While the company remained solidly profitable, Pakistan Petroleum Limited (PSX: PPL) delivered a weaker earnings profile in 1HFY26, due to a modest decline in revenue combined with cost pressure and a sharp normalization in other income.

The half-year numbers show that earnings momentum has softened compared to last year’s stronger base, with the impact visible across both operating and non-operating lines.

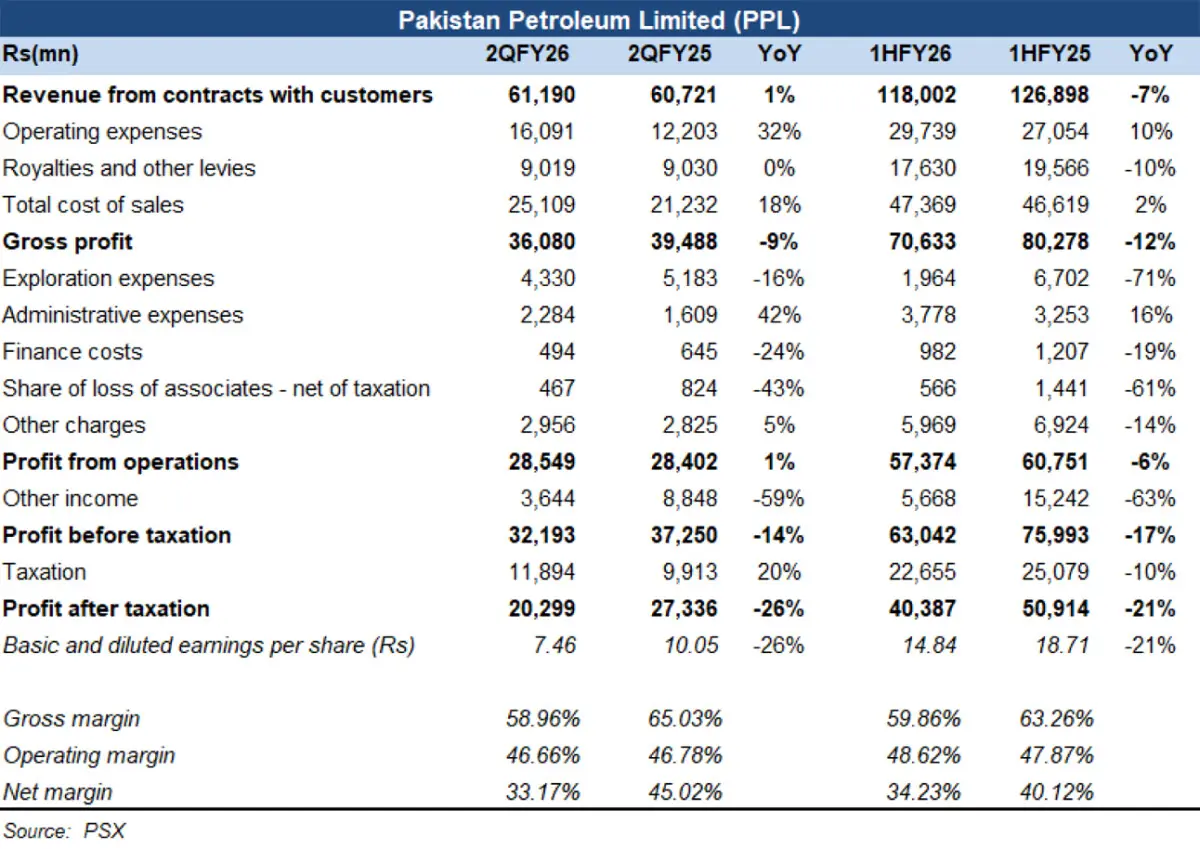

During 1HFY26, PPL’s revenue from contracts with customers were down by 7 percent year-on-year. This contraction in the topline was meaningful because it occurred at a time when the company’s cost base did not ease proportionately.

Royalties and other levies provided some relief, falling 10 percent year-on-year, but operating expenses moved in the opposite direction and rose 10 percent year-on-year.

The combined effect was a weaker gross profit outcome: gross profit declined 12 percent year-on-year, indicating margin compression despite a lower royalty burden.

Exploration expenses dropped sharply to Rs2 billion in 1HFY26 compared to Rs6.7 billion in the same period last year, a 71 percent year-on-year decline that offered a meaningful cushion to operating profitability. However, this was partially offset by higher administrative expenses, which increased 16 percent year-on-year, pointing to rising overheads even as exploration activity slowed.

Finance costs improved modestly, declining 19 percent year-on-year, while other charges also eased 14 percent year-on-year.

Taken together, these movements helped contain the deterioration in core profitability, but they were not sufficient to fully offset the pressure coming from weaker gross profit and the collapse in other income.

The swing factor in the half-year was other income, which fell sharply to Rs5.7 billion, down 63 percent year-on-year from Rs15.2 billion in 1HFY25. The tax line offered limited relief, but the reduction was not enough to prevent a decline in net profitability. Profit after tax closed at around Rs40 billion, down 21 percent year-on-year.

The quarterly pattern reinforces the same story. In 2QFY26 alone, PPL reported profit after tax of Rs20.3 billion, down 26 percent year-on-year, reflecting continued pressure from higher operating expenses and weaker other income, even as the revenue line remained broadly stable year-on-year.

Overall, PPL’s 1HFY26 unconsolidated results highlight a company still generating strong absolute earnings. With exploration spending significantly lower and administrative costs rising, the numbers also raise questions around the sustainability of future reserve replacement and production stability, even though the P&L alone does not provide a full operational picture.

What is clear from the unconsolidated income statement is that earnings resilience in the period was supported more by lower exploration charges than by revenue growth, while the year-on-year decline was ultimately driven by margin compression and a sharp drop in other income — a reminder that, for PPL, non-operating income can materially influence reported profitability in any given period.

Overall, PPL posted a soft 1HFY26, with PAT down 21 percent year-on-year, mainly due to higher OPEX and sharply lower other income, despite stable operations.

PPL maintained payouts, declaring Rs4.0/share interim dividend for 1HFY26 (Rs2.0/share in 2QFY26). Going forward, earnings in 2HFY26 will largely depend on oil/gas prices, OPEX normalization, and whether other income remains subdued amid lower interest rates.

Comments