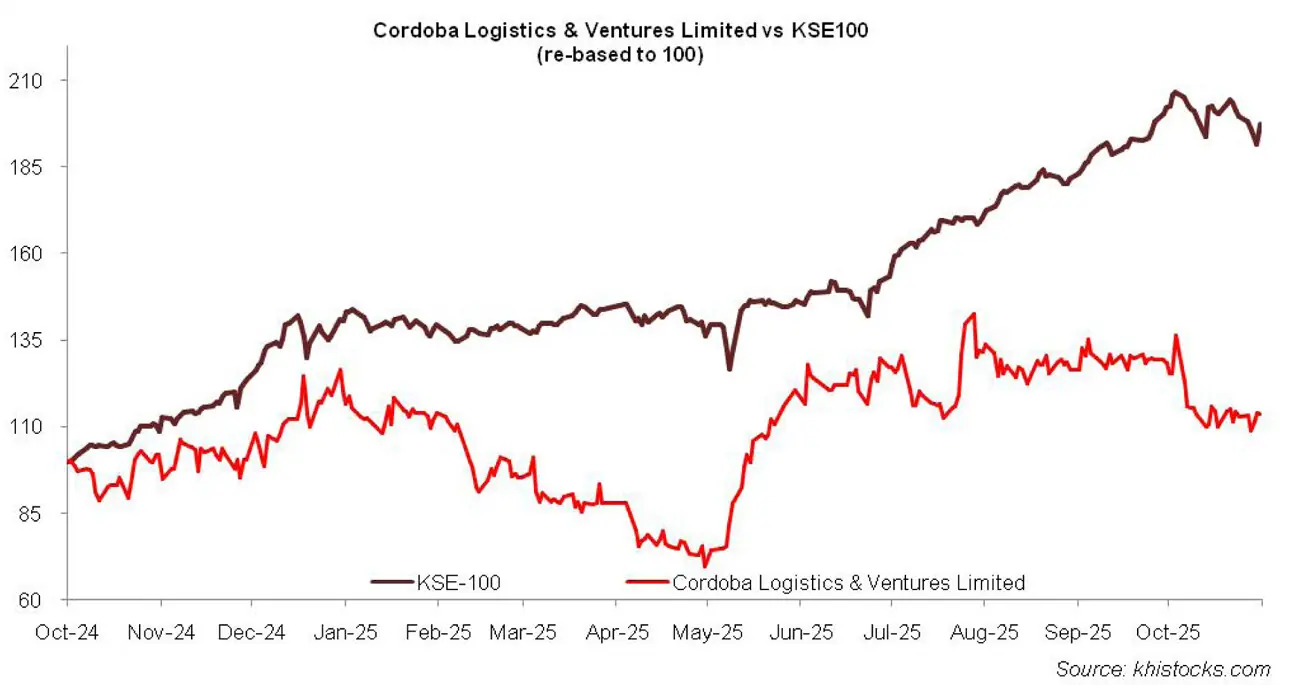

Cordoba Logistics & Ventures Limited (PS: CLVL) was incorporated in Pakistan as a public limited company n 1986. It was previously known as Mian Textile Industries Limited. The company changed its business from Textile to logistics and other ventures in 2021 after the acquisition of 70 percent of the company’s paid-up capital.

Pattern of Shareholding

As of June 30, 2025, CLVL has a total of 72.105 million shares outstanding which were held by 1669 shareholders.

Directors, CEO, Sponsors, spouses and relatives have the majority stake of 83.64 percent in the company followed by local general public holding 15.16 percent shares of CLVL. The remaining ownership is divided among other categories of shareholders.

Hisotrical Performance (2019-25)

CLVL’s topline immensely plunged in 2019; however its bottomline turned out to be much healthier than the previous year due to profit recognized from discontinued operations. In the subsequent two years, CLVL suspended its business activity due to bleak macroeconomic conditions. In the meantime, in 2020, it received an acquisition offer which was delayed due to outbreak of COVID-19.

During the first three quarters of 2021, the company was in the process of acquisition which was ultimately completed on April 22, 2021 after which the new management changed the principal line of business from Textile to logistics and other ventures.

