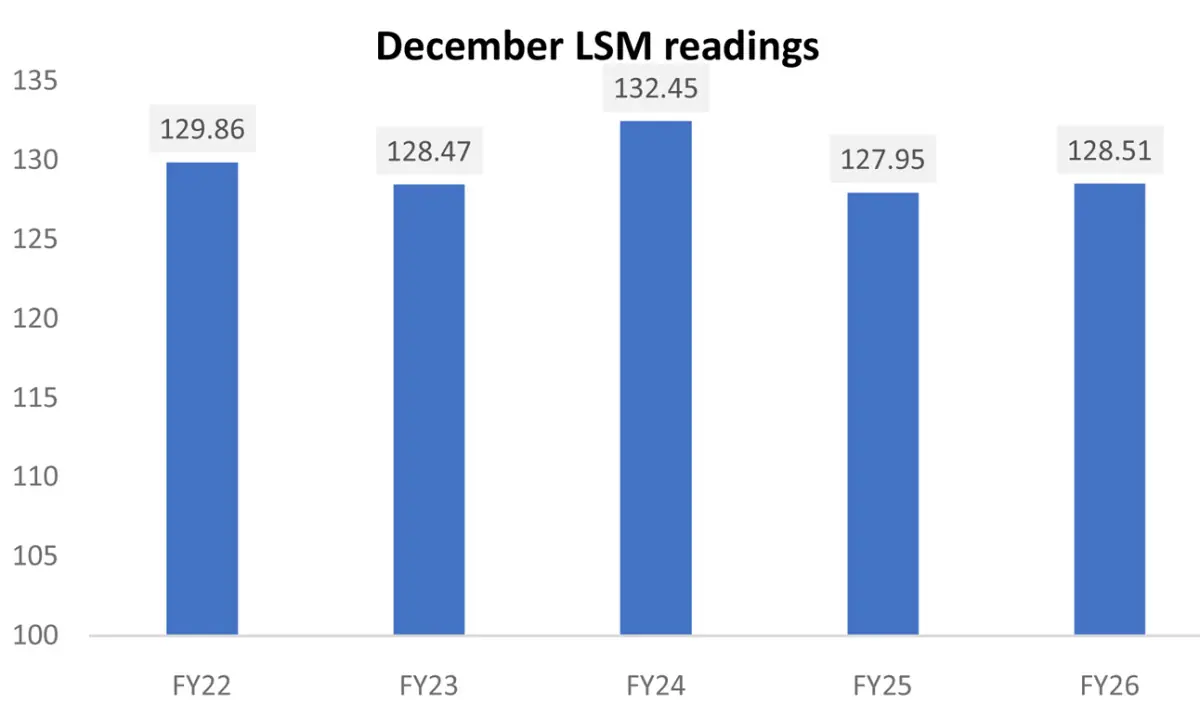

After an exceptionally strong November, Large-Scale Manufacturing entered December on a softer footing. Year-on-year growth slowed to 0.44 percent, the weakest reading since March 2025, signaling consolidation rather than reversal.

