Pakistan Hotels Developers Limited (PSX: PHDL) was incorporated as a private limited company in Pakistan in 1979 as Taj Mahal Hotels Limited. It was converted into a public limited company in 1981. The principal activity of the company was hotel business besides owning and operating a five star hotel, Regent Plaza Hotel and Convention Centre, Karachi. Recently, the company entered into a sale agreement for the transfer of its property to SIUT trust.

Pattern of Shareholding

As of June 30, 2024, PHDL had a total of 18 million shares outstanding which were held by 608 shareholders.

Directors and their relatives have the highest shareholding of 84.18 percent in the company followed by individuals accounting for 14.42 percent of PHDL’s outstanding shares. The remaining shares are held by other categories of shareholders.

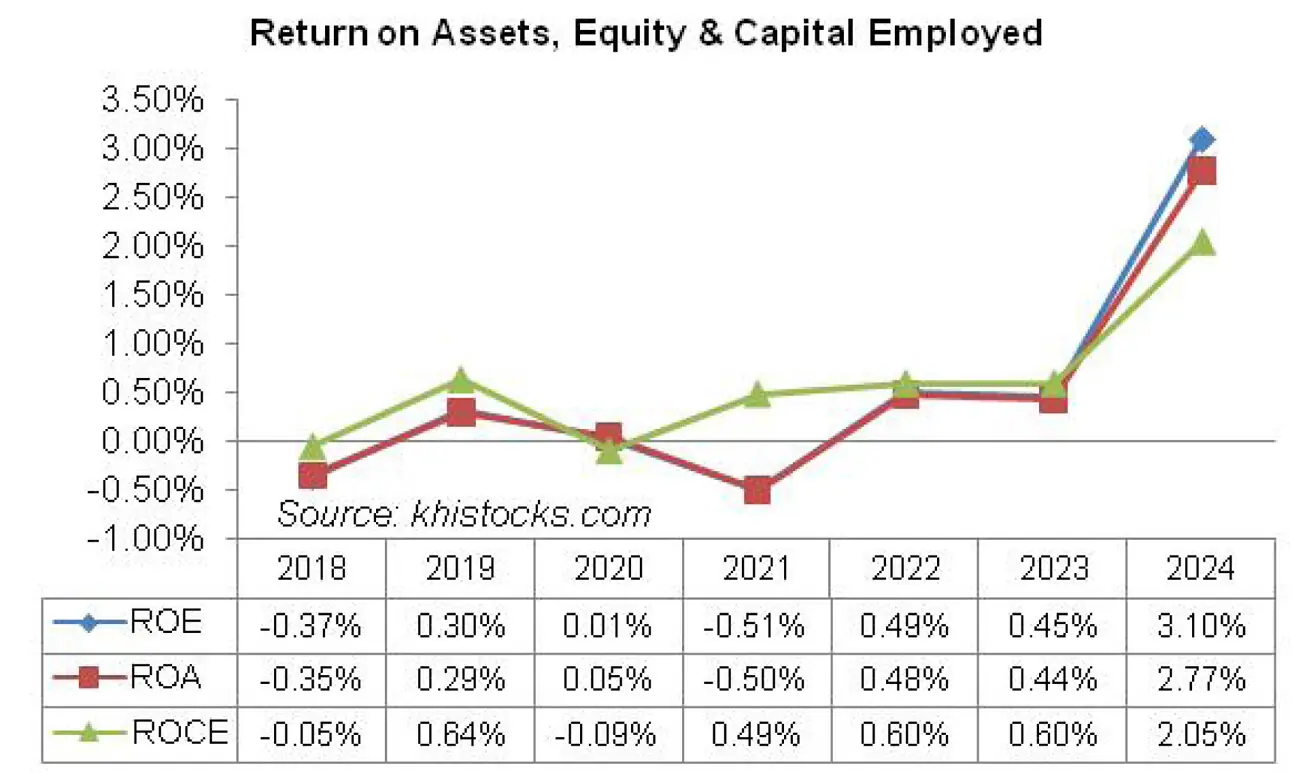

Performance trend (2019-24)

Except for a year-on-year decline in 2020 and 2021, PHDL’s topline rode an upward trajectory over the period under consideration. In between these years, PHDL’s bottomline strengthened in 2019 followed by a drastic plunge in 2020 and net loss in 2021. In 2022, PHDL posted net profit which leveled down in the subsequent year. In 2024, PHDL posted the highest ever net profit.

