Pioneer Cement Limited (PSX: PIOC) was incorporated as a public company limited by shares in Pakistan in 1986. The company is engaged in the production, marketing and sale of cement and clinker.

PIOC is geographically located in Punjab to cater the needs of central and South Punjab, however, the company has extended its services to other parts of the country through distributors, retailers and dealers. The company has also tapped the foreign market specially India and Afghanistan.

Pattern of Shareholding

As of June 30, 2025, PIOC has a total of 227.149 million shares outstanding which are held by 7371 shareholders. Associated companies, undertakings and related parties have the majority stake of 54.53 percent in the company followed by joint stock companies holding 20.69 percent shares. Local general public accounts for 8.02 percent shares of the company while Modarabas & Mutual funds hold 5.67 percent shares.

Around 4.68 percent of the company’s shares are held by foreign companies, 3.28 percent by Banks, DFIs and NBFIs and 2.06 percent by foreign general public. The remaining shareholding is distributed among other categories of shareholders.

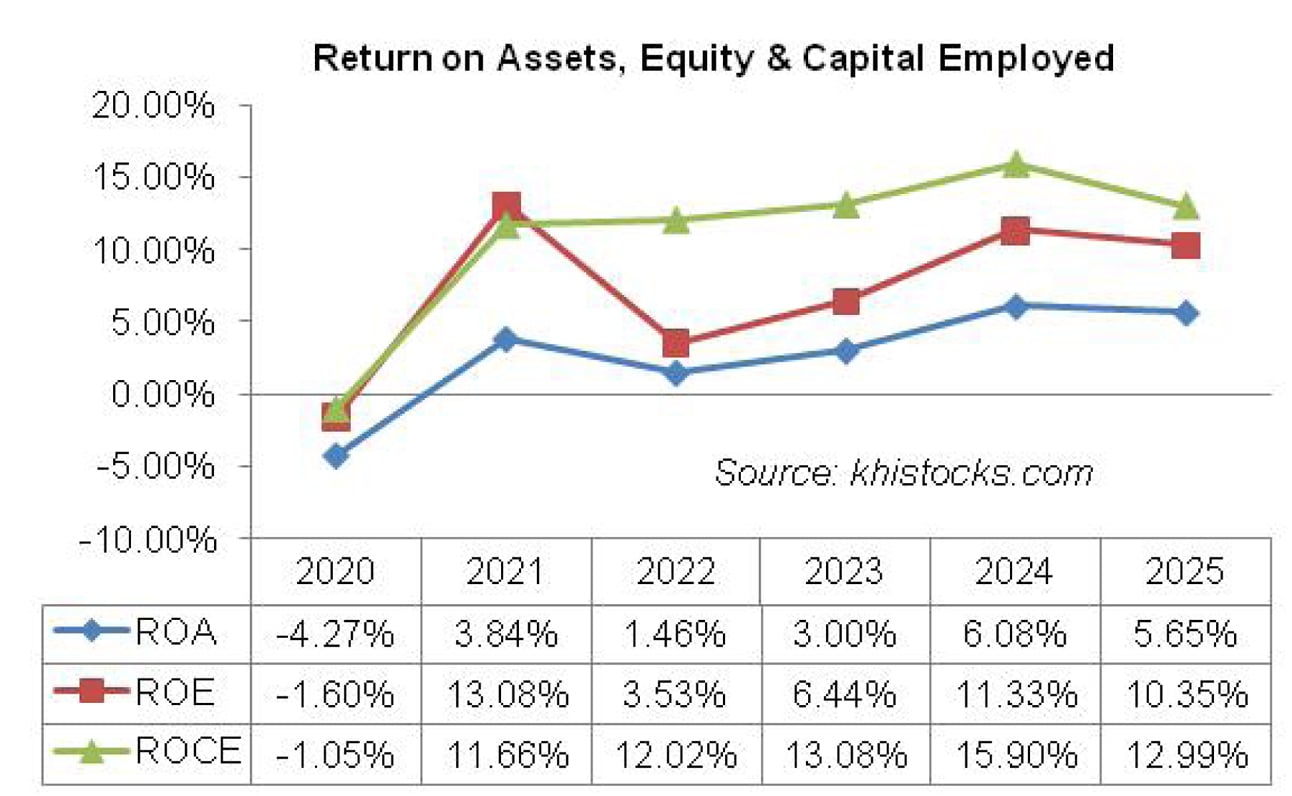

Historical Performance (2021-2025)

