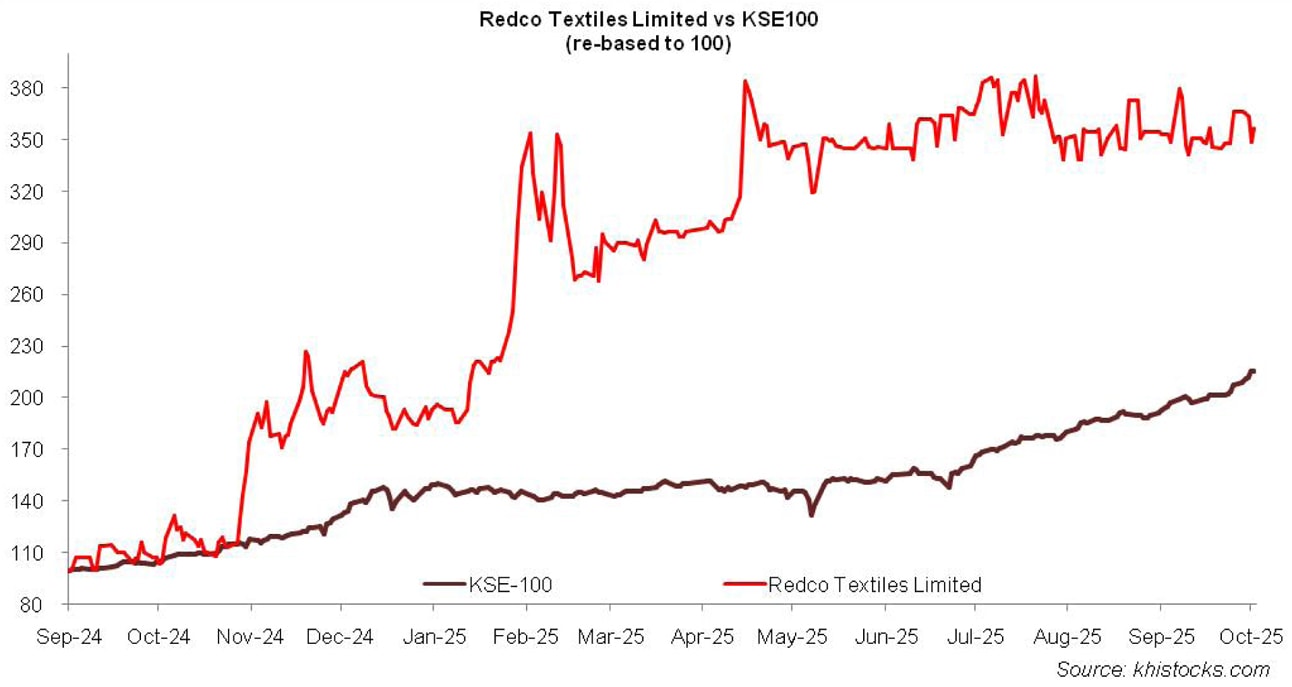

Redco Textiles Limited (PSX: REDCO) is incorporated in Pakistan as a public limited company. It began its operations in 1991 and is engaged in the manufacturing and sale of yarn and greige fabric.

Pattern of Shareholding

As of June 30, 2025, REDCO has a total of 49.293 million shares outstanding which are held by 761 shareholders. Directors, CEO, their spouse and minor children are the major shareholders of REDCO holding 60.52 percent shares followed by local general public holding 34.79 percent shares.

Banks, DFIs and NBFIs have a stake of 1.70 percent in REDCO while investment companies account for 1.31 percent shares. The remaining shares are held by other categories of shareholders.

