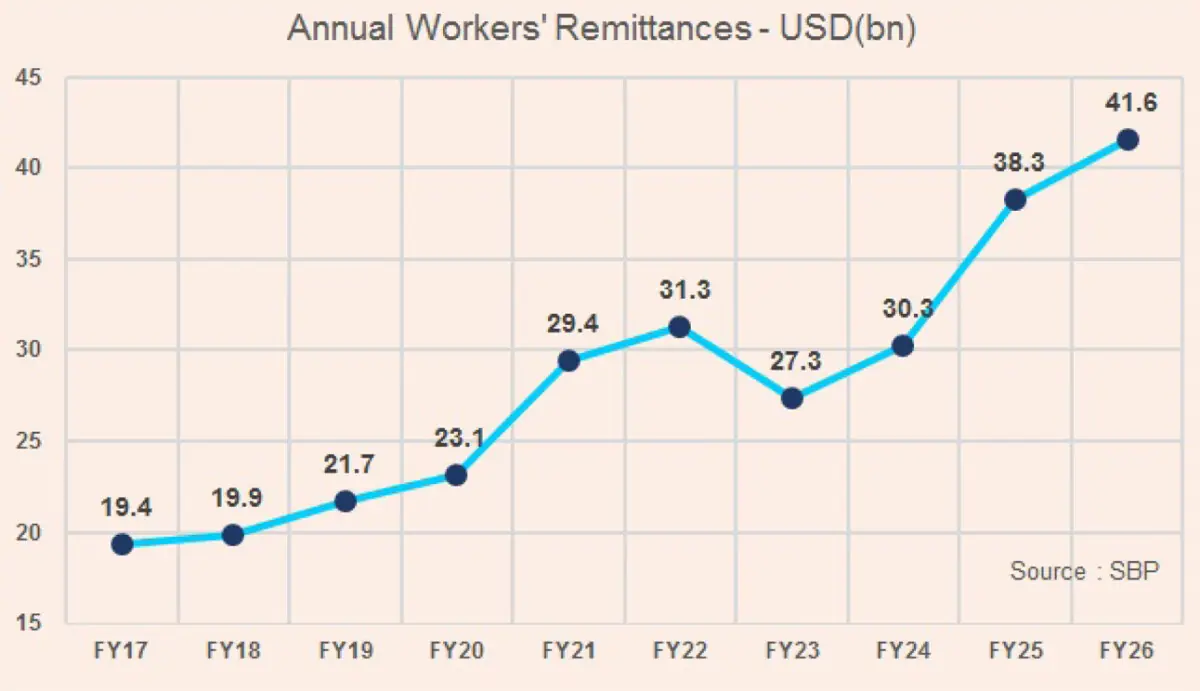

Pakistan’s remittance story ended FY26 on a strong note. Workers’ remittances reached a record USD41.6 billion, up 8.6 percent from USD38.3 billion last year. June inflows stood at USD3.475 billion, lower than the Eid driven peak in May, but still strong by historical standards.

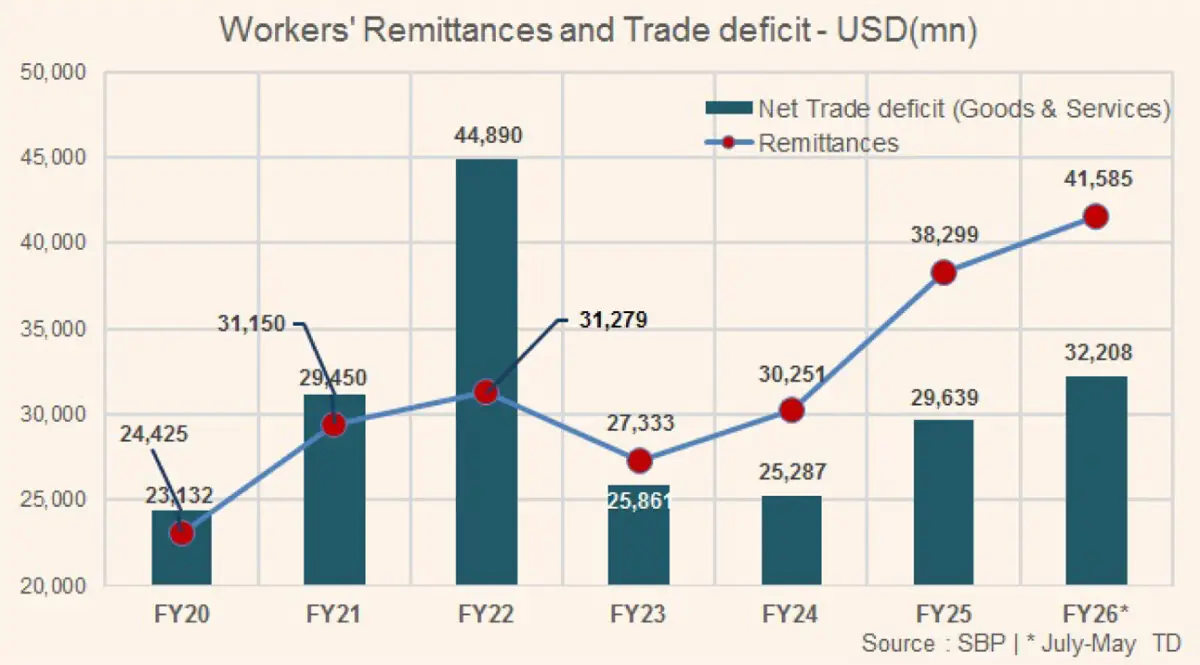

The number matters because remittances once again did the heavy lifting for the external account. In FY26, they were comfortably higher than the country’s net trade deficit in goods and services. That is a very different picture from FY22, when the trade deficit had ballooned against remittances.

