Pakistan Cables Limited (PSX: PCAL) was incorporated in Pakistan as a private limited company in 1953 and was converted into a public limited company in 1955.

The principal activity of the company is the manufacturing and sale of copper rods, wires, cables and conductors, aluminum extrusion profiles and PVC compounds.

Pattern of Shareholding

As of June 30, 2025, PCAL has a total of 54.457 million shares outstanding which are held by 2421 shareholders.

Directors, CEO, their spouse and minor children have the majority stake of 26.96 percent in the company followed by local general public holding 25.86 percent of its shares.

Associated companies, undertakings and related parties which comprise of International Industries Limited and Shirazi Investments (Private) limited hold 17.12 percent and 4.22 percent shares of PCAL respectively. Banks, DFIs, NBFIs, Insurance companies, Takaful, Modarabas & Pension funds collectively account for 2.28 percent of the company’s shares. The remaining shares are held by other categories of shareholders.

Financial Performance (2021-25)

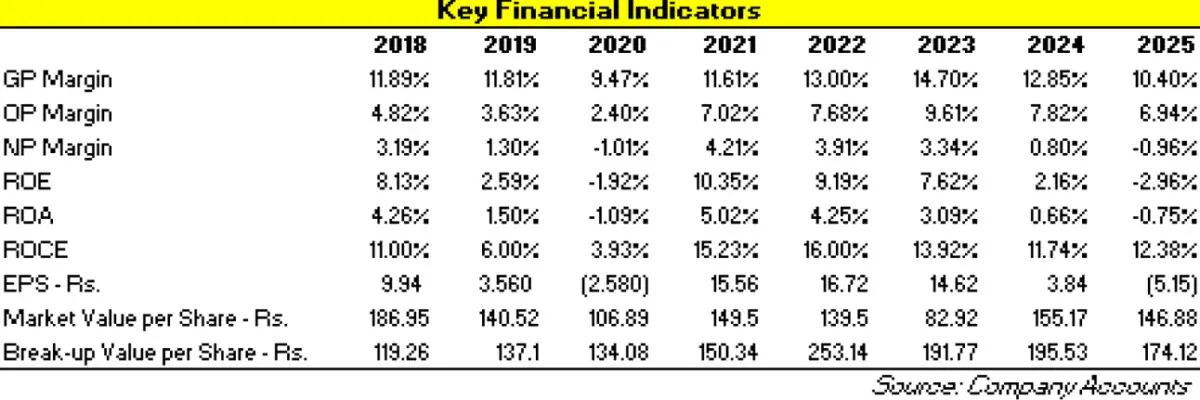

PCAL’s topline followed an upward trajectory over the period under consideration. PCAL’s bottomline mustered staggering growth in 2021 and 2022 with the highest ever net profit recorded in 2022. In the subsequent years, PCAL’s net profit considerably shrank.

The company posted net loss in 2025. PCAL’s margins which were dwindling until 2020, significantly recovered in 2021. In the next two years, while gross and operating margins kept rising to max out in 2023, net margin followed a descending route. In 2024 and 2025, all the margins registered a plunge. The detailed performance review of the period under consideration is given below.

With a magnificent 44.67 percent year-on-year rise in its topline, PCAL seems to have come out of its misfortune pitch in 2021. Net sales were recorded at Rs. 13,145.05 million in 2021. This was on account of a rebound in demand due to multiple policy initiatives undertaken by the government including construction package.

The company also invested in a new plant during the year using SBP Temporary Economic Refinance Facility (TERF). Sharp spike in international copper prices during the year resulted in price rationalization of PCAL’s products which also buttressed the net sales in 2021.

Besides Pakistan, the sales to African region also stayed upbeat during 2021. Cost of sales grew by 41.24 percent year-on-year in 2021. Robust sales volume and prices resulted in 77.44 percent year-on-year growth in gross profit with GP margin jumping up to 11.61 percent in 2021 from 9.47 percent in 2020.

Higher freight charges and payroll expense drove the distribution expense up by 19.46 percent year-on-year in 2021. Administrative expense also grew by 22.34 percent year-on-year in 2021. Other expense and other income posted an extraordinarily high growth of 1142.26 percent and 382.54 percent respectively in 2021. Higher other expense was due to increased provisioning done for WWF and WPPF booked in 2021. Other income grew primarily on the back of insurance claim received against business interruption.

