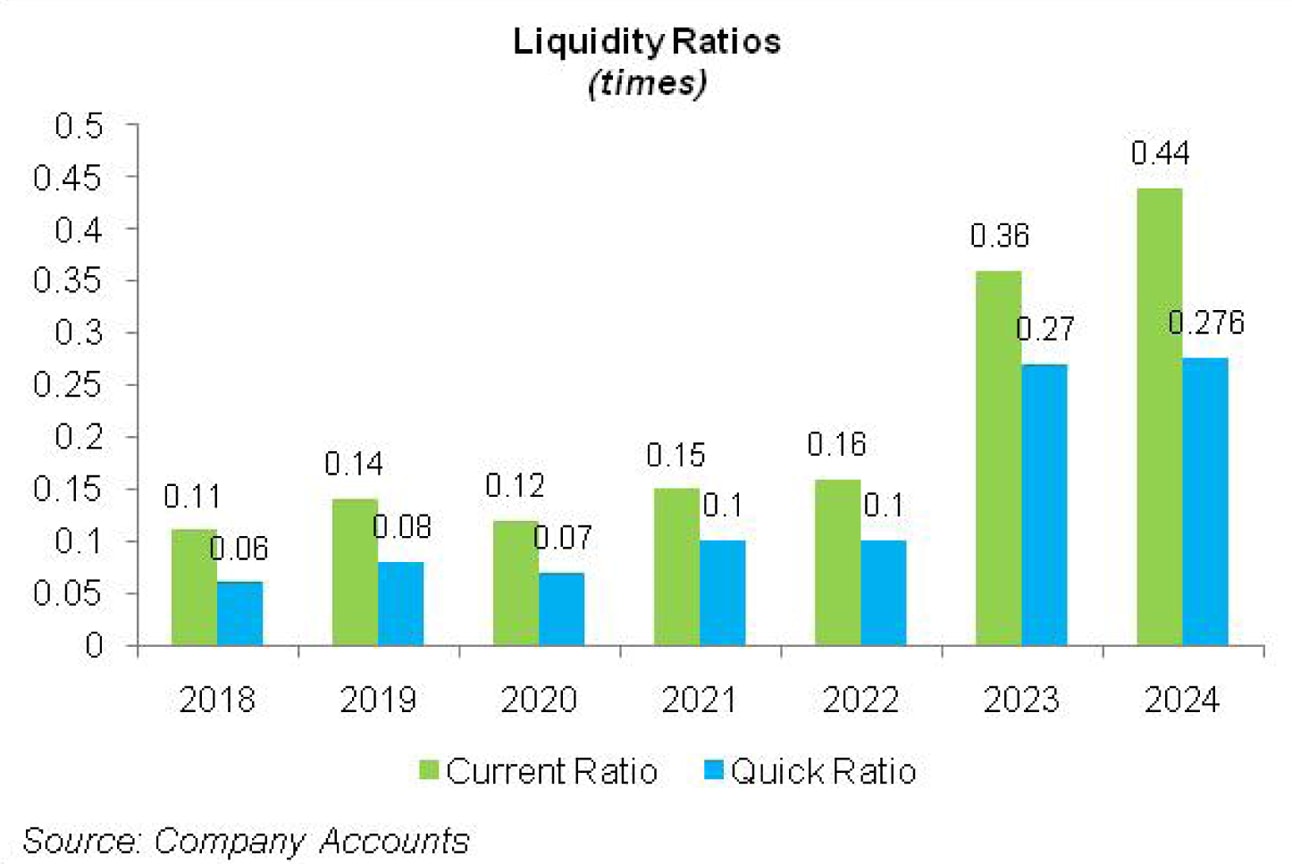

However, the joy appeared to be momentary as 27.80 percent year-on-year hike in finance cost didn’t allow the impressive operating performance to cascade down, resulting in net loss of Rs.652.78 million in 2019, down 80.48 percent year-on-year. Loss per share stood at Rs.1.66 in 2019 as against loss per share of Rs.8.52 in 2018. It is to be noted that AGL had a huge debt-to-equity ratio of 66 percent as of December, 31, 2019, hence finance cost stood at 27 percent of its topline in 2019.

In 2020, AGL’s topline slid by 53.18 percent year-on-year to clock in at Rs.5,699.72 million. While COVID related lockdowns had a significant negative impact on urea off-take in 2020, another significant phenomenon which produced an industry-wide decline in urea off-take in 2020 was market price distortion as the government abolished GIDC for the fertilizer sector that resulted in price cuts by various producers.

