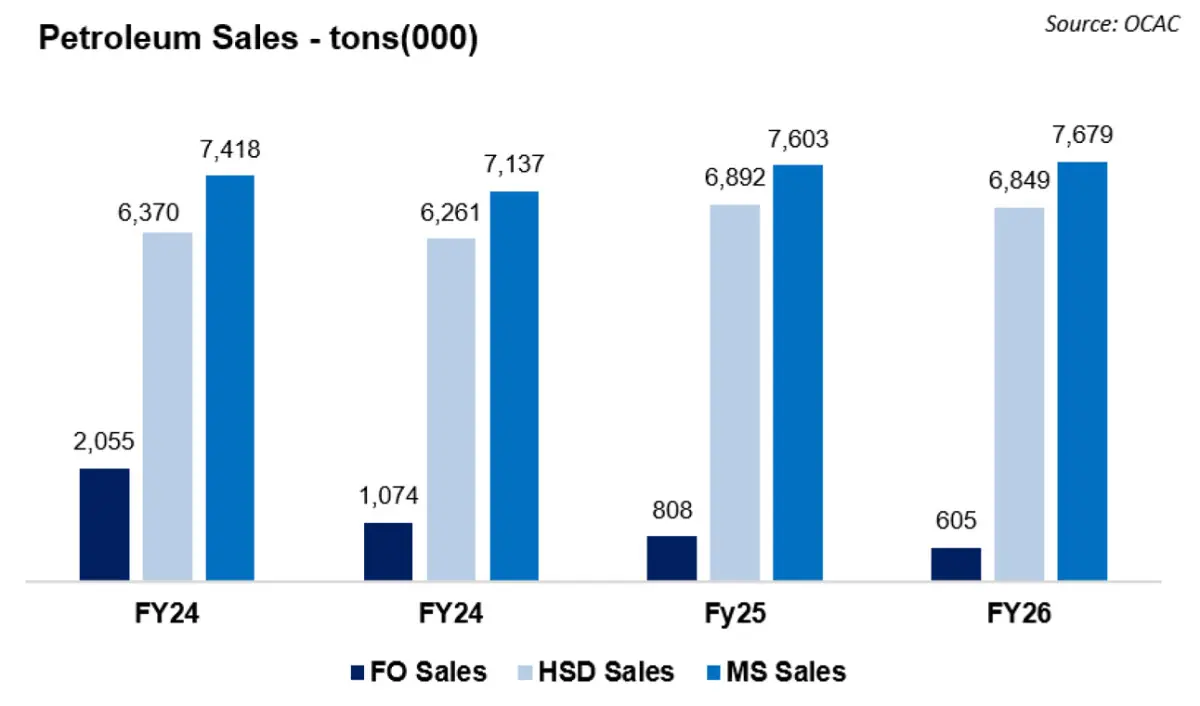

Pakistan’s oil marketing companies closed FY26 with a story that looks stable on the surface but weaker underneath. Total petroleum sales stood at 16.2 million tons during the year, almost unchanged from 16.3 million tons in FY25, showing a marginal decline of around one percent. But the full-year number hides the stress that emerged toward the end of the year, especially after the sharp increase in domestic fuel prices in the final quarter.

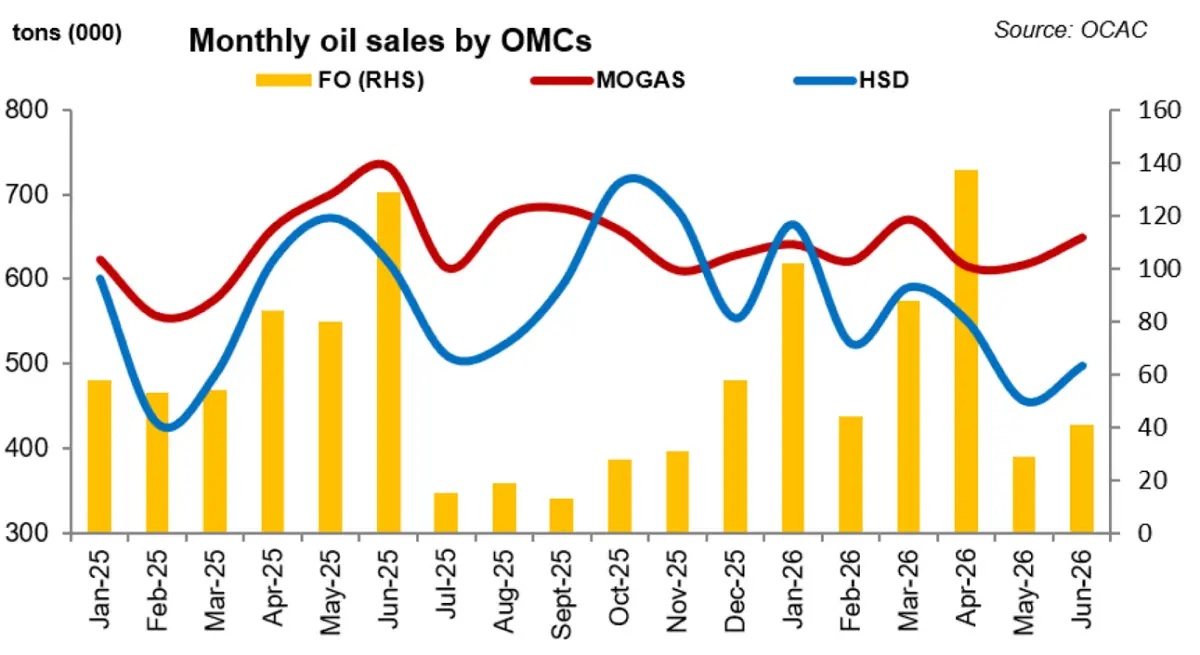

June captured that weakness clearly. OMC volumes fell to by nearly 20 percent year-on-year. Excluding furnace oil, volumes were down 15 percent, showing how quickly fuel demand can soften when prices rise sharply and when the economy is still operating with limited purchasing power.

