At-Tahur Limited (PSX: PREMA) was incorporated in Pakistan as a public limited company in 2007. The company is engaged in the production and processing of milk and dairy products.

Pattern of Shareholding

As of June 30, 2024, PREMA has a total of 218.639 million shares outstanding which are held by 2380 shareholders. Directors, CEO, their spouses, and minor children are the major shareholders of the company with a stake of 72.57 percent followed by the local general public holding 16.25 percent shares of PREMA. Modarabas and Mutual funds account for 5.01 percent shares of PREMA while joint stock companies hold 2.89 percent shares of the company. Around 1.54 percent of the company’s shares are held by insurance companies. The remaining shares are held by other categories of shareholders.

Financial Performance (2019-24)

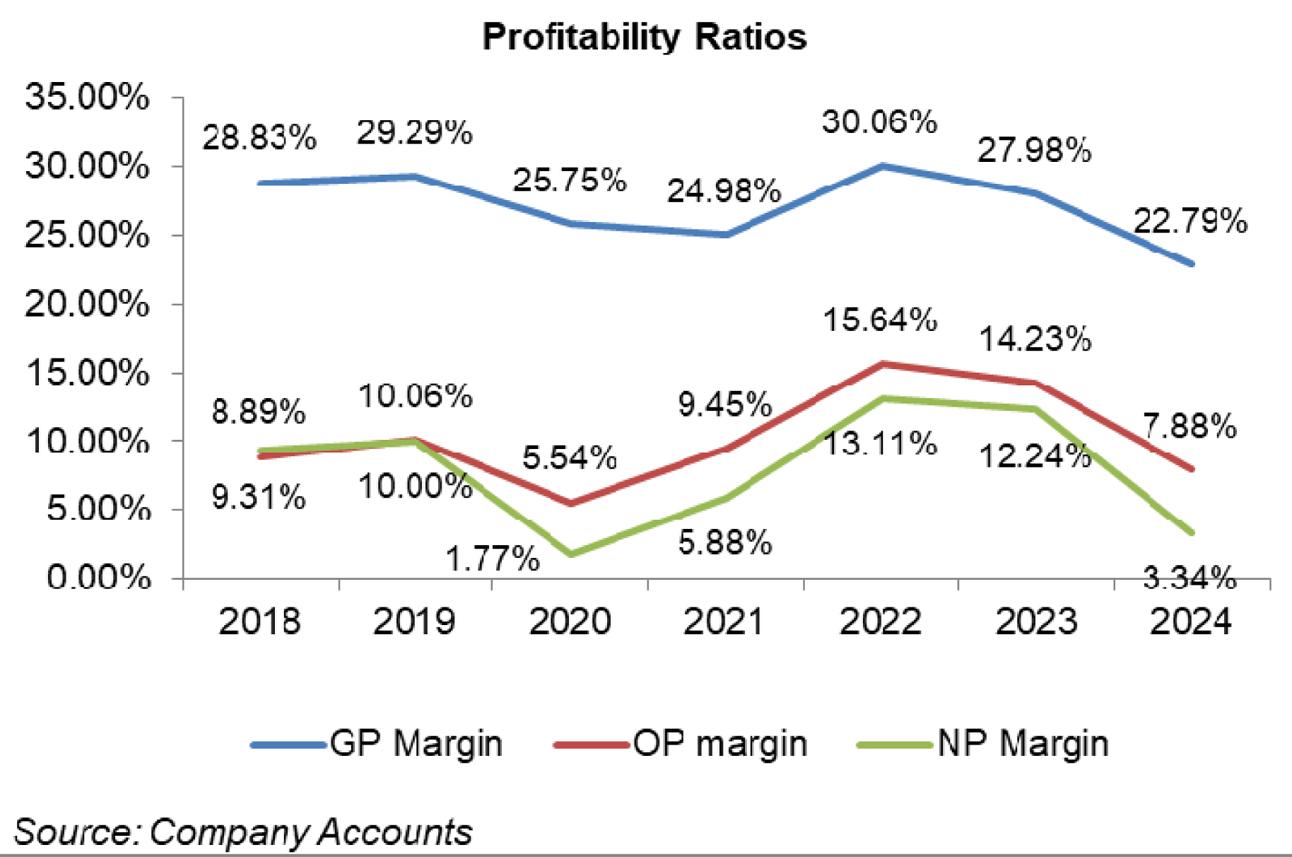

PREMA’s net sales have been expanding over the period under consideration. Conversely, its bottom line plunged in 2020 and 2024. PREMA’s margins which posted an uptick in 2019 drastically fell in 2020. In 2021, gross margin continued to shrink while operating and net margins considerably progressed. PREMA’s margins boasted their optimum level in 2022 followed by a plunge in the succeeding years. The detailed performance review of the period under consideration is given below.