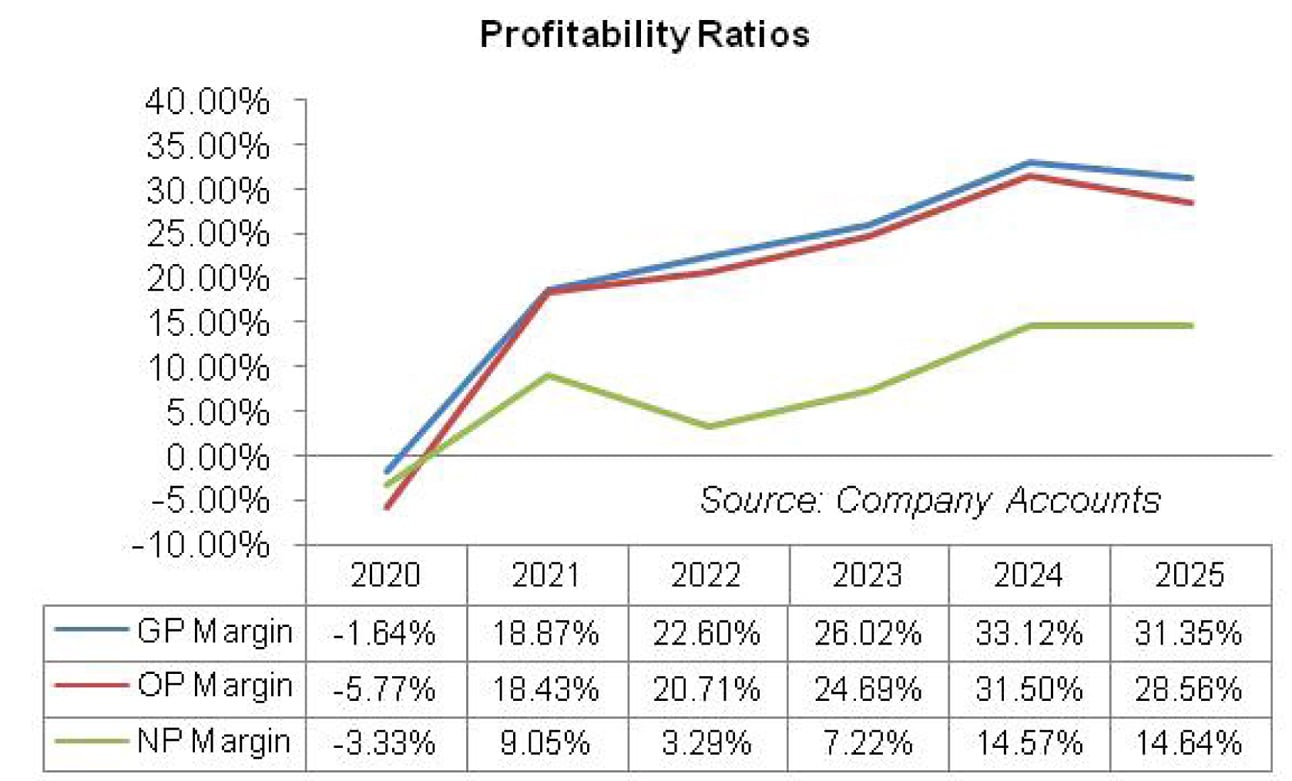

PIOC’s net sales rode an upward trajectory until 2023 followed by a decline recorded in 2024 and 2025. Its bottomline which registered net loss in 2020, posted net profit in 2021. This was followed by a plunge in net profit in 2022. In the following two years, net profit staggeringly enhanced followed by a downturn in 2025. The company’s margins show an ascending pattern until 2024 except for a downtick in net margin in 2022. In 2025, gross and operating margins fell while net margin slightly ticked up. It is to be noted that the company has made no export sales since 2022. The detailed performance review of the period under consideration is given below.

