Hala Enterprises Limited (PSX: HAEL) was incorporated in Pakistan as a private limited company and was subsequently converted into a public limited company. The company began its operations in 1974. The principal activity of the company is the manufacturing and sale of terry towels, kitchen towels and terry cloth.

Pattern of Shareholding

As of June 30, 2025, HAEL has a total of 12.996 million shares outstanding which are held by 992 shareholders.

Directors, CEO, their spouse and minor children have the majority stake of 53.28 percent in the company, followed by its parent company, M/S Teejay Corporation Limited holding 30.31 percent shares.

Local general public accounts for 14.58 percent shares of HAEL while joint stock companies hold 1.32 percent shares. The remaining ownership is distributed among other categories of shareholders.

Historical Performance (2019-25)

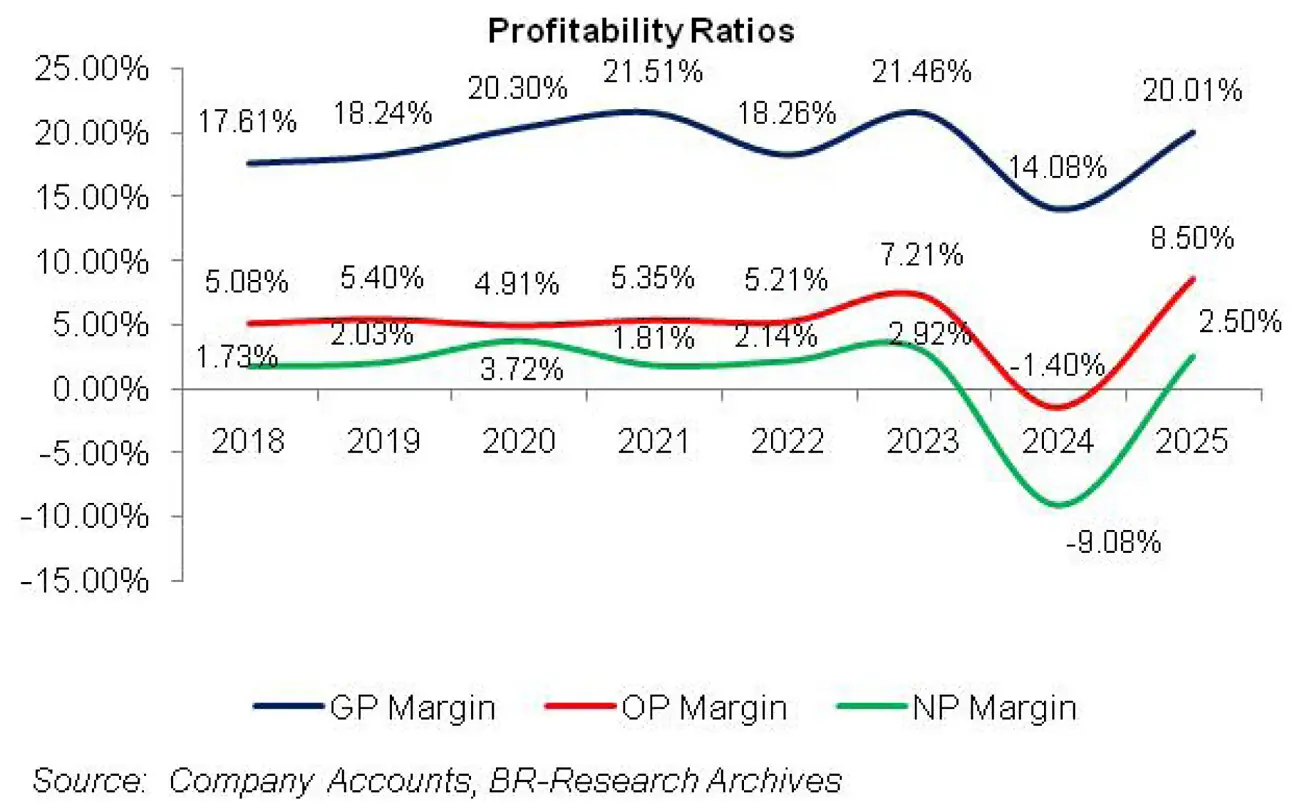

Barring year-on-year decline in 2020 and 2024, HAEL’s topline posted decent growth over the period under consideration. On the contrary, its bottomline plunged in 2021 and 2024 with operating and net losses recorded in the latter year. HAEL’s margins depict a fluctuating pattern.

