“Cause it don’t matter now what you do”, sang The Duke in 1967. It is as if he were speaking of the endless sugar price rally, which has taken a life of its own. Historic trends, Covid-19, food inflation, and demand compression now mean little to domestic commodity prices, because the music just won’t stop.

Back in May, an official of Pakistan Sugar Millers Association told BR Research that ‘the country had been saved from a price spiral in 2020 marketing season”, as the nationwide lockdown had brought sugar offtake down to a trickle”. Five months on since that pep talk, sugar prices have increased by 20 percent, and nearly 40 percent since last crushing season began in December 2019.

If national average retail price finally scores a century in November, it may at least bring some cynical comfort: the milling industry shall find a catchy benchmark to compare all future price reductions (hopefully).

Of course, the industry cannot be faulted if economic contraction coupled with double digit food inflation has failed to deter consumers from reducing their monthly ration of sugar. What other circumstantial evidence is needed to prove that sugar is a staple commodity in Pakistan? Even cigarette smokers probably display more price elasticity of demand than sugar addicts.

Except, some readers may find it tough to move past faulting the industry. “Cost of holding has declined significantly”, they argue, as monetary easing has brought down inventory carrying costs. Except, what is millers’ incentive to hold on to stocks right before the next harvest starts? 2020-21 season has so far only brought good news from farms. Crop outlook looks positive, and industry may finally be looking at a surplus season. And with input subsidy on fertilizer reaching growers, there are slim chances of an increase in procurement price either.

It is true that the industry has in the past used high opening stocks as an excuse to seek permission to export, but only a miracle may allow mills to pull that sleight of hand again this year. And if the millers sitting at farmgate have found no wisdom in hoarding, why would whole-sellers and dealers bet any differently?

Which brings us to the theory that has been reverberated in this space ad nauseum. That assuming average monthly consumption of 0.45 million tons, national stocks may fall to dead-level by November end. This means that even if demand has shrunk by 5-10 percent due to abnormal price increase, domestic stocks may not be sufficient to last beyond third week of December. This means the market can ill-afford any delays to crushing, as occurred in the outgoing season.

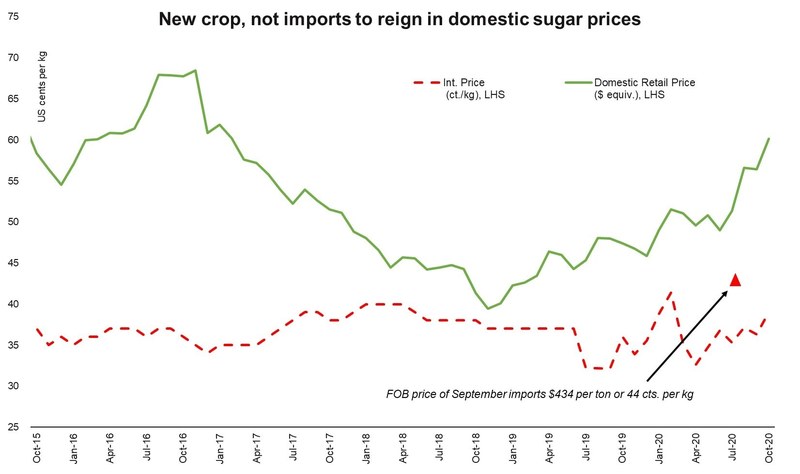

Hence, the imports. Although only a trickle had landed by September end – 28,429 tons against a shortfall of 0.25 – 0.35 million tons (in case crushing does not go in full swing by December second week). Note, that this is the first consignment to land against the duty-free import quota announced earlier this year. Interestingly, FOB price of imported sugar is Rs 72 per kg, which after including value chain margins of 15– 25 percent may be available for retail at Rs 85 – 90 per kg.

Therefore, imports made thus far shall have little bearing on domestic prices, considering the shortfall could be substantial in case of delayed crushing (not unheard of), and domestic prices are already retailing at Rs 98 per kg. And even with a carte blanche on duty free imports, no trader will make the mistake of flooding the market with large import volumes right before crushing begins – especially at a time when forecasts of surplus crop are aplenty.

Moreover, international prices have been resurgent, having climbed by one-fifth since they crashed in April 2020 when the global lockdown began. If the trend continues, soon imported and domestic retail prices may be at par.

But the theory presupposes that domestic prices will not increase in tandem with international prices. Ordinarily, they should; except commodity markets follow pre-deterministic paths, no matter how distorted any market may be. As the domestic monthly price chart indicates, retail prices (in Rupee terms) reverse gears at the beginning of every crushing season without fail. If the raw material crop outlook is positive, is there any reason why 2020-21 marketing year should be any different? The speculators rule will soon come to an end; whether it will take four weeks or eight, that’s the real bet.

Comments

Comments are closed for this article.