Petrol sales fell 11 percent year-on-year, while high-speed diesel declined by a much sharper 20 percent. Furnace oil remained the weakest product, falling 68 percent year-on-year.

The only comfort in June was sequential. Compared to May, total OMC sales were up 7 percent. Petrol volumes rose 5 percent month-on-month, while HSD improved 9 percent. This was helped by some price relief during the month as global oil prices cooled and geopolitical pressure eased. But the month-on-month recovery should not be confused with a real demand rebound. Volumes were still well below last year’s level, and the price shock had already done enough damage to demand.

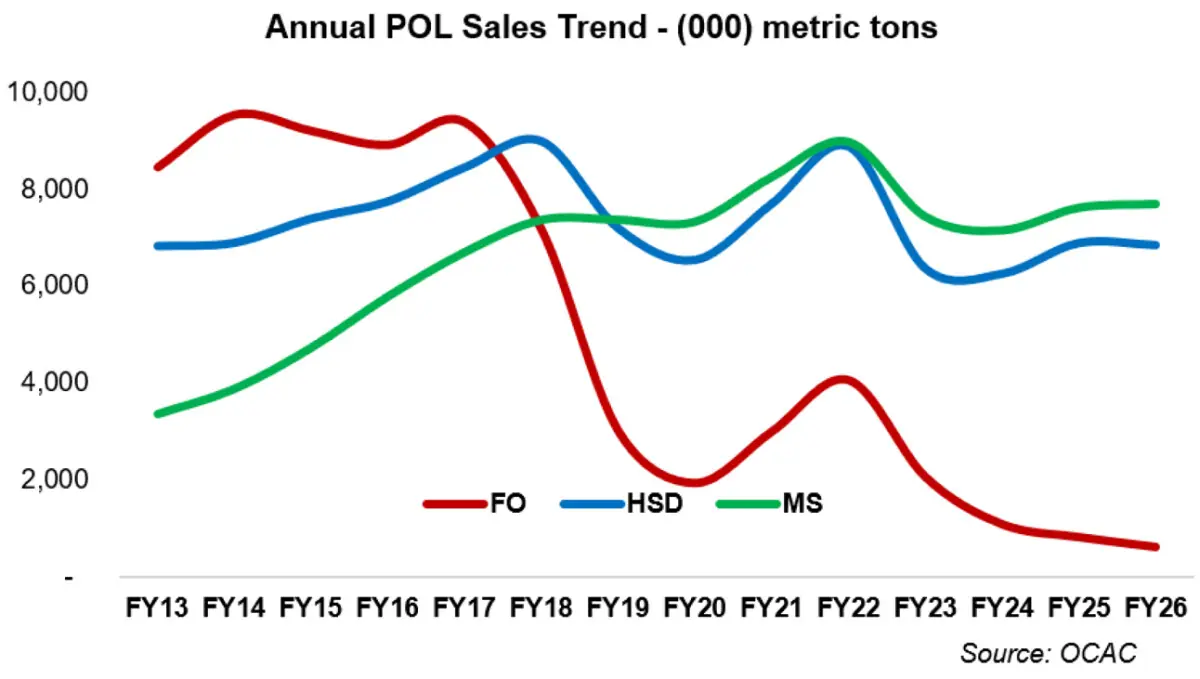

During FY26, petrol remained the most resilient part of the marketrising one percent. This reflects the relative stickiness of urban mobility demand. Even when prices rise, consumers reduce discretionary travel but cannot fully avoid daily commuting. Two-wheelers, ride-hailing, small cars, and urban transport needs keep petrol demand from falling too sharply.

Diesel, however, was almost flat for the year and weak in June. FY26 HSD sales stood slightly lower than last year. The June decline was far steeper because diesel demand is more linked to freight, agriculture, construction, and broader economic activity. Elevated domestic diesel prices also appear to have revived incentives for cross-border smuggling, which continues to distort formal demand.

Furnace oil remained in structural decline. FY26 FO sales fell 26 percent. This is not just a cyclical decline. FO has been losing relevance in the power mix as hydel, nuclear, imported fuels and renewables take a larger role. The sharp year-on-year fall in June was therefore not surprising.

The month-on-month rise in FO sales was more seasonal, linked to higher summer power demand, rather than a sign of durable recovery.

As for the outlook, if international oil prices remain soft and domestic prices continue to ease, petrol and diesel volumes could recover sequentially in the coming months.

But the recovery is unlikely to be aggressive unless prices fall meaningfully and stay lower. Real incomes are still stretched, freight activity is not booming, and the government’s revenue needs leave little room for sustained relief at the pump.

FY26 therefore ends as a year of apparent stability but fragile demand. The headline number says OMC sales were broadly flat. The closing month says consumers and businesses are price sensitive, diesel demand is vulnerable, and furnace oil is fading further. For FY27, the direction of OMC sales will depend less on market share and more on three variables: oil prices, petroleum levy policy, and the strength of real economic activity.

Comments