Moreover, cotton crop immensely declined during 2020, affecting farmers spending pattern. AGL sold 139 KT of Urea in 2020 which was around 57 percent lower than the last year’s volume. As the plant remained operational for only 123 days in 2020, cost of sales plunged by 35.17 percent year-on-year in 2020.

However, low volume and reduced price resulted in gross loss of Rs.1172.72 million in 2020. Lesser off-take also meant lesser freight charges which pushed distribution expense down by 57.61 percent year-on-year in 2020. Administrative expense inched up by 9.11 percent on account of higher legal and professional charges. Other expense and other income didn’t prove to be favorable during the year.

Other expense grew by 249.29 percent on account of higher provisioning done against doubtful advances. Other income dwindled by 88.44 percent year-on-year in 2020 as the PV adjustment of GIDC and reversal of LPS was no longer available in 2020. AGL posted operating loss of Rs.1541.38 million in 2020. Finance cost ticked down by 10.76 percent year-on-year in 2020 and stood at 52 percent of the topline. This was due to low discount rate.

Debt-to-equity ratio of AGL mounted to 76 percent as AGL’s equity was declining on the back of higher accumulated losses. Net loss surged by 558.25 percent to clock in at Rs.4296.90 million in 2020 with loss per share of Rs.10.95.

In 2021, the topline of AGL again recovered and posted year-on-year growth of 77.22 percent to clock in at Rs.10,100.92 million. Increase in the support price of wheat crop resulted in strong urea demand.

Moreover, introduction of hybrid seed varieties of rice and maize which had higher urea requirement per acre also resulted in boost in urea sales across the industry. This coupled with uninterrupted gas supply also facilitated the fertilizer sector to operate at an optimum level and meet the growing demand. AGL sold 230 KT of urea in 2021 which was 65 percent higher than the last year’s sales volume.

Higher prices of raw and packaging material as well as greater capacity utilization of 206 days resulted in cost of sales growing by 41 percent year-on-year in 2021. Yet, AGL was able to post gross profit of Rs.409.52 million in 2021 with GP margin of 4.1 percent.

Distribution cost ascended by 58.47 percent year-on-year in 2021 on account of higher freight charges. Administrative expense magnified by 14.35 percent on the back of inflation which particularly pushed up the salaries and wages expense.

IT consultancy charges as well as legal & professional fee also surged in 2021. Other expense shrank by 91.61 percent during 2021 as no provision against doubtful receivables was booked during the year. Other income also plummeted by 44.83 percent in 2021 due to lesser liabilities written back as well as lesser profit on P&L bank balance.

AGL posted operating loss of Rs.212.48 million in 2021 which was 86 percent lower than the last year’s figure. Finance cost ticked down by 4.75 percent year-on-year in 2021 and stood at 28 percent of AGL’s topline due to low discount rate.

Debt-to-equity ratio further climbed to its highest level of 85 percent in 2021 due to loss accumulation which gobbled up AGL’s equity. Net loss of Rs.2681.24 recorded by AGL in 2021 was 37.6 percent lesser than the net loss posted in 2021. AGL’s loss per share stood at Rs.6.83 in 2021.

The topline continued its growth journey with 71.23 percent escalation to clock in at Rs.17,296.18 in 2022. This was on the back of better farm economics that boosted the industry wide sales to an unprecedented level of 6616 KT in 2022. AGL touted 2022 as the best year since 2010 due to better gas supply which enabled it to operate for the longest period of 351 days.

The company was able to sell 351 KT urea in 2022, 53 percent higher than 2021. Cost of sales inclined by 56.58 percent year-on-year in 2022, yet gross profit mounted by 418 percent in 2022 with GP margin of 12.3 percent. Higher sales volume resulted in 81.32 percent surge in distribution expense in 2022. Increase in advertisement budget was also one of the factors which pushed the distribution expense up in 2022.

Administrative expense also grew by 29.96 percent due to higher salaries, travelling and conveyance expense, utilities as well as fee and subscription charges. Other expense enlarged by around 8178.29 percent in 2022 due to loss on the disposal of property, plant and equipment. Other income didn’t post any significant rise during 2022.

After two successive years, AGL posted operating profit of Rs.1068.99 million in 2022 with OP margin of 6.18 percent. Radical increase of 52.74 percent in AGL’s finance cost was on the back of record high discount rate coupled with increased borrowings. This resulted in net loss of Rs.2953.33 million in 2022 with loss per share of Rs.7.53. In 2022, debt-to-equity ratio slid to 64 percent as equity grew on account of surplus on the revaluation of property, plant and equipment.

