FDI stuck in low gear

Foreign direct investment saw a slight recovery in May 2026 but overall declined significantly in 11MFY26, failing to respond to macroeconomic stability despite new budget incentives.

- Cumulative decline in foreign direct investment.

- FDI concentration in power and financial sectors.

- Budget incentives and their potential impact on FDI.

- IMF projections for future foreign investment.

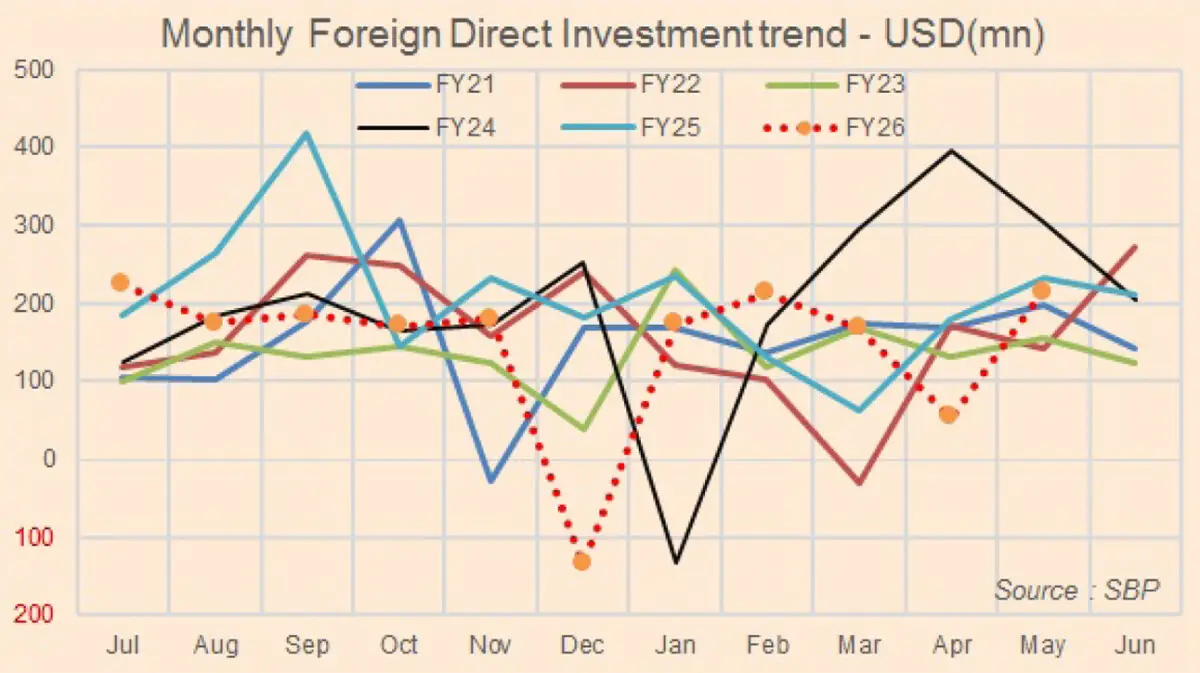

Foreign direct investment recovered in May 2026, but the improvement was neither enough to change the broader picture, nor anything out of ordinary when compared to previous average monthly bet inflows.