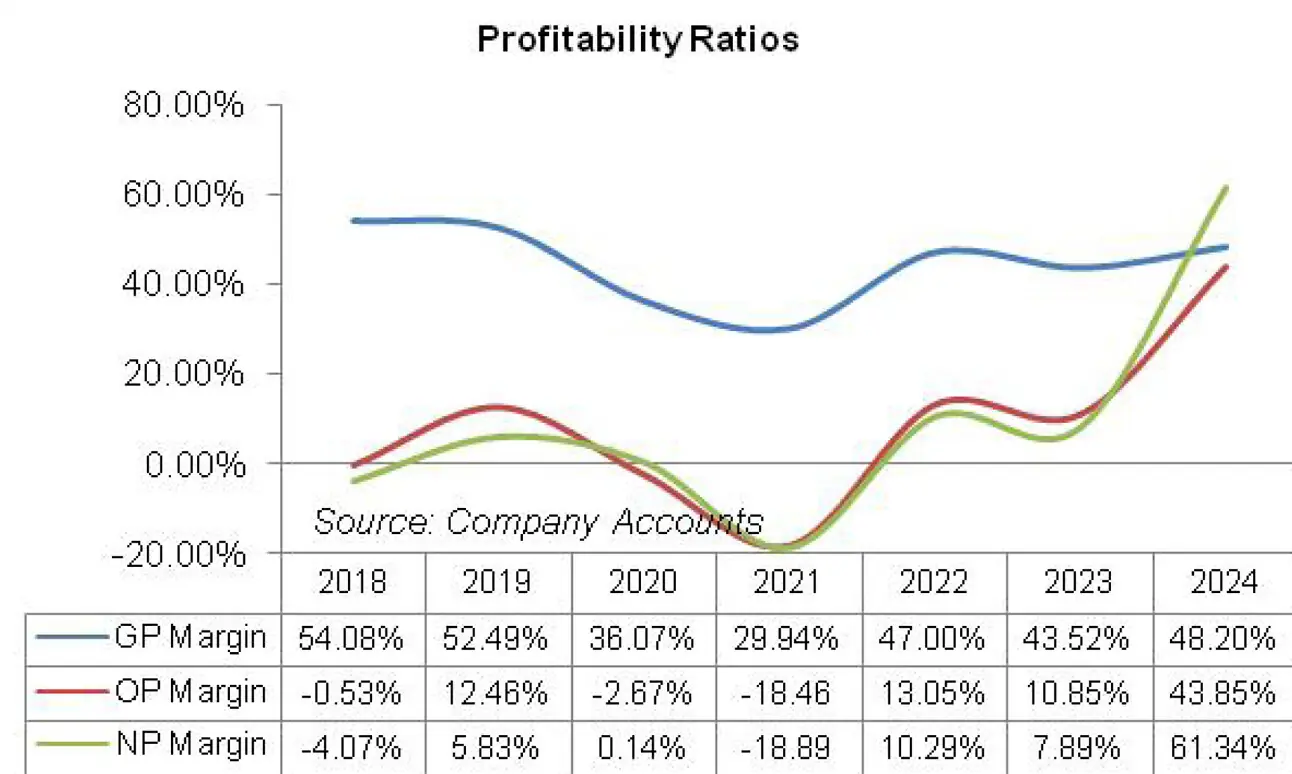

The company’s margins have shown volatility over the period. Gross margin dropped until 2021. Conversely, operating and net margins greatly improved in 2019 followed by a decline in 2020 and 2021. In 2022, all the margins rebounded, then ticked down in 2023 followed by a revival in 2024. The detailed performance review of the period under consideration is given below.

2019 was a stable year for PHDL as its topline grew by 15.29 percent year-on-year to clock in at Rs.480.539 million. This was on the back of higher occupancy as well as reasonable food and beverage sales.

