Since mid-2000s, Pakistan's major crops segment has underperformed other segments of the economy, including other agricultural heavyweights such as livestock. Consisting of wheat, cotton, rice, maize and sugarcane, major crops have particularly struggled during the last 5 years, when segment growth has often drifted in the red, averaging close to negative two percent.

Does that mean all crops are suffering? Not quite. Since the last GDP rebasing exercise in FY06, four out of five major crops have witnessed growth in output (volume). Of these, maize, sugarcane, and rice have posted decent CAGR of 6.22, 2.93, and 2.09 percent, although wheat output has increased at a muted rate of 1.14 percent. Why then is the cropped segment said to be underperforming?

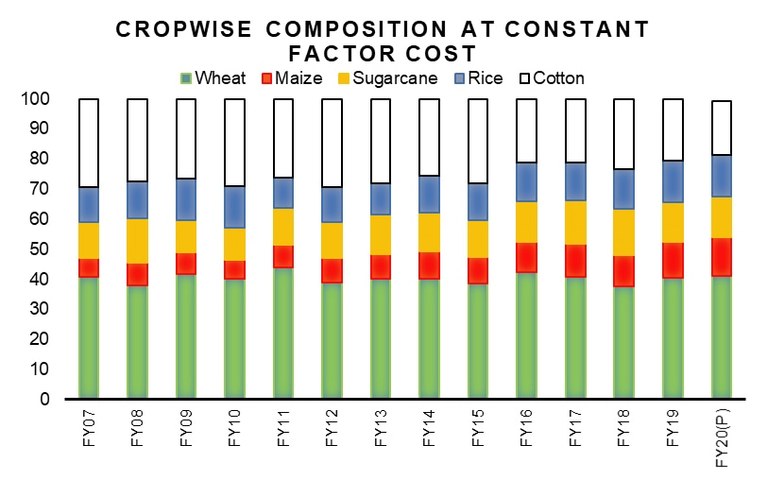

Two reasons. First is the sectoral GDP composition. Back in 2006, wheat and cotton together constituted the lion’s share within major crops, at over 70 percent of major crops index. Because the two crops have witnessed stunted (or in cotton’s case, negative) growth during the intervening years, this has often painted a picture of a segment in recession. Meanwhile, even as output of crops such as maize, cane, and rice has increased significantly during the period, these have failed to translate into commensurate GDP growth due to constant factor costs set at base year prices of FY06.

But an even greater reason why cropping segment is seen to be underperforming are the missed output targets set at the beginning of every season by Federal Committee on Agriculture. Here, the disappointment is multifold. Although the FCA sets higher output targets for each major crop every year - cotton being a conspicuous exception – the increase in target output is invariably driven by an increase in targeted area, instead of an increase in yield, latter being the universal indicator of farming productivity.

Between FY16 – FY20, targeted increase in yield averaged at a paltry 0.84 percent per annum for the five major crops. But here is a much more distressing bit: even those negligible increases in targeted yields are routinely missed. The underwhelming performance of productivity is exacerbated by the fact that target yields for cotton and wheat – with their current two-thirds weights in major crop index - have been missed in almost all years. Also consider that during the past five years, cotton missed its targeted yield by over 15 percent on average!

Meanwhile, output of crops such as maize, rice, and sugarcane has been slowly catching up. Apart from few exceptional seasons of water shortfall or depressed demand, the three crops have outperformed targeted output substantially. But is that enough cause for celebration?

It is important to remember the context. Underwhelming increases in yield means that the above par performance is a symptom of mediocre yield targets, especially when acreage achieved is also above target level. For example, during the five-year period under review, rice yield has increased at an annual average growth rate of just 0.16 percent. Similarly, while yields of both sugarcane and maize have made some strides, the rate of increase for each crop is nevertheless stuck below 3.5 percent per annum.

To most readers, Pakistan’s crop productivity challenge should come as no surprise. But it is important to scratch beneath the surface, which reveals that not all crops are created equal. Over the past decade, Pakistan’s two most important crops – wheat and cotton – have underperformed even mediocre target outputs, as yield levels have been on a decline. And while the rest may have arguably witnessed decent increase in output, it has mostly been driven by an increase in acreage rather than productivity.

With gated communities and housing schemes knocking at the doors of Bahawalpur and Rahim Yar Khan – the fertile crescent of Indus – the policy planners at MNFS&R must ask themselves: how long before Pakistan’s farmers run out of land to cultivate?

Comments

Comments are closed for this article.