Pakistan’s external account is once again coming under strain as import growth outpaces both exports and remittances, reviving the risk of renewed external imbalances.

The SBP and IMF now anticipate a current account deficit of 0.5–1 percent of GDP in FY26 — modest in size, but indicative of lingering pressure on external buffers.

While a widening trade gap is driving much of this shift, the loss of steam in remittance inflows — a key source of stability last year — can become a vulnerability.

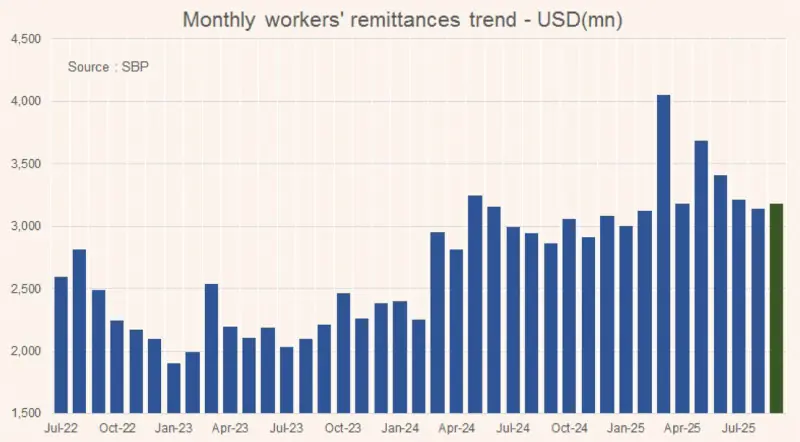

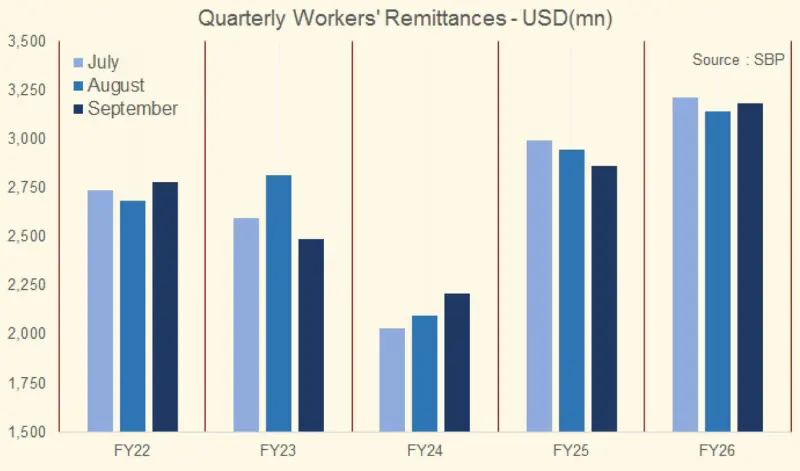

Remittances in Sep-25 remained largely unchanged from the previous month, continuing the stable but flat trend seen since the start of FY26.

Total inflows for 1QFY26 reached about $9.5 billion, 8.4 percent higher than last year, but this increase reflects the high base set in FY25 rather than fresh momentum.

The 12-month rolling average has alsolevelled off, showing that the strong growth phase is over.

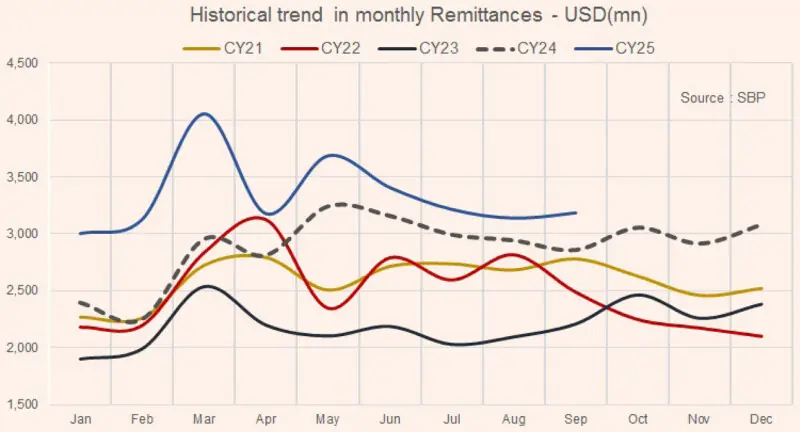

Last year’s surge came on the back of a strict crackdown on hundi/hawala channels and incentives for banks and exchange companies, which pushed more flows through official routes. UAE inflows, for instance, jumped over 40 percent despite lower new migration. But these policy boosts are unlikely to continue at the same scale this year.