Gross margin, which was on the rise since 2019 tumbled in 2022. This was followed by a recovery in 2023. Operating margin remained range-bound until 2022, however, reached its optimum level in 2023.

Conversely, net margin followed an upward trajectory until 2020, fell in 2021 and then took the route to recovery in the next two years. In 2024, all the margins drastically fell followed by a phenomenal recovery recorded in 2025 (see the graph of profitability ratios). The detailed performance review of the period under consideration is given below.

In 2019, HAEL’s net sales grew by 22.80 percent year-on-year to clock in at Rs.385.707 million. This was on the back of diversified product portfolio of the company as well as the sale of specialized towels.

In 2019, HAEL made 98.62 percent of its revenue from export market. Hence, Pak Rupee depreciation in 2019 proved to be a good omen for the company and buttressed its gross margin which clocked in at 18.24 percent in 2019 versus GP margin of 17.61 percent recorded in 2018. In absolute terms, gross profit picked up by 27.20 percent in 2019.

HAEL’s operating expense escalated by 32.80 percent year-on-year in 2019 which was mainly on account of elevated sales commission, freight, octroi, cartage and clearing charges.

Communication, utility and vehicle running expense also significantly surged during the year. Considerable boost in exchange income buttressed the company’s other income which mounted by 106.55 percent in 2019. Operating profit picked up by 30.39 percent year-on-year in 2019 with OP margin rising from 5.10 percent in 2018 to 5.40 percent in 2019.