The company commenced its new line of business on June 30, 2021. In 2022, CLVL made revenue from its logistics business however it trickled down into a net loss. In 2023, not only did the topline made a staggering growth but bottomline was also recovered from net loss. In 2024 and 2025, both topline and bottomline slid.

After two years of posting net profit, CLVL posted net loss in 2025. The detailed performance review of each of the years under consideration is given below.

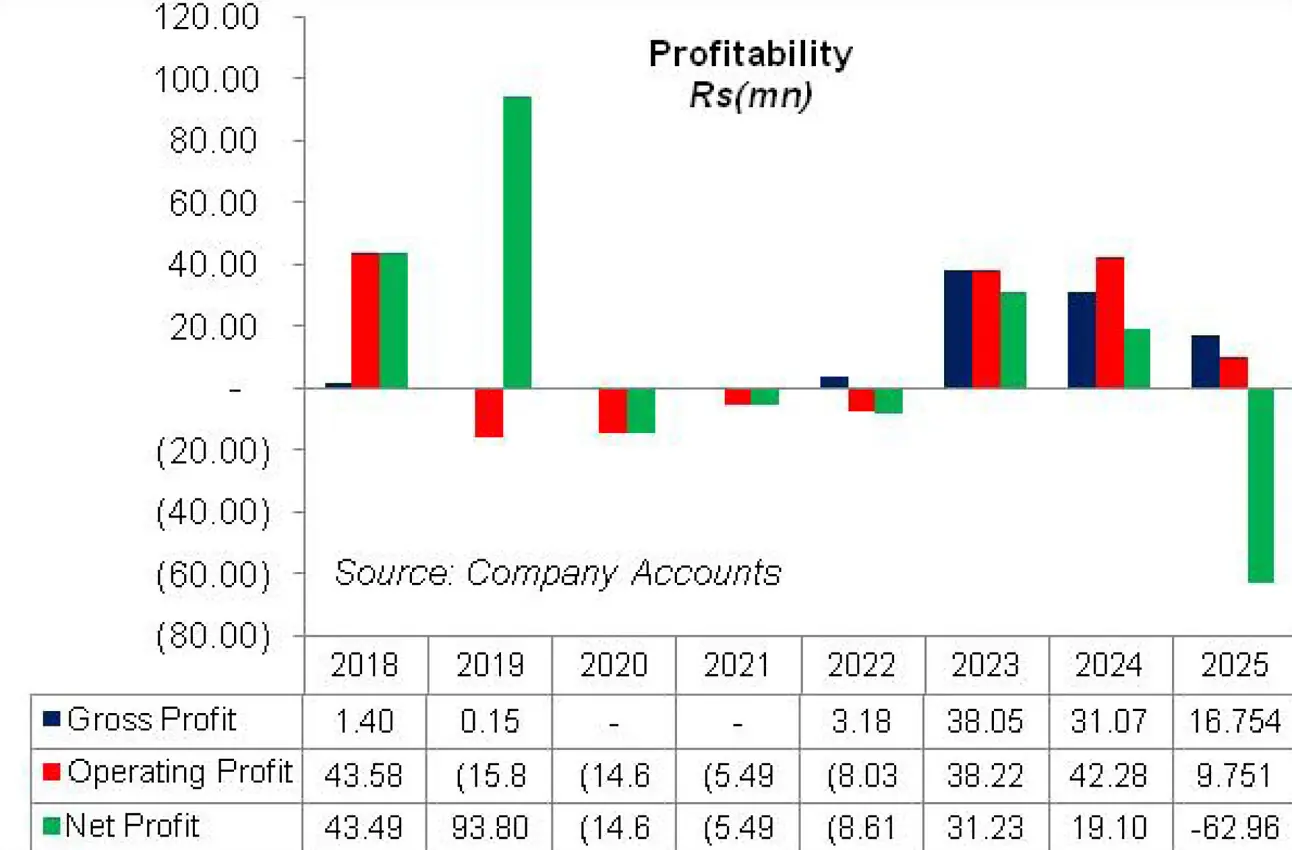

In 2019, CLVL (then Mian Textle Industries Limited) posted a topline drop of 88.84 percent year-on-year. Net sales clocked in at Rs 2.12 million in 2019 which represented income from trading of vehicles.