Historical Performance (2019-24)

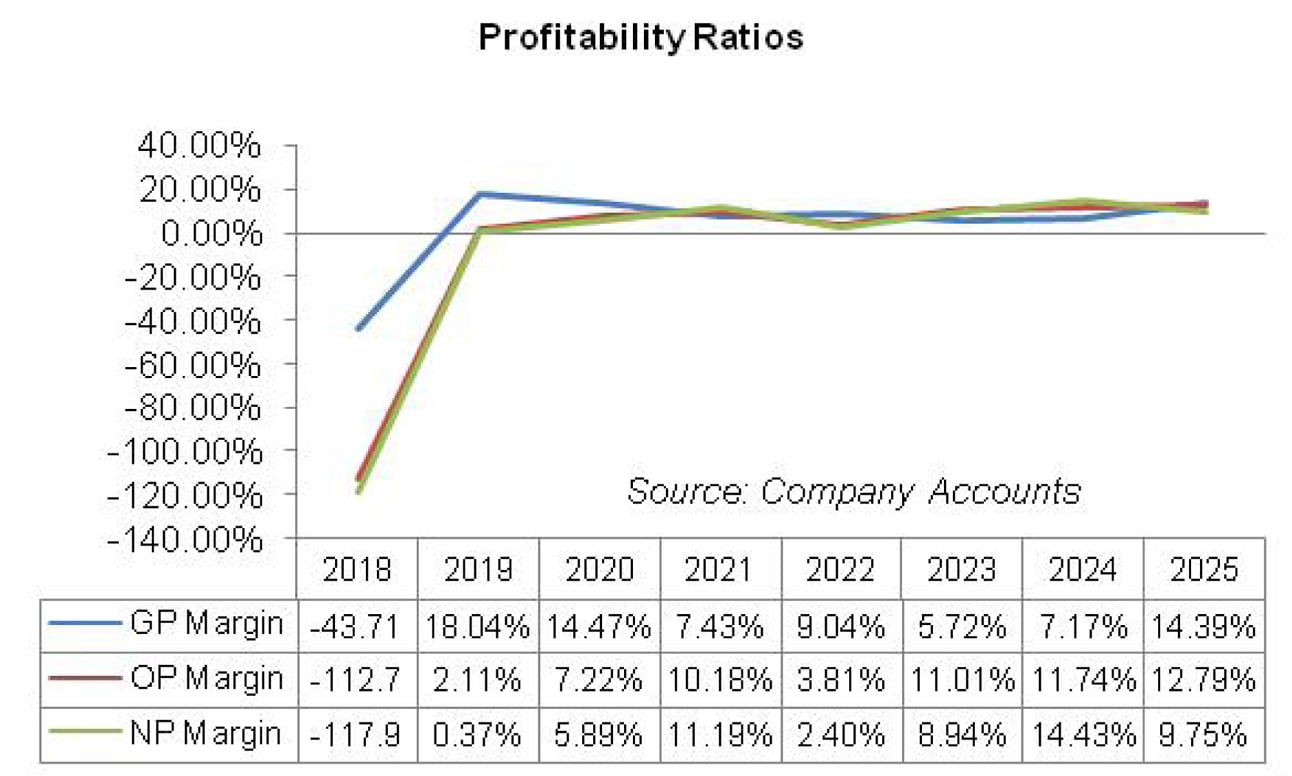

Except for a year-on-year decline in 2019, REDCO’s topline has registered growth over the period under consideration. Conversely, its bottomline slid in 2022 and 2025.

The gross margin of the company after posting a recovery in 2019 followed a downhill journey until 2021. It rebounded in 2022. In 2023, gross margin dipped followed by an uptick in the subsequent years.

