In December 2024, the State Bank of Pakistan in its monetary policy statement had taken heart from “a noticeable improvement” in key industrial sectors such as textile, tobacco, food and beverages, automobiles, and petroleum sectors. January 2025 monetary policy statement had to drop petroleum from the list of noticeably improved industrial sectorsas it went red. It is likely the next statement would also drop food from the ever-shrinking list, as December LSM numbers are out and they read a grim tale.

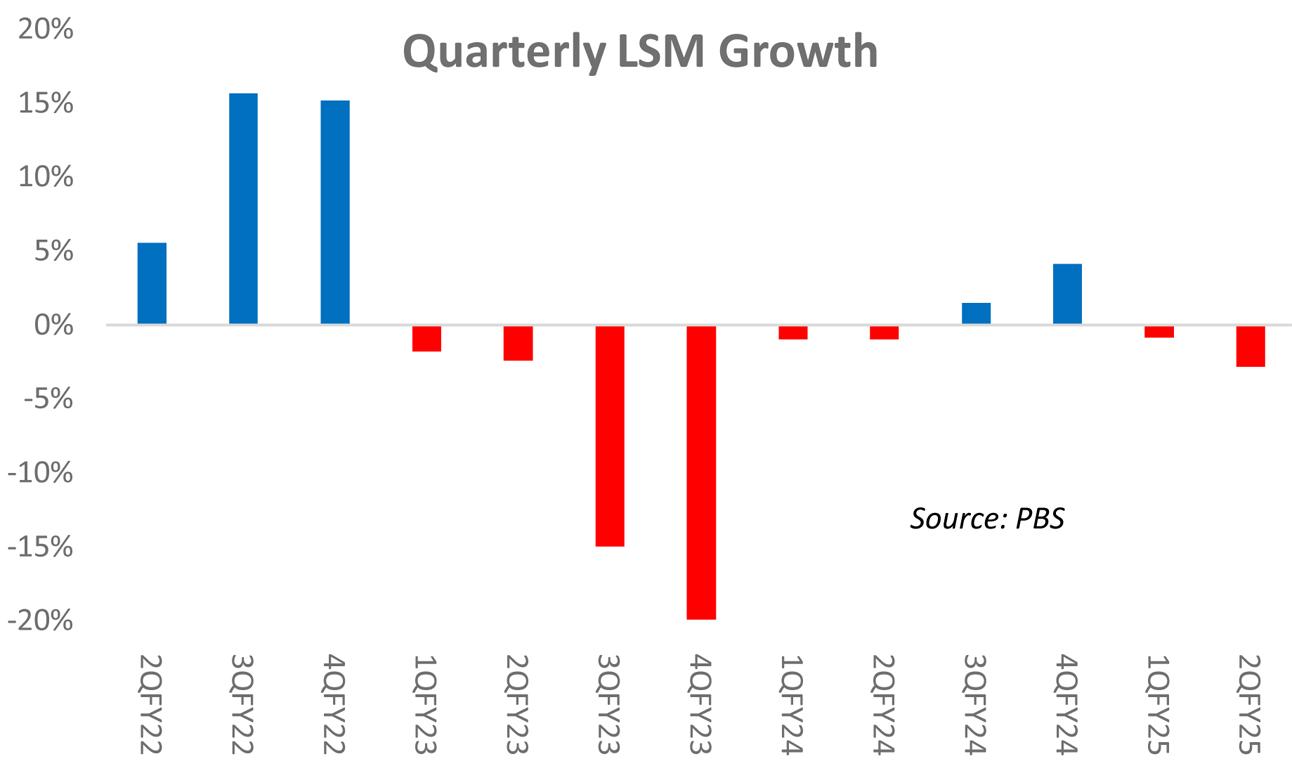

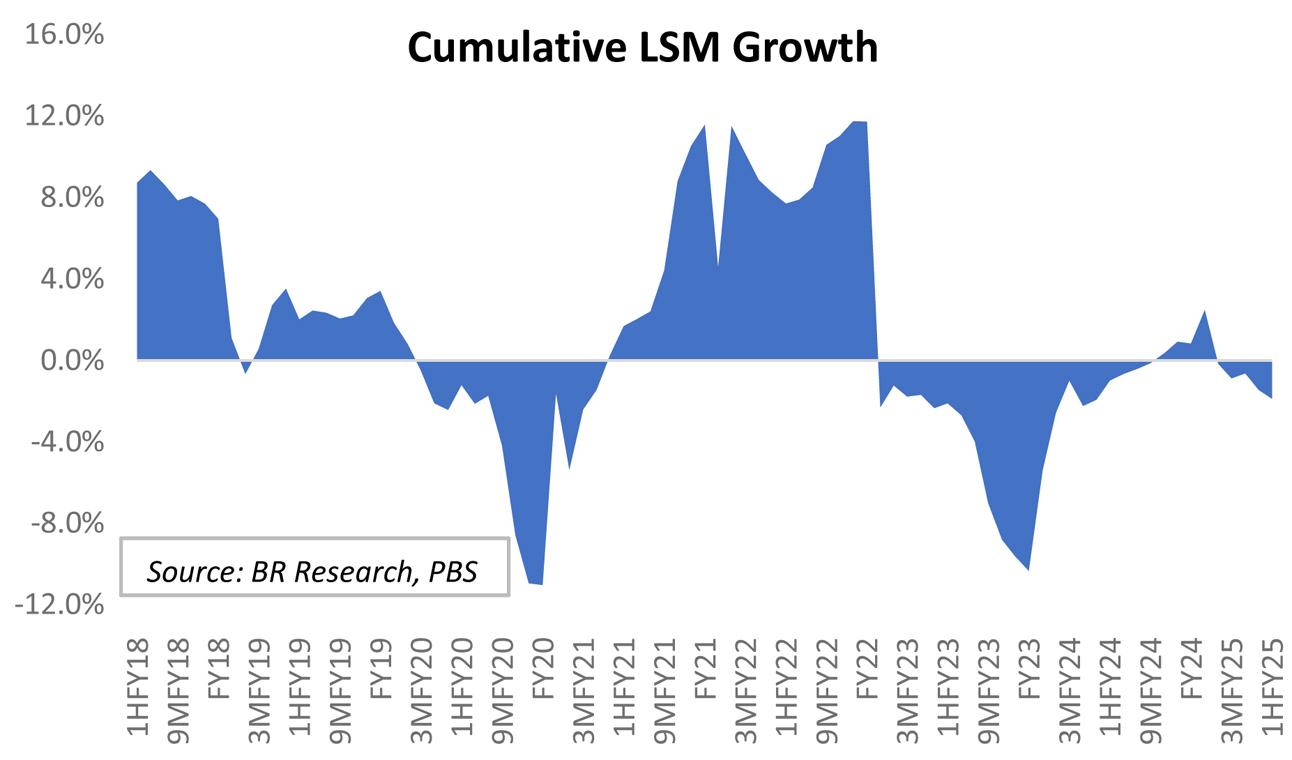

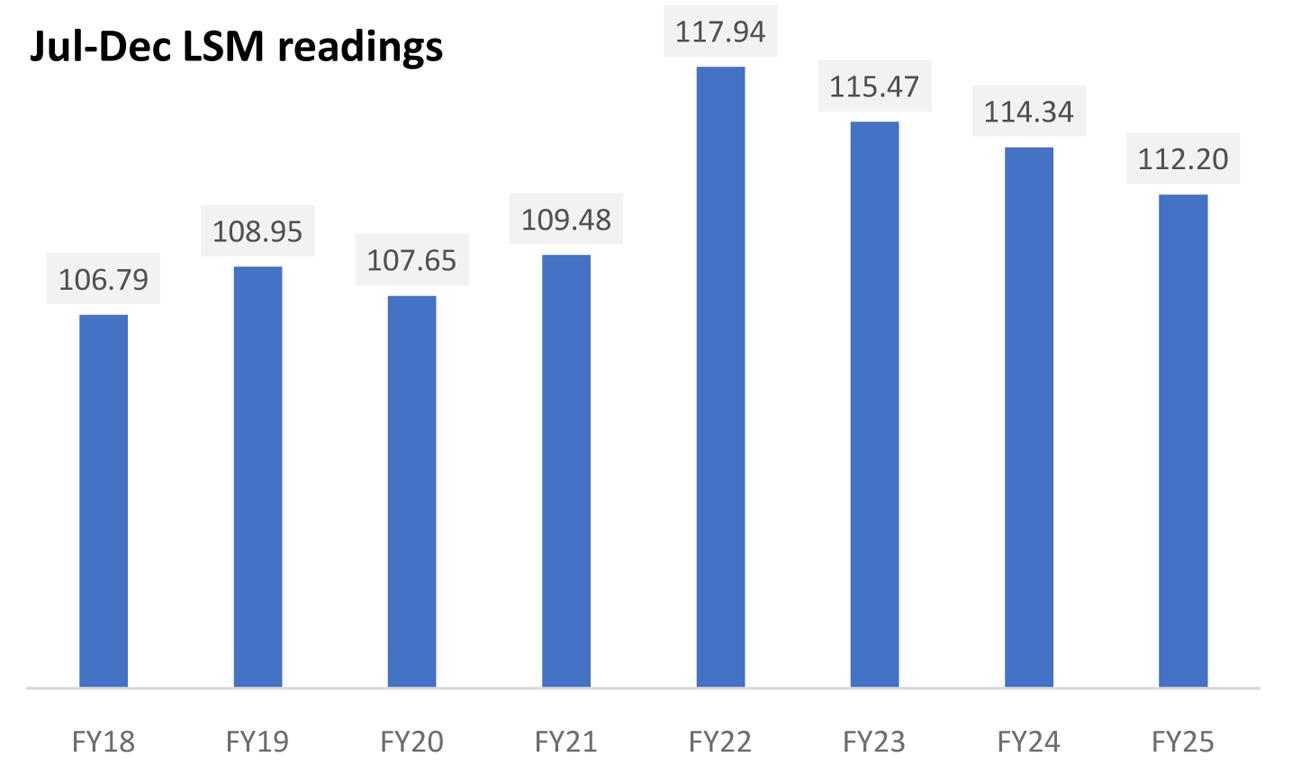

With December 2024 LSM growth going down another 3.7 percent year-on-year, the cumulative growth for 1HFY25 tanked to negative 1.87 percent –the lowest in 14 months. December 2024 and 1HFY25 LSM readings are the lowest since FY21. The second quarter LSM growth at negative 2.8 percent marks the eighth quarterly LSM contraction in the last ten quarters, as the rebound of 2HFY24 is proving short-lived. Mind you, both 1QFY25 and 2QFY25 contractions are already coming off a very low base – and this is the third consecutive year of the second quarter returning negative growth.

