Gharibwal Cement Limited (PSX: GWLC) was incorporated in Pakistan as public limited company in 1960. The principal activity of the company is the manufacturing and sale of cement.

Pattern of Shareholding

As of June 30, 2025, GWLC has a total of 400.274 million shares outstanding which are held by 5223 shareholders.

Directors, CEO, their spouse and minor children have the majority stake of 85.066 percent in the company followed by local general public holding 6.57 percent shares.

Around 5.10 percent of GWLC’s shares are held by executives, 1.53 percent by joint stock companies and 1.02 percent by foreign companies. The remaining shares are held by other categories of shareholders.

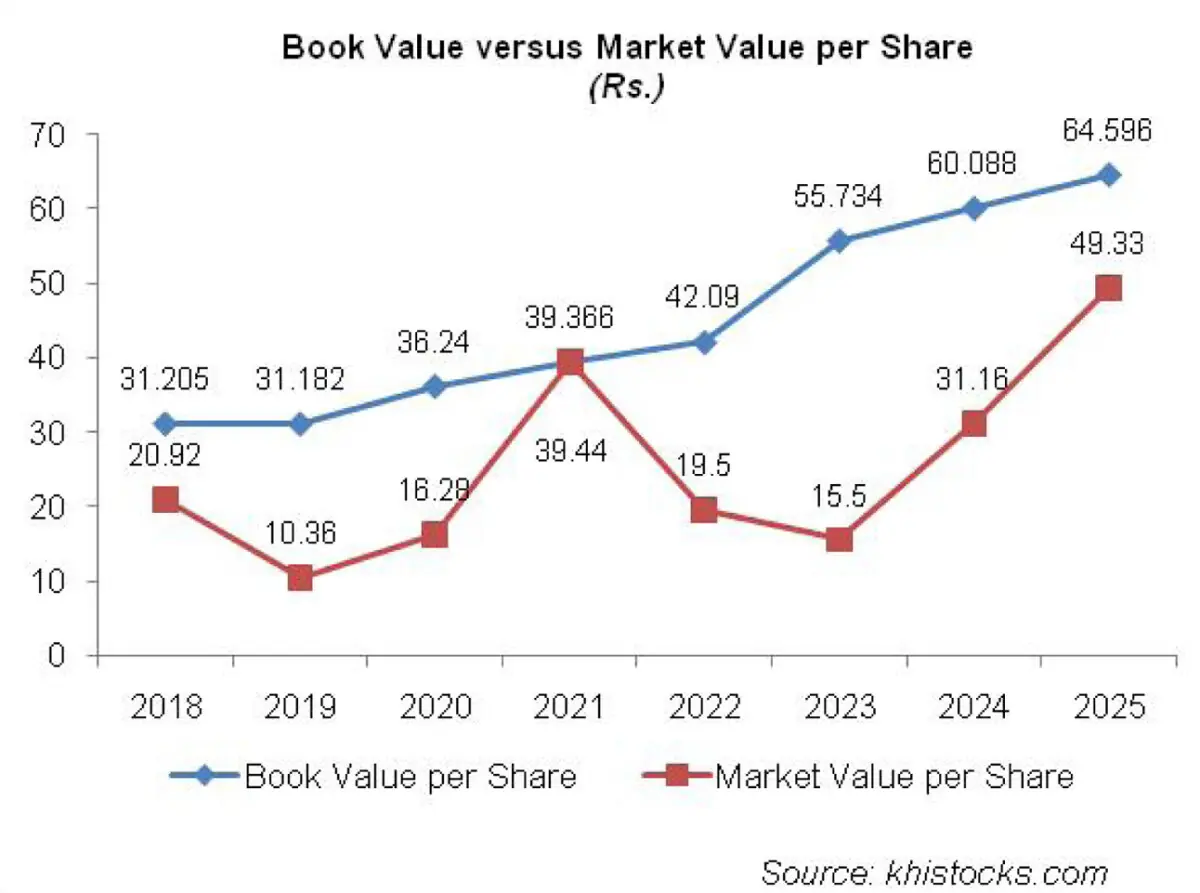

Historical Performance (2019-25)