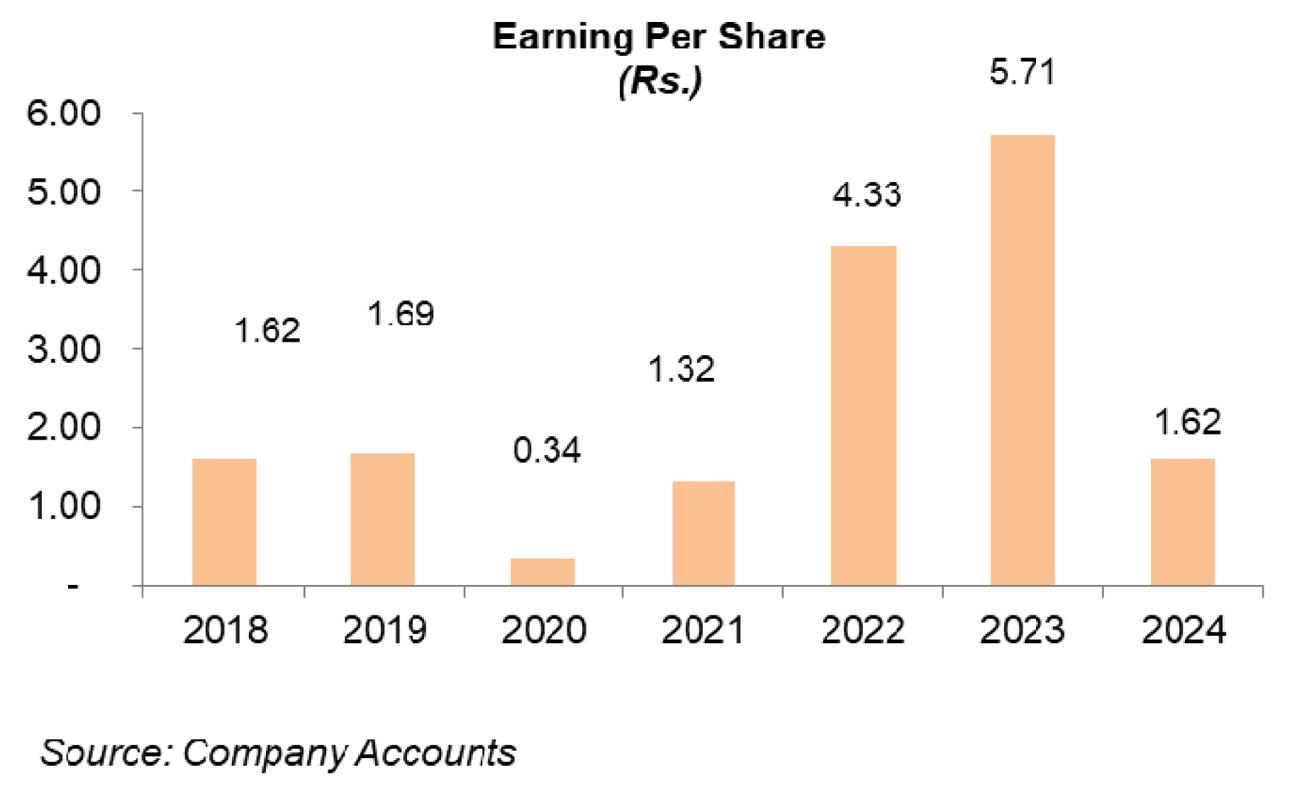

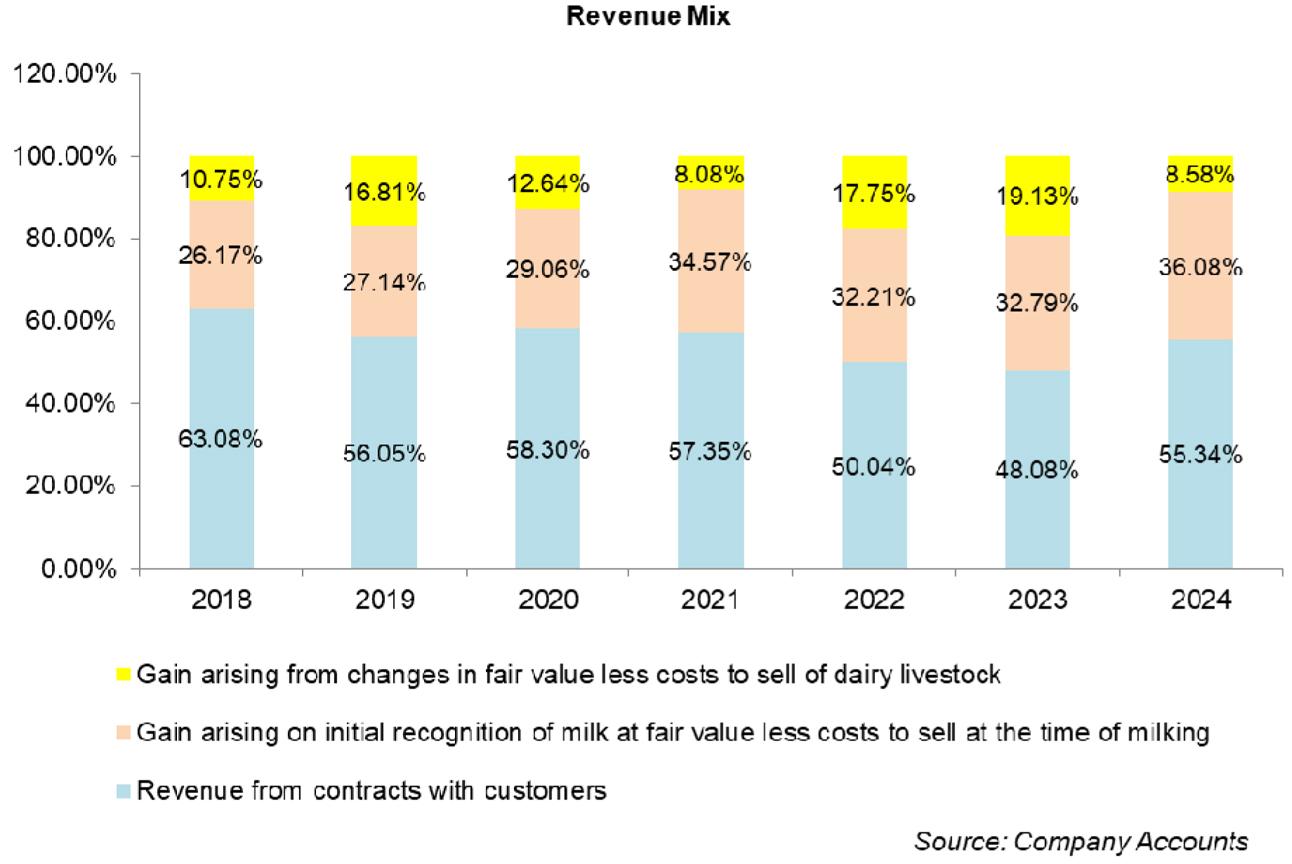

In 2019, PREMA’s total revenue jumped up by 41.4 percent year-on-year with the gain to sell dairy livestock boasting the highest rise of 121.13 percent, however, its contribution in the total revenue basket stays under 20 percent in all the years under consideration. Revenue from contracts with customers increased by 25.64 percent year-on-year while gain arising from initial recognition of milk grew by 46.62 percent year-on-year during 2019. The company sold 12.29 million liters of milk in 2019 as against 9.49 million liters sold in 2018. The increased volume is attributable to the launch of new products during the year. Gross profit grew by 43.69 percent year-on-year in 2019. GP margin also jumped from 28.8 percent in 2018 to 29.3 percent in 2019. Operating expenses increased in line with increased production and capacity utilization. During the year, PREMA inducted new employees which took the tally up to 475 employees from 354 employees in 2018. This particularly drove up the salaries expenses. Vehicles’ running expenses were another major contributor to elevated operating expenses in 2019. Other expenses magnified by 20 percent in 2019 on account of loss on sale of dairy livestock, allowance for ECL and WPPF. Other income dropped by 36.55 percent in 2019 due to the high-base effect as PREMA wrote off the credit balance in 2018 and also recorded amortization of deferred income on sale and lease back in the previous year. Operating profit grew by 60 percent year-on-year in 2019.OP margin enlarged from 8.89 percent in 2018 to 10.06 percent in 2019. Finance cost grew by 143.96 percent in 2019 due to a rise in discount rate coupled with increased borrowings during the year. However, with a debt-to-equity ratio of 6 percent, finance cost isn’t an issue for the company. PREMA’s net profit grew by 52 percent year-on-year in 2019 to clock in at Rs. 270.10 million with an NP margin of 10 percent versus an NP margin of 9.31 percent recorded in 2018. EPS stood at Rs.1.69 in 2019 versus EPS of Rs.1.62 posted in 2018.

