KSB Pumps Company Limited (PSX: KSBP) is a KSB group company incorporated in Pakistan in 1959. The company’s core business is the manufacturing and selling of industrial pumps, castings, valves and related products for industrial, construction and business services, energy, water and waste water applications. The company has its production facility in Hassanabdal, Punjab along with a full-fledged foundry. Besides catering to the needs of local market, KSBP has a significant export market in USA, UK, Canada, Australia, France and Germany. KSBP is a subsidiary of KSB SE & Co. KGaA.

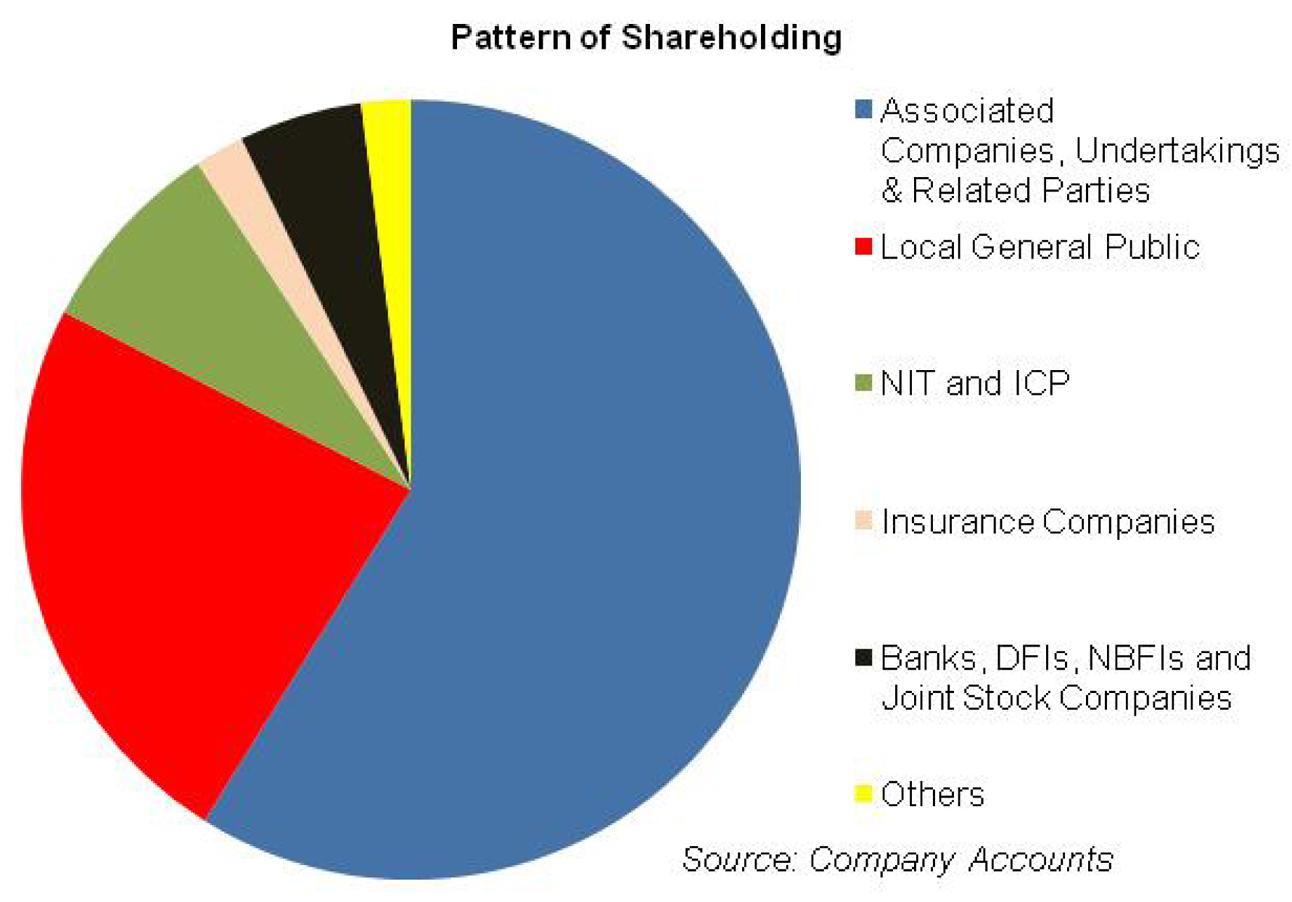

Pattern of Shareholding

As of December 31, 2021, KSBP has a total of 13.2 million shares outstanding which are held by 946 shareholders. Associated companies, undertakings and related parties have the highest stake of 58.89 percent in the company followed by local general public holding 23.65 percent shares. NIT and ICP account for 8.24 percent of KSBP’s shares while Banks, DFIs, NBFIs and Joint stock companies have a collective ownership of 5.11 percent shares. Insurance companies have a shareholding of 2.06 percent in KSBP. The remaining shares are held by other categories of shareholders.

