Ittehad Chemicals Limited (PSX: ICL) was incorporated in Pakistan in September 1991 to purchase the assets of Ittehad Chemicals and Ittehad Pesticides under a scheme of arrangement. The company was privatized in 1995. The company manufactures and sells caustic soda and other chemicals e.g. liquid chlorine, hydrochloric acid, calcium chloride, etc.

Pattern of Shareholding

As of June 30, 2024, ICL has 100 million shares outstanding which are held by 1090 shareholders. The local general public has a majority stake of 65.82 percent in the company followed by Directors, CEO, their spouses, and minor children holding 21.4 percent shares. Joint stock companies account for 11.02 percent of ICL’s shares while Modarabas & Mutual funds hold 1.05 percent of shares. The remaining shares are held by other categories of shareholders.

Financial Performance (2019-24)

The topline and bottom line of ICL present a contrasting journey over the period under consideration. While the topline has posted growth in all the years under consideration, the bottom line registered growth only in two years i.e. in 2021 and 2023. ICL’s margins have also been oscillating over the period. In 2019, gross and operating margins considerably picked up while net margins plunged. This was followed by the erosion of all the margins in 2020. In 2021, ICL witnessed a sound recovery in its margins which was significantly reversed in 2022. In 2023, the margins strengthened yet again followed by a downtick in 2024 (see the graph of profitability ratios). The detailed performance review of the period under consideration is given below.