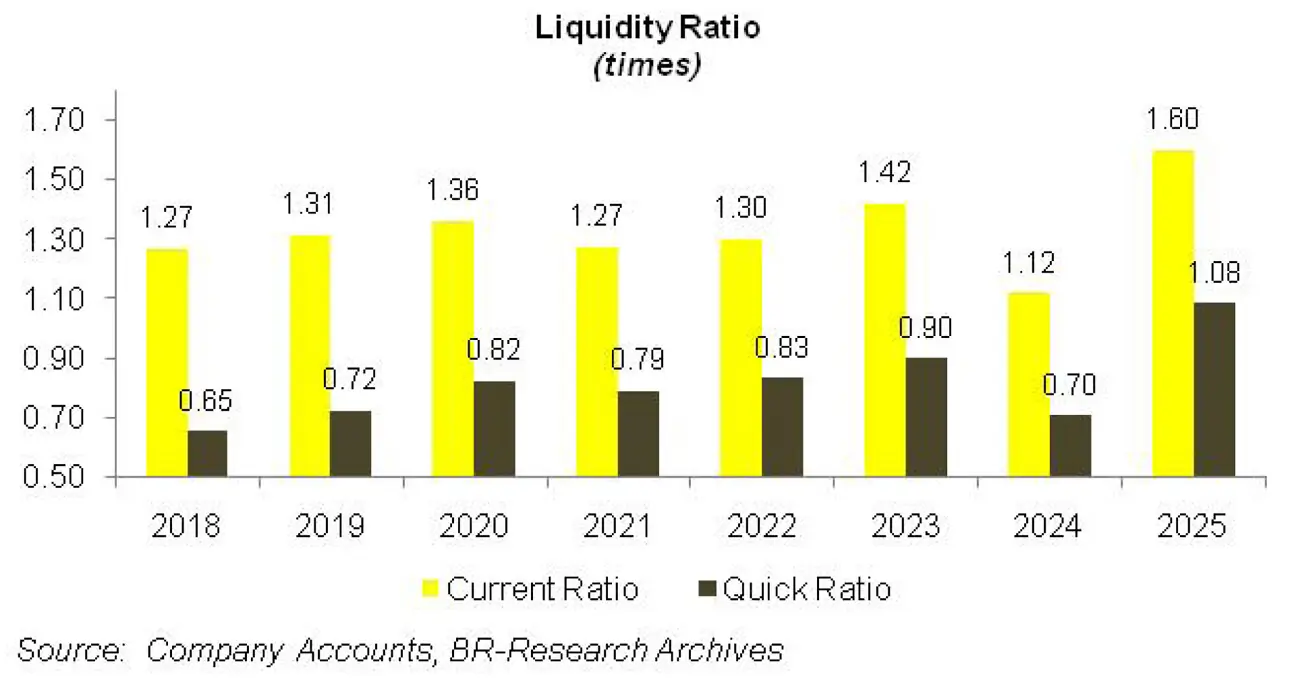

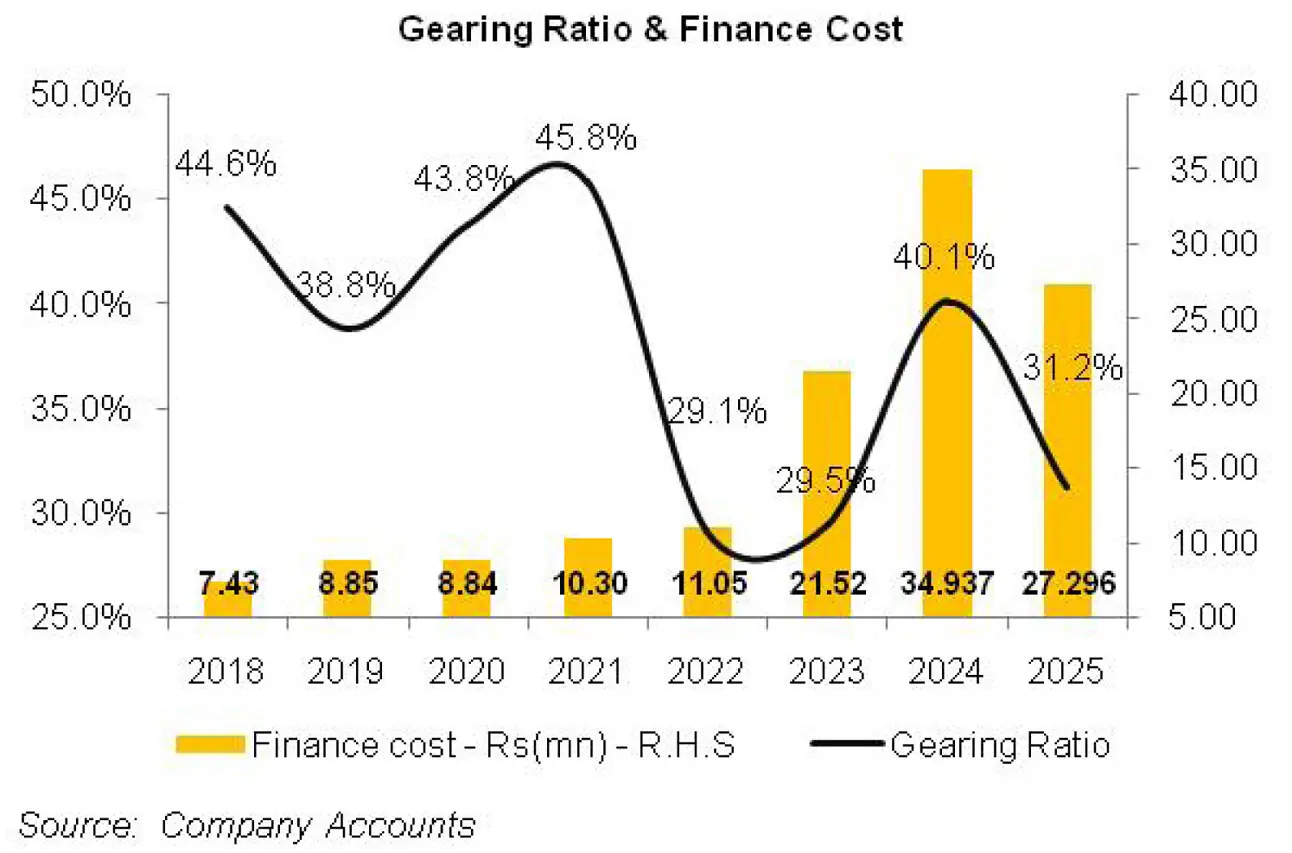

Finance cost surged by 19.23 percent year-on-year in 2019 on account of higher discount rate as well as increased borrowings. The drop in HAEL’s gearing ratio from 44.60 percent in 2018 to 38.80 percent in 2019 was due to the issuance of shares during the year which took the authorized share capital from Rs.80 million in 2018 to Rs.160 million in 2019.

