Energy is back at the center of the inflation narrative.

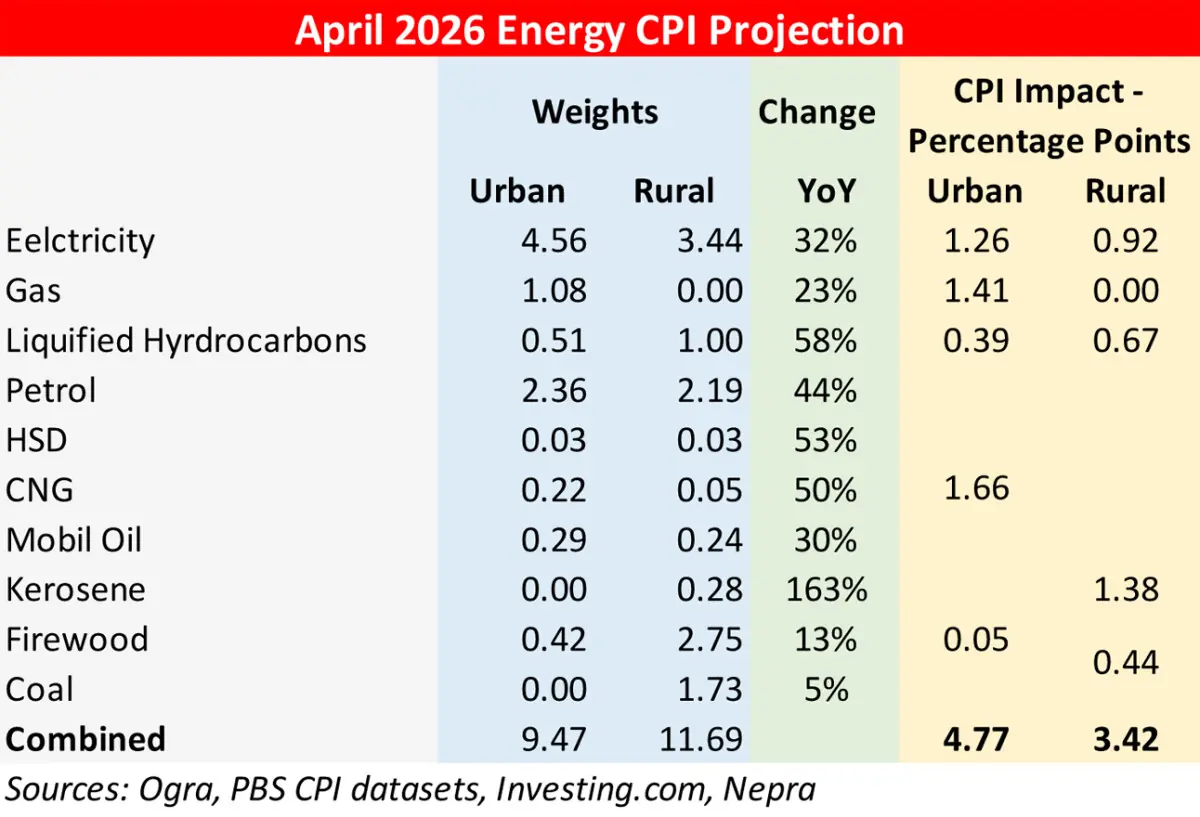

April 2026 CPI is shaping up under the impact of a sharp energy shock, with the projected contribution from the energy basket alone approaching 4 percentage points. This is notable given that energy carries a weight of just about 10 to 10.5 percent in the national CPI. A relatively small segment of the basket is set to account for a disproportionately large share of the headline print, raising the likelihood of a return to double digit inflation.

The impulse is concentrated in a few key items. Petrol, gas, and electricity dominate the urban profile, reflecting direct pass through into transport and utilities. On the rural side, kerosene, LPG, and firewood add meaningful pressure alongside electricity. The scale of increase in some of these components, particularly kerosene and LPG, is amplifying the overall contribution despite moderate weights.

Within transport fuels, it is also worth noting that HSD carries negligible weight in the CPI basket. Despite a steep increase in its price, its direct contribution to CPI remains minimal. The bulk of the transport fuel impact is therefore coming from petrol, which has a much larger weight and more immediate consumer pass through.

Petroleum pricing remains another open front. The petroleum levy on POL products is still not fully maximized, and with IMF conditionalities in play, the room for further increases remains intact. This implies that even in a scenario where global oil prices ease or geopolitical tensions subside, domestic relief may be limited. Any potential price cuts could be partially offset by efforts to recoup revenue shortfalls accumulated over the past couple of months, particularly on HSD. In effect, the downside to energy inflation may be capped, while upside risks remain firmly in place.

The risk extends beyond the first round. Energy pricing in Pakistan is administered with lags, particularly in electricity and gas. Quarterly tariff adjustments, fuel cost adjustments, and revisions linked to fiscal targets can keep feeding into inflation even after the initial shock. This creates the potential for a second round of price pressures across transport, food, and core goods.

There is also an emerging policy tradeoff on the power side. Reducing load shedding would likely require higher effective tariffs or lower subsidies, implying pricier electricity for consumers. The choice in the coming months may increasingly be between fewer hours without power and significantly higher electricity bills.

The base effect further sharpens the picture. April 2025 CPI stood at just 0.28 percent, a multi month low. This sets up a strong year on year rebound even before factoring in current price momentum. With both base and energy dynamics aligned, the headline number is all set to swing into double digits.

This trajectory is consistent with the risks flagged in the latest monetary policy stance by the State Bank of Pakistan, which highlighted energy price adjustments and global commodity volatility amid ongoing geopolitical tensions. The current projections suggest that energy is not just a risk factor. It is now the primary driver of the near-term inflation outlook.

Comments