Saif Power Limited (PSX: SPWL) was incorporated in Pakistan as a public limited company in 2004. The company commenced its operations in 2010. The company owns, operates and maintains a combined cycle power plant with nameplate capacity of 225 MW. It is engaged in generating and selling electricity to Central Power Purchasing Agency Guarantee Limited (CPPA-G).

Pattern of Shareholding

As of June 30, 2024, SPWL has a total of 386.472 million shares outstanding which are held by 7180 shareholders. Directors, CEO, their spouse and minor children have the majority stake of 28.07 percent in the company followed by associated companies holding 23 percent shares of SPWL.

Local general public accounts for 16.36 percent shares of the company while Banks, DFIs and NBFIs hold 10.22 percent shares. Around 2.12 percent of SPWL’s shares are held by foreign general public and 1.41 percent by insurance companies. The remaining shares are held by other categories of shareholders.

Financial Performance (2019-24)

Barring 2021 and 2022, SPWL’s topline has posted year-on-year decline over the period under consideration. Its bottomline rose only in 2019 followed by an unabated descending journey. SPWL’s bottomline hit its lowest level in 2024.

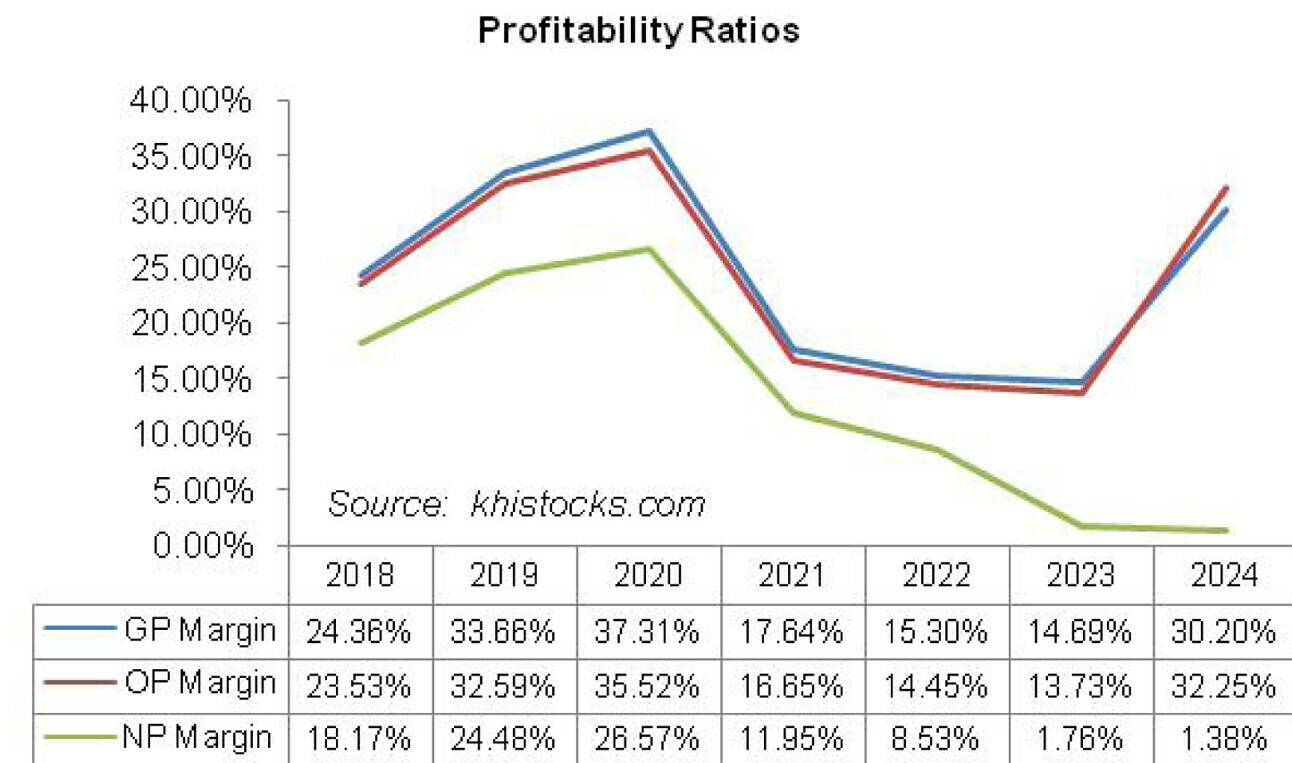

The company’s margins which climbed up until 2020 plunged thereafter to register their weakest level in 2023. In 2024, gross and operating margins significantly recovered while net margin continued to slide. The detailed performance review of the period under consideration is given below.

In 2019, SPWL’s topline tumbled by 10.66 percent year-on-year to clock in at Rs.14,910.38 million.