In 2021, PIOC’s net sales mounted by 247 percent to clock in at Rs.21,817.61 million. This came on the back of 94.87 percent spike in sales volume which clocked in at 3.38 million tons. Out of the total sales volume recorded by the company in 2021, export sales stood at 13000 tons versus 12000 tons in the previous year.

Increased demand due to stimulus packages introduced by the government post COVID-19 led to higher capacity utilization of 65.61 percent recorded in 2021 versus capacity utilization of 50.42 percent recorded in 2020.

Demand recovery also led to higher salesprice of cement. This coupled with cost optimization due to higher capacity utilization and efficient operation of new production line enabled PIOC to record gross profit of Rs.4117.95 million in 2021 versus gross loss of Rs.103.09 million posted in 2020.

GP margin was recorded at 18.87 percent in 2020. Despite enhancement in sales volume, distribution expense fell by 53 percent in 2021 as nominal sales were made on delivered basis which led to reduced freight & handling charges. Administrative expense surged by 18.22 percent in 2021 due to higher payroll expense as the company expanded its workforce from 1080 employees in 2020 to 1105 employees in 2021 to meet higher demand.

Provisioning done for WWF and WPPF resulted in other expense of Rs.152.77 million in 2021 versus other expense of Rs.1.03 million recorded in the previous year. Other income dipped by 35.86 percent in 2021 due to lesser dividend income, thinner profit on bank deposits due to monetary easing and no liabilities written back during the year. Re-measurement gain worth Rs.236.60 million on investments held at fair value also buttressed the financial results of the company in 2021.

PIOC recorded a phenomenal operating profit of Rs.4020.72 million in 2021 with OP margin of 18.43 percent. This was against the operating loss of Rs.362.63 million registered in the previous year.