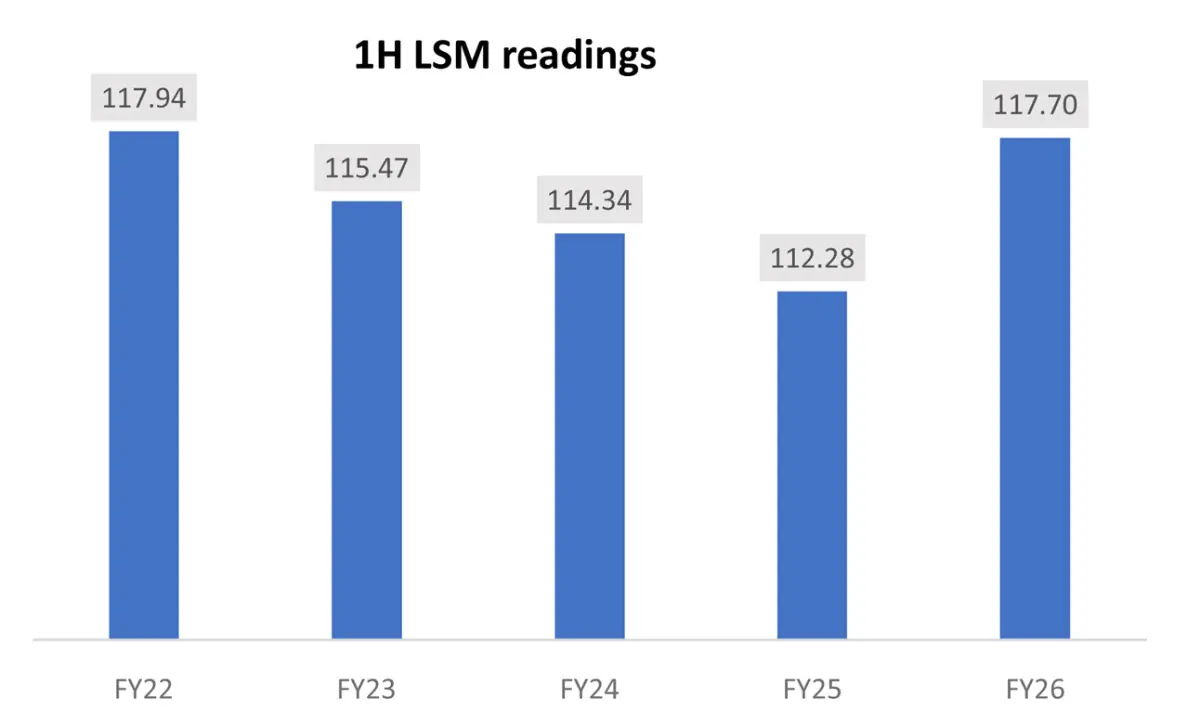

On a cumulative basis, however, LSM growth for 1HFY26 stands at 4.82 percent, with the index level for the first half ranking as the second highest ever for this period, marginally below the peak recorded in 1HFY22.

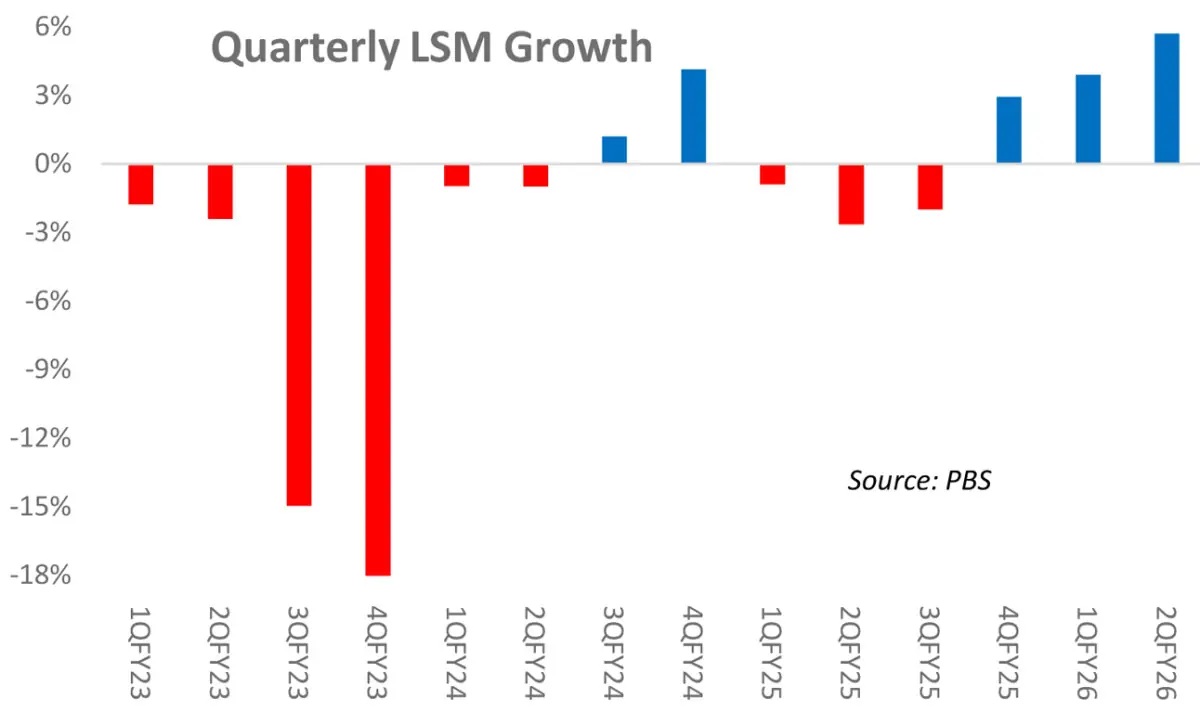

Pakistan has now recorded three straight quarters of positive LSM, which is a first since 4QFY22.