The company’s trading business of textile products wasn’t profitable anymore due to dejected macroeconomic backdrop and hence during the year, the company disposed off its fixed assets and transferred the ownership to M/s Pakistan Tiles (Private) Limited for Rs.410 million.

The gross profit declined by 89.10 percent year-on-year in 2019 with GP margin clocking in at 7.23 percent, slightly lesser than the GP margin of 7.41 percent posted in the previous year. Operating expense shrank by 17.22 percent year-on-year in 2019 due to considerable dip in non-operational expense particularly, fuel & power, impairment loss as well as salaries & wages.

Other income which greatly complimented its core revenue in 2018 massively slipped in 2019 due to high-base effect on account of write-off of long-term financial liabilities and deferred markup in 2018.

As a consequence, the company posted operating loss of Rs.15.83 million in 2019 as against operating profit of Rs.43.58 million posted in 2018. CLVL’s financial charges which comprised of bank charges inched down by 84.74 percent year-on-year in 2019.

Income from discontinued operations which comprised of gain on disposal of assets held for sale saved the day for CLVL and translated into net profit of Rs.93.80 million in 2019, up 115.69 percent year-on-year. EPS also surged from Rs.1.97 in 2018 to Rs.4.24 in 2019.

In 2020 and 2021, the company was in the process of acquisition and didn’t undertake any commercial business activity which pushed its revenue (trading income) to absolute zero for the two years and hence no cost of trading.

In 2020, the company’s operating expense slumped by 33.85 percent year-on-year due to no distribution expense and non-operational expense incurred during the year. Other expense also dived down by 90.73 percent year-on-year in 2020 due to a significant plunge in the provision for doubtful receivables booked during the year.

Operating loss measured down by 7.64 percent year-on-year in 2020 to clock in at Rs.14.61 million. As no financial charges and taxation was incurred in 2020, the net loss also stood at Rs.14.61 million in 2020 with loss per share of Rs.0.66. In 2021, operating expense further sank by 25.13 percent year-on-year due to sizeable drop in payroll expense, utilities expense as well as legal and professional charges incurred during the year.

CLVL didn’t incur any other expense in 2021, however, made other income of Rs.5.14 million mainly on account of disposal of land and other fixed assets.