In 2020, the total revenue of PREMA magnified by 15 percent year-on-year due to the launch of new products and a change in sales mix. Pak Rupee depreciation also increased the value of PREMA’s export sales. Due to a 20.86 percent year-on-year rise in cost of sales, gross profit could only grow by 1.17 percent in 2020 which pushed the GP margin down to 25.75 percent in 2020. Admin and marketing expenses didn’t show any respite due to the rise in inflation. To meet the rising demand, the company also hired new resources which drove up its workforce to 505 employees in 2020. Other expenses tremendously grew during 2020 due to the death of dairy livestock and loss on the sale of dairy livestock. Other income didn’t compensate either due to lesser profit on bank deposits, lesser sale of scrap, and no common facilities cost charged during the year. Operating profit contracted by 36.6 percent year-on-year in 2020 with OP margin sinking to 5.54 percent. Finance cost grew by 138.83 percent year-on-year in 2020 due to an increase in discount rate during the initial quarters of FY20 coupled with an increase in borrowings particularly running finance. Debt-to-equity ratio slightly increased to 8 percent in 2020. PREMA’s net profit declined by 79.68 percent to clock in at Rs.54.89 million in 2020 with an NP margin of 1.77 percent. EPS drastically dropped to Rs.0.34 in 2020.

In 2021, PREMA’s revenue rebounded by 43.56 percent year-on-year on the heels of a splendid rise in revenue from contracts with customers and gains arising from the initial recognition of milk. Despite a 45 percent year-on-year increase in cost of sales particularly on the back of raw milk and forage consumed during the year, gross profit multiplied by 39.29 percent year-on-year in 2021; however, GP margin ticked down to 24.98 percent. Administrative and selling expenses grew in line with inflation and increase in operations. Except for butter, the capacity utilization of all other segments – pasteurized milk, yogurt, raita, chunky yogurt, and cream cheese significantly improved during the year. This required additional resources resulting in workforce expansion to 570 employees in 2021. Enhanced sales also resulted in hefty vehicle running expenses incurred during the year. Other expenses massively increased due to the loss on the sale of dairy livestock and the death of dairy stock in 2021. WWF and WPPF also increased during the year due to high profitability. Other income grew by 12.19 percent in 2021 due to the reversal of allowance on ECL, amortization of government grant, and gain on termination of lease. Operating profit boasted a stunning growth of 144.72 percent year-on-year in 2021 with an OP margin of 9.45 percent. Finance costs grew by 8.29 percent in 2021 despite a drop in discount rates during the year. This was due to elevated long-term borrowings during the year. PREMA’s debt-to-equity ratio jumped up to 19 percent in 2021. The bottom line posted a staggering growth of 377.85 percent year-on-year in 2021 to clock in at Rs.262.27 million with an NP margin of 5.88 percent and EPS of Rs.1.32.

PREMA’s revenue continued to outshine the previous year’s mark in 2022 with year-on-year growth of 47.19 percent. Gain from the sale of dairy livestock which had been dropping since 2020 posted an incredible growth of 223.19 percent in 2022 with its share in total revenue basket jumping up to 18 percent in 2022 from 8 percent in 2021. This is attributable to local currency depreciation as well as an increase in the prices of herds globally. Cost of sales grew by 37.22 percent year-on-year in 2022, yet healthy revenue growth provided the impetus to gross profit which magnified by 77.11 percent in 2022 with a GP margin of 30 percent. Administrative and selling expenses grew by 32.68 percent and 28.71 percent respectively in 2022 due to increased payroll and vehicle running expenses. Number of employees grew to 695 in 2022 due to tremendous growth in capacity utilization across product categories. Other expenses didn’t show any respite and grew by 52.69 percent in 2022 due to the death of dairy livestock and loss on the sale of dairy livestock. Gain on the sale of fixed assets and amortization of government grants resulted in a 145.85 percent rise in other income in 2022. Operating profit posted 143.59 percent year-on-year growth in 2022 with OP margin climbing up to 15.64 percent. Finance costs kept moving up as the discount rate saw multiple upward revisions in 2022. PREMA’s short-term and long-term borrowings also heightened during the year driving up its debt-to-equity ratio up to 21 percent in 2022. Net profit grew by 228.34 percent year-on-year in 2022 to clock in at Rs.861.14 million with an NP margin of 13.11 percent, the highest mark achieved over the period under consideration. EPS also jumped up to Rs.4.33 in 2022.

