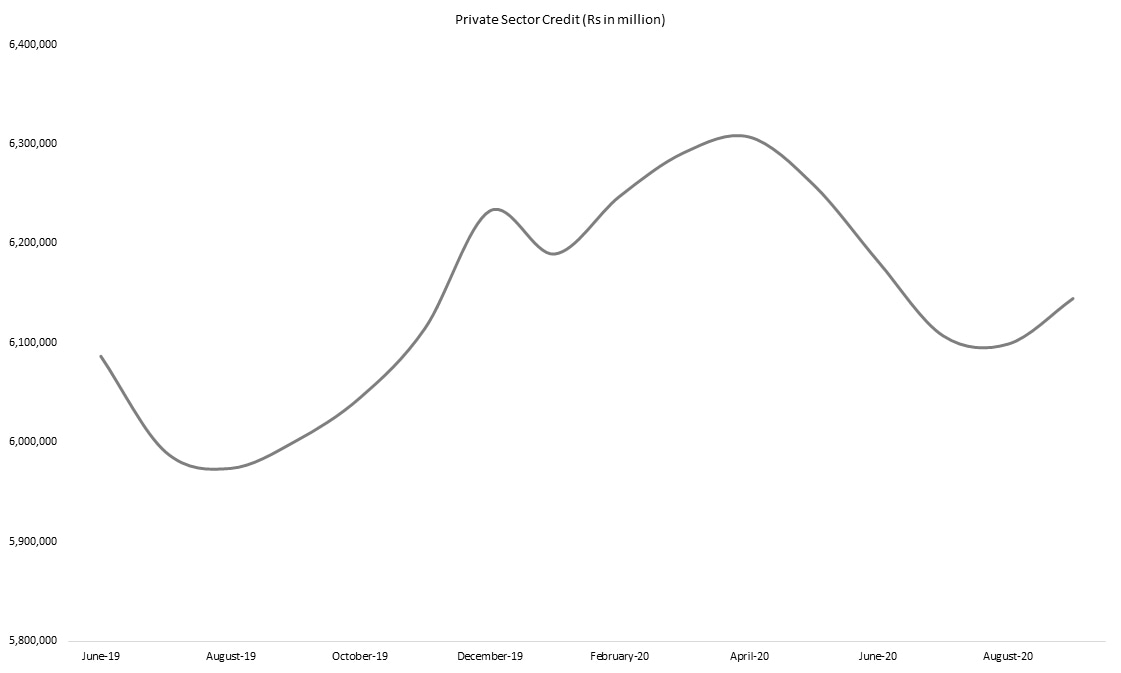

Loans to private sector businesses have continued to decline since December 2019, plateauing around Rs6.14 trillion by the end of September 2020. Despite a hefty decline of 625 basis points in the policy rate, the plunge in borrowing was worsened by the pandemic, as risk-off mode continues to prevail, and credit offtake stays muted. Restructuring, or rescheduling of loans worth more than Rs844 billion; making up 13.86 percent of private sector credit has also kept risk appetite of lenders subdued, as a significant portion of the lending book is either rescheduled, or restructured given unexciting economic prospects.

On the flipside, there has been an uptick in credit available under various schemes announced as a stop-gap measure by the central bank. Over the past six months, credit disbursements under Temporary Economic Refinance Facility (TERF) accumulated to Rs86 billion, primarily due to its long-tailed nature, and the subsidised rate offered by SBP. Notably, more than Rs241 billion have been requested under the facility, but banks have been very selective in assuming credit risk under prevailing circumstances.

Maximum mark-up rate for TERF is capped at five percent – but most entities with good credit standing are able to acquire long-term debt at a spread of 2-3 percent over the central bank’s rate of one percent. Such a subsidy provides a hedge against increasing interest rates (throughout the term of the debt), while also making available credit at significantly subsidized rates. This implies that there exists appetite to borrow and invest in long-term projects, but that is at a rate, which is at least 3-4% lower than prevailing interest rates.

Similarly, credit disbursements under the Wage Scheme over the last six months have accumulated to Rs48.7 billion, among at least 1,957 entities to support the wages of their employees.

If disbursements under these schemes are adjusted from total private sector credit outstanding – then credit private sector credit amounts to Rs6 trillion which is close to its twelve-month low, last witnessed in September 2019. In essence, without concessional debt, even a 625 basis points drop in policy rate was not able to trigger credit offtake – but it still did stimulate credit growth at slightly lower concessional rates.

This lays some groundwork for another round of monetary expansion to stimulate credit, and consequently economic growth. However, inflationary pressures largely driven by supply shocks are deterring further cuts in the policy rate. Will there be an interest rate reversal before any significant offtake in private sector credit? Or will policy makers take a pro-growth route and extend the easing cycle – which would also align with the goal of accelerating growth of mortgages in the country.

Comments

Comments are closed for this article.