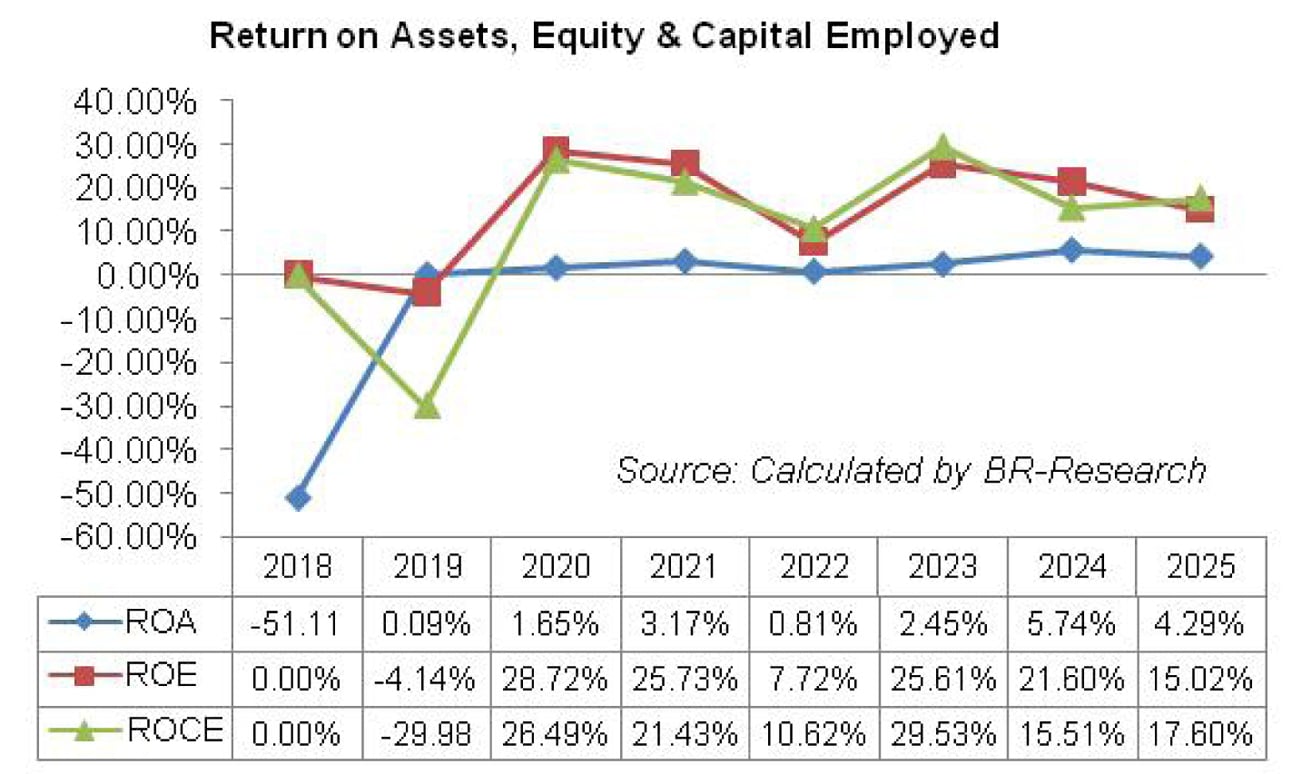

Conversely, operating margin and net profit margins followed an upward trajectory until 2021 followed by a drastic decline in 2022. In 2023 and 2024, both operating and net margins registered staggering growth. Operating margin continued to grow in 2025 while net margin attained its optimum level in 2024 and receded in 2025 (see the graph of profitability ratios). The detailed performance review of the period under consideration is given below.

In 2019, REDCO’s net sales dipped by 43 percent year-on-year to clock in at Rs.251.37 million. During the year, the company had suspended its operations due to high cost of doing business, incidental taxes, provincial cess and withholding tax which had rendered the local textile industry uncompetitive compared to their international counterparts. However, it resumed its operations in December 2018 after the government announced subsidy for textile industry by reducing RLNG rates.

Moreover, during the period of shutdown, the company installed 20 looms to increase its productivity and reduce conversion cost. Due to less number of operational days, the sales of both yarn and fabric tumbled; however, the company was able to post gross profit of Rs.45.34 million in 2019 as against gross loss of Rs.192.86 million recorded in 2018. GP margin stood at 18 percent in 2019.

The company was able to trim down its distribution cost by 93.28 percent year-on-year in 2019 mainly on account of lower salaries of sales force as well as low carriage, freight and taxes. Administrative expense also slumped by 6.17 percent year-on-year in 2019. Other expense which stood at a whopping Rs.285 million in 2018 due to impairment loss on fixed assets as well as loss on disposal of fixed assets shrank to Rs.25.77 million in 2019.

REDCO posted operating profit of Rs.5.305 million in 2019 with OP margin of 2.11 percent. This was against the operating loss of Rs.497.42 million recorded in 2018. Finance cost inched down by 76.47 percent year-on-year in 2019 despite high discount rate. This was because the company largely settled the loans obtained from the banking companies. As of June 30, 2019, REDCO’s balance sheet only contained interest free loans from associated undertakings and company directors.