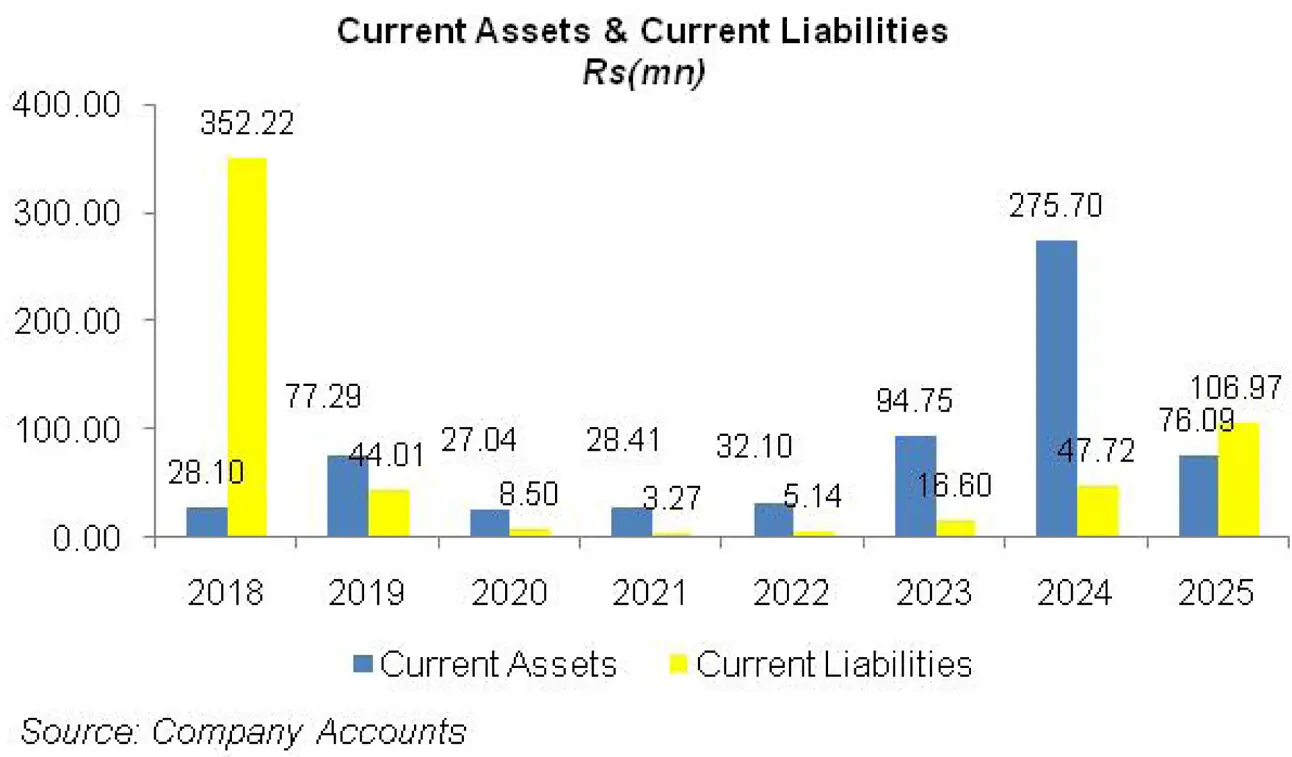

Operating loss and net loss were recorded at Rs.5.49 million in 2021, down 62.43 percent year-on-year with loss per share of Rs.0.24. In 2021, the new management approved to inject Rs.200 million to meet the working capital requirements of the company, out of which Rs.25 million were already injected by the end of the year. In 2021, the company commenced its commercial activity by acquiring equity stake in Trukkr (Private) Limited, a tech- enabled logistics company.

In 2022, CLVL registered revenue of Rs.8.30 million from its new line of business of providing commercial vehicles on rentals as well as logistics services. The sponsors further injected Rs.147.42 million in the company during the year and undertook other commercial activities such as investment in Finox (Private) limited and Children Clothing Retail (Private) Limited.

Direct cost was recorded at Rs.5.12 million which included loading and unloading cost as well as depreciation on vehicles. CLVL posted gross profit of Rs.3.18 million in 2022 which translated into GP margin of 38.28 percent. Operating expense escalated by 24 percent year-on-year primarily on the back of fee and subscription charges, directors’ meeting fee and auditors’ remuneration. Other income also slid by 61.45 percent year-on-year in 2022 due to high-base effect on account of disposal of fixed assets in 2021.

Operating loss grew by 46.25 percent year-on-year in 2022 to clock in at Rs.8.03 million. CLVL incurred finance cost (bank charges) of Rs.0.58 million in 2022 which translated into net loss of Rs.8.61 million, up 56.78 percent year-on-year. Loss per share grew to Rs.0.37 in 2022.

CLVL’s topline grew by 575.34 percent year-on-year in 2023 to clock in at Rs.56.05 million from logistics services and rental of commercial vehicles.

CLVL also invested in Neem Exponential (Private) Limited and International Learning Center (Private) Limited to diversify its business operations. Besides, the company also incorporated a wholly owned subsidiary NBFC called Cordoba Leasing Limited. These investments were financed by a right issue of Rs.500 million which drove its total paid-up capital to Rs.721.052 million. Direct cost surged by 251.38 percent year-on-year in 2023. This culminated into 1097.70 percent growth in gross profit in 2023 with GP margin jumping up to 67.89 percent.

Operating expense multiplied by 12.80 percent year-on-year in 2023. However, it was offset by a robust other income of Rs.15.04 million recorded in 2023, up 659 percent year-on-year. Hefty other income recorded during the year was the result of income on disposal of long-term investments, income on saving accounts and income on advances to subsidiary.