However, high cost of sales on the back of market driven increase in salaries coupled with guest supplies, heat and power prices kept GP margin under check which ticked down to 52.50 percent in 2019 versus GP margin of 54 percent recorded in 2018.

Operating expense slid by 15.46 percent year-on-year in 2019, allowing PHDL to record operating profit of Rs.59.869 million in 2019 with OP margin clocking in at 12.46 percent. This was against the operating loss of Rs. 2.213 million posted in 2018.

Finance cost gave major support to the bottomline as it plunged by 56.56 percent year-on-year during the year as the company settled running finances obtained in the previous years to overcome the liquidity shortfall.

During the year, the company obtained an interest free loan of Rs. 2.5 million from the director of the company for working capital requirements. Finance cost of the company comprised of remaining interest payable on short-term borrowing as well as interest on lease liabilities as it purchased furniture and fixtures and a vehicle through leasing during the year.

The company posted profit after tax of Rs.28.01 million in 2019 with NP margin of 5.83 percent. During the year company also made capital investment in fire safety equipment to avoid any mishap in the future.

Further, the management asked the tenants of their shops to vacate the premises for safety and security reasons. This added to operating expense as rent receivables were written off.

While the PHDL was in the process of recovering from the shocks of fire incident happened in December 2016 (FY17), the unpredictable COVID-19 jolted its subsistence.

The business activity of PHDL halted for more than three months which culminated into a topline drop of 32 percent year-on-year in 2020.

The company recorded net revenue of Rs.326.721 million in 2020. Cost of sales also plummeted due to low occupancy and food and beverages sales. GP margin nosedived to 36 percent in 2020 with 53.28 percent thinner gross profit.

Thankfully, operating expense gave some breather as they slid by 33.72 percent year-on-year as unlike last year, there was no compensation to the fire incident sufferers as well as no shops premium paid in 2020. Repair and maintenance cost also shrank during the year.

Other income grew significantly as the company disposed its assets and earned profit on saving accounts, however, in absolute terms, other income of Rs.1.186 million wasn’t capable enough of providing any support to the bottomline. The company made operating loss of Rs. 8.711 million in 2020.

Finance cost dropped by 74.45 percent year-on-year in 2020 as the company fully paid the interest charges on its short-term borrowings last year. PHDL posted loss before tax worth Rs.9.793 million in 2020, however, deferred taxation allowed PHDL to post positive bottomline of Rs0.442 million in 2020 with NP margin of 0.14 percent.