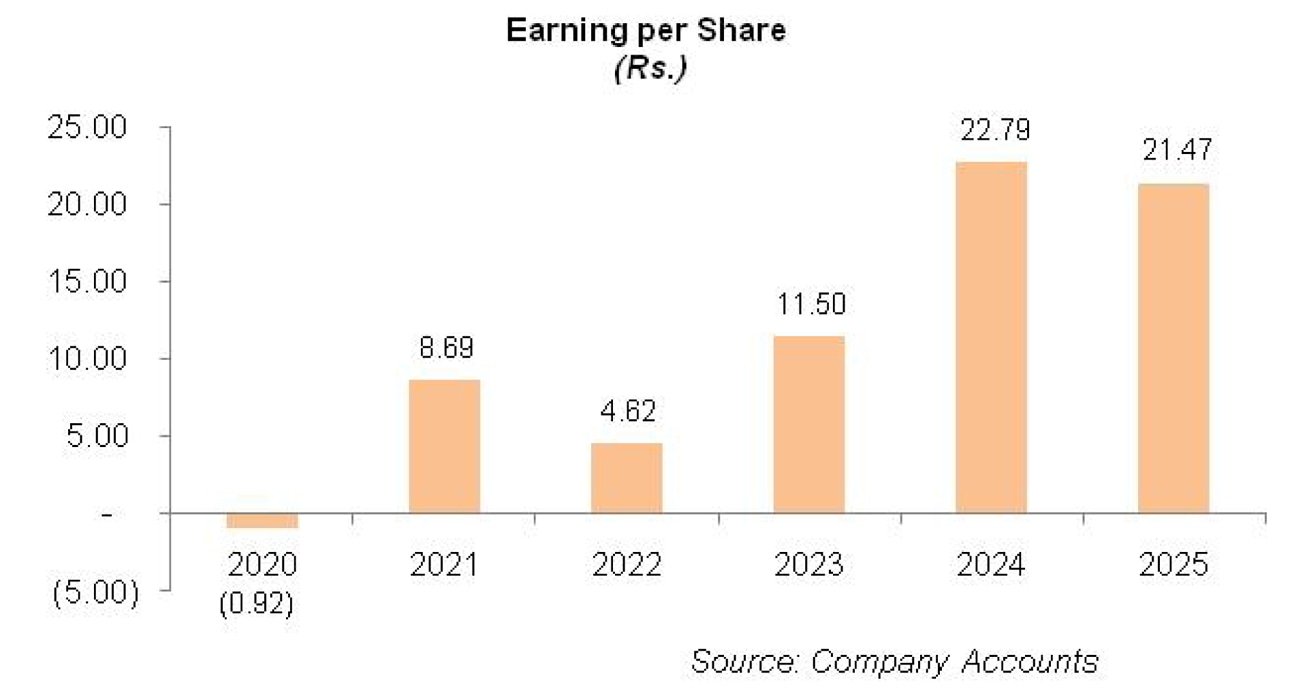

Finance cost escalated by 362.80 percent in 2021 despite monetary easing. This was due to increased borrowings to finance the establishment of new cement plant and waste heat recovery plant. PIOC posted net profit of Rs.1974.446 million in 2021 versus net loss of Rs.209.622 million recorded in 2020. EPS stood at Rs.8.69 in 2021 versus loss per share of Rs.0.92 registered in the previous year. NP margin clocked in at 9 percent in 2021.

In 2022, PIOC posted 46.12 percent improvement in its net sales which clocked in at Rs.31,879.21 million. During the year,the volumetric dispatches of Pakistan cement industry dropped from 57.43 million tons to 52.89 million tons. As against the industry-wide drop in sales volume, Pioneer Cement recorded volumetric sales growth of only 0.23 percent to clock in at 3.388 million tons.

The growth came on the heels of local sales as the company made no foreign sales during the year. Topline growth is largely attributable to the cost push increase in sale price in the local market. During 2022, the company operated on 64.93 percent of its capacity producing 6266 tons of clinker and cement out of which it could only sell 46 percent.

The decline in demand across the industry is attributable to myriad factors including ever increasing fuel prices, overall economic downturn, and multiple hikes in the discount rate as well as flood impact in the southern region of the country.

Moreover, there is a fall in construction activity due to global increase in prices of steel and other raw materials. Low allocation of PSDP also posed challenges for fuel intensive industries like Cement. Cost of sales also grew by around 39.42 percent year-on-year in 2022 primarily due to rise in fuel and power cost (from Rs. 3565 per ton in 2021 to Rs.5401 per ton in 2022) and packing material cost (from Rs.564 per ton in 2021 to Rs.646 per ton in 2022).The increase in cost of production is attributable to Pak Rupee Depreciation coupled with the rise the coal and paper prices both domestically and internationally.

The effect could be much bigger, but PIOC has mitigated the further adverse effect by switching to cost effective coal from local and Afghan market. To minimize the shock of rising power cost owing to an increase in electricity tariffs, the company largely relied upon captive power plant which used waste heat recovery and coal fire to generate electricity. This has enabled PIOC to attain a year-on-year growth of 74.92 percent in its gross profit in 2022. GP margin also strengthened to 22.60 percent in 2022.

Distribution and administrative expenses remained in check, posting a year-on-year rise of 0.7 percent and 4.6 percent respectively. Other expense spiked by 104.76 percent in 2022 due to increased provisioning done for WWF and WPPF. Other income couldn’t contribute much to the bottom line in 2022 and dropped year-on-year by 39 percent due to lesser scrap sales.

The company also recorded loss worth Rs.76.11 million on the re-measurement of assets held at fair value. PIOC posted 64.17 percent stronger operating profit in 2022 with OP margin rising up to 20.71 percent. Finance cost gave no breather and soared by 46.13 percent in 2022 on account of increase in the policy rate coupled with the increase in external borrowings to finance 24MW coal power plant.