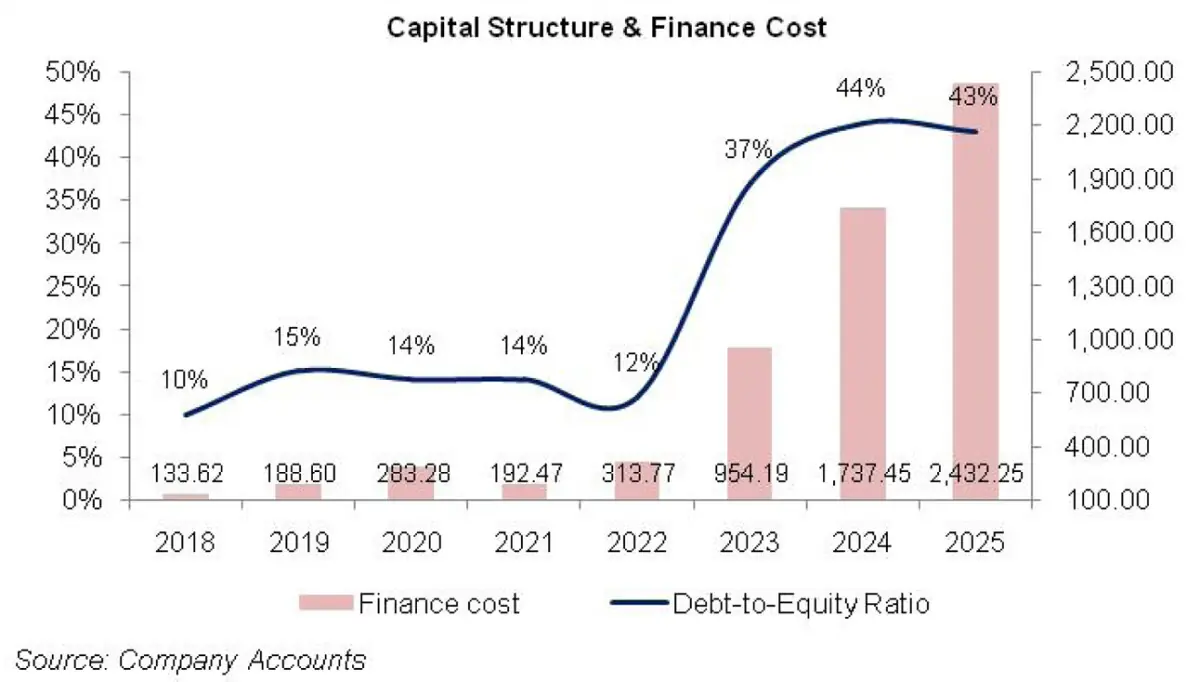

Operating profit posted a staggering year-on-year growth of 322.83 percent in 2021 with OP margin of 7 percent versus 2.40 percent in 2020. Finance cost shrank by 32 percent in 2021 despite increased borrowings during the year. This was on account of lower policy rate.

PCAL posted net profit of Rs.553.65 million in 2021 as against the loss of Rs.91.876 million posted in 2020. This translated into an EPS of Rs.15.56 and an NP margin of 4.21 percent in 2021 – the highest among all the years under consideration.

The luck streak continued in 2022 as PCAL posted a splendid 61 percent growth in its net sales which clocked in at Rs. 21,167.66 million. This came on the back of a rise in both volumes and prices of the company’s products. This was despite the fact that the country was passing through immense political turmoil during 2022 which had pushed it into serious macroeconomic vulnerabilities.

Cost of sales grew by 58.51 percent year-on-year in 2022 due to commodity super cycle on account of Russia-Ukraine crisis as well as Pak Rupee depreciation.

Energy price hike also added insult to injury. PCAL was able to attain 80.21 percent year-on-year growth in gross profit with GP margin jumping up to 13 percent in 2022.

Distribution expense grew by 46.77 percent year-on-year in 2022 on the back of higher advertising and freight charges. Administrative expense also escalated by 21 percent year-on-year in 2022 which was the result of an uptick in the number of employees from 465 in 2021 to 503 in 2022 and also because of the inflationary pressure which drove the salaries up.

During the year, PCAL booked an impairment allowance worth Rs.71.58 on investment in International Industries Limited (IIL), an associate company of PCAL. PCAL’s net sales were strong enough to absorb the elevated operating expenses and trickle down into 76.19 percent bigger operating profit in 2022 with OP margin of 7.68 percent.

Finance cost magnified by 63 percent year-on-year in 2022 due to higher discount rate and also because of increased borrowings particularly running finance facilities obtained during the year.

In 2022, PCAL’s net profit grew by 49.50 percent year-on-year to clock in at Rs.827.73 million with NP margin of 3.91 percent in 2022. EPS stood at Rs.16.72 in 2022.

In 2023, PCAL registered a paltry 2.29 percent growth in its net sales which clocked in at Rs.21,652.95 million. This was due to high prices of copper while sales volume remained depressed on account of slow construction and industrial activity in the country.