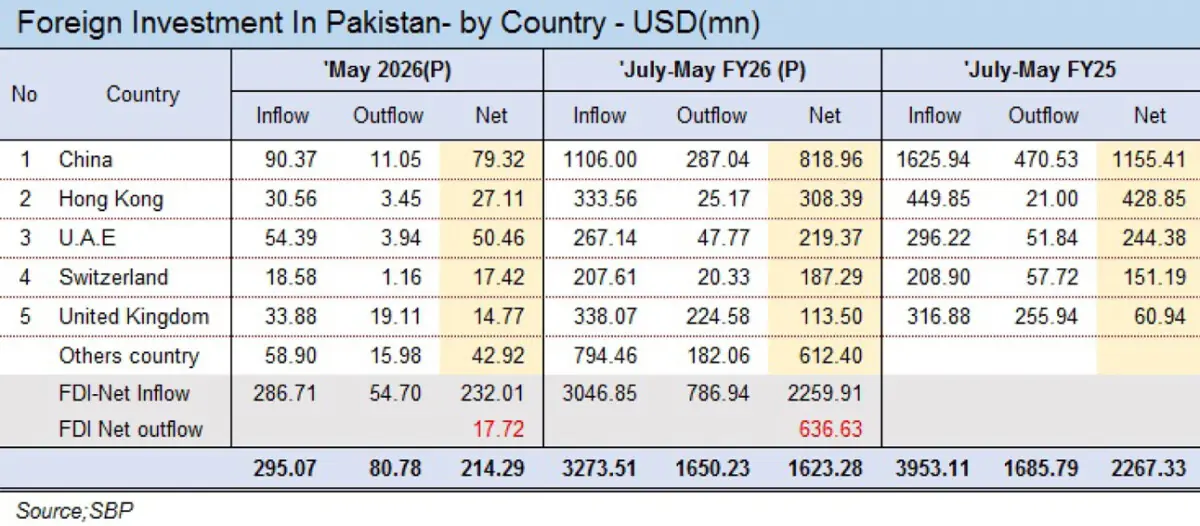

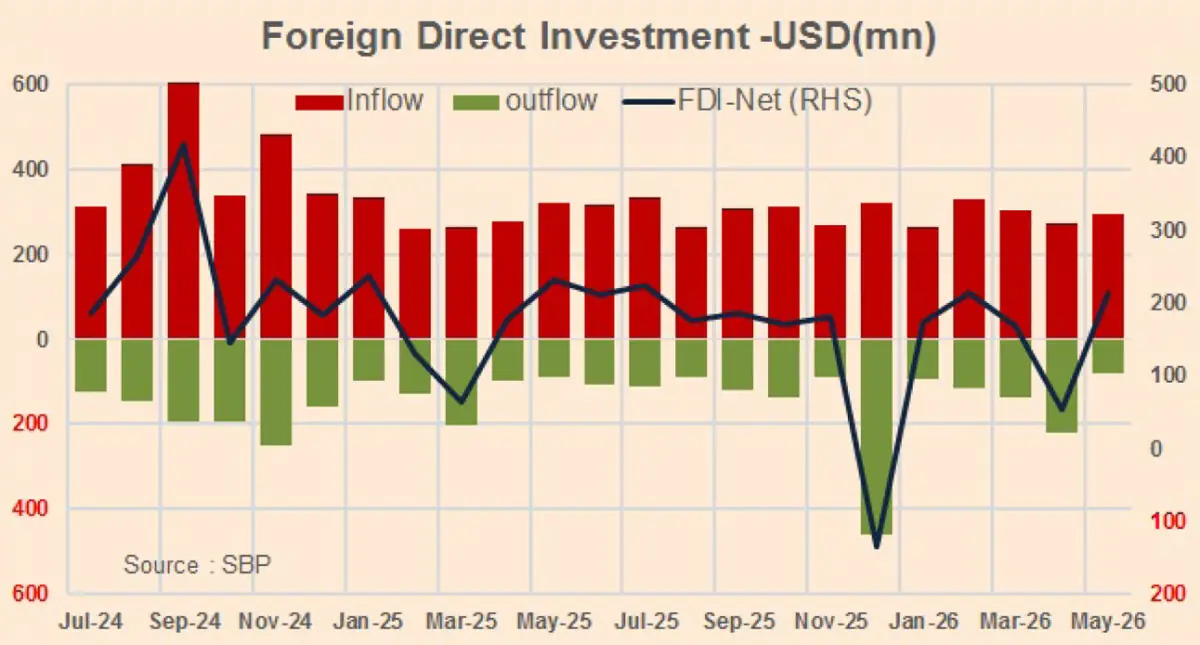

Net FDI stood at USD214 million during the month, compared to around $55 million in April. Gross inflows reached USD295 million, while outflows were contained at USD81 million.

Cumulatively, net FDI declined by 28 percent to USD1.62 billion during 11MFY26, compared to USD2.27 billion in the same period last year.The decline was mainly due to weaker fresh inflows.

Gross FDI inflows fell by 17 percent to USD3.27 billion, while outflows remained broadly unchanged at USD1.65 billion showing fewer new dollars are entering the country.

Pakistan may have achieved some degree of macroeconomic stability, but stability has yet to translate into a meaningful recovery in foreign investment.

Inflation and exchange-rate volatility have eased compared to the crisis years, the IMF programme remains on track, and foreign exchange reserves have improved. Yet foreign investors continue to take a cautious view.

China remained the largest source of investment during 11MFY26, with net inflows of USD819 million. However, this was 29 percent lower year-on-year. Hong Kong followed with USD308 million, also down by 28 percent year-on-year.

Net investment from the UAE declined by 10 percent to USD219 million. Investment from Switzerland increased by 24 percent to USD187 million, while flows from the United Kingdom almost doubled to USD114 million. But these improvements were not large enough to compensate for the decline in Chinese and Hong Kong FDI.

