Pakistan Oxygen Limited

Pakistan Oxygen Limited (PSX: PAKOXY), formerly Linde Pakistan, was established in 1949 as a private limited company under the Companies Act 1913, (now Companies Act, 2017). It was later converted into a public limited company in 1958.

The company has five business lines; bulk gases, which include liquid oxygen, liquid nitrogen, liquid argon, etc. compressed industrial gases which includes compressed oxygen, aviation oxygen, dissolved acetylene, etc. PGP and Hardgood; health care related gases, such as liquid helium for MRI scanners, gas mixtures for calibration of clinical blood gas analyzers. Lastly there is tonnage and plant engineering.

Shareholding pattern

Associated companies, undertakings and related parties own a large part of Pakistan Oxygen- a little over 69 percent. Of this 33 percent is with M/s Adira Capital Holdings (Pvt) Limited, followed by M/s Hilton Pharma (Pvt) Limited at 24 percent. About 16 percent is distributed with the local general public, while directors, CEO, their spouses and minor children own 7.33 percent of Pakistan Oxygen. Of this Mr. Shahid Mehmood Umerani, the director of the company holds 7.2 percent of the shares.

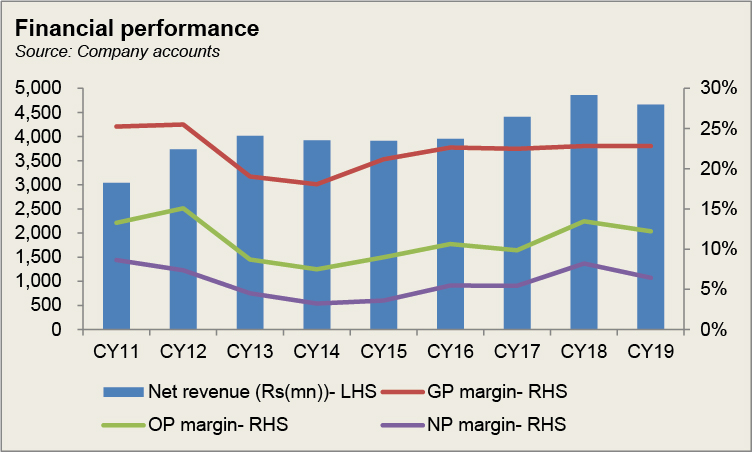

Historical operational performance

The topline of Pakistan Oxygen experienced its highest growth at the start of the decade after which the rate has been on a decline, before reaching double digits again in CY17. Profit margins also remained relatively subdued around CY13 and CY14 before recovering again in CY18.

In CY14, Pakistan Oxygen saw a 2 percent decline in its topline due to a number of factors. Despite the fact that all the plants remained operational, it could not be translated into higher revenue and margins; rather CY14 saw the lowest gross profit and bottomline in nearly a decade. So while volumes registered an 8 percent growth, prices declined sharply as a result of excess supply and low demand. In addition, there also existed increased competition, primarily in the ship breaking and health sector. The company also installed a new nitrogen plant to cater to the increased demand coming from PARCO refinery, among other replacements and upgradations.

Energy and gas shortage continued to adversely impact the Large Scale Manufacturing (LSM) sector during CY15. Although an improvement was seen, it still remained below the target. The company’s topline reduced marginally by less than a percent, while cost of production saw some decline, aiding an improvement in gross profit. Surplus product continued to hamper product prices, while imported, cheaper steel products from China adversely impacted the metal segments. Moreover, the fall in global oil prices affected exploration activities. Operating in this scenario, the company focused on plant productivity and value addition, along with reducing costs by curtailing power and diesel costs, and manpower reorganization, resulting in better margins despite the lower income from other sources.

In CY16, Pakistan Oxygen was able to post a positive growth rate in its topline, even if marginally. Cost of production saw a further decline which for some part enabled margins to improve. The improvement in net revenue was largely driven by the gases segment which grew by 4 percent. This was due to increased efforts towards building new customers in addition to a focus on energy, chemicals, food and beverages and oil and gas sectors. During the year, the company also faced challenges of imported cheaper goods, which pushed prices down. Despite these challenges, Pakistan Oxygen fared decently, improved its manufacturing efficiency and grew profit margins.

In CY17, Pakistan Oxygen experienced its first double digit growth in revenue since CY12- close to 12 percent. The healthcare segment and welding and hard goods segment largely contributed to this robust growth. Both segments recorded 25 percent and 20 percent growth, respectively. The gases segment also contributed to higher revenue due to growth in steel, ship breaking and manufacturing sectors. However, the higher revenue brought with it costs as well, which restricted the profit margins from taking off, remaining more or less flat year on year. During CY17, the company’s ASPEN 1000 plant delivered the highest production seen thus far, increasing by 17 percent. This was after its control system modification.

Despite the shutdown of activities at Gaddani which impacted sales negatively, the company grew its topline by 10 percent year on year. This was led by welding and healthcare segments which recorded 30 percent and 24 percent increase in sales, respectively. Within the welding segment, the brands Zodian, Fortrax and Matador were approved and demanded for various projects nationwide. In addition, the company’s facilities operated at full capacity. On the costs side, there was a notable decline in distribution and administrative expenses due to absence of technical assistance fee, support and services. With an increased topline for two consecutive years and curtailment of costs, the profit margins for the company peaked in CY18.

Recent annual result and future outlook

Large Scale Manufacturing (LSM) declined by 3.4 percent in FY19 along with GDP recorded at 3.3 percent. There was a slowdown in the economy; energy prices increased, inflation took off, and leading the policy rate to go up to 13.25 percent. The effect of this was seen in the company’s financials. Pakistan Oxygen witnessed a negative year on year growth rate of nearly 4 percent.

The automobiles and steel sector saw a 12 percent and 11 percent decline, in addition to a complete shutdown of ship breaking which contributed to lower net revenue. However, the company managed to keep its costs under control while the ‘in-house manufacturing of electrodes’ also allowed for cost saving. This, its gross and operating margins remained more or less similar, while net margin declined due to an escalated finance cost.

In the wake of Covid-19, and the consequent lock down, it is likely that the manufacturing sector will be impacted which will impact the company’s revenue; there is a certainty of subdued business activity and growth for the future.

Comments

Comments are closed for this article.