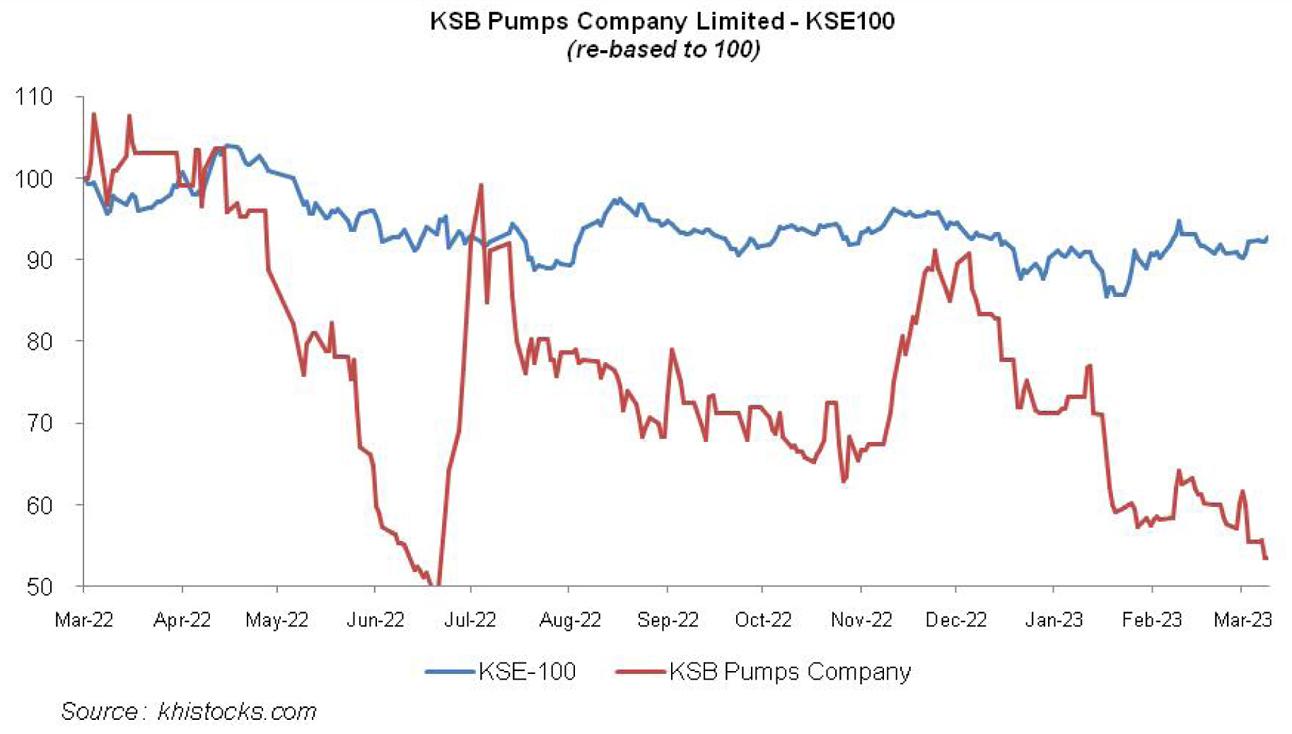

Financial Performance (2018-22)

The topline and bottomline of KSBP which had been dropping in 2018, 2019 and 2020 started rising thereafter.