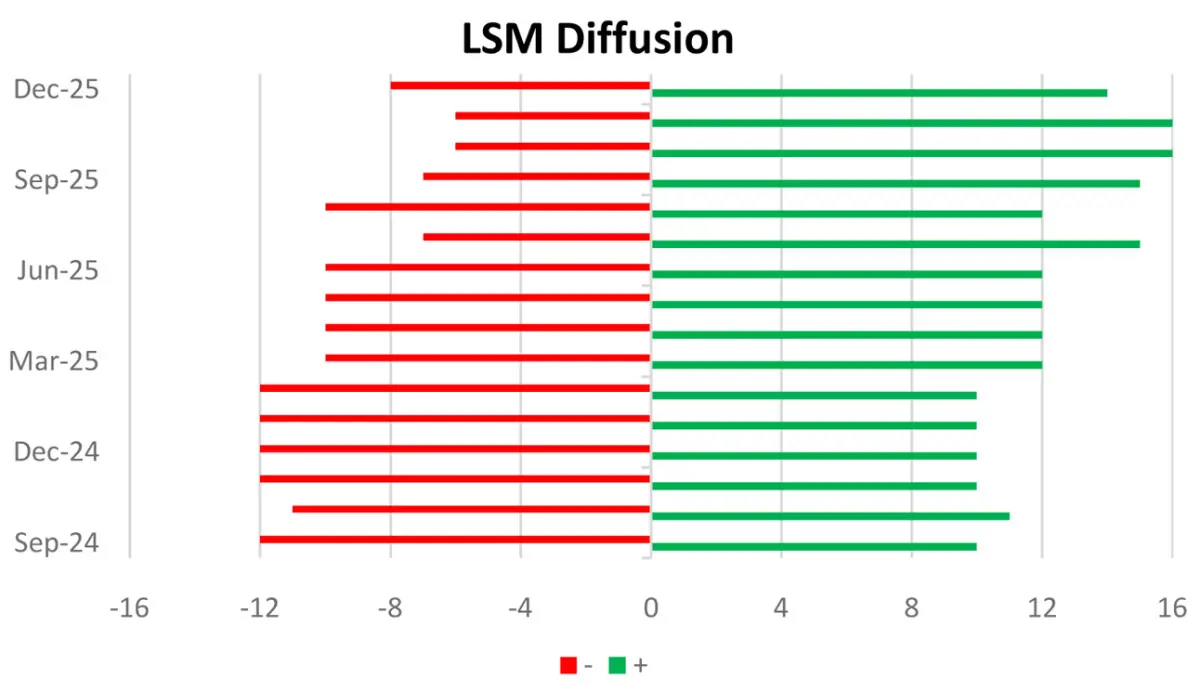

The diffusion index reflects a mild correction in breadth, but not a breakdown.

On a cumulative basis, 14 industries remain in positive territory while 8 are contracting, compared to 16 positive and 6 negative after five months. For December alone, nine industries were in the red, yet the overall growth profile remains broad-based.

Importantly, the sectors posting declines largely carry limited weights, with chemicals and pharmaceuticals being the notable exceptions.

Sectoral leadership rotated once again. Wearing apparel emerged as the single largest contributor to December LSM growth, tracked through export quantities of readymade garments.

Momentum here appears intact heading into the new year. January export data already shows readymade garment quantities at the highest-ever monthly level, suggesting that apparel is likely to remain a key growth driver in the near term.

Automobiles continue to provide a steady backbone to LSM, while petroleum sector growth moderated in December after an outsized November performance.

Despite the slowdown, petroleum remains a major contributor on a cumulative basis, ranking third after automobiles and wearing apparel. This follows record production of both petrol and high-speed diesel in November, which had lifted the sector to its highest index level since May 2018. December deceleration therefore appears more like normalization than fatigue.

Food sector dynamics turned less supportive. Sugar production fell 9.4 percent year-on-year and marked the lowest December output since 2021. With food and textiles together accounting for roughly one-third of total LSM weight, muted performance in both categories largely explains why headline growth has settled into low single digits. Textiles remained broadly flat, continuing a pattern of stagnation outside the export-oriented garment segment.

Pharmaceuticals remain a drag despite earlier signs of life in tablet production. December did little to alter the subdued trend, keeping the sector among the more persistent underperformers.

In contrast, transport-related segments stayed resilient. Motorcycle and bicycle production remained close to 4-year and 6-year monthly highs, respectively, reinforcing strength along the mobility value chain.

From a macro perspective, the environment continues to turn incrementally supportive. The interest rate cycle is easing, energy prices are materially lower than one and two years ago, and the latest reduction in industrial electricity tariffs adds to existing incentives on incremental consumption. These factors are improving cost visibility and underpinning capacity utilization, even as monthly growth rates fluctuate.

Perspective, however, remains critical. FY22 remains the reference point, and it is increasingly clear that matching it in FY26 is improbable. LSM growth would need to average close to 17.5 percent over the remaining six months to reach that benchmark. What the data does support is a more durable shift. The recovery is no longer narrow, sporadic, or policy-dependent. Growth has cooled in December, but the underlying base has widened enough to suggest that LSM has moved beyond a short-term rebound and into a more sustainable phase of repair.

Comments