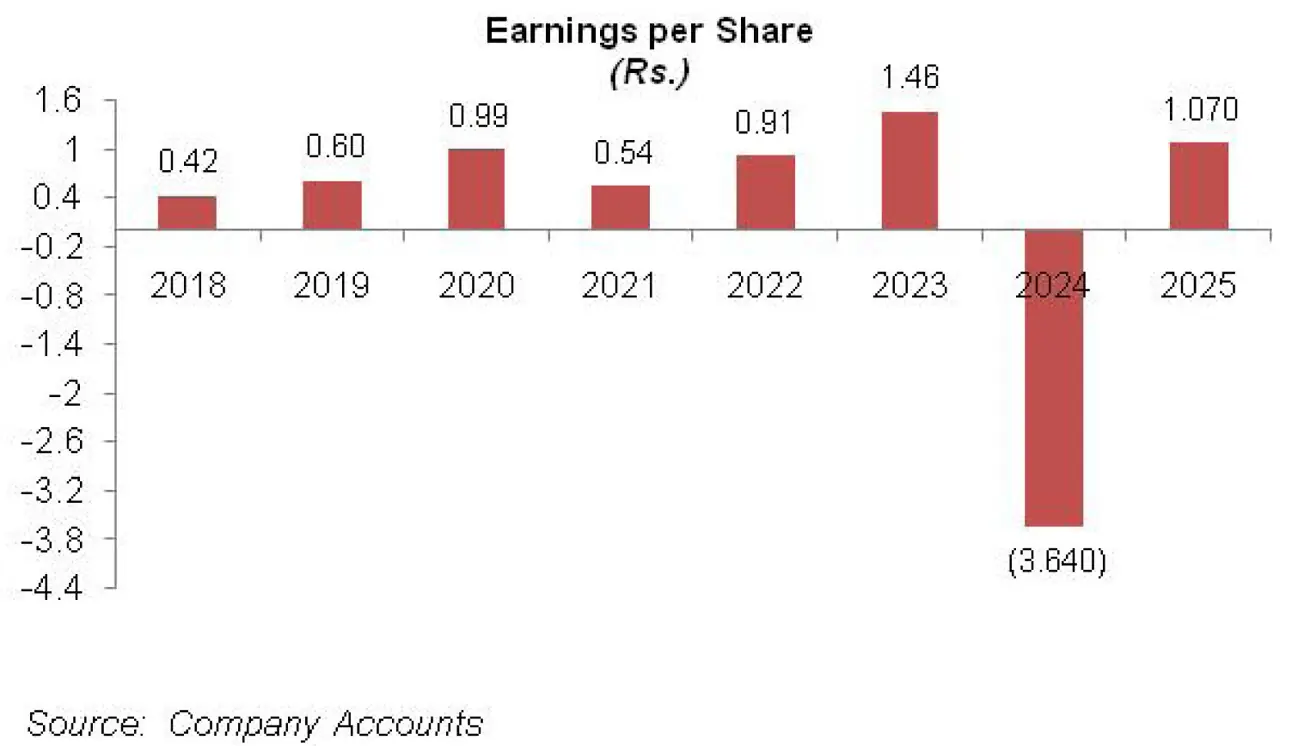

Net income rose by 44.58 percent year-on-year in 2019 to clock in at Rs.7.839 million. This translated into EPS of Rs.0.60 in 2019, up from EPS of Rs.0.42 posted in 2018. NP margin also grew from 1.73 percent in 2018 to 2.032 percent in 2019.

In 2020, the outbreak of COVID-19 and the associated lockdowns and restrictions on the movement of people and goods took its toll on the net sales of HAEL which plunged by 10.19 percent year-on-year to clock in at Rs.346.417 million.

As shipments were restricted, the company tapered its operations in 2020. This resulted in production of 365,065 kilograms in 2020, down 10 percent year-on-year. As institutional sales suffered due to shut-down of hospitality industry during the lockdown period, the company focused on retail sector and tapped the high value-added market. As a result, its gross profit remained static while GP margin jumped up to 20.30 percent in 2020.

HAEL was able to cut down its operating expense by 3.12 percent year-on-year in 2020 on account of lower sales commission, air freight charges as well as octroi, cartage and clearing charges. Thinner lease rentals, dividend income and interest charged to related parties squeezed other income by 58.27 percent year-on-year in 2020.

