Pakistan Oilfields Limited (PSX: POL) had a slower FY25, with earnings dragged by softer oil prices, volume curtailments, and a spike in exploration spend.

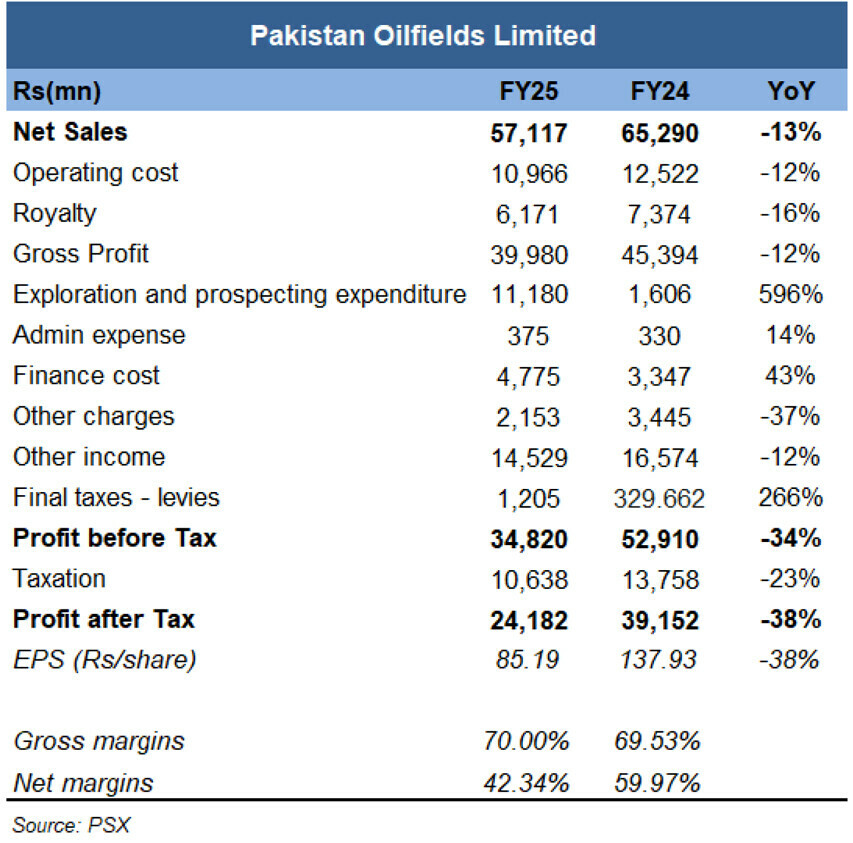

Profit after tax fell 38 percent year-on-year, even as gross margins stayed broadly resilient, highlighting how below-the-line items—chiefly exploration and lower treasury income—drove most of the damage.

Net sales declined 13 percent year-on-year on weaker realized oil prices and modest volume pressure; gross margin for FY25 was 70percent, while the net margin compressed to 42.3 percent from ~60 percent last year.

POL’s operations in FY25 were hit by a surplus of gas in the country’s network, which forced buyers to take less gas from its key fields in the Tal and Adhi blocks. With these curtailments cutting production and global oil prices averaging lower than last year, the company’s quarterly revenues stayed under pressure.4QFY25 sales were down 18 percent year-on-year, reflecting double-digit declines in both oil and gas output and weaker realized prices.

The biggest swing factor was exploration. POL booked Rs11 billion of exploration and prospecting expenses in FY25—about 6–7 times the prior year—largely due to a dry well recognized early in the year and higher seismic/geological spend across operated blocks.

Finance costs rose and other income fell as market yields eased, further weighing on the bottom line. Despite these headwinds, operating costs for the full year declined, helping keep the gross margin intact.

The E&P company announced a final dividend of Rs50 per share, taking the FY25 payout to Rs75 per share—still a double-digit yield even after the earnings drop.

For FY26, three things will matter most for POL: first, how quickly the gas supply issues ease so production from fields can return to normal; second, where oil prices and the rupee-dollar rate go, since both directly affect revenues; and third, the results from upcoming exploration after the big spending in FY25.

While analysts flag high reliance on the Tal and Adhi fields as risks, there could be upside from reserve updates other fields. With earnings now at a lower base, any boost in production or prices—along with steady exploration costs and normal taxes—could lift profits, and the strong dividend should continue to support investor returns.

Comments

Comments are closed for this article.