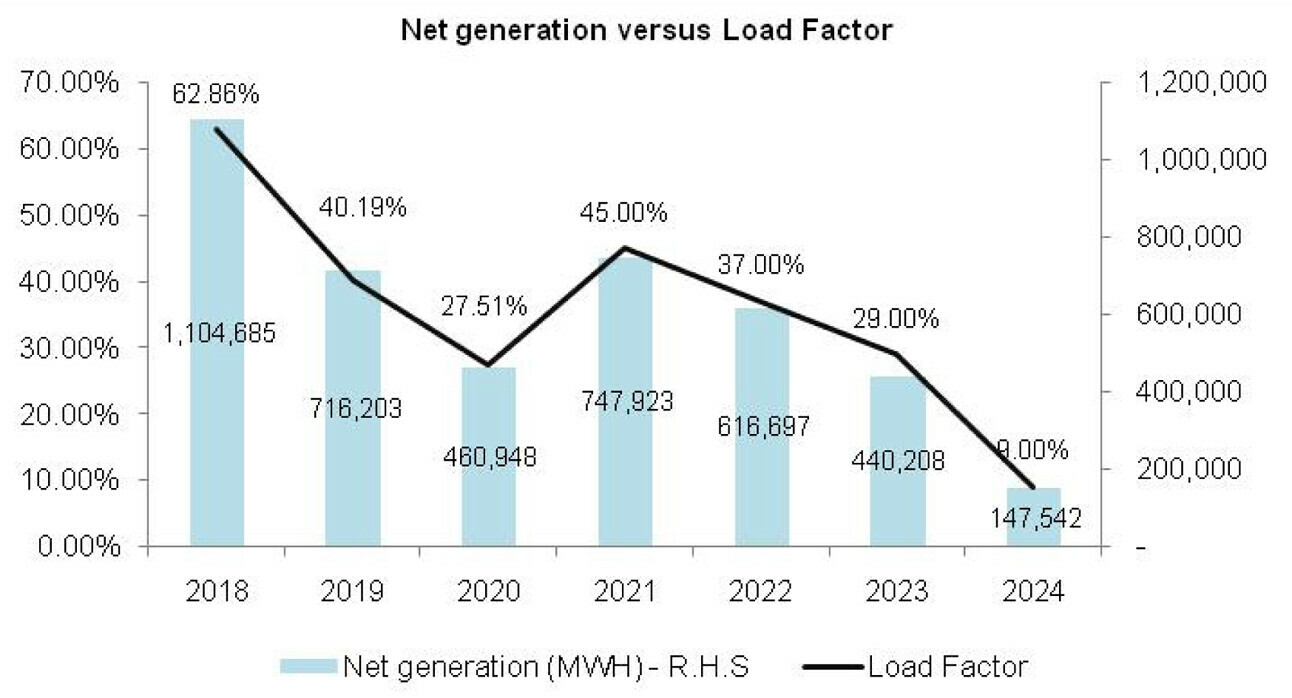

The company’s net generation fell by 35.17 percent during the year with load factor clocking in at 40.19 percent versus load factor of 62.86 percent recorded in the previous year (see the graph “Net generation versus Load Factor”). This was due to reduced requirement by the power purchaser. During the year, the plant was fully operated on RLNG fuel as against last year where 2,769 MWh were generated on HSD fuel.

Cost of sales dropped by 21.65 percent in 2019 due to lower raw material consumed in line with curtailed generation. Furthermore, insurance recovery of Rs.652.97 million also contributed in driving the cost down.

Gross profit improved by 23.45 percent in 2019 with GP margin rising up from 24.4 percent in 2018 to 33.7 percent in 2019. Administrative expense multiplied by 15.69 percent in 2019 mainly on account of higher payroll expense, depreciation on right-of-use assets, legal & professional charges as well as fee & subscription charges incurred during the year. While return on investment considerably fell during the year, hefty profit on deposit accounts sustained other income in 2019.

Operating profit grew by 23.71 percent in 2019 with OP margin clocking in at 32.6 percent versus OP margin of 23.5 percent recorded in 2018. Finance cost surged by 35.15 percent in 2019 on account of monetary tightening.

The company considerably reduced its debt profile during the year. Net profit enhanced by 20.34 percent in 2019 to clock in at Rs.3,649.95 million with EPS of Rs.9.44 versus EPS of Rs.7.85 recorded in the previous year. NP margin also boasted significant improvement to clock in at 24.48 percent in 2019 versus NP margin of 18.2 percent posted in 2018.

In 2020, SPWL recorded 40.14 percent year-on-year decline in its net sales which clocked in at Rs.8,925.18 million. The outbreak of COVID-19 shattered the economic and social activity in the country, resulting in sluggish power demand. Load factor stooped to its lowest level of 27.51 percent to-date in 2020 with net generation clocking in at 460,948 MWh, down 35.64 percent year-on-year. Out of the total electricity generated during the year, 5691 MWh were generated using HSD fuel.

