Mixed signals from commercial banks’ forex liquidity

While commercial banks show no immediate foreign currency stress, the private FX cushion is no longer improving, and rising external risks suggest a weakening bias for the rupee.

- FE-25 foreign currency deposits and trade finance trends.

- Rising external sector risks from geopolitical events.

- Implications for the rupee and central bank's management tools.

The latest FE-25 statistics from the central bank do not indicate immediate stress in the commercial banking system’s foreign currency position. However, it does show that the private FX cushion has stopped improving at a time when external sector risks are rising again. This is the more important signal.

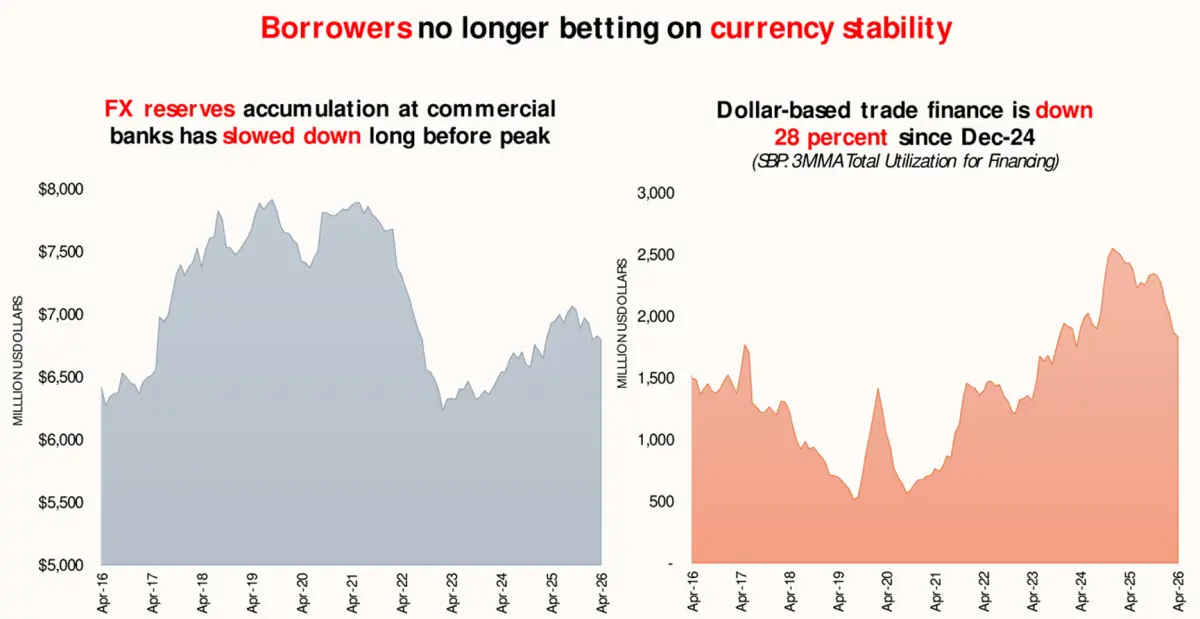

FE-25 deposits stood at approximately $6.8 billion in April 2026, compared to the latest peak of around $7.1 billion in September 2025. This represents a decline of about 3.8 percent from peak. On absolute levels, the position remains broadly intact. There is no evidence of a sharp drawdown or panic conversion out of commercial-bank foreign currency deposits. However, the relative movement is mildly adverse. The system still has a dollar cushion, but that cushion is no longer thickening.

This distinction is critical. SBP reserves reflect the state’s external buffer. FX liquidity held with commercial banks reflects the market-facing buffer. It captures depositor confidence, exporter conversion behavior, importer financing demand, and the banking system’s ability and willingness to intermediate foreign currency liquidity. A stable level offers comfort. A weakening trend reduces that comfort.

The trade-finance picture is also mixed. FE-25 export financing declined to approximately $872 million in April 2026, down from its recent peak of about $1.04 billion in November 2025. This is a decline of nearly 16 percent. Import financing stood at around $961 million, still well below its December 2024 peak of about $1.63 billion, but showing a slight increase over the previous month. Overall FE-25 trade finance remains around 28 percent below its late-2024 peak.

In normal conditions, lower trade-finance utilization may be read as lower pressure. In current conditions, the interpretation is less straightforward. It may indicate lower import demand, but it may also reflect caution by banks, or reduced appetite for FCY intermediation. The slight uptick in import financing in April therefore needs to be watched closely.

The external backdrop has become materially less benign. The Iran-US war and extended Gulf crisis have widened the pressure channels facing Pakistan. The risk is no longer limited to oil prices. It extends to LNG availability, freight costs, insurance premia, fertilizer imports, shipping delays, remittance sentiment, importer front-loading, and exchange-rate expectations. These pressures are emerging at a time when goods exports remain weak, services exports are improving but still insufficient, and remittances continue to carry much of the current account.

The short-term currency outlook is therefore not one of immediate disorder, but of a weakening bias. The April data does not justify panic. It does justify caution. If commercial-bank FX balances continue to drift down while import financing begins to rise, the pressure is likely to appear first in forward premia and importer behavior, before moving into the spot market. SBP can use reserves, interest rates, and administrative tools to manage the adjustment, but those tools cannot permanently replace private FX confidence.

The latest reading is clear: no rupture yet, but the direction has turned mildly bearish for the rupee. The private FX buffer remains present, but its momentum is fading just as the external shock is broadening.

Comments