As a consequence, operating profit slid by 18.36 percent year-on-year in 2020 with OP margin slipping to 4.91 percent. HAEL maintained its finance cost at Rs.8.8 million in 2020 despite increased borrowings. This was on account of lower bank commission, lesser interest charged by related parties as well no interest payments due to Comfort Textile (Private) Limited. HAEL’s gearing ratio hiked to 43.80 percent in 2020.

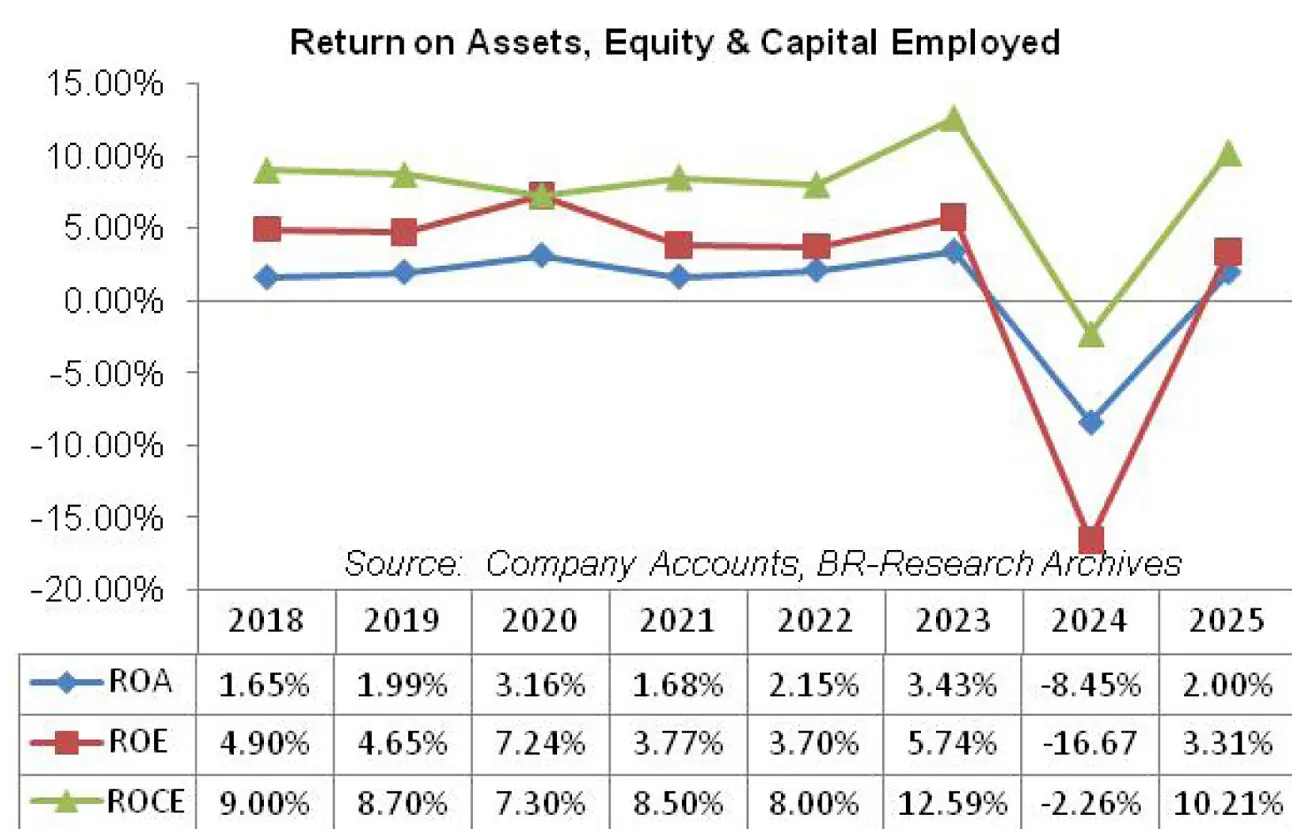

The company’s profit after tax in 2020 was 44 percent lower than the previous year, however, the gain on disposal of land held for sales drove the net profit of the year to Rs.12.885 million, up 64.37 percent year-on-year. This translated into EPS of Rs.0.99 and NP margin of 3.72 percent in 2020.

HAEL’s topline showed signs of recovery as it built up by 12.53 percent to clock in at Rs. 389.822 million in 2021. Owing to demand recovery and resumption of shipments which were stuck due to COVID-19, HAEL increased its production by 7 percent year-on-year to clock in at 390,286 kilograms in 2020.