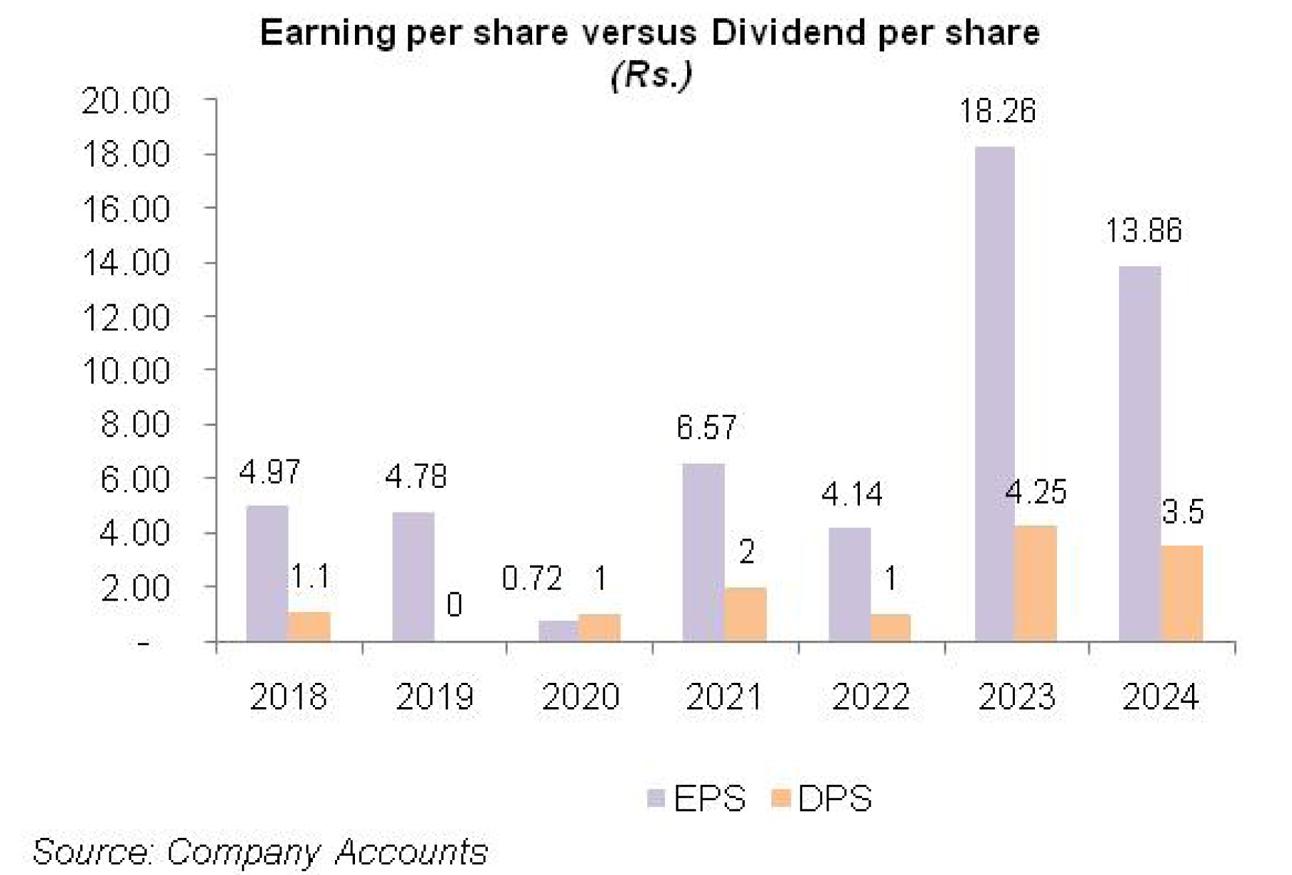

In 2019, ICL’s topline grew by 15.70 percent year-on-year to clock in at Rs.6644.38 million on the back of high demand as well as an upward revision of prices. During the year, ICL diversified its product line by commissioning the LABSA (Linear alkyl benzene sulphonic acid) plant with a capacity of 24000 M tons. The company also took cost control measures and shifted its production to its state-of-the-art power plant IEM Plant-3 which commenced its operation at the onset of 2019. This bore fruit and resulted in a 43.19 percent year-on-year rise in ICL’s gross profit in 2019. GP margin also rose from 16.77 percent in 2018 to 20.75 percent in 2019. Distribution expense ticked up by 13.85 percent in 2019 on account of higher freight charges. ICL hired additional resources for its new plant during the year which took its workforce tally up to 682 in 2019 versus 673 in 2018. This resulted in higher payroll expenses which drove up administrative expenses by 15.10 percent in 2019. Loss on decommissioned fixed assets and increased profit-related provisioning translated into 29.84 percent higher other expenses in 2019. Conversely, other income slumped by 51.8 percent in 2019 on the back of lower scrap sales. ICL was able to register a 49.90 percent rise in its operating profit in 2019 with OP margin picking up from 8.78 percent in 2018 to 11.38 percent in 2019. Finance costs mounted by 65.71 percent in 2019 due to higher discount rates and increased borrowings for BMR as well as working capital requirements. ICL’s gearing ratio rose from 40 percent in 2018 to 45 percent in 2019. Higher finance cost resulted in a 2.51 percent year-on-year drop in ICL’s net profit which clocked in at Rs.405.05 million in 2019 with EPS of Rs.4.78 versus EPS of Rs.4.91 in 2018. NP margin also nosedived from 7.23 percent in 2018 to 6.10 percent in 2019.

The bottomline of ICL took the hardest hit in 2020 where it plunged by 85 percent year-on-year despite sizeable 33.29 percent year-on-year growth in net sales which stood at Rs.8856.60 million. The growth in sales was the result of the instigation of ICL’s LABSA plant operations which added to its sales volume. However, the high cost of sales due to increased electricity and gas prices couldn’t let the company enjoy a higher gross profit. ICL’s gross profit plunged by 14.31 percent year-on-year, culminating in a thinner GP margin of 13.34 percent in 2020. Distribution expenses hiked by 21.61 percent year-on-year in 2020 on account of increased freight charges. Administrative expenses inched up by a marginal 4.52 in 2020 percent on account of inflationary pressure while a number of employees went down to 649 in 2020. Significantly lower profit-related provisioning pushed down other expenses by 21.13 percent in 2020 which was absorbed by 29 percent higher other income recorded by ICL in 2020. Improved other income was the result of higher scrap sales made during the year. ICL’s operating profit tumbled by 34.39 percent in 2020 with OP margin slipping to 5.60 percent. Finance cost was another stumbling block which grew by 87.81 percent year-on-year in 2020 owing to high discount rates in the first three quarters of the year. Finance costs would have soaked up the entire operating profit of the company and resulted in a negative bottom line had the fair value gain on investment property not lent the helping hand by growing by over 1200 percent in 2020. ICL posted a net profit of Rs60.8 million in 2020, down 85 percent year-on-year, resulting in EPS of Rs.0.72 and NP margin of 0.69 percent.

