Attock Cement is a prominent player in the cement industry and a shining star of the southern region with the company's facility located in Hub, Balochistan. The company established set-up in 1981 as a result of a joint venture between Pakistan and Saudi Arabia with an initial capital outlay of Rs1.5 billion including a foreign exchange component of $45 million and started commercial production in 1988 with a plant capacity of 2,000 tons per day of clinker. It has since kept its pace with the cement sector in Pakistan beefing up its capacity with modernisation. The current Hub facility has a production capacity of 1.74 million tons per annum.

ACPL is a part of the Pharaon Group, a group of companies that has investments in diversified fields such as cement, oil & gas, power generation and information technology. ACPL is listed on the Pakistan Stock Exchange.

The company primarily deals in the production of ordinary Portland cement, sulphate resistant cement and block cement and operates under the brand name Falcon. The brand has its market spread out across Pakistan and exports to South Africa, Sub-Saharan Africa, Iraq, the Gulf region reaching out to regional countries such as Sri Lanka and India. The company has several subsidiaries including Pakistan Oilfields Limited set up in 1950, Attock Refinery that was established in 1922, Attock Petroleum Limited that was established jointly by the Pharaon Investment Group Limited Holding (PIGL) and Attock Oil Group of Companies (AOC) in 1995. In 2005, the company also took over National Refinery Limited (NRL).

The company has been part of several large scale construction projects including HUBCO Power Company, Bahria Complex projects, Jinnah International Airport, Lyari Expressway and MCB Tower.

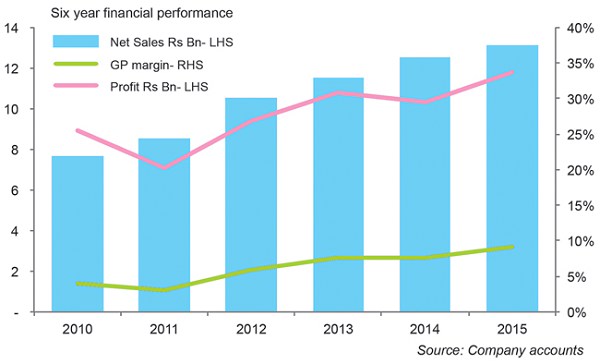

Six-year operational and financial performance

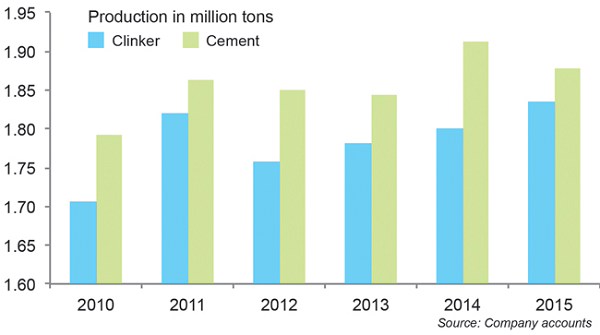

Production for both clinker and cement has grown in the past six years with clinker production growing by eight percent between 2010 and 2015 and cement production going up by five percent in this time period. FY15 was an exceptionally good year for the company recording its highest ever clinker production of 1.83 million tons, which stood at 1.7 million tons in FY10. Cement production was 1.87 million tons in FY15 compared to 1.79 million tons in FY10.

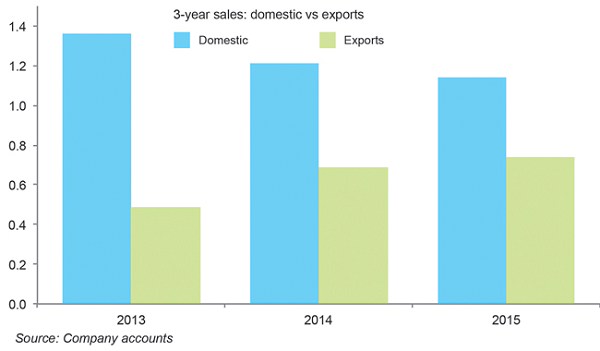

Combined domestic and export sales grew by four percent in the past six years with more than 60 percent of the sales contributing to the domestic market. Trends have been up for both domestic and export side with most notable growth registering between FY13 and FY15 where exports grew by 53 percent. Exports primarily went to South Africa but the recent slap of 63.53 percent anti-dumping duty will affect them in coming fiscals. Other export destinations for ACPL have been Iraq, Sri Lanka and Sub-Saharan African countries.

Net sales went up to Rs13.09 billion, a phenomenal growth of 71 percent year-on-year. Net profits have maintained a similar pattern. Before-tax profits grew by 132 percent between FY10 and FY15. Margins have seen a surge in recent years due to the low input cost and high domestic pricing, going from 26 percent in FY10 to 34 percent in FY15. Profits fell slightly in FY14 due to an increase of power tariff by 55 percent that increased the production cost by Rs366 per ton. In later years, the increase in production costs was passed onto consumers.

Coal prices have been falling. In FY15, they fell from $92 per ton to $81 per ton contributing favourably to lowering production costs. Power cost per ton was reduced by Rs45 per ton after a major overhaul and up-gradation to its cement mill. The company also installed variable frequency drives (VFDs) on its key motors, which contributed positively in the reduction of overall power cost.

In FY15, profits were supplemented by other income increasing by Rs153 million owing to the placement of surplus cash in better performing mutual funds. Boosting high profitability, the company paid a cash dividend of Rs10.5 per share (105 percent) to shareholders amounting to Rs1,202 million in FY15.