During the year, the company’s sales also suffered due to import restrictions, inflationary pressure, higher discount rate, Pak Rupee depreciation and supply chain disruptions. The devastating floods that occurred during the year further worsened the economic conditions. With lower off-take, cost of sales grew by only 0.28 percent, resulting in 15.74 percent year-on-year growth in gross profit in 2023.

GP margin considerably grew to 14.70 percent – the highest since 2018. Despite lower sales volume and dejected overall business performance, distribution expense grew by 5.78 percent due to elevated carriage and forwarding expenses. Administrative expense surged by 9.11 percent year-on-year in 2023 on account of unprecedented level of inflation.

Operating profit grew by 27.90 percent year-on-year in 2023 with OP margin marching up to 9.61 percent. Finance cost multiplied by 204.10 percent in 2023 on the back of high discount rate and increased long-term loans obtained during the year to finance the company’s capital expenditure plans.

PCAL’s net profit couldn’t sustain the massive finance cost and shed its value by 12.57 percent year-on-year in 2023 to clock in at Rs.723.65 million with NP margin of 3.34 percent and EPS of Rs.14.62.

PCAL registered year-on-year growth of 20.85 percent in its topline which clocked in at Rs.26,167.04 million in 2024. This was the result of improved sales volume as well as upward price revisions due to elevated copper prices.

During the year, copper prices touched its record high price of USD 11,105 per ton. In the presence of thin demand, the company couldn’t completely pass on the impact of cost hike to its consumers. While gross profit ticked up by 5.65 percent in 2024, GP margin slipped to 12.85 percent. Distribution expense mounted by 23.55 percent in 2024 due to higher advertising and promotion budget and an increase in carriage and forwarding charges incurred during the year.

Administrative expense ticked up by just 2.32 percent in 2024 on account of inflation. The company also expanded its workforce from 549 employees in 2023 to 574 employees in 2024. For the past three years, PCAL had been booking reversals of allowance on trade receivables.

However, it was replaced by booking of impairment allowance worth Rs.52.03 million during the year. Operating profit dwindled by 1.63 percent in 2024 with OP margin falling down to 7.82 percent. Finance cost escalated by 82 percent in 2024 due to higher discount rate and long-term debt obtained during the year to finance its manufacturing facility in Nooriabad. PCAL’s debt-to-equity ratio climbed up from 37 percent in 2023 to 44 percent in 2024.

The company recorded 71.14 percent year-on-year decline in its net profit in 2024 which clocked in at Rs.208.858 million with EPS of Rs.3.84 and NP margin of 0.80 percent.

In 2025, PCAL’s topline grew by 11.16 percent to clock in at Rs.29,088.37 million. This was mainly on account of upward price revision of the company’s products in line with the escalation in cost of sales.

The year was marked by an improvement in macroeconomic indicators - decline in inflation and discount rate, stability of Pak Rupee, rising foreign exchange reserves and current account surplus, however, subdued industrial and construction activity due to lackluster development spending, shattered investor confidence and elevated construction, cost resulted in low demand of PCAL’s products in 2025.

Cost of sales surged by 14.29 percent in 2025 due to elevated prices of copper and aluminum as the demand of these metals in the EV and renewable energy markets was higher than the supply. This resulted in 10 percent dip in gross profit in 2025 with GP margin falling down to 10.40 percent.

Distribution expense plunged by 2.34 percent in 2025 mainly on account of considerably lower advertising & promotion budget allocated for the year. Administrative expense ticked up by 1.42 percent in 2025 due to higher repair & maintenance charges as well as increased communication expense.

Payroll expense nosedived in 2025 as the company streamlined its workforce from 574 employees in 2024 to 536 employees in 2025. Other expense descended by 55.76 percent in 2025 as no provisioning was done for WWF and WPPF.

Other income strengthened by 147.91 percent in 2025 due to higher sale of scrap, increased gain on the disposal of fixed assets, greater income from bank deposits and TDRs as well as amortization of government grant. PCAL’s operating profit dipped by 1.28 percent in 2025 with OP margin falling down to 6.94 percent.

While discount rate considerably dropped during the year, PCAL’s finance cost mounted by 40 percent in 2025 due increased external borrowings to meet working capital requirements as well as to finance its manufacturing facility at Nooriabad. PCAL posted net loss of Rs.280.601 million in 2025 with loss per share of Rs.5.15.