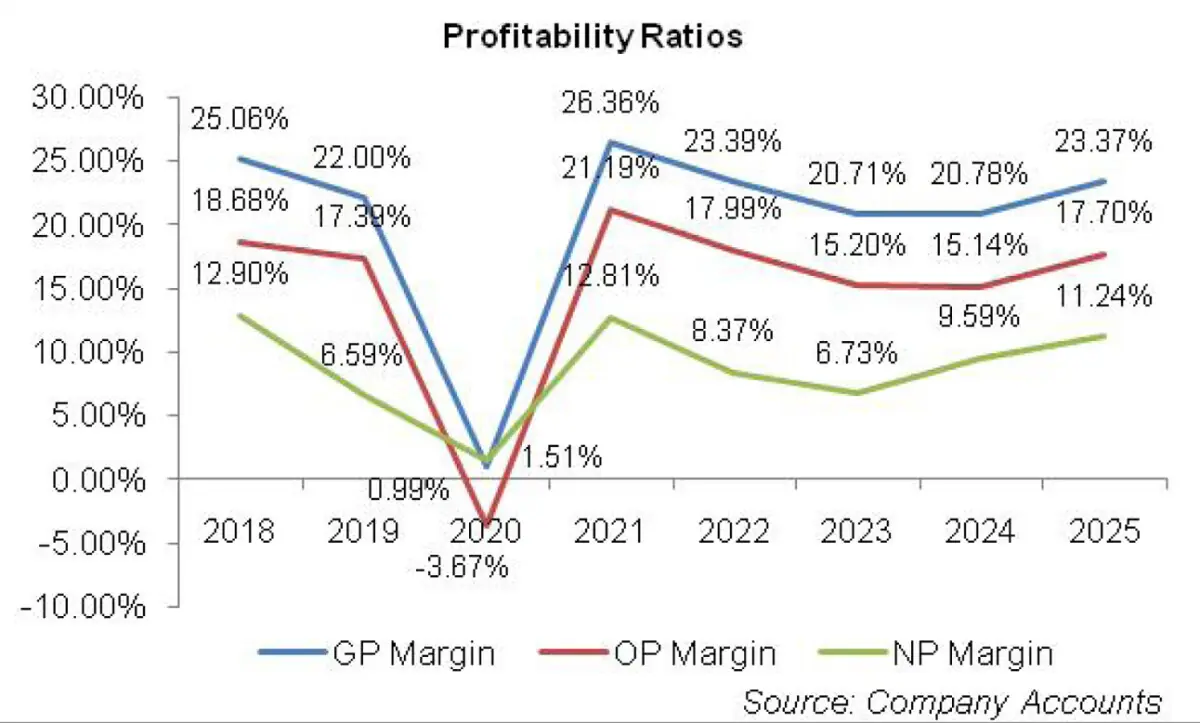

GWLC’s topline posted year-on-year plunge in 2019, 2020 and 2024. Conversely, its bottomline dwindled in all the years under consideration except in 2021, 2024 and 2025. The company’s margins drastically fell in 2019 and 2020 followed by a staggering rebound in 2021.

In the next two years, GWLC’s margins took a slide. In 2024, gross and operating margins largely stayed intact, however, net margin significantly picked up. In 2025, all the margins posted year-on-year growth (see the graph of profitability ratios). The detailed performance review of the period under consideration is given below.

In 2019, GWLC’s topline ticked down by 4.53 percent to clock in at Rs.11,174.33 million. This came on the back of 11.4 percent decrease in the cement dispatches which clocked in at 1.676 million tons in 2019.

The decline in sales volume was on the back of lackluster economic activity in the local market and a drastic decline in the company’s exports due to Pakistan-India border tensions.

High cost of raw materials particularly fuel and electricity charges coupled with Pak Rupee depreciation resulted in 16.16 percent downtick recorded in the company gross profit in 2019. GP margin also fell from 25 percent in 2018 to 22 percent in 2019 despite an increase recorded in the average selling price.

Lower sales volume resulted in 87 percent plunge in distribution expense in 2019. Administrative expense also plummeted by 1.63 percent in 2019 due to lower vehicle running & travelling charges as well as legal & professional charges. Payroll expense continued to enlarge during the year on the back of inflationary pressure and workforce enhancement from 420 employees in 2018 to 427 employees in 2019.

Other income deteriorated by 61 percent in 2019 as the company booked reversal on provision of doubtful debt and slow moving stores & spares in the previous year.