The longer trend is even more powerful. Remittances have more than doubled from USD19.4 billion in FY17 to USD41.6 billion in FY26. After slipping to USD27.3 billion in FY23, inflows recovered with a fresh peak in FY26.

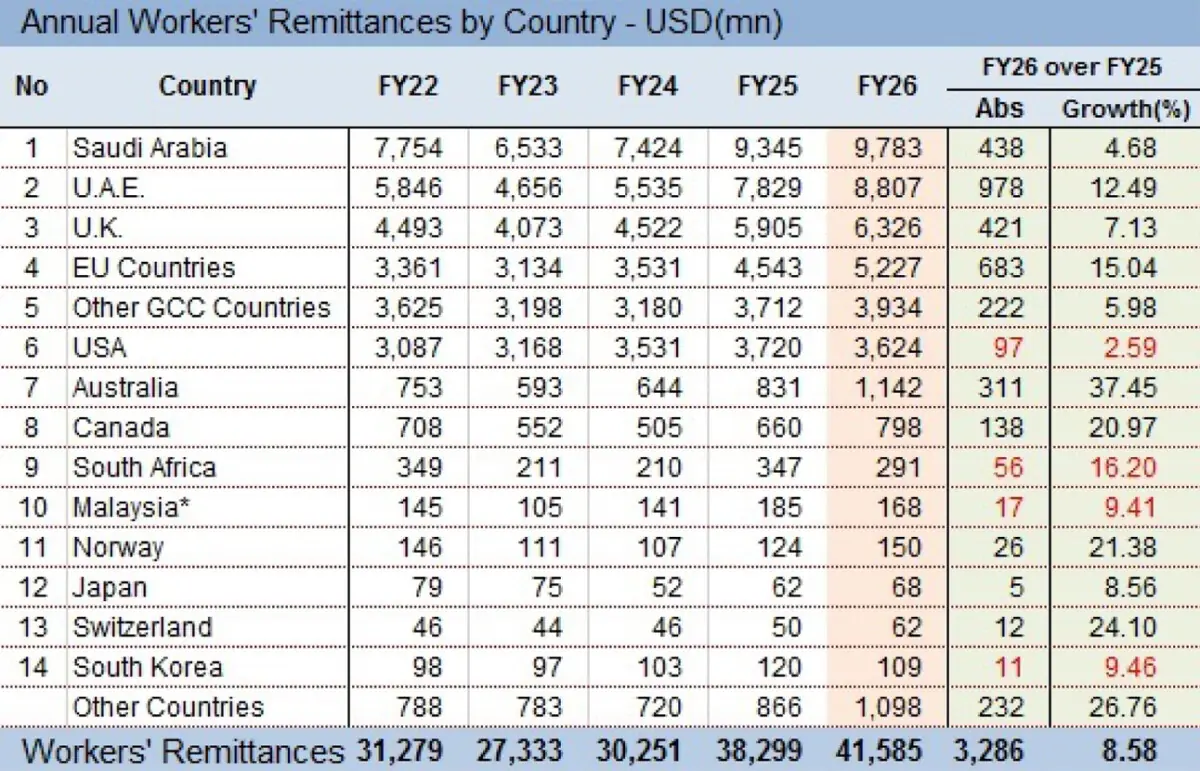

The Gulf remains the backbone of this flow. Saudi Arabia led with USD9.78 billion, followed by the UAE at USD8.81 billion. The UK contributed USD6.33 billion, EU countries USD5.23 billion, other GCC countries USD3.93 billion, and the USA USD3.62 billion.

The UAE was the standout, adding nearly USD978 million over last year, followed by EU countries, Saudi Arabia and the UK.

But the fine print matters. May’s record USD4.25 billion inflow was helped by Eid timing and should not be treated as the new monthly base. June’s decline confirms that some normalization was always likely.

There is also a possibility that part of the recent surge, especially from the UAE, reflects repatriation of accumulated savings or wealth parked abroad, not only regular monthly income.

From July 1, remittances will still remain free for senders and families receiving them, but the government will no longer pick up the bill. Banks will now have to bear that cost themselves. That is fair, because they already gain from remittance flows.

The real test is whether they can keep the service fast, easy and competitive. If they make it costly or complicated, some money can quickly move back to hundi and hawala.

The bigger lesson remains unchanged. Remittances are Pakistan’s strongest external cushion, but they are not a development model. They support reserves, households and the rupee, but they cannot permanently cover for weak exports, low investment and poor domestic savings.

FY26 showed the strength of overseas Pakistanis. FY27 will test the strength of Pakistan’s remittance system. The record inflow has bought breathing space. The challenge is to keep it formal, keep it reliable, and turn it into productive capital.

Comments