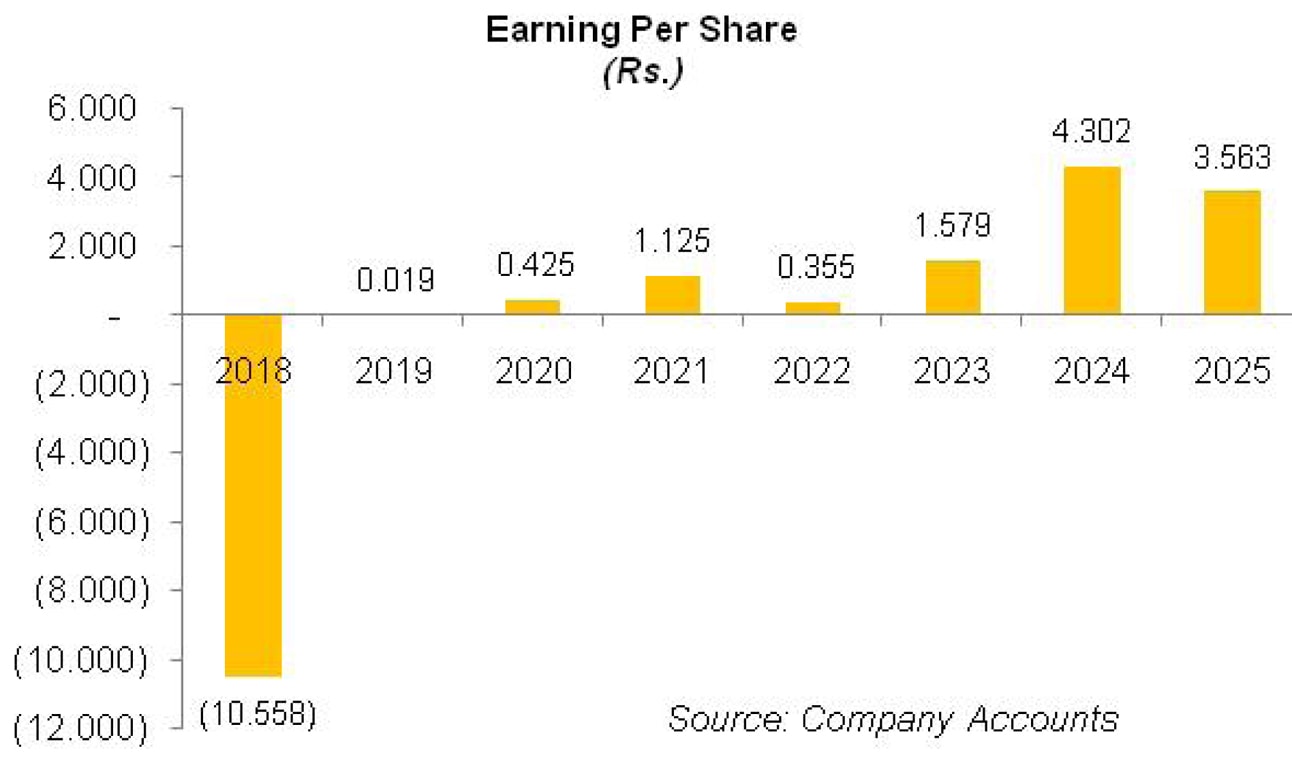

The company posted net profit of Rs.0.94 million in 2019 as against the net loss of Rs.520.43 million posted in 2018. EPS stood at Rs.0.019 in 2019 versus loss per share of Rs.10.558 registered in 2018. NP margin clocked in at 0.37 percent in 2019.

In 2020, REDCO’s topline grew by 41.42 percent year-on-year to clock in at Rs.355.48 million. This was despite the outspread of COVID-19. In the first three quarters of 2020, sales volume posted an impressive growth mainly due to the installation of 32 air jet looms and also because of replacement of sizing and warping with latest model machines. The topline also included export sales of Rs.11.083 million which wasn’t there until 2019.

Cost of sales grew by 47.57 percent year-on-year in 2020 due to increase in utility charges and also because of Pak Rupee depreciation. Gross profit grew by 13.44 percent year-on-year in 2020, however, GP margin climbed down to 14.47 percent. Distribution expense nosedived by 12.70 percent year-on-year in 2020 while administrative expenses rose by 20.89 percent year-on-year in 2020.