The final hit on the bottom line was made by hefty taxation charge owing to the imposition of super tax in 2022. This coupled with the consequent non-cash adjustments squeezed the profit after tax by 46.81 percent year-on-year to clock in at Rs.1050.27 million in 2022. EPS was recorded at Rs.4.62 while NP margin fell to 3.29 percent in 2022.

In 2023, PIOC’s net sales ticked up by 13.44 percent to clock in at Rs.36,165.27 million. This was despite the fact that sales volume dipped by 20.19 percent to clock in at 2.704 million tons in 2023.

Capacity utilization deteriorated to 52.78 percent in 2023. Increase in macroeconomic issues including heightened inflation, discount rate, energy tariff, commodity prices coupled with Pak Rupee depreciation took a heavy toll on the purchasing power of the potential investors in 2023. Moreover, political uncertainty also kept the investors at bay. While fuel and power cost surged to Rs.7361 per ton and packing material cost escalated to Rs.782 per ton, the company was able to drive 30.63 percent growth in its gross profit on the back of improved prices of cement as well as reliance on captive power plants including waste heat recovery and coal fired plants.

GP margin jumped up to 26 percent in 2023. Distribution expense grew by 18.67 percent in 2023 due to increased salaries of sales force. Administrative expense mounted by 25.68 percent in 2023 due to higher payroll expense on account of inflationary pressure as well as workforce enhancement to 1152 employees in 2023 from 1098 employees in the previous year.

Reversal of the provisioning done for WPPF resulted in 57.80 percent decline in other expense in 2023. Other income multiplied by 14.47 percent in 2023 due to greater scrap sales, higher rental income from investment property and gain recognized on the sale of fixed assets. PIOC also recorded allowance worth Rs.77.63 million for ECL.

Operating profit developed by 35.28 percent in 2023 with OP margin climbing up to 24.69 percent. Higher discount rate was the reason for 20.38 percent spike in finance cost in 2023 while overall debt burden was reduced during the year. PIOC posted 148.61 percent higher net profit to the tune of Rs.2611.106 million in 2023. This translated into EPS of Rs.11.50 and NP margin of 7.22 percent in 2023.

In 2024, PIOC recorded 1.79 percent downtick in its net sale which clocked in at Rs.35,519.27 million. This came on the back of 12.65 percent drop in sales volume of the company which clocked in at 2.362 million tons. However, cost push increase in sales price greatly diluted the effect of thinner sales volume.

Capacity utilization was recorded at 44.57 percent in 2024. Cost of sales dipped by 11.21 percent in 2024 due to curtailed operations and also because the company relied on captive power plants and sourced its coal locally and from Afghanistan. This enabled the company to post 25 percent higher gross profit in 2024 with GP margin clocking in at 33.12 percent.

Higher payroll expense, repair & maintenance charges as well as depreciation expense were the core reasons behind elevated operating expense recorded in 2024. PIOC streamlined its workforce from 1152 employees in 2023 to 1095 employees in 2024. 262.59 percent higher other expense incurred in 2024 was the result of increased provisioning done for WWF and WPPF.

However, it was greatly offset by 838.24 percent higher other income recorded in 2024 on the back of gain realized on the sale of short-term investments, greater scrap sales, gain on disposal of fixed assets as well as rental income. Allowance for ECL diminished by 38.33 percent in 2024. PIOC posted 25.31 percent higher operating profit in 2024 with OP margin clocking in at 31.50 percent.

Despite monetary tightening, the company was able to cut down its finance cost by 12.25 percent in 2024 due to settlement of outstanding liabilities. Gearing ratio fell from 29.72 percent in 2023 to 18.09 percent in 2024. Net profit was recorded at Rs.5176.166 million in 2024, up 98.24 percent year-on-year. This translated into EPS of Rs.22.79 and NP margin of 14.57 percent.