2021 was the most fortunate year for ICL in terms of bottom-line growth. During the year, the company acquired the entire equity of its group company Ittehad Salt Processing (Private) Limited. ICL’s net sales clocked in at Rs.11,123.79 million in 2021 after achieving year-on-year growth of 25.59 percent. LABSA sales greatly contributed to the topline growth amid sluggish demand from other segments as economies began to regain their lost momentum after COVID-19. Moreover, upward revision in prices as well as cost control measures implemented by the company resulted in 59.57 percent higher gross profit recorded by ICL in 2021. GP margin also climbed up to 16.95 percent in 2021. 15 percent higher distribution expense incurred in 2021 was the consequence of higher freight and marketing service charges. During the year, ICL streamlined its workforce to 621 employees, resulting in lower payroll expenses. This drove down the administrative expense by 3.71 percent in 2021. Higher profit-related provisioning, loss on sale of fixed assets as well as foreign exchange loss resulted in 77.56 percent higher other expense in 2021. Other income grew by a marginal 9.35 percent in 2021 due to a gain on discounting of GIDC payable, recovery of doubtful debts, and gain on sale and disposal of assets. ICL posted a 120.35 percent year-on-year escalation in its operating profit in 2021 with OP margin mounting to 9.83 percent. Finance cost, which had been suppressing ICL’s bottom line, was contained in 2021 owing to low discount rates and curtailed long-term borrowings. ICL’s gearing ratio tumbled from 41 percent in 2020 to 35 percent in 2021. Then fair value gain on investment property also grew significantly, providing impetus to the bottom line which grew by 980.21 percent year-on-year to clock in at Rs.656.77 million with EPS of Rs.6.57 and NP margin of 5.9 percent in 2021.

In 2022, the company’s topline posted robust year-on-year growth of 40.97 percent to clock in at Rs.15,681.37 million. During the year, the company enhanced the capacity of its LABSA plant to 70,000 metric tons per annum. This greatly improved the sales volume of the company which is evident in its topline growth. During the year, the company also improved its fuel efficiency by upgrading its power plant engines. Gross profit posted year-on-year growth of 9.5 percent despite high inflation and elevated cost of raw materials. However, due to low consumption in the market, the company couldn’t pass on the impact of cost hikes to its consumers. Consequently, the GP margin dropped to 13.17 percent in 2022. In 2022, the company’s export sales improved by 52 percent over the last year, especially in the UAE region. This resulted in higher freight charges which pushed up the distribution cost by 39.79 percent year-on-year. Administrative expense also escalated by 22.22 percent in 2022 on account of inflationary pressure although ICL undertook workforce rationalization to bring it down to 617 employees in 2022. Other expenses declined by 24.80 percent in 2022 due to no loss incurred on the sale of fixed assets, lower exchange loss, and lower profit-related provisioning. Other income also dropped by 34.93 percent in 2022 as unlike the previous year, the company didn’t book any gain on the sale of fixed assets, discounting of GIDC payable as well as recovery of doubtful debts during the year. This shrank the operating profit by 9.17 percent year-on-year in 2022 which culminated into an OP margin of 6.33 percent. Finance cost soared by 46.40 percent in 2022 owing to a high discount rate coupled with increased long-term financing. The gearing ratio, once again, climbed up to 40 percent in 2022. Fair value gain on investment property also contracted by 10 percent during the year. The bottom line weakened by 36.88 percent year-on-year to clock in at Rs. 414.54 million with EPS of Rs.4.15 and NP margin of 2.64 percent in 2022.