The biggest uncertainty now is whether remittance subsidies will continue. The remittance subsidy approved recently is far below what was allocated in FY25. As a result, banks may reduce incentives, making formal channels less attractive.

Adding to the uncertainty around local incentives is the cooling of global remittance trends. The sharp rise in inflows last year was partly a one-off — driven by post-pandemic adjustments and exchange rate gaps that made formal channels more attractive.

Now that labour migration is steady and those currency gaps have narrowed, the chances of strong double-digit remittance growth in FY26 are slim.

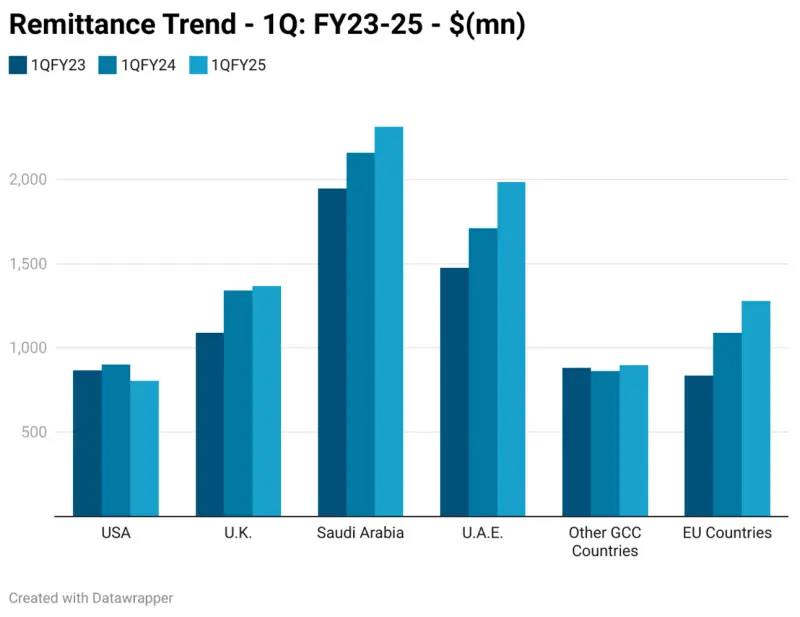

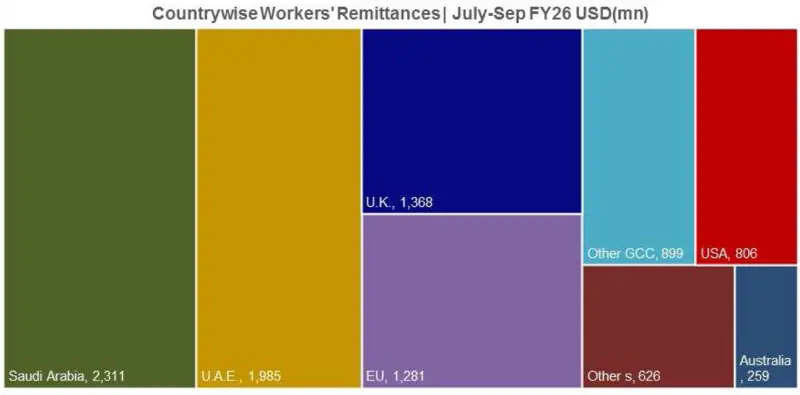

A global or regional shock could make matters worse. A slowdown in the GCC economies or heightened geopolitical tensions could drag down remittances further, especially from Saudi Arabia and the UAE, which together send almost 60 percent of the total inflows to Pakistan.

Pakistan’s remittances might not grow fast enough to offset the rising trade gap. With remittance flows flattening and imports picking up as the economy slowly recovers, the external account is becoming more exposed to shocks.

If incentives for remittances are withdrawn while imports keep increasing, the pressure may fall on the exchange rate or interest rates, making economic stabilization harder to maintain.

Copyright Business Recorder, 2025

Comments

Comments are closed for this article.