Cost of sales spiked by 10.83 percent in 2021 on account of higher prices of cotton in the international market and Pak Rupee depreciation. However, as the company derives more than 98 percent of its revenue from export market, higher cost was largely offset by lofty translation gain. This pushed the gross profit up by 19.21 percent year-on-year in 2021 with GP margin rising to its optimum level of 21.51 percent.

HAEL’s ever-increasing focus on higher value-added products was also one of the reasons behind robust GP margin recorded in 2021.

Operating expense elevated by 11.28 percent year-on-year in 2021 due to higher selling and distribution charges on account of improved sales volume. Operating profit enlarged by 22.68 percent year-on-year in 2021 with OP margin moving up to 5.35 percent. Finance cost escalated by 16.53 percent year-on-year in 2021 despite monetary easing due to increased short-term and long-term borrowings and higher bank commission.

HAEL’s gearing ratio surged to 45.8 percent in 2021. Net profit slumped by 45.36 percent in 2021 to clock in at Rs.7.04 million with EPS of Rs.0.54 and NP margin of 1.81 percent.

Among all the years under consideration, HAEL boasted the highest topline growth of 41 percent in 2022. Net sales were recorded at Rs. 549.65 million in 2022. The company produced 445,615 kilograms of product, up 14 percent year-on-year in 2022, in order to meet rising demand.

The growth in net sales was also the result of upward price revision to account for high inflation, increased commodity prices, Pak Rupee depreciation and a sharp spike in energy tariff during the year.

Due to the aforementioned factors, HAEL’s cost of sales rose by 46.83 percent year-on-year in 2022. While gross profit picked up by 19.72 percent year-on-year in 2022, GP margin slipped to 18.26 percent. Operating expense mounted by 23.36 percent year-on-year in 2022 due to exorbitant sea freight charges.

The company also realized an exchange income of Rs.2.690 million in 2022 unlike exchange loss of Rs.2.56 million realized in 2021. As a consequence, operating profit in 2022 turned out to be 37.42 percent bigger when compared to that of 2021. OP margin slightly tumbled to 5.21 percent in 2022.

Finance cost ticked up marginally by 7.28 percent year-on-year in 2022 despite multiple rounds of monetary tightening undertaken by the central bank during the year. This was on account of a plunge in external borrowings which squeezed HAEL’s gearing ratio to 29.1 percent in 2022. Net profit jumped up by 67.38 percent year-on-year in 2022 to clock in at Rs.11.78 million in 2022 with EPS of Rs.0.91 and NP margin of 2.14 percent.

HAEL’s topline improved by 17.93 percent to clock in at Rs.648.204 million in 2023. Diminished demand in the global market due to recessionary pressure and stiff competition from regional counterparts pushed the company to reduce its production to 381,154 kilograms in 2023, down 14 percent year-on-year. This shows that change in the pricing strategy was the major contributor of enhanced net sales in 2023.

Cost of sales hiked by 13.31 percent year-on-year in 2023, yet HAEL was able to drive its gross profit up by 38.60 percent in 2023, resulting in a GP margin of 21.46 percent. Operating expense grew by 18.34 percent year-on-year in 2023 on account of higher commission on sales, freight and clearing charges.

HAEL incurred an exchange loss of Rs.3.565 million in 2023 which drove up its other expense by 219.40 percent. Nevertheless, the company was able to post 63.13 percent improvement in its operating profit in 2023 with OP margin jumping up to 7.212 percent.

Finance cost enlarged by 94.77 percent year-on-year in 2023 despite a drop in borrowings. This was the consequence of high discount rate during the year. HAEL’s gearing ratio ticked up to 29.5 percent in 2023. Net profit rose by 60.66 percent year-on-year in 2023 to clock in at Rs. 18.93 million with EPS of Rs.1.46 and NP margin of 2.92 percent.

In 2024, HAEL recorded 19.53 percent year-on-year decline in its topline which clocked in at Rs.521.606 million. This was on account of subdued demand of home textile products in the international market due to global recessionary pressure and Suez Canal crisis which delayed the transit time to Europe besides driving up the freight charges by manifold.

Moreover, Pakistan was also at competitive disadvantage as it had the highest energy cost in the South and South East region. Cost of sales tamed by a much lesser magnitude of 11.96 percent in 2024 due to high inflation, towering energy cost and falling indigenous cotton crop output leading to the import of expensive cotton. This squeezed HAEL’s gross profit by 47.23 percent in 2024 with GP margin falling down to its lowest level of 14.10 percent.