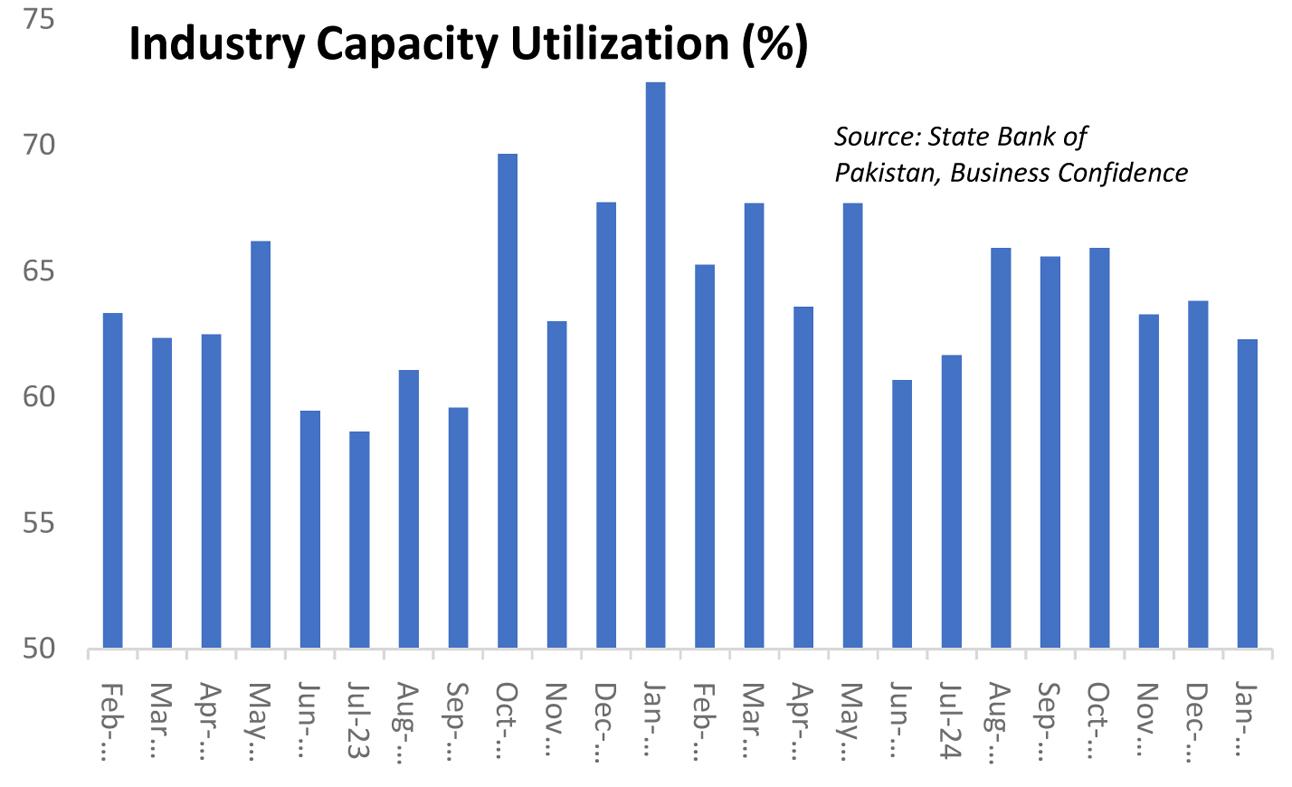

The diffusion index stayed over 50 for the fourth consecutive month, with 12 of the 22 industrial sectors showing negative growth. Nine sectors still show an index value lower than 100 at the start of the base period in FY16. All this while, the industry capacity utilization as tracked by the State Bank of Pakistan’s Business Confidence Survey is reeling at 62 percent for January 2025 – 10 percentage points shy of the capacity utilization achieved a year ago away. The record-breaking credit spree in 2QFY25 has not yet translated into higher capacity utilization, just yet. Remains to be seen if 3Q will be any different.

Wearing apparel remains the largest contributor in terms of impact accounting for nearly half of the positive growth during 1HFY25. With January export numbers out, readymade garment export quantity growth has now moderated to single digits, down from the high teens by the end of 1QFY25. The second biggest contribution comes from the strong recovery in the automobile sector. The low base is likely to keep the growth coming, and January’s car production numbers at nearly 11,000 is the highest since December 2022. Cheaper consumer loans and stable prices will likely keep the momentum up, going forward.

Growth in the heavyweight textile sector demonstrated by cotton yarn and cotton cloth continues to be checked at 2 percent year-on-year – and that too is coming off a very low base. The textile sector’s index value at 84 in December 2024 marked the 27th straight month of sub-100 value, having peaked at 115 in April 2022. The largest industrial sector employer has seen employment levels go down drastically of late, with employment in the Punjab textile industry down 20 percent from the peak of 15 years ago, according to data by the Punjab Bureau of Statistics.

Construction-related industry remains heavily under pressure, and the interest rate reversal so far has not done the trick, as cement, glass, steel, paints, and wood are all down from near-past historical averages. White goods have not shown any signs of significant reversal either, as evidenced by the sluggish performance of electrical equipment from refrigerators to TV sets and from ACs to electric fans.

Comments

Comments are closed for this article.