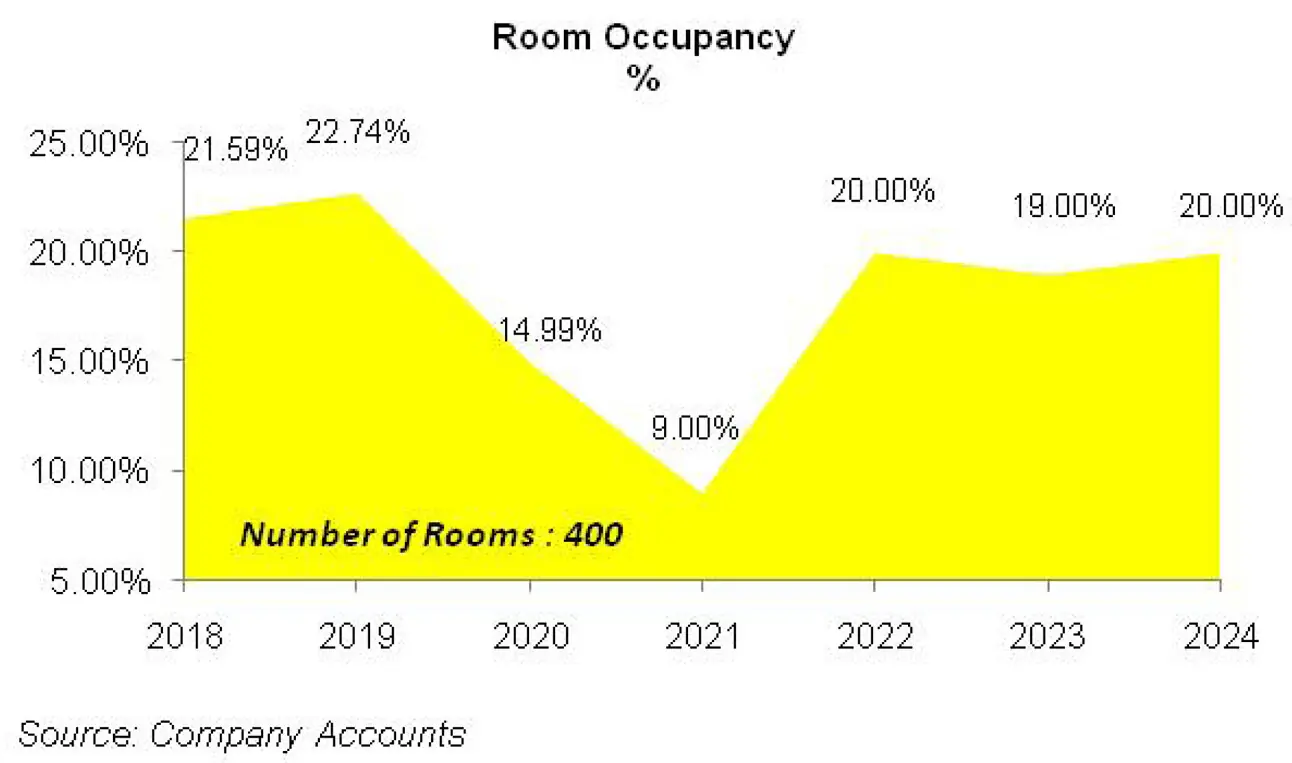

The economic headwinds that came with the global pandemic didn’t fully subside in 2021. The room occupancy of PHDL which slid down to 14.99 percent in 2020 further dropped to 9 percent in 2021. The company nearly halved its workforce from 151 workers in 2020 to 75 workers in 2021.

The topline also shrank by 23.57 percent year-on-year to clock in at Rs. 249.724 million. This resulted in GP margin sinking to 29.94 percent in 2021. Operating expense also dropped by 5.18 percent year-on-year on account of low guest turnover.

Operating loss further magnified to Rs46.089 million in 2021, up 429 percent year-on-year. Finance cost which represented interest on lease assets tapered off by 75.23 percent in 2021. The net loss for 2021 stood at Rs47.165 million with loss per share of Rs. 2.62.

PHDL, which had been grappling firstly against the fire incident and then against COVID-19 heaved a sigh of relief in 2022 as its topline grew by 86 percent year-on-year to clock in at Rs.464.552 million.

Room occupancy grew to 20 percent as the signs of global pandemic began to fade and the hotel and tourism industry picked up.

Cost of sales increased by 40.71 percent in 2022 due to market driven increase in salaries coupled with elevated heat, light and power charges. GP margin grew to 47 percent in 2022 with 192 percent rise in gross profit.

As the company made capital investments in air-conditioning, equipments and restaurants for the improvement of its services, operating expenses mounted by 30.35 percent year-on-year in 2022. The company posted operating profit worth Rs. 60.624 million in 2022 with OP margin of 13 percent.

Finance cost continued to diminish during the year and PHDL was able to post net profit of Rs. 47.817 million with EPS of Rs.2.66 and NP margin of 10.29 percent. This was the highest bottomline as well as operating margin and net margin seen by the company since 2017.

In 2023, PHDL’s net sales improved by 20.34 percent year-on-year to clock in at Rs.559.042 million. Room occupancy slightly fell to 19 percent in 2023, however, room revenue rose owing to price rationalization to make up for the higher cost. Food & beverages revenue and other services revenue (convention center, health, laundry, telephone etc) also buttressd topline growth in 2023.

Heat, light & power charges continued to be the major component of cost. In the wake of heightened energy tariff, cost of sales mounted by 28.25 percent in 2023. This translated into 11.42 percent growth in gross profit with GP margin falling down to 43.52 percent.