Other expense fell by 66.27 percent year-on-year in 2020 on account of lesser loss on the disposal of fixed assets and lesser allowance booked for expected credit loss on trade debts. Operating profit grew by a massive 384 percent year-on-year in 2020 while OP margin mounted to 7.22 percent.

Finance cost shrank by 90.91 percent year-on-year in 2020 as there were no short-term borrowings from banking institutions as of June 2020. However, the company borrowed Rs.12.049 million under SBP Refinance Scheme for the payment of salaries and wages at a mark-up rate of 3 percent per annum. The bottomline expanded by 2124.26 percent year-on-year in 2020 to clock in at Rs.20.95 million with NP margin of 5.89 percent. EPS surged to Rs.0.425 in 2020

In 2021, REDCO posted topline growth of 39.38 percent year-on-year. Its topline clocked in at Rs.495.47 million in 2021. During the year, the company installed another 40 air jet looms to increase its productivity. While there were no export sales in 2021, local sales of both yarn and fabric posted a staggering growth. Cost of sales increased by 50.86 percent in 2021 because of high inflation, high utility charges as well as Pak Rupee depreciation.

Consequently, gross profit dropped by 28.45 percent year-on-year in 2021 with GP margin falling down to 7.43 percent. Lesser local taxes, carriage and freight resulted in 28.51 percent year-on-year drop in distribution expense while administrative expense grew by 2.10 percent year-on-year on the back of high payroll expense in 2021. Other expense dwindled by 20.86 percent year-on-year in 2021 due to lesser provisioning done for WPPF and no loss recorded on the disposal of fixed assets in 2021.

Other income multiplied by over 52026 percent to clock in at Rs.37.94 million in 2021. This was on account of previous year impairment coupled with the amortization of government grant. Operating profit grew by 96.50 percent year-on-year in 2021 translating into OP margin of 10.18 percent .

Finance cost grew by over 1525 percent to clock in at Rs.2.06 million due to higher bank charges, elevated mark-up on WPPF and long-term borrowings. Bottomline grew by 164.59 percent year-on-year in 2021 to clock in at Rs.55.44 million with NP margin of 11.19 percent. EPS rose to Rs.1.125 in 2021.

In 2022, REDCO witnessed topline growth of 47 percent year-on-year. Its net sales were recorded at Rs.728.59 million in 2022. The company increased its production capacity by adding 36 air jet looms in 2022. While the sale of yarn significantly dropped during the year, the sale of fabric posted an encouraging growth.

Due to shortage of gas, the company had to rely on electrical energy which increased the cost of sales by 44.49 percent year-on-year in 2022. However, as the sales mix majorly included fabric which had better pricing, GP margin mounted to 9 percent in 2022. Distribution and administrative expense mounted by 150.12 percent and 32.54 percent respectively in 2022 mainly on account of higher payroll expense. Higher loss on disposal of fixed assets resulted in 126.44 percent year-on-year rise in other expense in 2022.

Consequently, operating profit declined by 45 percent year-on-year in 2022 with OP margin shrinking to 3.81 percent. Finance cost shriveled by 58.85 percent year-on-year in 2022 due to massive drop in company’s long-term financing as well as bank charges during the year coupled with lesser WPPF.

The bottomline tapered off by 68.45 percent year-on-year in 2022 to clock in at Rs.17.49 million with NP margin of 2.40 percent. EPS dropped to Rs.0.355 in 2022.

During 2023, REDCO’s topline grew by 19.54 percent year-on-year to clock in at Rs,870.96 million. While the company made no yarn sales in 2023, the growth was driven by the sale of fabric. The company installed 20 new Toyota air jet looms during the year as a part of its periodic plant renewal strategy. This greatly improved the company’s production capacity and efficiency in 2023.

However, high cost of sales due to mounting energy charges, higher inflation and supply chain impediments due to massive floods which destroyed the crop, resulted in 24.40 percent drop in gross profit in 2023 with GP margin plummeting to 5.72 percent. Distribution cost multiplied by 7.44 percent year-on-year in 2023 on account of higher salaries paid in the distribution network.