Cost of sales nosedived by 43.44 percent in 2020 on account of lower cost and quantity of raw material consumed during the year due to COVID-19. Considerable cut in depreciation expense and impairment loss also pushed the cost down in 2020.

Gross profit shrank by 33.64 percent in 2020, however, GP margin ticked up to its peak level of 37.31 percent. Administrative expense largely stayed intact in 2020. Other income slid by 28.43 percent in 2020 on the back of paltry return from financial assets. Operating profit nosedived by 34.75 percent in 2020 with OP margin clocking in at 35.5 percent. Finance cost slumped by 33.93 percent in 2020 due to monetary easing in the later part of the fiscal year.

While the company completely paid off its long-term debt in March 2020, it had to raise additional working capital loan to sustain its operations amid surging circular debt and rising receivables due from the power purchaser. Net profit contracted by 35 percent to clock in at Rs.2371.50 million in 2020 with EPS of Rs.6.14 and NP margin of 26.57 percent.

In 2021, SPWL’s topline boasted a staggering 83.69 percent year-on-year rise to clock in at Rs.16,394.34 million. With the resumption of economic activity, SPWL’s load factor considerably improved to 45 percent in 2020. This resulted in 62.26 percent growth in the company’s power generation which stood at 747,923 MWh in 2021, 87090 MWh of which were generated on HSD fuel in 2021.

Cost of sales multiplied by 141.33 percent in 2021 due to increase in the quantity and cost of raw materials consumed during the year as well as elevated operational & maintenance charges incurred during the year. This slashed the gross profit by 13.17 percent in 2021 with GP margin drastically falling down to 17.64 percent.

Administrative expense posted an uptick on 2.13 percent in 2021. Momentous spike of 63.89 percent in payroll expense was largely offset by lower legal & professional and consultancy charges as well as low rent, rate and taxes paid during the year. Other income picked up by 102.17 percent in 2021 due to robust return on investment and deposit accounts as well as higher insurance claim.

During the year, SPWL invested Rs.1000 million in TDRs and Rs.15.664 million in T-bills. Besides, the company also purchased additional 440,441 fully paid ordinary shares of Saif Cement limited (SCL) which increased its holding in SCL to 96.39 percent. The company’s liquidity position also greatly improved in 2021 as it received the first installment of 40 percent of its receivables as per agreement with GoP and CPPA-G.

Operating profit slumped by 13.90 percent in 2021 with OP margin slipping to 16.65 percent. Finance cost dropped by 3.46 percent in 2021 due to monetary easing. Net profit dwindled by 17.41 percent year-on-year to clock in at Rs.1958.52 million in 2021 with EPS of Rs.5.07 and NP margin of 11.95 percent.

In 2022, SPWL recorded 39.5 percent year-on-year growth in its net sales which clocked in at Rs.22,869.65 million. While load factor dropped to 37 percent in 2022, resulting in net generation of 616,697 MWh, down 17.55 percent year-on-year, topline growth was on account of higher fuel charges. 23,705 MWh were generated on HSD fuel while the remaining 592,993 MWh were generated on gas in 2022.

Cost of sales spiked by 43.46 percent in 2022 due to exorbitant fuel charges, operation & maintenance charges, insurance expense as well as depreciation expense incurred during the year. Gross profit grew by 21 percent in 2022, however, GP margin dipped to 15.30 percent.

Administrative expense surged by 25.93 percent in 2022 due to elevated payroll expense coupled with an upsurge in legal & professional charges due to its ongoing pending issues with SNGPL.

Other income boasted 310.20 percent year-on-year enhancement due to hefty profits earned on deposits and investments coupled with gain on sale of fixed assets recorded during the year.

Operating profit mounted by 21.03 percent in 2022 with OP margin of 14.45 percent. 75.47 percent escalation in finance cost in 2022 was the result of monetary tightening as well as momentous rise in the utilization of working capital lines. This resulted in 0.40 percent decline in SPWL’s net profit in 2022 which clocked in at Rs.1950.66 million with EPS of Rs.5.05 and NP margin of 8.53 percent.

In 2023, SPWL’s topline slid by 16.73 percent to clock in at Rs.19,043.73 million. Load factor dropped to 29 percent in 2023 with net generation clocking in at its lowest level of 440,208 MWh, down 28.62 percent year-on-year.

The plant completely operated on gas in 2023. Curtailed generation was the result of lower demand by the power purchaser coupled with the overhaul and maintenance of steam turbine during the year after almost six years.

Unlike previous years, where overhaul expenses were charges annually based on operating hours of plant in a particular year, the revision of accounting standards implied that the additional expense charged in the previous years was reversed and incurred in the current year. This translated into momentous rise in operational & maintenance charges in 2023.