2023 stands out from other years as ICL recorded the highest topline growth of 54.76 percent during the year to clock in at Rs.24,268.28 million. Better margins on export sales and superior energy management resulted in 141.86 percent higher gross profit recorded by ICL in 2023 with GP margin rising up to 20.58 percent. Robust export sales also resulted in a 101.92 percent surge in distribution expense on account of higher freight charges. Higher prices of POL products also played a role in driving up the freight charges in 2023. Administrative expenses built up by 22.35 percent in 2023 on account of higher payroll charges as ICL grew its workforce to 682 employees in 2023. Other expenses mounted by 142.53 percent in 2023 due to heightened provisioning for WWF and WPPF. However, a sharp rise in other expenses was counterbalanced by 263.86 percent higher other income which was primarily the effect of higher foreign exchange gain. Operating profit magnified by 211.11 percent in 2023 with OP margin reaching its highest level of 12.73 percent. Finance cost swelled by 70.37 percent in 2023 due to an unprecedented level of discount rate although ICL was able to bring its gearing ratio down to 26 percent in 2023. The imposition of a 10 percent super tax was also a cause of concern for the company in 2022. However, a 51.85 percent higher fair value gain on investment property gave considerable support to the bottom line which posted a 340.54 percent year-on-year improvement in 2023 to clock in at Rs.1826.196 million with EPS of Rs.18.26 and NP margin of 7.53 percent – the highest among all the years under consideration.

In 2024, ICL’s topline inched up by a marginal 0.19 percent year-on-year to clock in at Rs.24,314.59 million due to sluggish economic activity and lackluster demand. Conversely, the cost of sales grew by 1.18 percent in 2024 due to elevated energy tariffs. Fuel cost accounts for more than half of the company’s cost of sales. This resulted in a 3.65 percent downtick in the company’s gross profit in 2024 with GP margin falling down to 19.79 percent. To control its energy cost, a wholly owned subsidiary of ICL, M/s ICL Power (Private) Limited was incorporated during the year to establish a biomass power plant. Distribution expenses dropped by 16.91 percent in 2024 on account of lower freight charges. Conversely, administrative expenses hiked by 19.94 percent in 2024 on account of higher payroll expenses on account of inflation as well as workforce enhancement from 682 employees in 2023 to 712 employees in 2024. Other expenses mounted by 15.87 percent in 2024 due to loss incurred on the sale of scrap. Other income eroded by 46.87 percent in 2024 due to a drastic decline in exchange gain. This was due to stability in the value of local currency coupled with considerably lower export sales. ICL recorded a 3.26 percent downtick in its operating profit in 2024 with OP margin clocking in at 12.29 percent. Finance costs surged by 30 percent in 2024 owing to higher discount rates and increased working capital-related borrowing obtained during the year. Net profit tapered off by 24.12 percent to clock in at Rs.1385.75 million in 2024 with EPS of Rs.13.86 and NP margin of 5.7 percent.