2018 was a slow year for the company on account of sluggish public sector activity considering the fact that it was a year of general elections and there was a restriction on development fund since April 2018. While the industrial sector remained strong and proved to be the largest contributor to KSBP’s revenue during the year but couldn’t offset the lackluster demand in the public sector, resulting in a topline dip of 3.2 percent year-on-year in 2018. Cost of sales continued to grow on the back of currency devaluation which jacked up the cost of production resulting in GP margin clocking in at 13.4 percent in 2018 from 22.4 percent in 2017. Finance cost grew due to investment in a new fully automated foundry. However, “other income” played the game-changer role in 2018 and resulted in the NP margin being higher than the OP margin. In 2018, other income magnified to Rs. 226.66 million mainly on account of sundry income whereby KSBP had reversed the group service provision maintained since 2014 on the instructions of KSB SE & Co. KGaA. NP margin for 2018 clocked in at 3.96 percent versus 7.74 percent in the previous year.

In 2019, the topline dipped by 24 percent on the back of low public sector spending as there was a drastic cut in development expenditure. There was a significant business from the oil marketing companies as a result of infrastructure development. Export sales also picked up during the year. However, tamed public sector activity resulted in low production and sales of KSBP. Cost of production also took a nosedive resulting in the GP margin of 19.5 percent in 2019. Operating expenses were in check which dipped by 8 percent year-on-year, resulting in 142 percent year-on-year jump in the operating profit. This culminated into an OP margin of 5.1 percent in 2019 versus 1.6 percent in the previous year. While the GP margin and OP margin turned out to be greater than the previous year, finance cost didn’t prove to be kind enough to buttress the bottomline and elevated by 213 percent year-on-year in 2019 due to high discount rate coupled with high short-term borrowings during the year. Other income also dipped by 58 percent year-on-year principally because of high-base effect on account of sundry income in the previous year. This put a dent on the bottomline which shrank by 55 percent year-on-year with NP margin standing at 2.3 percent in 2019.

2019 was followed by another slow year due to COVID-19 which not only affected KSBP’s local business but also turned down the growth prospects in its export business due to worldwide lockdowns and supply chain disruptions. The topline slid by 4 percent year-on-year. This could’ve been worse had the water and general industry market area not provided reasonable growth in orders. Cost of sales and operating expenses were kept quite in check during the year, however, GP margin and OP margin dropped to 16.5 percent and 2 percent respectively. Other income didn’t buttress the bottomline either as KSBP didn’t make any exchange gain during the year. Finance cost provided a little breather due to discount rate cut during the year coupled with a drop in short-term finances secured during the year. The bottomline plunged by 81 percent year-on-year with NP margin moving down to 0.5 percent in 2020.

In 2021, the company’s business activity geared up with a topline growth of 20 percent year-on-year. Although economic activity remained weak in the 1HCY21, the recovery in the second half of the year spoke for itself. The main areas which propelled KSBP’s growth in 2021 were general industry, petrochemicals, building services, foundry business and intercompany export business. There were significant price pressures and supply disruptions during the year. The company was able to partially pass on the price increase to the customers, however, GP margin turned out to be 13.7 percent in 2021. Operating expenses grew in line with inflationary pressure, however, operating profit slid by 49 percent year-on-year with OP margin hovering around 1 percent in 2021. Other income and finance cost provided the much needed support to the bottomline which grew by 66 percent year-on-year. NP margin marginally rose to 0.6 percent in 2021.

2022 also proved to be a great year for KSBP despite all the economic headwinds. Sales revenue grew by 15 percent year-on-year. GP margin and OP margin which had been dropping since 2020 started recovering in 2022. GP margin stood at 15.6 percent while OP margin stood at 3.2 percent. Other income did a tremendous job during the year by expanding by 65 percent over last year. While the detailed financial statements of 2022 are not available, we can assume that exchange gain might have worked its magic. However, the growth in other income was overshadowed by finance cost multiplying by 131 percent in 2022. This resulted in bottomline growth of 59 percent year-on-year with NP margin of 0.9 percent in 2022.

Future Outlook

During the first week of 2023, KSBP had to shut down its plant operations due to lack of demand in the local market due to leisurely economic activity on the back of uproar in inflation, Pak Rupee devaluation and low purchasing power of consumers. This put brakes not only on the industrial sector but also on the public sector spending. This coupled with import restrictions deprived the company of essential raw materials to fulfill export orders. While the company has resumed its operations, KSBP’s sales isn’t expected to post any striking growth in the ongoing quarter as its major clients have either shut down or scaled down their production. Moreover, high cost of production and finance cost will keep the margins constricted.

Comments

Comments are closed for this article.