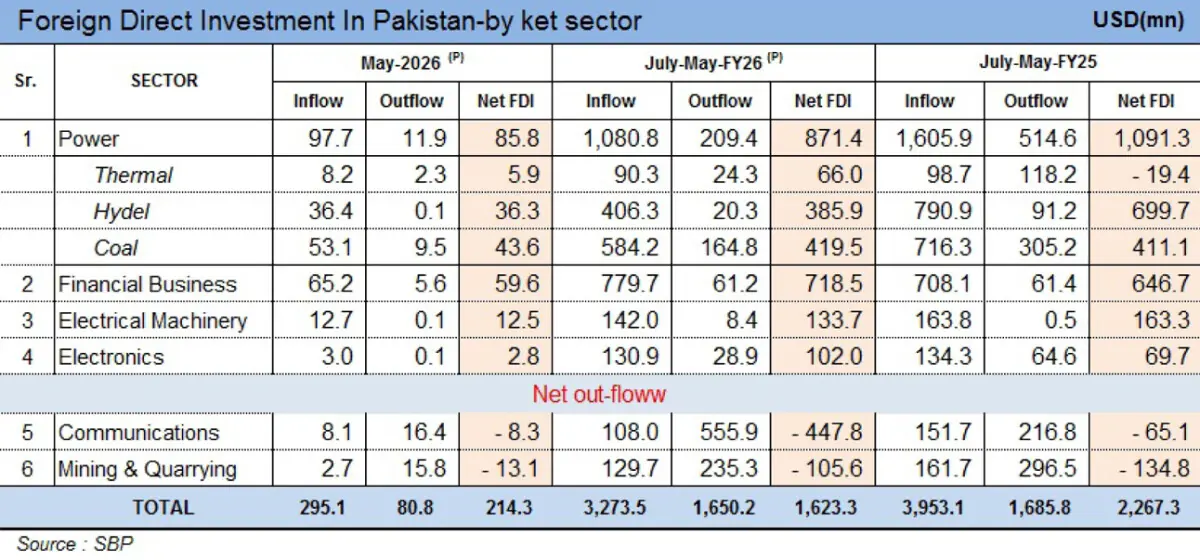

The sectoral composition is even more revealing. Almost the entire net FDI during 11MFY26 was concentrated in power and financial businesses. The power sector attracted USD871 million, while financial businesses received USD719 million. Together, the two sectors accounted for nearly 98 percent of overall net FDI.

Power-sector investment, however, declined by 20 percent from USD1.09 billion last year. Hydropower investment fell sharply, while coal investment remained broadly stable. Thermal power, on the other hand, moved from a net outflow last year to net inflows in 11MFY26.

Financial businesses performed better, with net FDI increasing by 11 percent to USD719 million. The biggest drag came from communications, which recorded net outflows of USD448 million, compared to an outflow of only USD65 million last year. Mining and quarrying also recorded net outflows of USD106 million. These numbers may reflect divestments, repayments of intercompany liabilities, etc.

The heavy concentration of FDI remains a big concern. Pakistan is still not attracting meaningful foreign investment in export-oriented manufacturing, information technology, agriculture, logistics and other sectors capable of generating recurring foreign exchange earnings.

The latest Economic Survey highlights improving macroeconomic conditions and investor confidence. Yet the overall investment-to-GDP ratio remains low at 14.38 percent, while national savings stand at 14.13 percent of GDP. That is hardly the investment base required to sustain high growth over several years.

The IMF’s projections are equally telling. FDI is expected to remain flat at only 0.5 percent of GDP in both FY26 and FY27, slightly below 0.6 percent in FY25, which means that even the baseline outlook does not show a meaningful investment breakthrough over the next year.

The recently announced budget has attempted to improve the corporate and investment climate. The Super Tax rate has been reduced to 8 percent for corporate incomes exceeding Rs500 million and abolished for most sectors earning below that threshold. The income tax exemption for the IT sector has also been extended until June 2029, while withholding tax on export proceeds has been reduced to 1.25 percent.

These measures can improve after-tax returns and provide greater visibility to businesses, particularly export-oriented firms, and technology companies. The extension of the IT tax exemption is especially relevant because technology investment requires policy continuity and a longer planning horizon. Similarly, lower taxation of export proceeds could make Pakistan more attractive for companies earning in foreign currency.

But tax incentives alone will not deliver FDI. Foreign investors also look for predictable policies, reliable energy supplies, the ability to repatriate profits, contract enforcement, and regulatory consistency. The budget incentives may help at the margin, particularly for corporates and the IT sector. But unless they are backed by policy credibility and broader structural reforms, the IMF’s projection of FDI remaining stuck at 0.5 percent of GDP may prove difficult to beat.

Comments