Operating expense surged by 18.50 percent in 2023 due to higher payroll expense as well as repair & maintenance charges paid during the year. Number of employees which stood intact at 75 for the past two years grew to 105 in 2023.

Other income enhanced by a massive 3529.11 percent in 2023 as prior year liability of WWF worth Rs.4.416 million was written back during the year.

Operating profit grew by 2.15 percent in 2023 to clock in at Rs.61.927 million with OP margin clocking in at 10.85 percent. While PHDL didn’t incur any finance cost in 2023, it registered other expense of Rs.3.12 million on account of provisioning done for WWF and ECL.

PHDL posted net profit of Rs.44.129 million in 2023, down 7.71 percent year-on-year. EPS stood at Rs.2.45 and NP margin fell to 7.89 percent in 2023.

While there was no respite in economic and political instability in 2024, PHDL posted 30.32 percent year-on-year rise in its net revenue which clocked in at Rs.728.524 million. This mainly comprised of room revenue which improved by 36.66 percent and food & beverages revenue which strengthened by 30.40 percent.

Cost of sales grew by 19.51 percent in 2024 due to high inflation, increased customer traffic and heightened energy tariff. However, the company passed on the impact of cost hike to its customers which resulted in 44.34 percent healthier gross profit recorded in 2024 with GP margin rising up to 48.20 percent.

Operating expense grew by 17.17 percent in 2024 due to higher payroll expense, utility expense as well as legal & professional charges incurred during the year.

Number of employees grew from 106 in 2023 to 114 in 2024. Other income grew by a massive 3170 percent in 2024 due to hefty profit recognized on bank accounts. Operating profit grew by 415.84 percent in 2024 with OP margin clocking in at 43.85 percent.

No finance cost was incurred during the year, however other charges mounted by 595.19 percent in 2024 on the back of provisioning done for WWF, ECL and lost inventory.

Net profit stood at Rs.446.877 million in 2024, up 912.66 percent year-on-year. This culminated into EPS of Rs.24.83 and NP margin of 61.34 percent in 2024.

During the year, PHDL entered into a sale agreement with SIUTTrust for the sale of hotel building along with all the furniture, fixtures, equipments, fittings and construction for a total of Rs.14.5 billion.

Recent Performance (9MFY25)

In July 2024, PHDL received full payment of Rs.14.5 billion from SIUT Trust for the sale of its building and property and closed its operations on July 19, 2024. 90 percent of the sale proceeds was paid as an interim cash dividend for FY25 @ 7250 percent (Rs.725 per share).

PHDL also paid Rs.850 million as advance income tax from the balance amount of 10 percent and the remaining amount was kept for the settlement of current and future liabilities. The company had no other line of business and the only source of income was interest income on its retained funds.

During 9MFY25, PHDL’s net revenue fell by 86.60 percent to clock in at Rs.78.266 million. Gross profit also tapered off by 91.90 percent with GP margin clocking in at 30.15 percent in 9MFY25 versus GP margin of 49.89 percent recorded during the same period last year.

The company incurred administrative expense of Rs.84.26 million in 9MFY25, down 47.19 percent year-on-year. This included legal & professional charges, utility expense as well as remuneration of directors and other key resources which the company will continue to incur until all the residual proceeds are distributed to the shareholders after the payment of outstanding taxes and other dues.

Other income multiplied by 130.59 percent in 9MFY25 seemingly due to higher income from financial assets and gain on the sale of fixed assets.

Operating profit deteriorated by 17.82 percent in 9MFY25, however, OP margin surged to 257.97 percent versus OP margin of 42 percent recorded in 9MFY24.

This was due to hefty other income and curtailed expenses. Net profit dwindled by 18.10 percent to clock in at Rs.141.431 million with EPS of Rs.7.86 and NP margin of 180.71 percent. This was against the EPS of Rs.9.59 and NP margin of 29.57 percent registered in 9MFY24.

With over 88 percent of the shares already held by the company’s directors and their relatives, it is easier to attain 90 percent shareholding threshold and carry out successful buy back and delisting of the company from the exchange which is the most likely outcome for the company as per industry insiders.

Comments

Comments are closed for this article.