Haleon Pakistan limited (formerly known as GlaxoSmithKline) was incorporated in Pakistan as a public limited company in 2015.

The principal activity of the company is the manufacturing, marketing and sales of consumer healthcare and over the counter health products. The company is a subsidiary of “Haleon Netherlands B.V.’ while Haleon plc is the ultimate parent company.

Pattern of Shareholding

As of December 31, 2024, HALEON has a total of 117.055 million shares outstanding which are held by 5124 shareholders.

Haleon Netherlands B.V. holds the majority stake of 85.79 percent in the company followed by local general public accounting for 5.80 percent shares of the company. Modarabas & Mutual Funds hold 3.16 percent shares while Insurance companies hold 2.84 percent shares of HALEON. The remaining shares are held by other categories of shareholders.

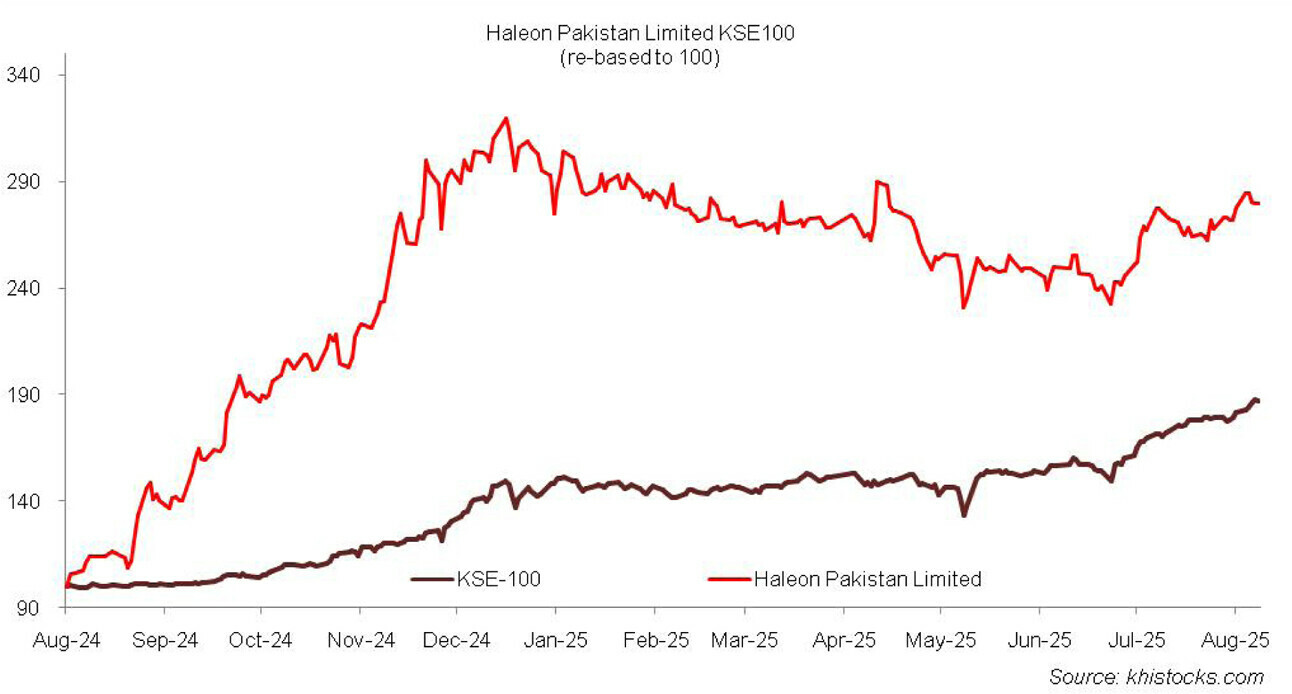

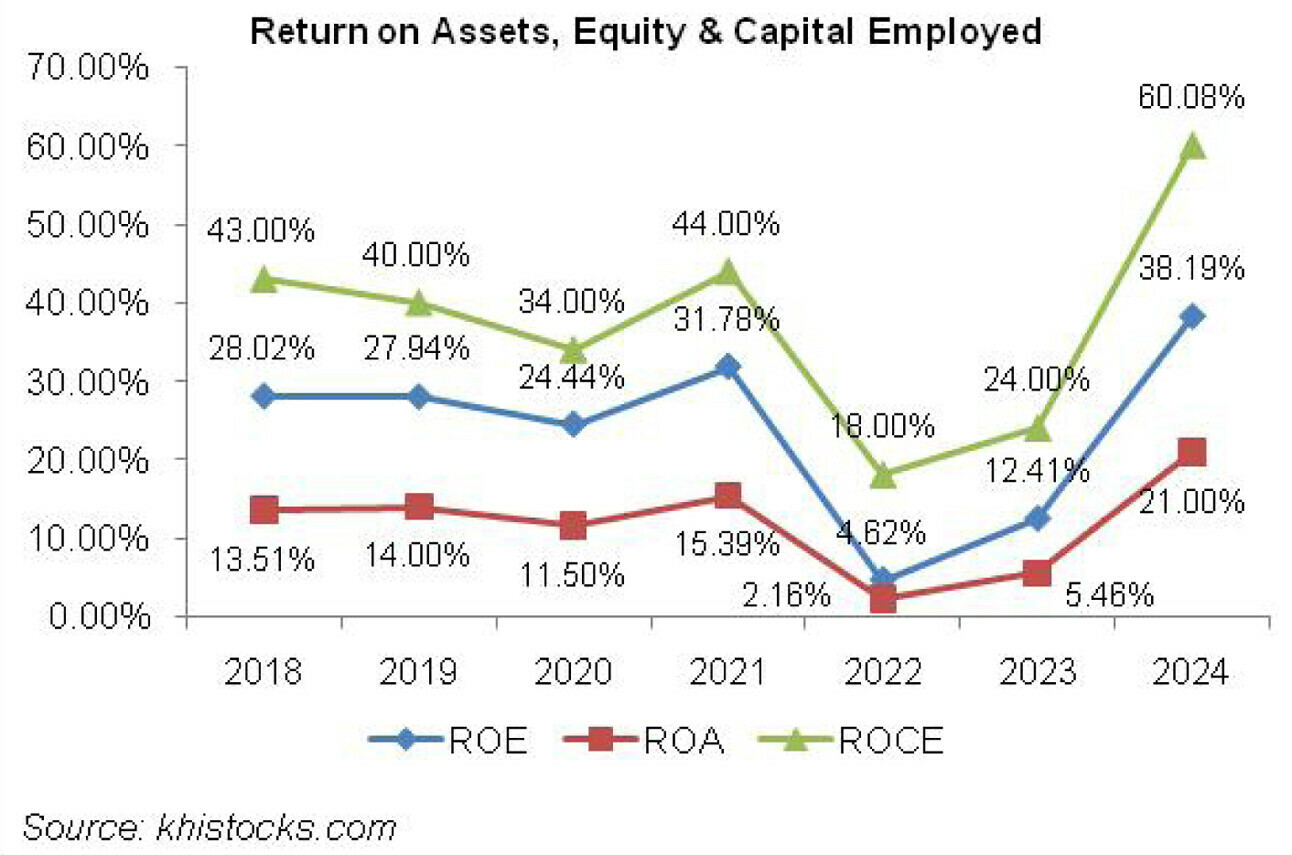

Historical Performance (2019-24)

