Oil and Gas Development Company Limited (PSX: OGDC) closed FY25 with a mixed set of results, reflecting the twin pressures of declining production volumes and lower global oil prices, offset partially by robust other income and the company’s continued exploration drive.

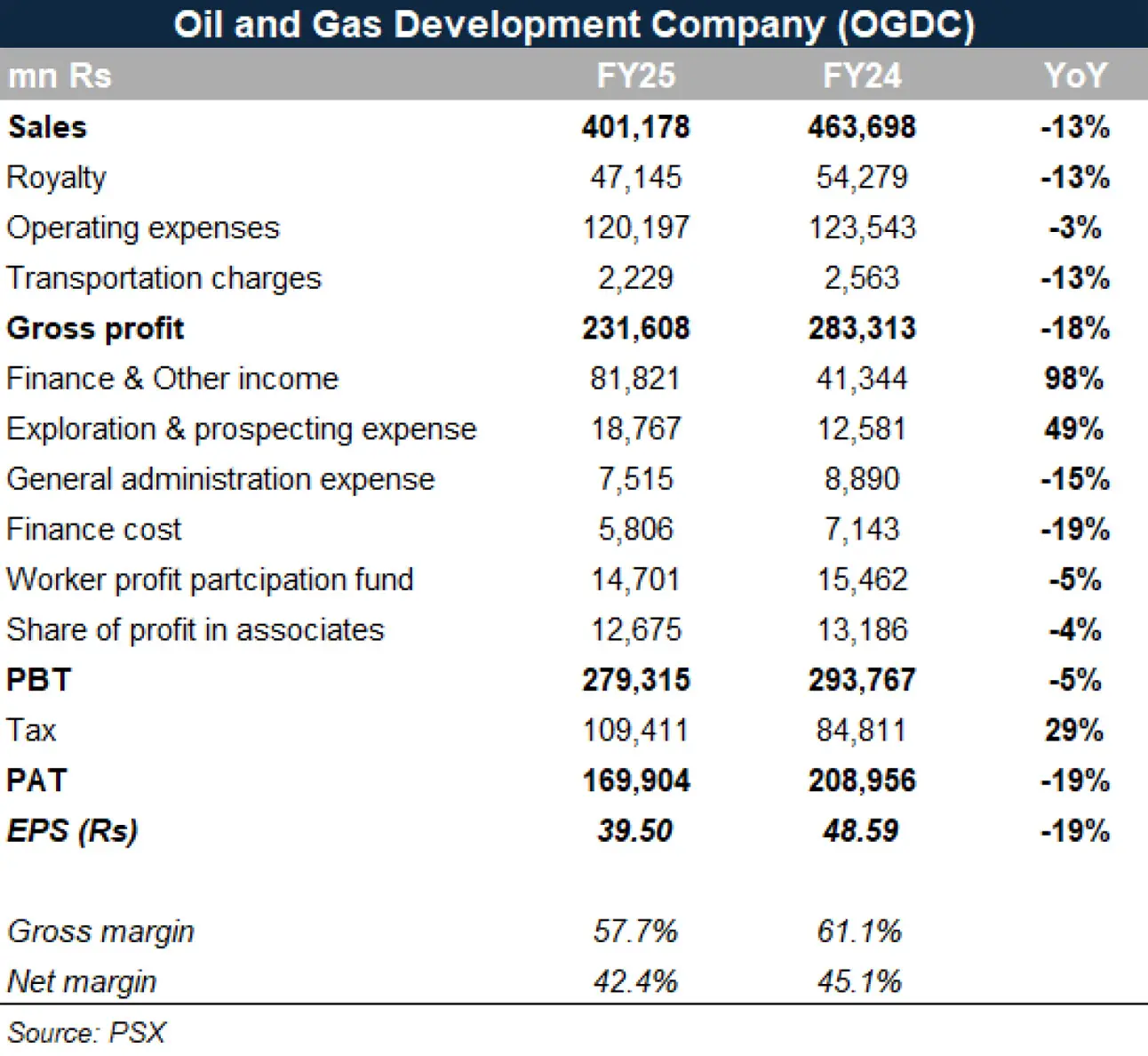

The firm reported after-tax earnings of around Rs170 billion, representing a 19 percent year-on-year decline compared to FY24.

The fall in profitability was primarily attributable to a 13 percent drop in net sales, caused by a 6–7 percent decline in oil output to around 30,900 barrels per day, a 9 percent decline in gas production to 652 mmcfd, and lower realized oil prices averaging $60.8 per barrel versus USD 68.7 last year.

Gas curtailment by SNGPL due to surplus RLNG was particularly costly, with management estimating a revenue loss of Rs40–43 billion.**

Despite weaker earnings, OGDC declared its highest ever full-year dividend at Rs15.05 per share, compared to Rs10.10 in FY24. Gross margins narrowed to 57.7 percent from 61.1 percent, reflecting the impact of lower volumes and prices, while the effective tax rate rose sharply to 39.2 percent against 28.9 percent in FY24.

Exploration costs climbed 49 percent to Rs18.8 billion, largely due to three to four dry wells and intensified seismic activity across blocks. However, other income nearly doubled to Rs82 billion, driven by interest income from TFCs, delayed payment surcharges, and significant foreign exchange gains amid PKR volatility.

Operationally, OGDC continues to dominate the domestic upstream landscape, holding 49 percent of Pakistan’s oil reserves and 31 percent of gas reserves, while contributing nearly half of national oil output and over a quarter of gas. The company drilled 15 wells during the year—nine exploratory, five development, and one re-entry—resulting in five new discoveries. Seismic activity remained strong resulting in a large share foo OGDC of national exploration activity.

Several projects are in the pipeline. Production from the Wali block is expected in the coming months, with initial flows estimated at 25–35 mmcfd of gas and 2,500–3,500 barrels of oil per day, scaling up to 50 mmcfd and 5,000 barrels per day by FY27.

Compression projects at Dakhni, KPD-TAY, and Uch are due for completion in FY26, which together should add around 737 mmcfd of gas processing capacity. The company has also advanced its overseas exploration, with phase one of its Abu Dhabi ADNOC block yielding discoveries; production is anticipated by FY28–29.

Improved collections, with a 109 percent recovery ratio in FY25, have also strengthened the company’s liquidity. While capital expenditure for FY26 is projected at PKR 50–60 billion, with an additional USD 50–100 million earmarked for Reko Diq and other development projects.

While FY25 earnings were subdued, OGDC’s record dividend payout underscores its resilience, underpinned by strong reserves, active exploration, and stable cash generation along with ongoing production revival projects and planned capex.

Comments

Comments are closed for this article.