Lower profit related provisioning done during the year pushed down other expense by 12.84 percent in 2019. GWLC recorded 11.15 percent drop in its operating profit in 2019 with OP margin clocking in at 17.39 percent versus OP margin of 18.68 percent recorded in the previous year.

Finance cost mounted by 39.66 percent in 2019 due to higher discount rate. This was despite the fact that the company settled a significant portion of its outstanding liabilities in 2019. This brought down its gearing ratio from 25 percent in 2018 to 22 percent in 2019.

Net profit tapered off by 51.22 percent to clock in at Rs.736.41 million. This translated into EPS of Rs.1.84 in 2019 versus EPS of Rs.3.77 percent registered in 2018. NP margin also thinned down from 12.90 percent in 2018 to 6.59 percent in 2019.

GWLC recorded 22 percent year-on-year decline in its topline which clocked in at Rs.8714.09 million in 2020. Sales volume dropped by 1 percent to clock in at 1.659 million tons in 2020. This was due to the outbreak of COVID-19 in the last quarter of FY20.

GWLC made on export sales in 2020. During the year, average selling price of cement also fell by 21 percent which put a dent on the net sales of GWLC. During the year, the government of Punjab increased the rate of royalty on raw materials.

This coupled with elevated raw materials, packing materials and fuel charges alongside Pak Rupee depreciation wreaked havoc on the gross profit of the company which sank by 96.49 percent in 2020.

GP margin fell to its lowest ebb of 1 percent in 2020. 31 percent decline in distribution expense in 2020 signifies lower sales volume. Administrative expense also slid by 11.82 percent in 2020 primarily due to lower sales volume as the company streamlined its workforce to 382 employees.

Other income deteriorated by 28.68 percent in 2020 due to lower rental income received from Baluchistan Glass Limited (a related party).

No provisioning done for WWF and WPPF pushed down other expense by 51.13 percent in 2020. GWLC recorded operating loss of Rs.319.43 million in 2020. Finance cost narrowed down by 57 percent in 2020 due to lesser borrowings and the onset of monetary easing in the COVID quarter.

Gearing ratio fell to 16 percent in 2020. The realization of deferred tax assets during the year transformed loss-before-tax of Rs.561.69 million into net profit of Rs.131.32 million in 2020, down 82.17 percent year-on-year. This culminated into EPS of Rs.0.33 and NP margin of 1.51 percent.

After two successive years of posting decline in net sales, 2021 brought merry times for GWLC.

During the year, its topline posted a phenomenal year-on-year growth of 38.94 percent to clock in at Rs.12,106.99 million. This came on the back of 7.1 percent uptick in the company’s dispatches which clocked in at 1.78 million tons. Increase in selling prices also played a pivotal role in driving up the net sales. This coupled with reduction in energy prices during the year pushed up gross profit by an unparalleled rate of 3599 percent.

GP margin also attained its optimum level of 26.36 percent in 2021. Distribution expense mounted by 176.76 percent in 2021 on account of higher salaries of sales force.

Administrative expense escalated by 18.68 percent in 2021 due to inflationary pressure and hiring of additional employees which took its workforce to 395 employees.

GWLC didn’t record any other income in 2021 as no rental income was received from its related party Baluchistan Glass Limited. Conversely, other expense magnified by 213.44 percent in 2021 due to hefty provisioning done for WWF and WPPF. Operating profit clocked in at an unprecedented level of Rs.2,565.34 million in 2021 with OP margin clocking in at 21.19 percent.

Despite monetary easing and lesser borrowings, net finance cost multiplied by 14.44 percent in 2021. This was due to lower finance income recognized during the year as GWLC booked reversal of late payment surcharge on GIDC in the previous year. Gearing ratio fell to 8 percent in 2021.

Net profit strengthened by 1081.40 percent to clock in at Rs.1551.38 million in 2021. EPS was recorded at Rs.3.88 and NP margin at 12.81 percent in 2021.

In 2022, GWLC’s net sales mounted by 33.76 percent to clock in at Rs.16,193.79 million. This was due to higher prices of cement while there was 5.2 percent dip in the company’s dispatches which clocked in at 1.683 million tons in 2022.