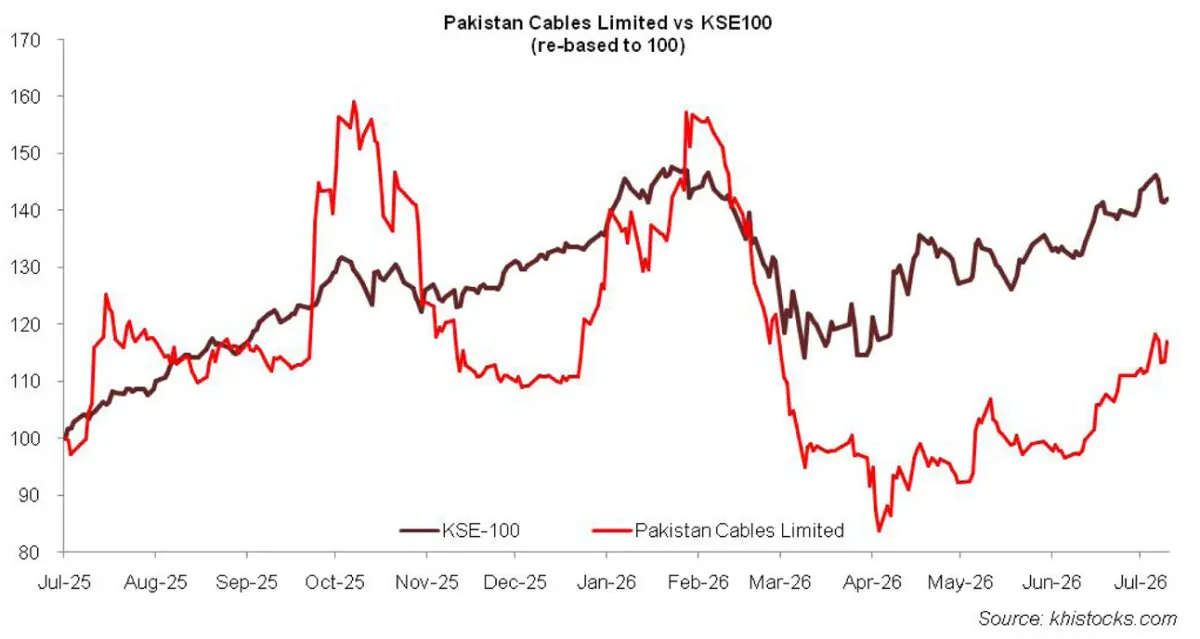

Recent Performance (9MFY26)

During the nine-month period of the ongoing fiscal year, PCAL posted year-on-year uptick of 5.51 percent in its net sales which clocked in at Rs.23,471.25 million. The growth came on the back of local sales while export sales ticked down during the period. Improvement in local sales was due to the revival of construction activity in the country on the back of recovery witnessed in the local macroeconomic indicators.

Export sales weakened during the period due to lesser sales recognized from American and Middle Eastern region and no sales made to Asian region (besides local sales). Stronger topline could only muster a marginal 2.15 percent uptick in gross profit in 9MFY26 due to elevated prices of copper and aluminum and higher energy cost.

GP margin dipped from 10.50 percent in 9MFY25 to 10.16 percent in 9MFY26. Selling & distribution expense inched up by 8.51 percent in 9MFY26 on the back of higher advertising & promotion budget which was partially offset by lesser carriage & forwarding expense incurred during the period. Administrative expense surged by 13.12 percent in 9MFY26 due to higher payroll expense.

Other expense dropped by 76.59 percent in 9MFY26 likely due to lesser liquidated damages for late deliveries. Other expense was offset by other income of Rs. 235.50 million recognized during the period, up 11.75 percent year-on-year. This was due to robust gain recognized on the sale of fixed assets in 9MFY26.

PCAL recorded 2.86 percent dip in its operating profit in 9MFY26 with OP margin clocking in at 6 percent versus 6.58 percent recorded in 9MFY25. Finance cost shrank by 9.63 percent in 9MFY26 due to monetary easing.

Conversely, short-term borrowings escalated during the period. What massively strengthened PCAL’s bottomline was the robust share of profit from associate (Chinoy Engineering & Construction Private Limited) worth Rs.480.64 million recognized during the period, up 980.12 percent year-on-year. This enabled the company to record net profit of Rs.206.23 million in 9MFY26, versus net loss of Rs.260.986 million recorded in 9MFY25. EPS clocked in at Rs.3.79 in 9MFY26 versus loss per share of Rs.4.79 recorded in 9MFY25.

Future Outlook

Investment in the country’s grid infrastructure and renewable energy to mitigate the soaring energy cost as well as increased development spending to make up for the infrastructure losses due to floods will create ample demand for the company’s products.

Besides, the policy measures taken by the federal government and Sind government to stimulate growth in the construction and housing sectors will also result in improved demand of PCAL’s products. The company has recently completed the expansion of its Nooriabad manufacturing facility. This will also boost the company’s operational efficiency and result in improved financial performance.

On the flipside, the company’s financial performance hinges on the prices of copper, aluminum and petroleum which are projected to spike in the wake of the ongoing geopolitical tensions.

The onset of monetary tightening may also mar the company’s financial performance given its highly leveraged capital structure.

Comments