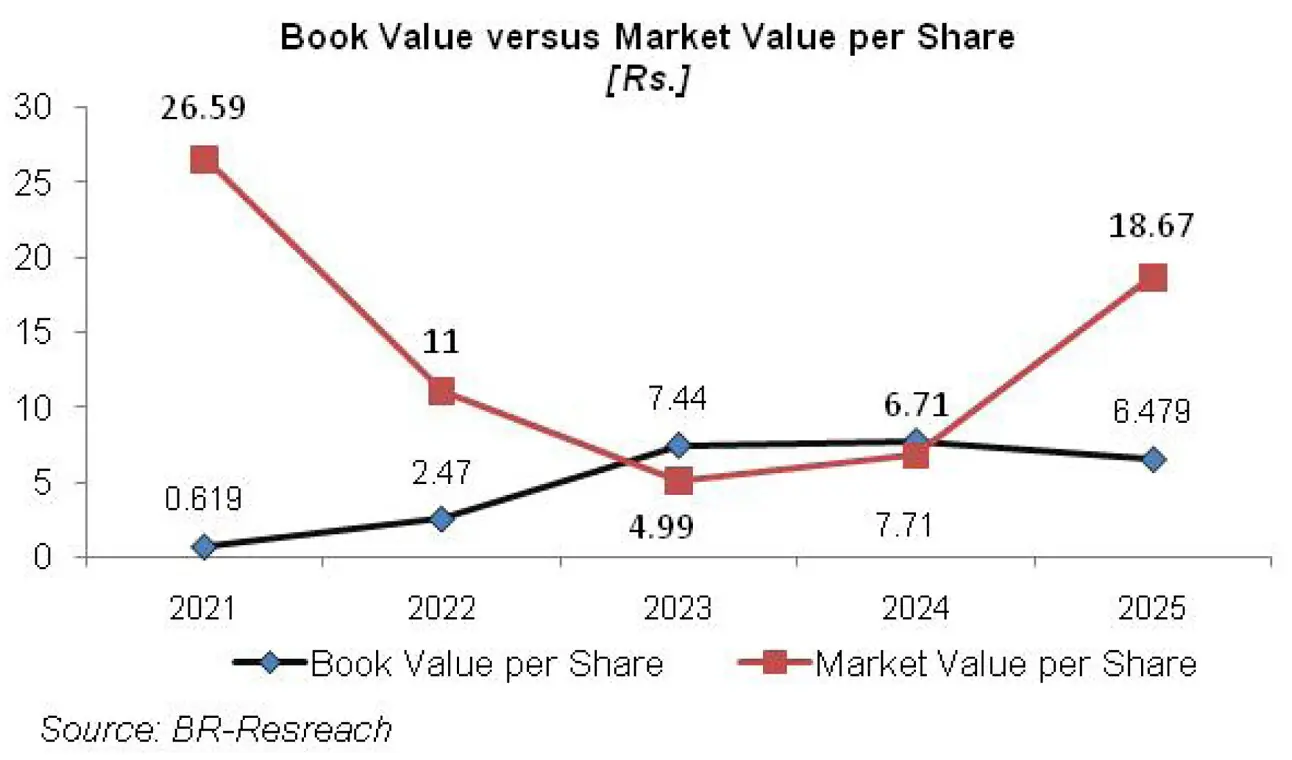

CLVL made operating profit of Rs.38.22 million in 2023 which translated into OP margin of 68.19 percent. Finance cost grew by 670.18 percent year-on-year in 2023. This was the result of mark-up on sponsor loan worth Rs.75 million obtained during the year to meet working capital requirements. After accounting for taxation expense, the company recorded net profit of Rs.31.23 million in 2023. EPS clocked in at Rs.0.52 in 2023 while NP margin stood at 55.71 percent.

In 2024, CLVL recorded 18.05 percent year-on-year dip in its topline which was recorded at Rs. 45.94 million. This was due to a decline in revenue from logistics and rental service business.

Revenue descent was on account of deteriorating macroeconomic fundamentals which resulted in depressed business activity of its customers. Direct cost dropped by 17.44 percent in 2024, resulting in 18.34 percent shrinkage in gross profit. GP margin largely remained intact at the last year level. Operating expense tumbled by 14.24 percent in 2024 due to considerably lower fee subscription charges, directors’ meeting fee as well as payroll expense.