Deteriorating macroeconomic indicators resulted in a slowdown in construction and infrastructure related activities in the country, resulting in low demand of cement. Pak Rupee depreciation as well as higher fuel and power cost drove the cost of sales up by 39.15 percent in 2022.

Gross profit grew by 18.69 percent in 2022, however, GP margin fell to 23.39 percent. Distribution expense posted 33.40 percent increase in 2022 on the back of market induced rise in the salaries of sales forces.

Administrative expense mounted by 62.72 percent in 2022 on account of higher payroll expense. This was due to inflationary pressure while the company squeezed its workforce to 393 employees in 2022.

During the year, the company sold a property (a piece of land) on gain, resulting in other income of Rs.60.93 million. Other expense escalated by 24.40 percent in 2022 due to higher profit related provisioning done during the year.

Operating profit picked up by 13.56 percent in 2022, however, OP margin fell to 18 percent. Net finance cost slipped by 42.54 percent in 2022 due to considerable decline in outstanding borrowings. This brought down gearing ratio to 2 percent in 2022.

The imposition of 10 percent super tax during the year resulted in 12.68 percent diminution recorded in GWLC’s net profit which clocked in at Rs.1354.72 million in 2022. EPS ticked down to Rs.3.38 while NP margin also fell to 8.37 percent in 2022.

GWLC’s topline climbed up by 13.10 percent to clock in at Rs.18,315.89 million in 2023. Cement prices continued to soar, buttressing the company’s net sales. This was despite 19.80 percent downtick in GWLC’s dispatches which clocked in at 1.350 million tons in 2023.

Higher fuel & electricity charges, elevated rate of royalty on raw materials, Pak Rupee depreciation and higher indigenous inflation allowed the company to record a paltry 0.15 percent uptick in its gross profit in 2023.

GP margin also fell to 20.71 percent in 2023. While the company continued to rationalize its workforce which clocked in at 381 employees in 2023, inflation induced spike in salaries pushed up administrative expense by 11.15 percent in 2023.

Distribution expense also grew by 12.12 percent in 2023 due to higher salaries of sales force. High-base effect due to the sale of land in 2022 resulted in 98.95 percent decline in other income in 2023. Other expense also slid by 3 percent in 2023 due to lower profit related provisioning.

Operating profit narrowed down by 4.45 percent in 2023 with OP margin clocking in at 15.20 percent. Net finance cost plummeted by 55.11 percent in 2023 as the company recognized higher markup income on its bank deposits and on loan advanced to Baluchistan Glass Limited.

Conversely, its finance cost shrank due to settlement of substantial portion of its liabilities during the year. Gearing ratio was recorded at 0 percent in 2023 as the company’s cash & bank balances were higher than its total debt.

Net profit weakened by 9 percent to clock in at Rs.1232.41 million in 2023. This translated into EPS of Rs.3.08 and NP margin of 6.73 percent in 2023.

In 2024, the company’s dispatches fell by 11.6 percent to clock in at 1.19 million tons. While average selling price of cement continued to keep its chin up, GWLC couldn’t sustain its topline which dipped by 0.82 percent to clock in at Rs.18,165.08 million.

Elevated cement price during the year was able to absorb 12.1 percent increase in the cost of sales per ton and yielded a GP margin of 20.78 percent in 2024. Gross profit posted 0.50 percent dip in 2024. Lower sales volume pushed distribution expense down by 3.43 percent in 2024.

Conversely, administrative expense ticked up by 2.91 percent in 2024 due to inflationary pressure. Number of employees stood intact at 381 in 2024. Gain worth Rs.7.68 million recognized on the disposal of fixed assets resulted in 1101.41 percent growth in other income in 2024.

Other expense ticked up by 2.15 percent in 2024 due to higher profit related provisioning done during the year. Operating profit dipped by 1.21 percent in 2024 with OP margin clocking in at 15.14 percent, almost at the last year level.

GWLC recorded net finance income of Rs. 80.75 million in 2024 due to hefty dividend income and mark-up income on loan granted to Baluchistan Glass Limited which offset its finance cost. Gearing ratio clocked in at 3 percent in 2024 as the company obtained huge long-term loan to finance its capital expenditure.