In 2023, AGL posted 28.19 percent year-on-year rise in its net sales which clocked in at Rs.22,172.16 million. During the year, the company operated with 277 days of gas supply versus 351 days in 2022 and produced 292k tons of urea, resulting in capacity utilization of 67.44 percent. AGL sold 287k tons urea in 2023, down 18.23 percent year-on-year.

Conversely, the sales volume of phosphate fertilizer increased to 80k tons in 2023 versus 54k tons in 2022. This greatly contributed to profitability of the company in 2023. Gross profit improved by 107.32 percent in 2023 with GP margin attaining a new high level 19.84 percent. Higher gas prices and inflationary pressure was absorbed by favorable changes in the prices of fertilizer products.

Distribution expense posted a nominal rise of 5.28 percent in 2023 due to increased petroleum prices which pushed up the freight charges.

Administrative expense mounted by 34.44 percent in 2023 on account of exorbitant hike in payroll expense as the company expanded its workforce from 959 employees in 2022 to 979 employees in 2023. Legal & professional charges also drove up administrative expense in 2023. 68.88 percent higher other expense in 2023 was the consequence of higher provisioning for WWF and loss incurred on the disposal of property, plant & equipment in 2023.

Higher other expense was conveniently offset by 588.53 percent higher other income recorded by AGL in 2023. This was primarily driven by hefty profit on short-term investments coupled with gain on settlement of short-term loan and accrued markup. All these factors translated into 249.67 percent higher operating profit in 2023 with OP margin of 16.86 percent. Finance cost escalated by 42.3 percent in 2023 due to unprecedented level of discount rate. Debt-to-equity ratio stayed at 64 percent in 2023.

AGL also booked gain amounting to Rs.3207.11 million on restructuring of loan in 2023. This one-off gain converted loss before taxation into net profit of Rs.1085.79 million in 2023. EPS stood at Rs. 2.77 in 2023 while NP margin clocked in at 4.9 percent in 2023.

In 2024, AGL’s topline posted year-on-year growth of 41.20 percent to clock in at Rs.31,306.77 million. During the year, the company operated at the highest number of days due to uninterrupted gas supply and produced 372k tons of urea which was the highest production volume in last 15 years. This was against the production volume of 292k tons achieved in 2023. Capacity utilization was recorded at 85.91 percent in 2024 versus capacity utilization of 67.44 percent recorded in the previous year.

While the sector was plagued by negative farm economics of wheat in 2024 which took its toll on the purchasing power of farmers, however, the farm economics greatly improved towards the end of CY24. AGL sales volume was recorded at 325k tons in 2024, up 13.24 percent year-on-year. Besides, the company also sold 71k tons of phosphate, down 11.25 percent year-on-year.

The company also increased the prices of its products in 2024 to pass on the onus of higher gas prices and inflationary pressure to its customers. This resulted in 42.45 percent stronger gross profit recorded in 2024 with GP margin attaining its highest level of 20 percent.

Distribution expense mounted by 76.31 percent in 2024 due to higher freight charges which was the impact of improved volumes and implementation of axle load. Administrative expense surged by 26.77 percent in 2024 due to higher payroll expense, vehicle running & maintenance charges as well as fee & subscription charges incurred during the year.

The company also expanded its workforce from 979 employees in 2023 to 998 employees in 2024. Other expense escalated by 543.11 percent in 2024 due to higher provisioning done against doubtful receivable (government subsidy) and loss on disposal of property, plant & equipment recorded during the year. Other expense was completely offset by 188.19 percent higher other income recognized during the year which was the result of tremendous profit on short-term investments.

Operating profit picked up by 58.68 percent in 2024 with OP margin clocking in at 18.95 percent. Finance cost grew by 15 percent in 2024 due to higher discount rate and increased borrowings. This resulted in the gearing ratio of 71 percent in 2024 versus gearing ratio of 69 percent recorded in 2023. Higher finance cost invalidated the superior operating performance recorded by the company during the year and resulted in net loss of Rs.1114.18 million in 2024. This translated into loss per share of Rs.2.71 in 2024.