In 2023, PREMA’s topline registered staggering year-on-year growth of 55.20 percent on account of successful upward price revision, increased sales volume, product portfolio expansion, gain arising from the sale of dairy livestock, and gain arising from initial recognition of milk. High cost of raw and packaging material, Pak Rupee depreciation as elevated energy cost resulted in 59.82 percent higher cost of sales in 2023. While gross profit enhanced by 44.47 percent in 2023, GP margin ticked down to 27.98 percent. Administrative and selling expenses escalated by 20.48 percent and 54.15 percent respectively in 2023 on the back of high vehicle running expenses as well as payroll expenses. Number of employees mounted to 701 in 2023. 64.29 percent higher other expenses incurred by PREMA in 2023 were the result of higher losses from the death and sale of dairy livestock. Other income grew by 130.39 percent in 2023 on account of higher sales of scrap, sales of operating fixed assets, and amortization of government grants. Operating profit posted a 41.24 percent rise in 2023, however, OP margin ticked down to 14.23 percent. 97 percent higher finance cost registered by PREMA in 2023 was the consequence of the unprecedented level of discount rate while the debt-to-equity ratio plunged to 17 percent. PREMA’s net profit progressed by 44.90 percent in 2023 to clock in at Rs.1247.78 million with EPS of Rs.5.71 and NP margin of 12.24 percent.

In 2024, PREMA posted a marginal uptick of 3.65 percent in its sales. While revenue from contracts with customers and gain arising from initial recognition of milk posted reasonable growth of 19.3 percent and 14 percent respectively during the year, a 53.5 percent plunge in gain arising from the sale of dairy livestock diluted the overall impact. During the year, the valuation of biological assets was considerably affected by the appreciation of the Pak Rupee vis-à-vis the US Dollar. Operating costs mounted by 11.12 percent in 2024, squeezing gross profit by 15.6 percent. GP margin slid to its lowest level of 22.79 percent in 2024. Administrative and selling expenses surged by 11.12 percent and 6 percent respectively in 2024. The main contributors of higher operating expenses were payroll expenses, vehicle running expenses as well as product handling and sales promotion expenses incurred during the year. The company further expanded its workforce to 711 employees in 2024. Loss on the sale of dairy livestock coupled with provisioning done for WWF and WPPF resulted in a 14 percent spike in other expenses in 2024. Conversely, other income plummeted by 46.59 percent in 2024 due to lower sales of scrap and lower gains on the sale of operating fixed assets. PREMA’s operating profit dwindled by 42.61 percent in 2024 with OP margin falling down to 7.88 percent. Finance costs surged by 25 percent in 2024 due to higher discount rates. Higher finance costs incurred during the year were regardless of the fact that the company settled some of its outstanding liabilities during the year which drove its debt-to-equity ratio down to 13 percent in 2024. Net profit shrank by 71.69 percent in 2024 to clock in at Rs.353.23 million with EPS of Rs.1.62 and NP margin of 3.34 percent.

Recent Performance (1QFY25)

With an 8.47 percent year-on-year decline in sales during 1QFY25, the ongoing fiscal year doesn’t appear encouraging for PREMA. Sales proceeds from all three sources posted a plunge during the period. While the stability of the Pak Rupee continued to affect the valuation of biological assets, shrunken demand also played its role in squeezing sales. Cost of sales dropped by 10.14 percent resulting in a 2.14 percent diminution in gross profit in 1QFY25. However, the GP margin progressed from 20.86 percent in 1QFY24 to 22.30 percent in 1QFY25. Lower sales volume resulted in selling expenses posting a marginal uptick of 3.29 percent in 1QFY25, and administrative expenses escalated by 25.97 percent during the period. This was due to inflationary pressure which particularly drove up payroll expenses and vehicle running expenses. Other expenses ticked up by 3.59 percent during the period probably due to loss on sale of dairy livestock. Other income considerably expanded during 1QFY25 may be on the back of the sale of operating fixed assets. During 1QFY25, PREMA’s operating profit slid by 21 percent with its OP margin clocking in at 3.86 percent versus the OP margin of 4.47 percent recorded in 1QFY24. A decline in outstanding liabilities and monetary easing resulted in a 21.66 percent shrinkage in finance costs in 1QFY25. Net profit of Rs.24.42 million recorded during 1QFY25 was 20 percent less than the net profit recorded during the same period last year. EPS dipped from Rs.0.14 in 1QFY24 to Rs.0.11 in 1QFY25. NP margin also inched down from 1.21 percent in 1QFY24 to 1 percent in 1QFY25.

Future Outlook

The future of PREMA looks promising due to constant innovation and renovation of its product portfolio, offering of value-added products, and optimization of its value chain. The company has expanded its geographical footprint across the country to drive better sales volume.

Comments

Comments are closed for this article.