The current account was in deficit in Dec-2020 after five straight months of surpluses. This coupled with SBP forward guidance on monetary policy to keep the stance accommodative is making some worry on the currency movement, given the current account deficit may continue. Real Effective Exchange Rate (REER) from its recent low of 91.8 in August 2020 moved to 99.4 in November 2020. But this does not mean that any currency depreciation against USD is warranted anytime soon.

The basic principle of economics is that there is always a trade-off. If one variable is eased (interest rates), the other variable has to be tightened (currency) relatively to keep the external system in equilibrium. But everything must be seen in context. The high CAD in December and REER at 99.4 in November should not send jitters through the currency market. And it has not, even after the forward guidance of accommodative monetary policy.

With Pakistan entering into flexible exchange rate regime, short term rates are driven by market flows and sentiments. Both are positive right now. The SBP reserves were up by $300 million in December despite CAD of $662 million. These had some impact on the currency – PKR depreciated by 0.6 percent against US dollar.

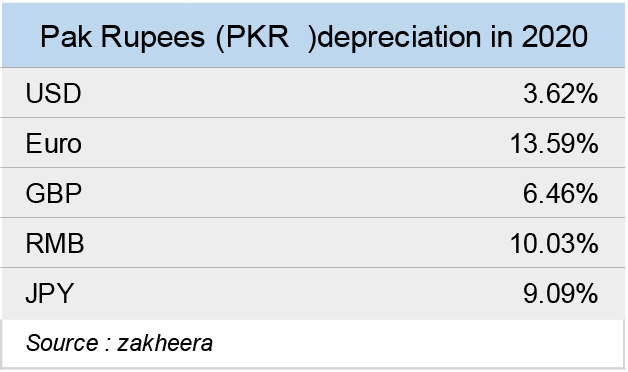

In fact, the currency depreciated significantly against major currencies in 2020 – 13.6 percent against Euro, 10.0 percent against Chinese RMB, 9.1 percent against Japanese Yen, 6.5 percent against British Pound and 3.6 percent against USD. The fact is that the USD is falling against other currencies and since in Pakistan normally only looks at the USD as the benchmark, an illusion is building that currency could be under pressure.

However, that might not be the case. Exporters are adequately compensated in Europe and imports are adequately becoming expensive from China. Seeing this and market-based flows, it seems that PK Rupee against USD will fairly remain stable in the short run (next 1-2 months).

In the medium term, the currency movement follows the fundamental value (as is the case for any other commodity or stock). There are three ways to look at the fundamentals. REER, current account, and financial/capital accounts. REER coming at 99 should not raise flags. The number is believed to have come down to 97-98 in December as PK Rupee depreciated in December and the inflation at home is lower. The trend of low inflation shall continue in January – expectation of below 7 percent.

On current account, the high deficit in December seems to be one–off. In January, based on the market flows, it seems, it would be marginally in deficit, if not in surplus. The higher commodity imports and dividend payments (norm at the end of year) kept deficit high in December. The six-month number is surplus, and outlook does not foresee a big deficit anytime soon. No pressure from here.

The capital/financial accounts situation is fine. The current account surplus was $1.1 billion in Jul-Dec and SBP’s reserves are up by $1.3 billion in the same time. This means that capital/financial account was in surplus of $200 million. Then SBP reduced its forward/swap liabilities by $1.2 billion in Jul-Dec. This implies that market based flows are in surplus and SBP is buying from the market. The overall forex flows are up by $2.5 billion (including off balance sheet items). Hence, no pressure on capital/financial accounts.

Seeing all this, the currency is fairly comfortable at current levels. There is no pressure of depreciation in the next 1-2 months. Once the IMF is back, it would be interesting to see the quarterly targets and that would imply how much SBP would be buying from the market. And if the targets are stiff and there is some current account deficit (March onwards), then currency may come under some pressure. Inflation would be in double digits in Apr-Jun 20 too. The key variable to look, apart from these, are capital/financial account flows such as RDA, issuance of bonds/Sukuk in international markets, and FDI.

Comments

Comments are closed for this article.