Administrative cost also inched up by 9.78 percent year-on-year in 2023 due to inflationary pressure which drove the payroll expense. The company downsized its workforce from 699 employees in 2022 to 549 employees in 2023. Other expense slid by 37.21 percent year-on-year in 2023 due to no loss recorded on the disposal of fixed assets in 2023. REDCO also didn’t record the unwinding of salary loan in 2023. Other income grew by 10084 percent year-on-year to clock in at Rs.81.49 million in 2024 due to liability written off during the year.

Hefty other income allowed the company to record operating profit of Rs.95.90 million in 2023, up 245.54 percent year-on-year. Finance cost mounted by 111 percent in 2023 to clock in at Rs.1.79 million. This was due to unprecedented level of discount rate which increased the mark-up incurred on WPPF. Bank charges & commission also greatly increased during the year. Net profit strengthened by 345.10 percent to clock in at Rs.77.845 million in 2023 with EPS of Rs.1.579 and NP margin of 8.94 percent.

In 2024, REDCO’s topline posted a phenomenal year-on-year rise of 66.80 percent to clock in at Rs.1470.17 million. This was driven by the sale of fabric. Inflationary pressure coupled with elevated prices of energy and other inputs drove the cost of sales up by 66.19 percent in 2024. Gross profit improved by 111.85 percent in 2024 with GP margin climbing up to 7.17 percent. During the year, the company’s distribution expense spiked by 331.48 percent due to massive increase in salaries & benefits of sales force.

Conversely, administrative expense slid by 3.18 percent in 2024 due to lower depreciation expense incurred during the year. Other expense mounted by 83 percent in 2024 due to higher provision booked for WPPF, doubtful debts & advances and ECL on trade debts. Other income strengthened by 36.96 percent in 2024 on account of gain recognized on the sale of assets. REDCO recorded 79.96 percent improvement in its operating profit in 2024 with OP margin rising up to 11.74 percent.

Finance cost increased by 49.39 percent in 2024 to clock in at Rs.2.68 million. This was on account of higher bank charges & commission and higher mark-up incurred on WPPF. REDCO recorded 172.44 percent year-on-year growth in its net profit in 2024 which clocked in at Rs.212.08 million with EPS of Rs.4.302. NP margin attained its highest level of 14.43 percent in 2024.

In 2025, REDCO’s net sales rebounded by 22.47 percent to clock in at Rs.1800.495 million. This was due to increased sales of value added fabric. Weaving looms were utilized at 70 percent capacity in 2025.

The company continued to focus on operational efficiency by modernization of its machinery, installing of solar panels etc. This resulted in 145.73 percent improvement recorded in gross profit in 2025 with GP margin mounting to 14.39 percent.

Higher freight charges and increased salaries of sales force resulted in 10.94 percent spike recorded in distribution expense in 2025. Administrative expense inched up by 1.88 percent in 2025 due to higher payroll expense on account of inflationary pressure and workforce expansion from 535 employees in 2024 to 540 employees in 2025.

Other expense escalated by 41.74 percent in 2025 due to higher provisioning done for WPPF and slow moving store and spares. Other income deteriorated by 80 percent in 2025, however, could easily offset other expense. Other income dipped due to high-base effect as the company recorded hefty gain on sale of assets in 2024. REDCO recorded 33.42 percent rebound in its operating profit in 2025 with OP margin inching up to its optimum level of 12.79 percent.

Finance cost ticked up by 6.31 percent in 2025 despite monetary easing. This was due to higher interest incurred on WPPF. Net profit dwindled by 17.19 percent to clock in at Rs. 175.631 million in 2025. This was because the company recognized deferred tax asset in the previous which buttressed its net profit. EPS clocked in at Rs.3.563 while NP margin was recorded at 9.75 percent in 2025.

Future Outlook

REDCO’s increased inclination towards alternate energy sources and up-gradation of its machinery will continue to benefit the company by cutting down its cost and improving its margins. Improved prospects of Pakistan’s textile exports on the back of international restrictions on China will also augur well for the company and result in improved margins and profitability. REDCO is also exploring new export markets to diversify its geographical mix and reduce its dependence on limited number of international customers.

Copyright Business Recorder, 2025

Comments

Comments are closed for this article.