Gross profit slid by 20 percent in 2023 with GP margin registering its lowest level of 14.69 percent. Administrative expense ticked up by 5.67 percent in 2023 due to higher payroll expense which was somewhat offset by lower legal & professional charges incurred during the year.

Other income multiplied by 188.83 percent in 2023 due to higher return on investment followed by gain on disposal of property, plant & equipment and profit of bank deposits earned during the year.

Operating profit ticked down by 20.84 percent in 2023 with OP margin clocking in at 13.73 percent. Finance cost surged by 68.45 percent in 2023 due to monetary tightening while the company’s outstanding short-term loans slid during the year. Net profit dipped by 82.77 percent to clock in at Rs.336.10 million in 2023 with EPS of Rs.0.87 and NP margin of 1.76 percent.

SPWL’s net sales dipped by 49.22 percent to clock in at Rs.9,670.86 million. Net generation dropped by 66.48 percent to clock in at its lowest level of 147,542 MwH. Load factor also stood at its lowest level of 9 percent in 2024. During the year, the government of Pakistan constituted a task force to make amendments in the power purchase agreement, implementation agreement and tariff.

SPWL, along with other IPPs underwent several rounds of negotiations with the task force and the result was the conversion of existing tariff to “Hybrid Take & Pay Model”. As per the amendment agreement, the power purchaser also made full payment of overdue claims of Rs.5207 million.

Decline in operational & maintenance charges as per revised accounting standards coupled with lower power generation resulted in 58.45 percent lower cost of sales in 2024. This translated into GP margin of 30.20 percent in 2024.

Gross profit ticked up by only 4.39 percent in 2024. Administrative expense spiked by 50.88 percent in 2024 mainly driven by higher payroll expense. This was due to inflationary pressure as well expansion of workforce from 40 employees in 2023 to 62 employees in 2024.

Other income progressed by 1353.73 percent in 2024 mainly on account of hefty dividend income received from Saif Cement Limited (subsidiary company) as well as exchange gain recognized during the year. During the year, the sales agreement of Saif Cement Limited was realized and cash was distributed to the shareholder in respect of their shareholding ratios.

Operating profit grew by 19.26 percent in 2024 with OP margin clocking in at 32.25 percent. Despite unprecedented level of discount rate, the company was able to cut down its finance cost by 43.12 percent in 2024 as the company squeezed its short-term borrowings. This enabled SPWL to record net profit of Rs.133.34 million in 2024, down 60.33 percent year-on-year. EPS stood at Rs.0.35 in 2024. SPWL registered NP margin of 1.38 percent in 2024.

Recent Performance (9MFY25)

During the 9-month of the ongoing fiscal year, SPWL registered 40 percent year-on-year growth in its topline which clocked in at Rs.1490.34 million. Dispatch level was recorded at 4.89 percent in 9MFY25 versus dispatch level of 0.13 percent recorded during the same period last year. The company has not used the depreciation allowance it created in its books for the past 14 years and is actually a cash profit for the company.

Cost of sales mounted by 98.86 percent during 9MFY25 due to higher generation and increased cost of raw materials. This resulted in 36.98 percent diminution recorded in the gross profit of SPWL in 9MFY25 with GP margin clocking in at 19.50 percent versus GP margin of 43.32 percent recorded during 9MFY24.

Administrative expense escalated by 14.67 percent in 9MFY25 primarily due to higher payroll expense. Other income strengthened by 64.51 percent during the period under review seemingly due to higher interest income on loan to subsidiary companies and investment of Rs.5207 million received from CPPA-G in the T-bills bearing return of 11.90 percent.

Operating profit dwindled by 44.62 percent during 9MFY25 with OP margin falling down to 14.80 percent versus OP margin of 37.41 percent recorded in 9MFY24. Monetary easing resulted in 53.43 percent decline in finance cost in 9MFY25. This enabled SPWL to record net profit of Rs.36.07 million in 9MFY25, up 1584.59 percent year-on-year. This translated into EPS of Rs.0.09 in 9MFY25 versus EPS of Rs.0.01 registered in 9MFY24. NP margin significantly improved from 0.20 percent in 9MFY24 to 2.42 percent in 9MFY25.

Future Outlook

Seasonal increase in demand is expected during the ongoing quarter. Improvement in the macroeconomic indicators also hints towards the enhancement in power demand. The government is also discouraging captive power plants and incentivizing the industries to return to the national grid by increasing the gas prices to the CPPs by up to 23 percent and imposing a grid levy.

Furthermore, industries are also directed to ensure dual connectivity. While this is a good men for the power companies, other industries may suffer as they have substantially invested in CPPs and switching back to the grid will require further investment.

Comments

Comments are closed for this article.