The federal budget has shifted the policy conversation from stabilization toward growth. That was inevitable.

After nearly three years of compression, there is growing impatience with an economy that remains well below its potential. Businesses want demand. Households want income growth. Provinces want development spending. Industries operating below capacity want relief. The political cycle is moving deeper into its second half, and governments rarely enter the latter stages of their tenure arguing for more austerity.

Yet the timing is awkward.The Monetary Policy Committee meets at a moment when the case for growth is becoming stronger, even as the case for complacency on inflation is becoming weaker.

At first glance, that may appear counterintuitive. Inflation is nowhere near the levels witnessed during the crisis years. The economy remains fragile, private investment has yet to recover meaningfully, and development spending continues to face pressure. The federal budget itself is hardly a classic stimulus package. However, monetary policy is not designed to respond to today’s inflation; it is designed to prevent tomorrow’s.

That distinction is important because inflation is often the final stage of a process whose earlier signals appear elsewhere. The relevant question is not whether inflation is currently being driven by oil prices, electricity tariffs, or taxation measures. It almost certainly is. The more relevant question is whether prevailing monetary and financial conditions remain consistent with inflation eventually returning to the State Bank’s medium-term target range of 5-7 percent.

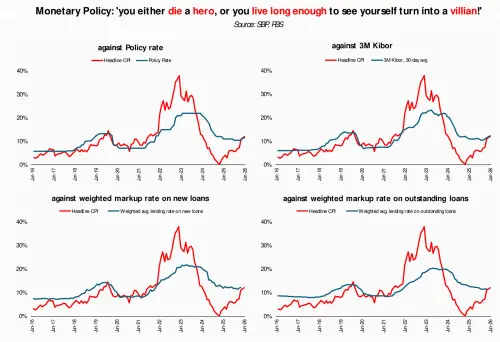

The evidence is becoming less clear.Broad money growth accelerated into the mid-to-high teens during FY26, while currency in circulation has been growing close to 20 percent year-on-year. Deposit growth has strengthened materially as well. At the same time, the spread between policy rates and broader market rates has narrowed, financing conditions have eased, and the effective degree of monetary restraint has softened despite the policy rate remaining in double digits.

None of these indicators, taken individually, would ordinarily warrant concern. Monetary aggregates do not translate mechanically into inflation, just as a single month’s inflation print rarely reveals much about the future. Yet monetary conditions are assessed in aggregate, not in isolation.

Nor is there a stable one-for-one relationship between money growth and consumer prices. However, monetary aggregates growing materially faster than the inflation target inevitably raise a question about where the adjustment is expected to occur.

Historically, the answer has been some combination of stronger nominal growth, higher asset prices, faster credit creation, and eventually higher inflation. The precise transmission mechanism varies from cycle to cycle. The underlying arithmetic does not.

This is where the budget becomes relevant.The debate over whether the budget is expansionary misses the point. Aggregate fiscal policy remains constrained by IMF commitments, while development spending continues to face pressure. Yet aggregate fiscal restraint and marginal demand impulses are not the same thing. Tax relief, transfers, and other measures that increase disposable income may not fundamentally alter the fiscal picture, but they nevertheless operate in one direction.

Ordinarily, such measures would not be particularly noteworthy. The complication is one of timing.These developments are emerging after nearly three years of stabilization. Economic growth remains weak by historical standards, investment remains subdued, and development spending has yet to recover meaningfully. At the same time, pressures for normalization are building across the economy. Businesses want stronger demand; households want income growth; provinces want greater fiscal space; and industries operating below capacity want relief. Unsurprisingly, the demands for wage increases, public spending, infrastructure investment, housing activity, and credit expansion are becoming louder as well.

Politicians are not immune to these pressures. The current government is now beyond the midpoint of its term, and the incentives that dominate the second half of a political cycle are rarely the same as those that dominate the first. Stabilization may have been the priority during the opening years; growth, jobs, incomes, housing, and development increasingly become the priorities thereafter.

None of this implies an imminent abandonment of fiscal discipline. It does, however, suggest that the balance of pressure is beginning to shift.

For monetary policymakers, that shift matters. Inflation expectations are rarely tested during periods of adjustment, when weak demand and tight financial conditions do much of the central bank’s work. They are tested during recovery, when policymakers are simultaneously being asked to support growth, accommodate political demands, and preserve price stability.

A central bank can accommodate temporary supply shocks. It can look through one-off increases in energy prices, indirect taxes, or commodity prices. What it cannot afford is a situation in which households, businesses, and investors begin assuming that inflation will remain above target because monetary and financial conditions no longer appear consistent with the target itself.That is ultimately how inflation cycles begin.

They rarely begin because oil prices rise. Rather, they emerge when temporary price shocks occur in an environment where liquidity is expanding, financial conditions are easing, demand is recovering, and economic agents begin assuming that inflation will remain elevated. At that point, inflation ceases to be merely a supply-side phenomenon and becomes an expectations problem.

The issue facing policymakers today is therefore not whether inflation is demand-driven. The issue is whether current monetary conditions are consistent with inflation returning sustainably to the target range.

Broad money growth in the mid-teens. Currency growth approaching 20 percent. Narrowing spreads between policy and market rates. Recovering imports. Stabilizing economic activity. A modest fiscal demand impulse. Growing pressure for economic recovery. An approaching political cycle.

Individually, none of these developments are alarming. Collectively, however, they are difficult to reconcile with the assumption that inflation expectations remain perfectly anchored.

And that is ultimately the question confronting the MPC. Not whether inflation has risen. Nor whether oil prices have increased. But whether the conditions required to bring inflation sustainably back to the target range remain firmly in place.

Comments