GWLC installed 12 MW solar power plant in 2024 with an approval of additional 8 MW to be installed in 2025. Net profit built up by 41.41 percent to clock in at Rs.1742.73 million in 2024. This culminated into EPS of Rs.4.35 and NP margin of 9.59 percent in 2024.

In 2025, GWLC posted 8 percent uptick in its net sales which clocked in at Rs.19,620.35 million.

During, the year, the company’s sales volume posted a decent year-on-year growth of 2.3 percent to clock in at 1.22 million tons. This was despite the fact that the cement producers in the northern region collectively posted 2.6 percent decline their sales volume which clocked in at 30.726 million in 2025. This was due to demand destruction and liquidity constraints in the real-estate sector and subdued construction activity.

Cost of sales mounted by 4.47 percent in 2025 on the back of higher royalty on raw materials imposed by the Government of Punjab. However, the impact of royalty charges was greatly offset by energy efficiency achieved from the recently commissioned 12 MW solar plant which took GWLC’s total solar capacity to 24.5 MW.

Waste Heat Recovery plant as well as successful cooler retrofit project achieved during the year also contributed in cost saving in 2025. Gross profit picked up by 21.49 percent in 2025 with GP margin jumping up to 23.37 percent. Distribution expense stayed intact at the last year due to restricted sales promotion budget.

Administrative expense ticked up by 4.90 percent in 2025 due to higher payroll expense as well as elevated legal & professional charges.

GWLC streamlined its workforce from 381 employees in 2024 to 377 employees in 2025. Higher profit related provisioning drove other expense up by 26.82 percent in 2025. Other income also grew by 51.26 percent in 2025 due to superior gain recognized on the disposal of fixed assets.

GWLC’s operating profit posted 26.27 percent growth in 2025 with OP margin bouncing to 17.70 percent. Net finance income strengthened by 45.43 percent in 2025 due to superior capital gain, profit on bank deposits and commission on LG for Baluchistan Glass Limited/During the year, the company’s short-term investments and loan granted to related parties significantly increased which bolstered its finance income.

Net profit mounted by 26.51 percent to clock in at Rs.2204.74 million in 2025. This translated into EPS of Rs.5.51 and NP margin of 11.24 percent in 2025.

Recent Performance (9MFY26)

During the nine month period of the ongoing fiscal year, GWLC’s net sales strengthened by 11.79 percent to clock in at Rs.16,511.82 million. This was on the back of 18.20 percent greater sales volume to the tune of 1.083 million tons achieved during the period. The effect of volumetric growth was partially offset by 5.4 percent slump in selling prices.

Cost control achieved on the back of solar power generation and higher capacity utilization resulted in 21.54 percent stronger gross profit in 9MFY26 with GP margin clocking in at 20.12 percent versus GP margin of 18.51 percent achieved in 9MFY25.

Distribution expense ticked down by 18 percent in 9MFY26 likely due to a decline in promotional budget. Administrative expense surged by 11.46 percent in 9MFY26 due to inflationary pressure.

High base effect provided by the disposal of fixed assets in the previous year resulted in 69 percent thinner other income registered in 9MFY26. Conversely, higher profit related provisioning continued to drive other expense up in 9MFY26. GWLC posted 23.86 percent higher operating profit in 9MFY26 with OP margin clocking in at 15 percent versus OP margin of 13.59 percent recorded in 9MFY25.

While finance expense ticked down in 9MFY26 due to monetary easing, finance income continued to thrive, resulting in net finance income of Rs.212.37 million in 9MFY26, up 165.20 percent year-on-year.

Increased short-term investment in mutual funds was the reason for the superior finance income recognized during the period. GWLC registered net profit of Rs.1752.287 million in 9MFY26, up 39.34 percent year-on-year. This translated into EPS of Rs.4.38 and NP margin of 10.61 percent in 9MFY26 versus EPS of Rs. 3.14 and NP margin of 8.51 percent posted in 9MFY25.

Future Outlook

Going forward, government policies to boost construction and real estate sectors will boost the demand, resulting in robust performance of cement sector. GWLC is aggressively working on cost effective alternative energy solution to cut down its energy cost. This coupled with cooler replacement project and BMR of its production lines will boost the operational efficiency and reduce the cost.

GWLC should also focus on export sales to utilize its idle capacity, cover its fixed cost, hedge against its import and improve its margins and profitability.

Comments