Back in FY24, Hub Power Company Limited (PSX: HUBC) delivered strong financial results, reporting consolidated earnings growth of 22 percent year-over-year. Revenue growth was driven by higher dispatches from Thar Energy Limited (TEL), currency devaluation, and improved operational efficiencies. While Thar coal-based plants (TEL & TNPTL) performed well, China Power Hub Generation Company (CPHGC) experienced a decline. Gross margins improved despite a significant rise in finance costs, supported by a jump in associate profits due to new plant operations and currency depreciation.

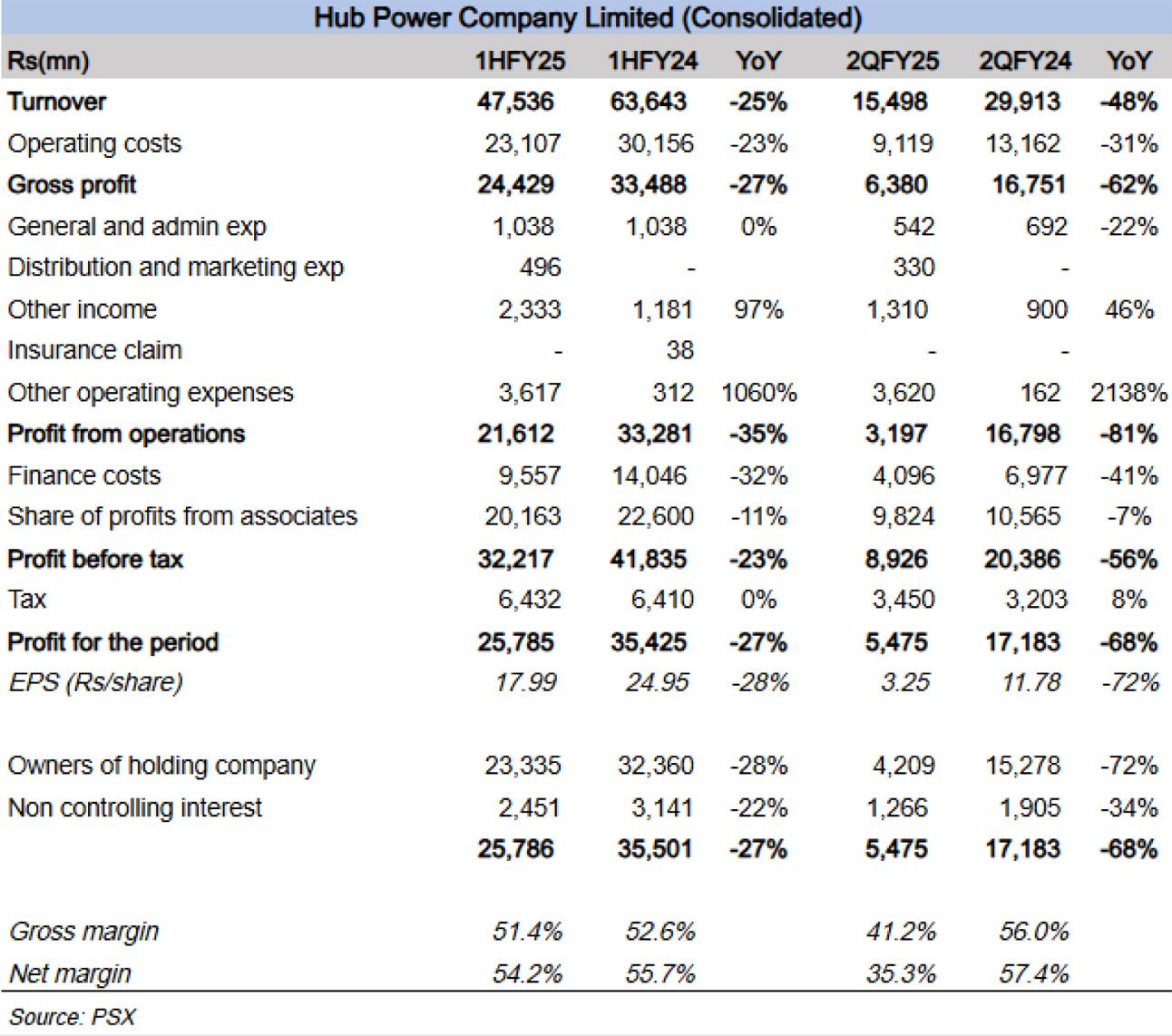

In FY25, HUBC continues to navigate challenges but has witnessed a decline in earnings growth. The company reported a 28 percent year-on-year decline in earnings for 1HFY25, with 2QFY25 profit dropping sharply by 72 percent year-on-year. This downturn was primarily due to the termination of the Hub base plant’s Power Purchase Agreement (PPA), which significantly impacted revenue.

For 1HFY25, revenues declined by 25 percent year-on-year, while 2QFY25 revenue dropped by 48 percent. Gross profit also fell by 27 percent and 62 percent year-on-year in 1HFY25 and 2QFY25, respectively, mainly due to the absence of earnings from the base plant.

HUBC’s finance cost supported the bottom line, as it declined by 32 percent in 1HFY25 and 41 percent in 2QFY25. This drop was driven by lower debt levels and declining interest rates. However, bottom-line growth was negatively impacted by a surge in other expenses, primarily due to the disallowance of the late payment surcharge for the Narowal plant. As a result, other expenses soared 22 times year-on-year in 2QFY25 and 11 times in 1HFY25.

Thar coal-based plants remained operational, while earnings from Prime International declined, further weighing on profitability. Additionally, a lower share of profits from associates and higher taxation contributed to the slowdown in profits. During this period, HUBC also provided capital to HPHL and may allocate further funds for its investment in BYD.

Back in FY24, HUBC declared a lower dividend of Rs20 per share, down from Rs30, reflecting higher capital expenditures and new investments. In 2QFY25, the company announced a Rs5 per share payout, marking a partial resumption of cash distribution.

Looking ahead, HUBC’s strategic investments in Thar coal, BYD, and CPEC-related projects will be key drivers of long-term earnings growth. However, short-term profitability and dividend sustainability may remain under pressure due to higher taxation and restructuring costs.

Comments

Comments are closed for this article.