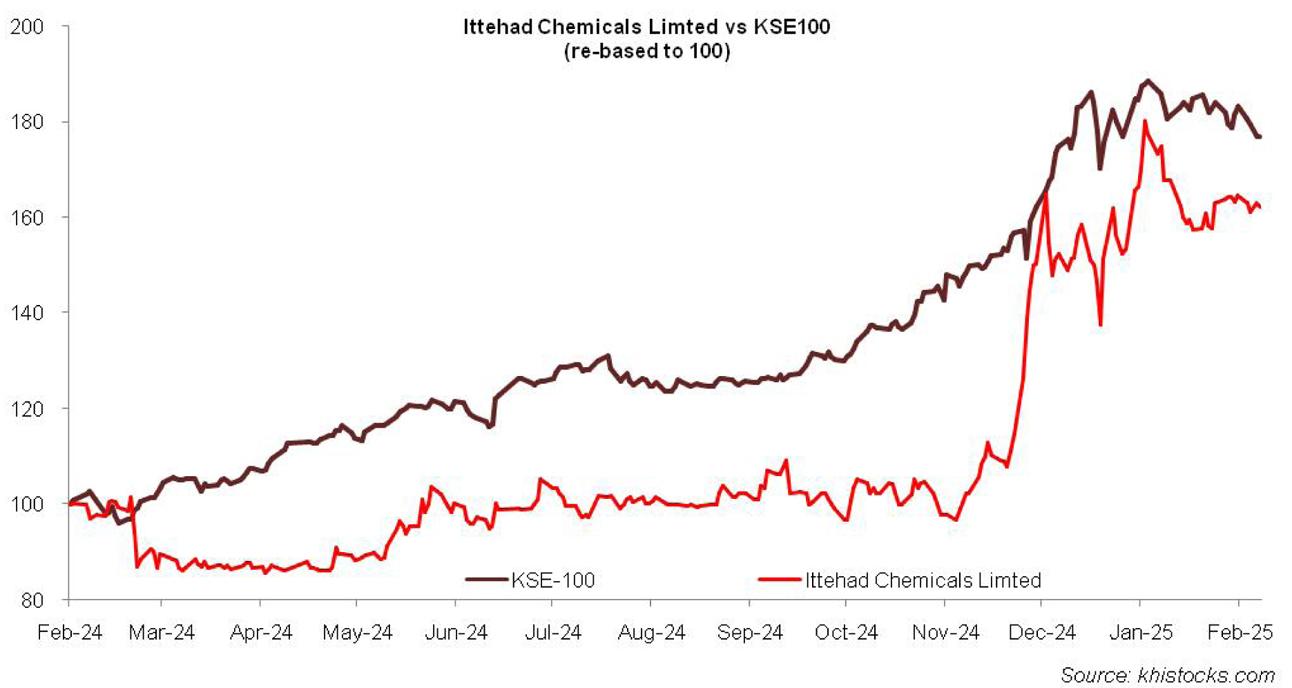

Recent Performance (1HFY25)

During the 1HFY25, ICL’s topline grew by 7.96 percent to clock in at Rs.13,143.26 million. This was due to a phased recovery in macroeconomic indicators which resulted in demand recovery in the second quarter of FY25. However, a 9.41 percent higher cost of sales due to elevated energy tariff resulted in a marginal 2.16 percent uptick in gross profit in 1HFY25 with GP margin clocking in at 18.89 percent versus GP margin of 19.97 percent recorded in 1HFY24. Selling & distribution expenses mounted by 37.73 percent in 1HFY25 due to higher freight charges incurred during the year. Administrative expenses also escalated by 11.70 percent in 1HFY25 owing to inflationary pressure. Other expenses dropped by 14.56 percent in 1HFY25 probably on account of lower profit-related provisioning and lesser loss incurred on the sale of scrap vis-à-vis last year. Other income also tumbled by 52.32 percent during the period under consideration possibly due to thinner exchange gain. ICL recorded a 13.94 percent downtick in its operating profit in 1HFY25 with OP margin recorded at 10.94 percent versus OP margin of 13.72 percent recorded during the same period last year. Finance cost ticked down by 10.60 percent in 1HFY25 due to a lower discount rate. Net profit plunged by 11.51 percent to clock in at Rs.614.396 million in 1HFY25. This translated into EPS of Rs.6.14 in 1HFY25 versus EPS of Rs.6.94 recorded in 1HFY24. NP margin also slumped from 5.7 percent in 1HFY24 to 4.67 percent in 1HFY25.

Future Outlook

ICL is making concerted efforts to strengthen its footprint in the global market amid weak demand in the home market. The company is also investing in multiple projects such as the establishment of the biomass power plant, installation of a flaker plant, addition of an electrolyzer as well as expansion of a calcium chloride plant. All these projects once commissioned will provide immense operational efficiency to ICL and reduce its cost. This will make the company’s products more competitive in the local and global markets and will greatly improve its margins and profitability.

Comments

Comments are closed for this article.