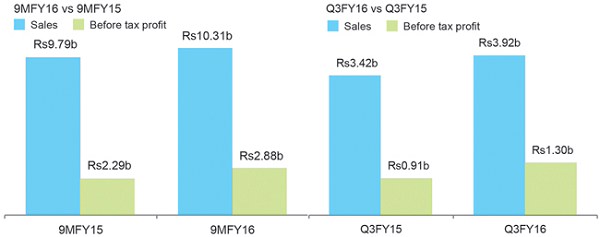

Operations in 9MFY16 and Q3FY16

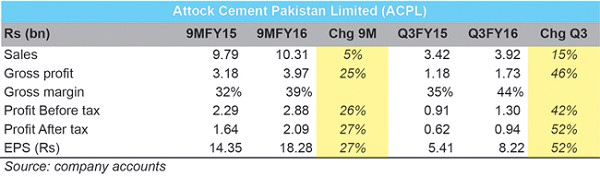

Recent financial performance points toward a sustained growth pattern. In 9MFY16, production of clinker stood at 1.42 million tons, 3 percent higher than 9MFY15; cement production also had the same year-on-year growth standing at 1.455 million tons in 9MFY16. While volumetric sales grew substantially with 26 percent year-on-year growth between the two nine-month fiscals, exports remained depressed owing largely to the infamous South African anti-dumping levy and currency devaluations in other African markets. Sales in exports recorded a decline of 27 percent in 9MFY16 in year-on-year change.

Profit before taxes show a 26 percent growth between 9MFY15 and 9MFY16. Net sales grew by three percent in this time period. Margins rose subsequently: 39 percent in 9MFY16 from 32 percent in 9MFY15 and major contributors are lower coal prices and the company's energy efficiency measures that cut down on power cuts. Prices have remained high for local markets compared to export markets.

The third quarter was extraordinary in itself. Quarterly results show bolstered margins at 44 percent in Q3FY16 as opposed to 35 percent in Q3FY15; net sales growth was at 15 percent in this time and net profit growth was 42 percent.

Stock performance

Looking just at the last one year starting May 2015, stock prices have moved in tandem with the benchmark KSE index. More notable changes were seen from March 2016 and May 2016 when stock price reached Rs241 from Rs160 in March, a growth of 51 percent. Recent financial performance and positive future outlook are both contributing to investor optimism.

Energy and cost efficiency

The cement sector should get credit for forward thinking in developing an infrastructure for efficient use of energy and reducing dependence on the unreliable national grid. The company's move to upgrade the cement grinding mill and installation of VFD's led to higher energy efficiency and lower costs. Continuing on this track and following suit with other cement firms, ACPL had commissioned a coal-fired power plant to provide 40 MW of energy to its factory in Hub. The process was slowed down due to a water shortage in the Hub dam but is expected to be picked up in the coming fiscal. The plant would power the factory as well as sell off surplus power to K-electric and is expected to be operational in FY18.

Expansion plans

ACPL announced that it is installing a new production line with a capacity of 1.2 million tons annually (3,300 tons per day) at its existing site which will add to its existing 1.8-million-ton capacity. The cost of this expansion is $120 million. Hoping to set a footprint outside Pakistan, the company announced that it would be establishing a cement grinding facility in Basra, Iraq with a production capacity of 900,000 tons per annum laying a capital of $40 million. A joint venture agreement was signed with an Iraqi firm where ACPL will hold 60 percent of the share. The project is now near completion.

Opportunities, threats and outlook

The up tick in domestic consumption driven by more public and private construction projects, greater PSDP spending (68 percent releases to date) recently compared to earlier years and low cost-high efficiency has paid dividends to the company. The company's strategic geographic advantage will prove even more profitable once the CPEC projects are initiated. DG Khan announced that it would be setting up shop in Hub with the plant capacity of 1.3 million tons which could prove to be competition and ACPL's expansion plans in this scenario are almost imminent and necessary if it intends to keep its share of the market, already lower than the big-three.

The company has been marketing its products to areas in upper Sindh and Punjab to reap benefits from development in these regions which is a positive.

The government imposed a hefty super tax in its budget FY15-16 bumping effective tax rate from 23.6 percent to 31.5 percent. It remains to be seen whether another super tax is on the cards. While it won't affect the bottom line of the company, the sector is likely to pass the prices onto consumers. There is already a wide differential between domestic and export prices. More taxes and expansion plans by all major firms could potentially set in motion a price war in the sector that would ultimately affect margins for smaller firms and domestic consumers.

But opportunities are enormous and with the promise of CPEC, however challenging, and improved security condition within the country, the economy is likely to stabilise with more investments in infrastructure and real estate. But whether there will be enough for everyone to get a piece of the pie remains to be seen.

On the international side, ACPL has shown perseverance with increase in exports compared to some of its competitors. Overall export dispatches have been falling this year and will continue to fall given the largest market South Africa is barring imports via massive taxes. The company should leverage its good standing in regional countries such as Sri Lanka and Nepal that are growing and dependent on imports. Though the change in duty regime in Sri Lanka is a challenge for Pakistani cement facing competition from Thailand and Vietnam and companies here will have to buck-up in terms of quality and better pricing.

India is an emerging market with major infrastructure opportunities but competitive since its expanding indigenous capacity. UAE is pretty self-sufficient in cement production, but Gulf regions and Saudi Arabia are open markets that need to be explored.

Comments

Comments are closed for this article.