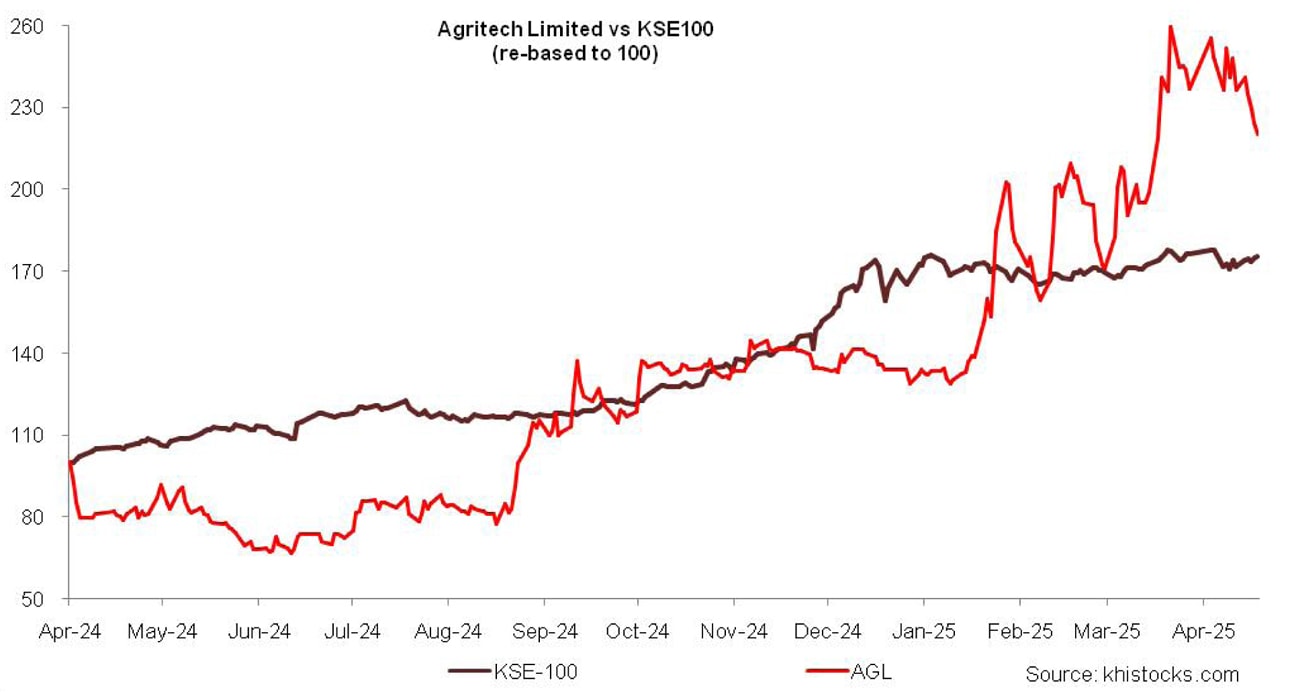

Recent Performance (1QCY25)

During the first quarter of 2025, AGL’s recorded 18.36 percent year-on-year dip in its topline which clocked in at Rs.7544.11 million. This was due to decline in sales volume of urea from 98000 tons in 1QCY24 to 89000 tons in 1QCY25. Sales volume of SSP also dipped from 15000 tons in 1QCY24 to 6000 tons in 1QCY25. This was due to weak farm economics of Rabi crops.

Cost of sales dipped by 12.40 percent during the period under consideration. This resulted in 46.12 percent erosion recorded in gross profit in 1QCY25 with GP margin clocking in at 11.67 percent versus GP margin of 17.68 percent recorded during the same period last year.

Distribution expense and administrative expense mounted by 42.80 percent and 36.30 percent respectively during the period seemingly due to implementation of axle load and higher payroll expense incurred during the period.

AGL didn’t record any other expense during the period. Its other income recorded 9.81percent uptick during 1QCY25 seemingly due to higher return on investments. AGL recorded 54.84 percent thinner operating profit in 1QCY25 with OP margin of 9.59 percent versus OP margin of 17.35 percent recorded in 1QCY24. Finance cost tumbled by 41.54 percent during the period under review due to lower discount rate and lesser outstanding borrowings.

AGL posted net loss of Rs.238.425 million in 1QCY25, up 38 percent year-on-year. This translated into loss per share of Rs.0.56 in 1QCY25 versus loss per share of Rs.0.41 recorded in 1QCY24.

Future Outlook

Lower than expected rainfall has created drought like conditions in Sindh and Punjab resulting in the shrinkage in wheat cultivation area. This coupled with the ongoing wheat prices crisis due to government exiting wheat procurement and offloading the old grain stock into the market at below market rates has resulted in price distortion. This has significantly affected the purchasing power of farmers and will likely affect the demand of Urea and phosphates.

Comments

Comments are closed for this article.