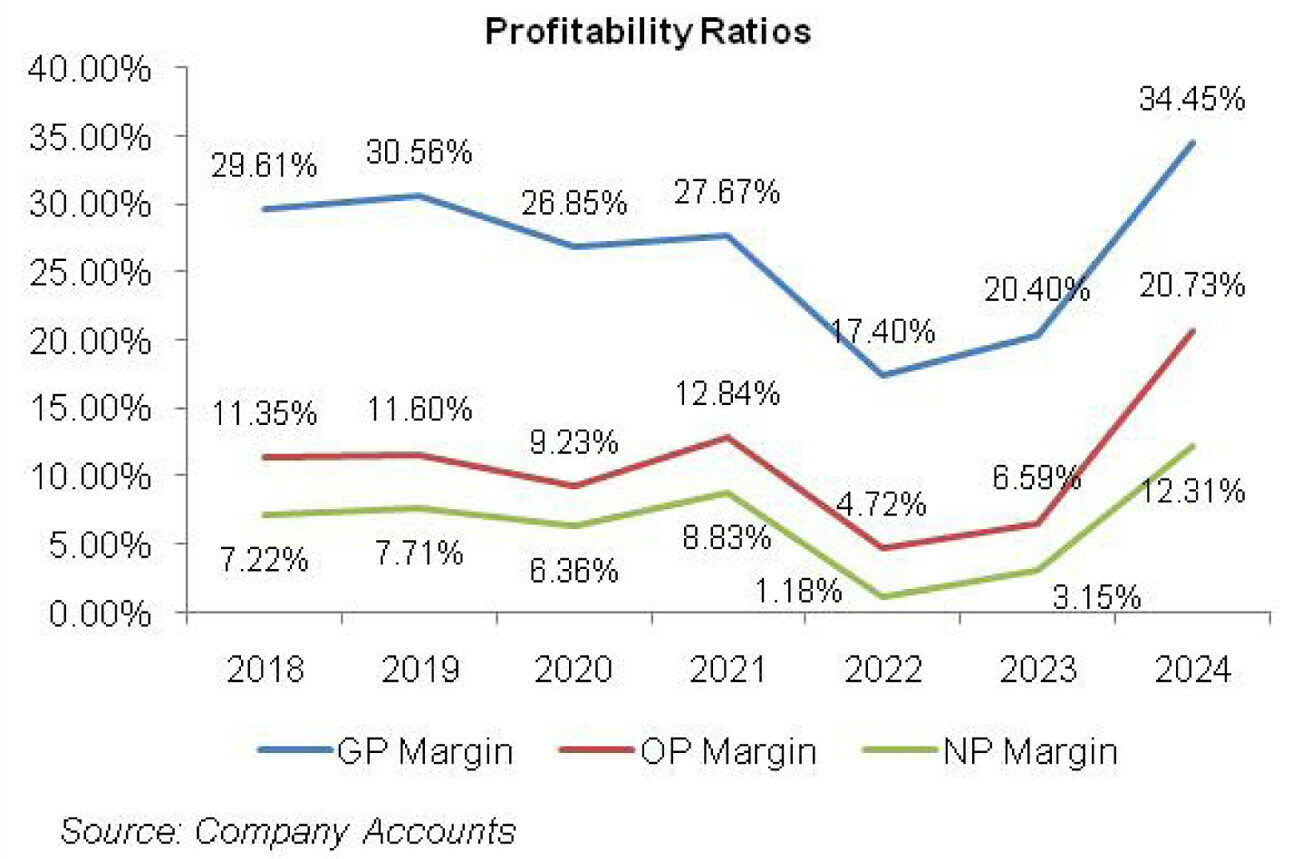

HALEON’s topline rode an upward trajectory over the period under consideration. Conversely, its bottomline posted a decline in 2022. The company’s margins slightly ticked up in 2019 followed by a drop in 2020.

The margins bounced back in 2021, however fell to its lowest level in 2022. HALEON’s margins considerably recovered in the subsequent years and attained their optimum level in 2024. The detailed performance review of the period under consideration is given below.

In 2019, HALEON’s topline grew by 9.69 percent year-on-year to clock in at Rs.16,316.65 million. Except for respiratory health and toll manufacturing business, all other segments, which included oral healthcare, skin health, nutrition & digestive health as well as pain management registered sound growth in 2019.

Despite 10 percent depreciation in the value of local currency, HALEON was able to drive its GP margin from 29.61 percent in 2018 to 30.56 percent in 2019 due to the implementation of price increase twice during the year. Distribution expense multiplied by 12.24 percent in 2019 mainly due to higher budget allocated for advertising & promotion.

Administrative expense slid by 1.88 percent in 2019 primarily due to lower legal & professional charges incurred during the year. Other income fell by 49.30 percent in 2019 due to massive plunge in insurance claim recoveries and income on saving & deposit accounts. Other expense surged by 12.10 percent in 2019 due to increased provisioning for WWF, WPPF and CRF.

Operating profit posted 12 percent year-on-year rise in 2019 with OP margin picking up from 11.35 percent in 2018 to 11.60 percent in 2019. Despite higher discount rate, HALEON was able to cut down its finance cost by 14.81 percent in 2019 by keeping a check on its outstanding borrowings.

Net profit improved by 17 percent to clock in at Rs.1,257.52 million in 2019 with EPS of Rs.10.74 versus EPS of Rs.9.18 recorded in 2018. NP margin ticked up from 7.22 percent in 2018 to 7.71 percent in 2019.

HALEON’s net sales grew by 21.63 percent to clock in at Rs.19,846.11 million in 2020. This was on account of an upsurge in local demand particularly in pain, nutrition and oral healthcare categories. Export sales declined during the year due to COVID-19 related restrictions which created supply chain impediments.

Massive depreciation in the value of Pak Rupee resulted in 28.13 percent year-on-year spike in cost of sales. Gross profit inched up by 6.85 percent in 2020, however, GP margin fell down to 26.85 percent. The decline in GP margin would’ve been much intense, had the mandated price increase not implemented during the year.

Distribution expense escalated by 13.10 percent in 2020 mainly on the back of superior advertising & promotion budget allocated for the year. Administrative expense inched up by 2.26 percent in 2020 on account of higher payroll expense and depreciation which were partially offset by lower legal & professional charges and curtailed travelling & entertainment expense incurred during the year.