While the impediments at Suez Canal drove the freight charges up by 3 to 4 times during the year, reduced sales volume resulted in 10.28 percent year-on-year plunge in operating expense in 2024.

HAEL recorded operating loss of Rs.7.296 million in 2024. Finance cost surged by 62.33 percent in 2024 due to elevated discount rate and increased short-term borrowings to sustain cash-flow constraints owing to additional freight cost, heightened raw material charges, delayed government refunds and high energy cost.

Gearing ratio mounted to 40.1 percent in 2024. The company recorded net loss of Rs.47.356 million in 2024 with loss per share of Rs.3.64.

In 2025, HAEL’s net sales ticked up by 6.13 percent to clock in at Rs.553.56 million. While the first three quarters of the year were characterized by softer sales, the last quarter proved to be a game-changer for the company, leading to a robust close to the year.

Not only did the sales volume enhanced during the last quarter of the year, the company also undertook measures over the year to achieve operational efficiency. These included the commissioning of solar power plant, conversion of its thermal energy system to bio-fuel to avoid gas supply disruptions and price volatility and also commenced the expansion of its weaving unit through self-financing. This resulted in 50.85 percent improvement in HAEL’s gross profit in 2025 with GP margin jumping up to 20 percent.

Operating expense tumbled by 14.74 percent in 2025 on the back of lower sea freight, octroi and cartage charges as well as thinner commission on sales.

Drastic decline in payroll expense also squeezed the operating expense in 2025. Other expense dropped by 58.27 percent in 2025 as no exchange loss was realized during the year. Other expense was completely offset by 76.83 percent higher other income recorded in 2025 on the back of exchange gain.

HAEL recorded the highest ever operating profit of Rs.47.076 million in 2025 with OP margin attaining its optimum level of 8.50 percent. Finance cost slumped by 21.87 percent in 2025 due to monetary easing. Gearing ratio was recorded at 31.2 percent in 2025 which was mainly on account of greater equity as the Director and CEO of the company granted an interest free loan of Rs.120 million to the company in 2025.

The loan is payable at the discretion of the company and has been classified as equity. Net profit clocked in at Rs.13.858 million in 2025 with EPS of Rs.1.07 and NP margin of 2.50 percent.

Recent Performance (1QFY26)

During the first quarter of the ongoing fiscal year, HAEL recorded 92.96 percent enhancement in its net sales which clocked in at Rs.169.23 million. During the period under consideration, the company shifted its focus from commodity business to high value-added products which not only resulted in increased demand but also were able to absorb the cost more efficiently.

Gross profit strengthened by 79.82 percent in 1QFY26, however, with the stability of Pak Rupee, GP margin inched down from 19.62 percent in 1QFY25 to 18.29 percent in 1QFY26. Steady fuel prices resulted in 24.94 percent dip in selling expense in 1QFY26.

Conversely, administrative expense enlarged by 24.73 percent during the period certainly due to higher payroll expense which might be due to employee induction as the company is planning to enhance its capacity by operationalizing its air jet looms imported from China before the end of the calendar year.

HAEL posted operating profit of Rs.13.32 million in 1QFY26 as against operating loss of Rs.0.448 million recorded in 1QFY25. OP margin stood at 7.87 percent in 1QFY26. Finance cost nosedived by 15.46 percent in 1QFY26 due to monetary easing as well as lesser short-term borrowings.

On the contrary, interest free loan from directors increased during the period to clock in at Rs.188 million as of September 30, 2025 versus Rs.120 million as of June 30, 2025. The company recorded net profit of Rs.3.173 million in 1QFY26 versus net loss of Rs.10.828 recorded in 1QFY25. EPS stood at Rs.0.24 in 1QFY26 versus loss per share of Rs.0.83 posted during the same period last year. NP margin was witnessed at 1.875 percent in 1QFY26.

Future Outlook

HAEL’s enhanced focus on high-margin products will not only improve its profitability but will also pave way for its entry into new export markets.

Besides, the company is also religiously working to control its cost by installing solar power, using bio-gas instead of natural gas and expanding its weaving unit. These measures will enable HAEL to close FY26 on a robust note.

Comments

Comments are closed for this article.