Suraj Cotton Mills Limited (PSX: SURC) was established in 1984 as a public limited company. The company manufactures and trades high quality yarn and woven fabrics at the four business units it has; three are spinning units while one is weaving unit. Suraj Cotton caters to customers, both in the domestic market as well as in the international market.

Shareholding pattern

Majority of the shares- more than 47 percent are held under the associated companies, undertakings and related parties’ category. Within this, Crescent Powertec Limited is a major shareholder, owning 44 percent of the shares. The next major shareholder are the directors, CEO, their spouses and minor children that hold 29 percent of the shares. Of this, Mrs. Humera Iqbal, spouse of Mr. Muhammad Iqbal, a director of the company holds, about 7 percent of the shares. About 14 percent of the shares are distributed with the general public, while the remaining about 10 percent of the shares are distributed among the rest of the categories.

Historical operational performance

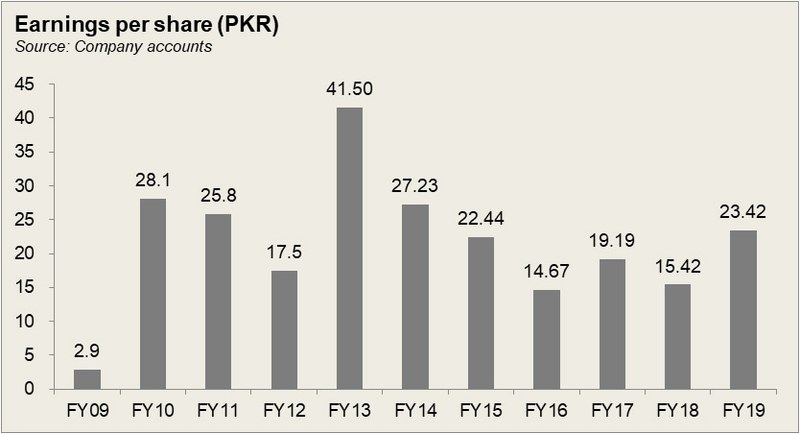

Suraj Cotton’s profits peaked twice in a decade, once in FY10 and then again in FY13 after which it followed a downward trend before rising again in FY19. Sales revenue have been mostly growing, although at varying rates.

In FY15, the company saw a 13 percent decline in its topline. This was the highest decline seen in a decade. It was attributed to a fall in prices accompanied by demand contraction. China is a primary export market for Pakistan’s textile sector; with a fall in demand from China, export sales of the country took a hit, especially in the face of competition from India and Vietnam. Apart from a fall in revenue, which affected gross margins, other factors of the financials witnessed negligible change which kept operating and net margins flat year on year at close to 7 percent.

Sales revenue fell by another 10 percent in FY16 as depressed demand and prices prevailed. With a high cost of energy and shortfall in the production of cotton, the cost of doing business did not allow for domestic players to compete effectively in the international market; it faced competition from regional peers to maintain market share. With lower sales, cost of production as a percentage of revenue rose, whereas operating margin was somewhat supported by other income; latter came from dividend income and gain on disposal of fixed assets. However, it was offset by the collective increase in expenses coming from donations and impairment loss on investments thus reducing net margin to about 6 percent.

Sales revenue recovered in FY17 as it grew by around 8 percent, although this was offset by a more than corresponding increase in costs; the latter was driven by increases in raw material expenses, fuel and salaries expense. Minimum wages were increased while shortage of fuel and energy continued to be an obstacle for smooth operations. This meant that the industry had to look towards more expensive alternatives. This rose the cost of production which made it difficult to compete against regional peers such as India, Vietnam, Bangladesh. The domestic market faced the problem of cheaper imported yarn from India. However, the lower gross margin did not reflect net margin as other income increased to make up nearly 5 percent of topline, as a result of investment income.

There was a whopping 33 percent increase in revenue during FY18, coming mostly from domestic sales, while export sales nearly halved. Within the textile industry the spinning segment witnessed the most decline; the company does not operate in value added industry; hence it was not able to take advantage of currency depreciation since demand for yarn remained subdued. Therefore, it focused on sales in the domestic market. With better sales, gross margins improved, however due to other income nearly disappearing in comparison to previous levels, net margin reduced to 5 percent.

Revenue continued to increase in FY19, partly attributed to an improvement in selling prices. This was possible due to currency depreciation. Despite increase in cotton prices and fuel, the company managed to improve gross margin due to economies of scale. With most other factors remaining unchanged, the effect of this was reflected in the bottomline that increased to 6 percent.

Quarterly results and outlook

The company saw an 11 percent rise in revenue during 9MFY20 year on year, with local sales increasing whereas exports continued to decline, particularly from the weaving segment. While other factors saw insignificant changes, other income more than doubled year on year due to dividend income. This provided notable support to the bottomline and net margin, with the latter increasing to almost 6 percent.

As a result of the ongoing pandemic, demand for yarn and fabric is at an extremely low level, with raw cotton prices declining and industries holding inventories. While there is no doubt that the lock down and shutting down of operations would significantly affect the last quarter of FY20, the effect would also continue into the first quarter of FY21.

Comments

Comments are closed for this article.