Lower gain recorded on the disposal of operating assets coupled with no insurance claim and insurance commission recorded during the year resulted in 34.53 percent decline in other income in 2020. Other expense grew by 8.20 percent in 2020 due to higher provisioning done for WWF, WPPF and CRF. Operating profit ticked down by 3.16 percent in 2020 with OP margin slipping to 9.23 percent.

Finance cost shrank by 69.84 percent in 2020 due to improved cash position and a downtick in discount rate during the year. Net profit grew by a paltry 0.36 percent in 2020 to clock in at Rs.1262.009 million with EPS of Rs.10.78 and NP margin of 6.36 percent.

HALEON recorded 21.75 percent year-on-year rise in its net sales in 2021 which were recorded at Rs.24,163.15 million. The growth was backed by increase in demand in all the segments. The growth in local demand was partially offset by lower exports sales made during the year.

Besides inflationary pressure, the closure of a major Chinese supplier of Paracetamol led to 20.39 percent upsurge in cost of sales in 2021.

The company was able to drive its gross profit up by 25.48 percent in 2021 with GP margin climbing up to 27.67 percent by exercising cost control measures. Relatively stable value of Pak Rupee during the year also helped HALEON attain better GP margin in 2021.

Distribution expense inched up by 8.24 percent in 2021 on account of elevated advertising and freight charges incurred during the year.

Administrative expense surged by 12.19 percent in 2021 on account of higher payroll charges incurred during the year despite rationalized headcount of 459 employees versus 492 employees in 2020.

One-off legal & professional charges incurred during the year also contributed in driving up administrative expense in 2021. 627.58 percent higher other income registered by HALEON in 2021 was on account of improved income on saving accounts and recovery of expenses from group entities. Other expense surged by 58.48 percent in 2021 which was in line with higher statutory charges (WWF, WPPF and CRF).

HALEON posted 69.37 percent improved operating profit in 2021 with OP margin of 12.84. Finance cost spiked by 50.55 percent in 2021 mainly on account of greater exchange loss incurred during the year. Net profit strengthened by 69.12 percent to clock in at Rs.2134.33 million in 2021 with EPS of Rs.18.23 and NP margin of 8.83 percent.

In 2022, HALEON’s topline improved by 13.84 percent to clock in at Rs. 27,507.21 million. This was driven by growth in all the segments. New launches in Paradontax and Sensodyne were well received by the market.

Cost of sales magnified by 30 percent in 2022 due to sharp spike in the price of Paracetamol which was further exacerbated by depreciation of Pak Rupee.

The price adjustment provided by the government couldn’t absorb the massive cost pressure, resulting in 28.42 percent year-on-year decline in gross profit in 2022 with GP margin slipping to its lowest level of 17.40 percent. Distribution expense dipped by 2.78 percent in 2022 due to controlled advertising budget.

Administrative expense mounted by 42 percent in 2022 due to higher payroll expense as number of employees grew to 478. Higher legal & professional charges also contributed in pushing up the administrative expense in 2022.

Other income fell by 5.89 percent in 2022 due to liquidity crunch during the year. Other expense tumbled by 67 percent in 2022 due to lower provisioning done for WWF, WPPF and CRF.

HALEON registered 58.13 percent lower operating profit in 2022 with OP margin of 4.72 percent. Finance cost amplified by 251 percent in 2022 mainly on account of higher exchange losses incurred on the revaluation and resettlement of foreign liabilities.

Net profit dwindled by 84.75 percent to clock in at Rs.325.41 million in 2022 with EPS of Rs.2.78 and NP margin of 1.18 percent – the lowest during the period under consideration.

HALEON’s topline picked up by 14.91 percent in 2023 to clock in at Rs. 31,609.78 million. This was driven by growth in OTC and FMCG portfolio by 29 percent and 13 percent respectively.

Oral care and pain management appeared to be the star categories in 2023. Cost of sales grew by 10.74 percent on account of spike in the prices of major APIs besides inflation and Pak Rupee depreciation. Gross profit magnified by 34.76 percent in 2023 with GP margin climbing up to 20.40 percent. 28.25 percent higher distribution expense incurred in 2023 was the result of higher fuel prices.

Administrative expense also surged by 37.79 percent in 2023 due to higher payroll expense and higher registered office expense incurred during the year. Other income strengthened by 86.13 percent in 2023 on the back of improved liquidity which in turn resulted in higher income from treasury bills and saving accounts. Other expense surged by 95.49 percent in 2023 on the back of higher statutory provisioning.