For the second year in a row, PIOC posted a plunge in its net sales to the tune of 6.22 percent in 2025. Net sales clocked in at Rs.33,308.61 million in 2025. This came on the back of 12.28 percent dip in sales volume, which was recorded at 2.072 million tons. Lackluster private sector demand, slow PSDP disbursement, elevated energy tariff and hike in federal excise duty on cement to Rs.4000 per ton were the main reasons behind demand destruction. Capacity utilization fell to its lowest level of 40.18 percent in 2025.

While the company took effective measures to reduce its cost which included sourcing of coal locally and from Afghanistan and reliance on captive power plant, the increase in provincial government royalty from Rs.250 per ton of mineral extracted to 6 percent of ex-factory cement price wreaked havoc on the overall cost structure of the company and resulted in 11.22 percent deterioration in its gross profit in 2025. GP margin fell to 31.35 percent in 2025. Lesser salaries of sales force translated into 13.87 percent decline in distribution expense in 2025.

Conversely, administrative expense surged by 47.93 percent in 2025 due to higher payroll expense, repair & maintenance charges, legal & professional charges as well as depreciation expense incurred during the year.

The company expanded its workforce to 1105 employees in 2025. Other expense escalated by 36 percent in 2025. This was the result of business development and technical fee pertaining to due diligence of a prospective project which was ultimately not pursued. Other income deteriorated by 41.77 percent in 2025 due to high-base effect as the company realized gain on the sale of short-term investments and fixed assets in the previous year. Re-measurement gain on assets held at fair value progressed from Rs.0.41 million in 2024 to Rs.64.61 million in 2025.

The company also booked reversal of allowance booked for ECL in 2025. Despite all these measures, operating profit dropped by 14.98 percent in 2025 with OP margin clocking in at 28.56 percent. Finance cost fell by 49.81 percent in 2025 due to monetary easing and early debt settlement. Gearing ratio was recorded at 15 percent in 2025. PIOC recorded net profit of Rs.4876.097 million in 2025, down 5.80 percent year-on-year. This translated into EPS of Rs.21.47 and NP margin of 14.64 percent in 2025.

Recent Performance (1QFY26)

Following a dip in 2025, PIOC recorded 6.67 percent increase in its net sales which clocked in at Rs.8416.62 million in 1QFY26. This came on the back of 18.73 percent higher sales volume which was partially offset by lower selling prices. Rising overhead cost due to low-capacity utilization and higher royalty fee on minerals pushed cost of sales up by 7.65 percent in 1QFY26. Gross profit ticked up by 4.41 percent in 1QFY26, however GP margin fell to 29.78 percent from GP margin of 30.43 percent recorded in 1QFY25.

Distribution and administrative expense were largely stable during the period. Increased profit-related provisioning appears to be the cause of higher other expense in 1QFY26. Other expense was greatly offset by 73.97 percent higher other income recorded during the period, which might be the consequence of higher scrap sales and rental income. Operating profit ticked up by 6.13 percent in 1QFY26 with OP margin recorded at 27.36 percent marginally lower than the OP margin of 27.50 percent recorded in 1QFY25.

Reduction in policy rate coupled with early settlement of outstanding debt resulted in 56.55 percent thinner finance cost in 1QFY26. Net profit picked up by 24.56 percent to clock in at Rs.1274.108 million in 1QFY26. This translated into EPS of Rs.5.61 in 1QFY26 versus EPS of Rs.4.50 recorded in 1QFY25. NP margin progressed from 12.96 percent in 1QFY25 to 15.14 percent in 1QFY26.

Future Outlook

Gradual recovery in private sector demand on the back of rebound in macroeconomic indicators bodes well for the cement industry. The rehabilitation of flood-stricken areas will provide further impetus to cement demand. However, the industry is far from realizing its full potential which is making it difficult to absorb fixed overheads efficiently in the face of high input cost

particularly royalty on minerals and federal excise duty. Heightened tension with Afghanistan has also blocked the supply of coal which is another factor contribution to hike in cost.

Recently, Maple Leaf Cement Factory Limited (MLCF) has announced an intention to acquire 58.03 percent shares and control of PIOC. This will reportedly increase MLCF market share from 12 percent to 19 percent.

Comments

Comments are closed for this article.