Other income mounted by 59.29 percent in 2024 due to tremendous rise in mark-up income from loan to subsidiary. Operating profit ticked up by 10.62 percent in 2024 with OP margin climbing up to 92 percent. Finance cost escalated by 313.23 percent in 2024 due to higher discount rate and increase in sponsor’s loan.

CLVL recorded net profit of Rs.19.105 million in 2024, down 38.82 percent year-on-year. This translated into EPS of Rs.0.32 and NP margin of 41.59 percent in 2024.

In 2025, CLVL’s net revenue plunged by 48.42 percent to clock in at Rs.23.70 million. This was on account of logistics services and rental of commercial vehicles. In line with thinner revenue, cost of revenue also fell by 53.30 percent in 2025 mainly on the back of lower loading and unloading cost. Gross profit tapered off by 46 percent to clock in at Rs.16.75 million in 2025. This translated into GP margin of 70.71 percent in 2025.

Administrative expense ticked up by 8.17 percent in 2025 due to higher payroll expense as well as provision booked on ECL. Number of employees went down from 7 in 2024 to 4 in 2025. Other income also dwindled by 71.65 percent in 2025 due to considerable decline in mark-up income on loan to subsidiary. This was due to lower discount rate and also because the loan of Rs.113.400 million granted to Cordoba Financial Service Limited was matured in the previous year and a new long-term loan of Rs.20.900 million was granted to the same subsidiary in 2025.

Operating profit diminished by 76.94 percent in 2025 to clock in at Rs.9.75 million. Finance cost mounted by 243.14 percent in 2025 despite monetary easing. This was because the sponsor loan surged from Rs.78.715 million in 2024 to Rs.485.215 million in 2025. CLVL posted net loss of Rs.62.959 million in 2025 as against net profit posted during the last two years. Loss per share was recorded at Rs.0.87 in 2025.

Recent Performance (1QFY26)

During the first half of the ongoing fiscal year, CLVL posted 31.75 percent year-on- year dip in its topline which clocked in at Rs.5.32 million. This was primarily due to lesser logistics and rental services. Lower fleet utilization, stable fuel cost and steady Pak Rupee resulted in 31.82 percent decline in cost of sales in 1QFY26.

Gross profit also tapered off by 31.72 percent to clock in at Rs.3.94 million in 1QFY26, however, GP margin stayed intact at 74 percent in 1QFY26.

Administrative expense multiplied by 32.72 percent in 1QFY26 due to mounting fee & subscription charges. Other income deteriorated by 80.19 percent in 1QFY26 due to lower mark-up income on loan to subsidiary on account of monetary easing. Loss recorded on the disposal of fixed assets also contributed in squeezing other income in 1QFY26.

CLVL recorded 72.81 percent thinner operating profit to the tune of Rs.1.99 million in 1QFY26. This translated into OP margin of 37.48 percent in 1QFY26 versus OP margin of 94 percent posted in 1QFY25.

Finance cost surged by 134.37 percent in 1QFY25 due to higher mark-up incurred on sponsor’s loan. CLVL posted net loss of Rs.14.16 million in 1QFY26 versus net profit of Rs.0.25 million registered during the same period last year. Loss per share was recorded at Rs.0.20 in 1QFY26 versus EPS of Rs.0.003 recorded in 1QFY25.

Future Outlook

Depressed business activity didn’t allow the company to materialize its forecasted revenue stream as a logistics and vehicle rental business. However, the company is making continuous efforts to diversify its revenue by investing in varied businesses and sectors. This may keep CLVL revenue and profits afloat in the coming times.

The company has been granted permission by the SECP to form a NBFC under the name of Cordoba PE Management Limited (CPML) to carry out private equity and fund management services. CLVL has injected Rs.49.999 million against allotment of 4,999,996 shares of CPML.

Besides, the company has also invested Rs.20.90 million as loan in Cordoba Financial Services Limited (CFSL) besides injecting Rs.425 million as equity. The company is also converting its outstanding loan of Rs.113.40 million into equity at par value of Rs.10 per share.

The company is also in the process of restructuring its loan to cater to the deferment of repayment of loan and markup. This will improve the liquidity position of CLVL.

Copyright Business Recorder, 2025

Comments

Comments are closed for this article.