HALEON posted 60.24 percent higher operating profit in 2023 with OP margin of 6.60 percent. Despite tight monetary stance undertaken by the central bank, the company was able to squeeze its finance cost by 23 percent in 2023 which was the result of relatively lower exchange loss incurred during the year.

Net profit grew by 205.95 percent to clock in at Rs.995.586 million in 2023 with EPS of Rs.8.51 and NP margin of 3.15 percent.

HALEON posted year-on-year growth of 17.70 percent in its topline which clocked in at Rs.37,205.89 million in 2024. The growth was primarily backed by local sales. One of the main reasons behind the improved sales performance was the deregulation of pricing of non-essential medicines by DRAP. This gave enough space to the company to share the onus of cost hike with its consumers.

During the year, the company’s over-the-counter (OTC) portfolio registered 18 percent growth while its FMCG posted 11 percent growth mainly backed by oral health segment. With 99 percent localization of operations, the considerable decline in inflation proved to be a blessing and resulted in 3 percent drop in cost of sales in 2024.

Moreover, the company also did a capital expenditure of Rs.3,186 million during the year to enhance operational efficiency and attain economies of scale which also helped in streamlining cost.

The company augmented the capacity of its flagship brands Panadol and CAC-1000 in 2024. Gross profit strengthened by a staggering 98.78 percent in 2024 with GP margin reaching its optimum level of 34.45 percent.

Distribution expense surged by 13.38 percent in 2024 on account of increased salaries of sales force, elevated advertising and promotion budget as well as higher freight and handling charges incurred during the year.

Market induced rise in salaries resulted in 25.19 percent spike in administrative expense in 2024 despite workforce rationalization from 481 employees in 2023 to 450 employees in 2023.

One notable development during the year was the massive 79.96 percent growth recorded in HALEON’s other income which stood at 2.90 percent of its topline in 2024 versus its share of less than 1 percent at the beginning of the period under consideration. This was the consequence of robust income on saving accounts. The company’s saving deposits almost doubled in 2024 which enabled it to bag enormous interest income despite the onset of monetary easing during the year.

Other expense escalated by a drastic 308 percent in 2024 due to higher provisioning done for WWF, WPPF and CRF.

HALEON recorded 270.49 percent stronger operating profit in 2024 with OP margin climbing up to 20.73 percent. Finance cost fell by 68.12 percent in 2024 due to considerably lower exchange loss. Net profit picked up by 359.85 percent to clock in at Rs.4,578.247 million in 2024. This translated into EPS of Rs.39.11 and NP margin of 12.31 percent in 2024.

Recent Performance (1QCY25)

HALEON kicked off 2025 on a robust note with 26.10 percent growth recorded in its topline in 1QCY25. The company’s topline clocked in at Rs.10,029.84 million in 1QCY25. OTC sales boosted by 32 percent during the period while FMCG sales registered 11 percent improvement.

During 1QCY25, HALEON launched the renowned multivitamin brand “Centrum” in Pakistan and also shipped the first consignment of this brand to Kenya. With the installation of solar power project, the operational efficiency further improved and resulted in 56.84 percent enhancement in the company’s gross profitability in 1QCY25 with GP margin clocking in at 34.20 percent versus GP margin of 27.50 percent recorded in 1QCY24.

Distribution expense surged by 13.86 percent in 1QCY25 primarily on the back of increased sales promotion activities undertaken during the year. Higher payroll expense seemingly on the back of workforce enhancement appears to have driven the administrative expense up by 11.87 percent in 1QCY25. With substantial liquidity available as cash & cash equivalents, HALEON was able to drive its other income up by 25.58 percent in 1QCY25.

Higher provisioning for WWF, WPPF and CRF resulted in 94.78 percent spike in other expense in 1QCY25. HALEON recorded 93 percent superior operating profit in 1QCY25 with OP margin clocking in at 21.68 percent versus OP margin of 14.16 percent posted during the same period last year. Finance cost mounted by 46.22 percent in 1QCY25 probably due to exchange loss on its export sales.

Net profit multiplied by 107.55 percent in 1QCY25 to clock in at Rs.1347.596 million with EPS of Rs.11.51 versus EPS of Rs.5.55 recorded in 1QCY24. NP margin also improved from 8.16 percent in 1QCY24 to 13.44 percent in 1QCY25.

Future Outlook

The company is constantly expanding its production lines, tapping new markets and introducing new products. These measures will not only control its cost but will also ensure the company’s enhanced presence in the local and export markets.

Comments

Comments are closed for this article.